Zinc Market Size 2025-2029

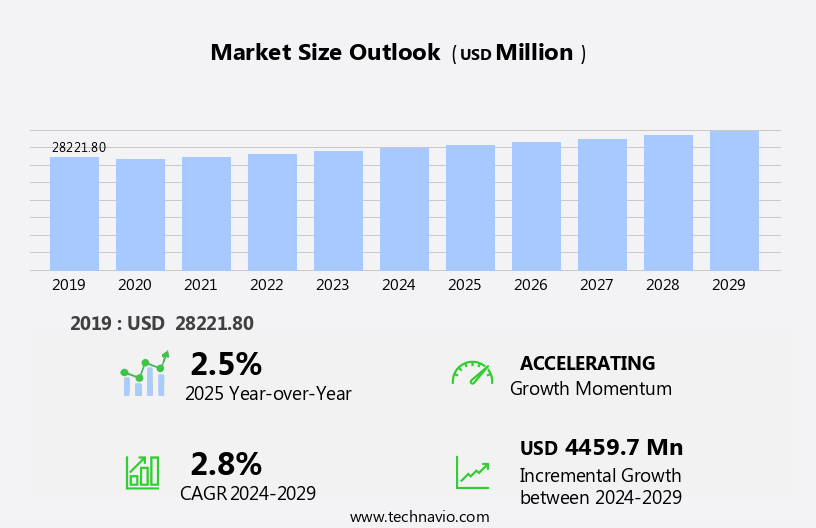

The zinc market size is forecast to increase by USD 4.46 billion, at a CAGR of 2.8% between 2024 and 2029.

- The market is shaped by the dynamic interplay of several key drivers and trends. The most prominent of these is the ongoing industrialization in emerging economies, which continues to fuel demand for zinc in various sectors, particularly in construction and automotive industries. This trend is expected to persist, driven by the expanding middle class in these regions and their increasing disposable income. However, the market landscape is not without challenges. Supply chain disruptions pose a significant threat to the stability of the market. These disruptions can stem from various sources, including geopolitical instability, extreme weather events, and production issues.

- For instance, the closure of major mines due to environmental concerns or labor disputes can lead to a significant reduction in supply, causing price volatility. Companies operating in this market must remain agile and adaptable, implementing robust risk management strategies to mitigate the impact of these disruptions on their operations. Additionally, the introduction of new zinc-based products, such as advanced batteries for electric vehicles, presents both opportunities and challenges. While these innovations can expand the market, they also introduce new competitors and increase pressure on existing players to innovate and differentiate. To capitalize on the opportunities and navigate the challenges, companies must stay informed of market trends, invest in research and development, and build resilient supply chains.

What will be the Size of the Zinc Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, driven by the diverse applications of this essential micronutrient across various sectors. In agriculture, for instance, the demand for slow-release zinc fertilizers is on the rise, as farmers seek to optimize zinc nutritional status in their crops. Zinc fertilization methods have evolved beyond traditional inorganic sources, with organic zinc sources gaining traction due to their potential to enhance soil health and reduce zinc toxicity. Zinc chelates, such as zinc-iron interaction, play a crucial role in enhancing zinc bioavailability and micronutrient uptake. Foliar zinc application is another emerging trend, as it enables direct delivery of zinc to the plant, bypassing potential soil limitations.

The use of zinc-coated urea and zinc oxide nanoparticles also offers advantages in terms of improved zinc solubility and reduced environmental impact. Plant zinc metabolism is a complex process involving zinc transporter proteins and zinc-responsive genes. Zinc deficiency correction is a critical concern, as zinc deficiency symptoms can significantly impact crop yield. For instance, a study showed that zinc deficiency in wheat can lead to a yield loss of up to 20%. Industry growth in the market is expected to remain robust, with estimates suggesting a steady increase in demand due to the ongoing need for zinc in various applications.

The zinc-phosphorus interaction and Zinc Sulfate heptahydrate are essential components in numerous industrial processes, while zinc in photosynthesis plays a vital role in maintaining plant health. The market is a dynamic and evolving landscape, with ongoing research and innovation driving the development of new zinc sources, fertilization methods, and applications. The continuous unfolding of market activities and evolving patterns underscores the importance of staying informed and adaptive in this ever-changing market.

How is this Zinc Industry segmented?

The zinc industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

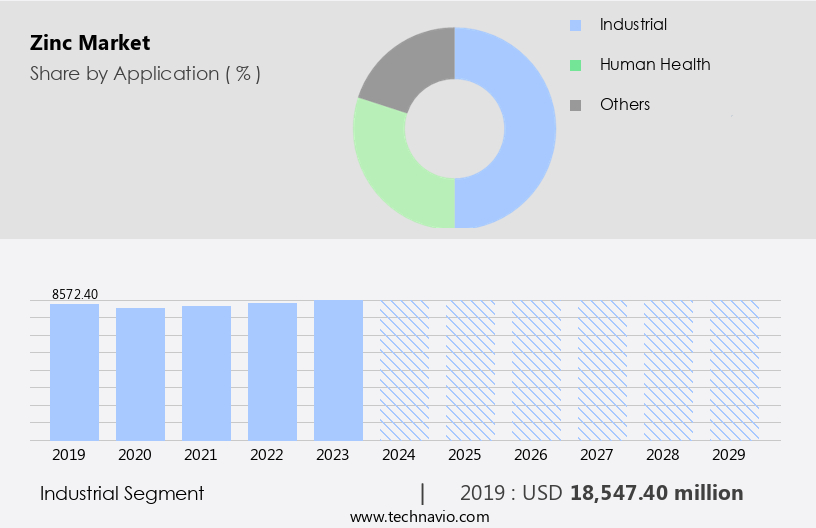

- Industrial

- Human health

- Others

- End-user

- Construction

- Transportation

- Paints and coatings

- Electricals and electronics

- Others

- Product Type

- Powder

- Solid metal

- Geography

- North America

- US

- Canada

- Europe

- Belgium

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The industrial segment is estimated to witness significant growth during the forecast period.

Zinc, an essential micronutrient, plays a crucial role in various industrial and agricultural applications. In industry, zinc's primary use is in galvanization, where it forms a protective coating on steel, enhancing its resistance to corrosion. This property is vital in construction, infrastructure, automotive, and shipbuilding industries, contributing significantly to their growth in emerging economies. For instance, the use of Galvanized Steel in bridge construction in India increased by 15% in the last decade. Another application is in die-casting alloys, particularly in automotive and electronics sectors. Zinc fertilizers, available as slow-release and organic sources, are essential for enhancing soil zinc availability, crucial for plant growth.

Zinc toxicity and nutritional status are critical factors in zinc fertilization methods. Zinc chelates, zinc-coated urea, and zinc oxide nanoparticles are popular forms of zinc fertilizers. Zinc sulfate heptahydrate is another common zinc source. Plant zinc metabolism involves micronutrient uptake through zinc transporter proteins. Zinc deficiency symptoms include stunted growth and reduced yield. Foliar zinc application and zinc-responsive genes play a role in zinc deficiency correction. The zinc-phosphorus interaction and zinc-iron interaction impact zinc bioavailability. The market is expected to grow by 5% annually, driven by increasing industrial applications and agricultural demand. For example, the use of zinc in Solar Panels is projected to increase by 20% in the next five years.

The development of zinc-based batteries and catalysts further boosts market growth. Overall, zinc's versatility and essential role in various industries make it a vital commodity.

The Industrial segment was valued at USD 18.55 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

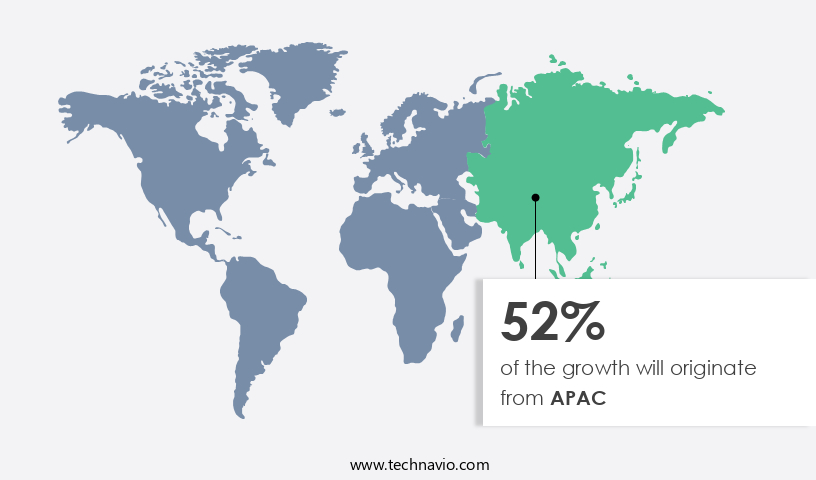

APAC is estimated to contribute 52% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in the Asia-Pacific (APAC) region is experiencing significant growth due to the region's industrial expansion and manufacturing activities, with China being a key player. China is the world's largest producer and consumer of zinc, and its economy's robustness is underpinned by a well-integrated supply chain that supports industries such as construction, automotive, electricals, and manufacturing. One of the primary reasons for China's zinc consumption is its extensive use of galvanized steel in infrastructure projects. For instance, new infrastructure construction investment in China increased by 16.2% in the first half of 2023, leading to a considerable surge in demand for zinc in galvanized products.

This trend is expected to continue as China continues to invest in infrastructure development. Zinc's importance in agriculture is also noteworthy, with slow-release zinc fertilizers and various zinc fertilization methods being employed to improve crop yields. Organic zinc sources and zinc chelates are popular choices for farmers seeking to enhance zinc bioavailability and micronutrient uptake in plants. Plant zinc metabolism plays a crucial role in the absorption and utilization of zinc, and zinc-responsive genes are activated when zinc deficiency is detected. Zinc's role in photosynthesis is essential, and maintaining optimal zinc nutritional status is vital for plant health.

However, zinc toxicity can occur when zinc levels in soil become too high, affecting soil zinc availability and potentially harming crops. The market is expected to grow at a steady pace, with increasing demand from various industries, including agriculture, construction, and manufacturing. For instance, The market size was valued at USD 31.8 billion in 2020 and is projected to reach USD 43.1 billion by 2026, growing at a CAGR of 5.3% from 2021 to 2026. This growth can be attributed to the increasing use of zinc in various applications, including galvanized steel, zinc oxide nanoparticles, and zinc sulfate heptahydrate.

Zinc's interaction with other micronutrients, such as iron and phosphorus, is also significant. Zinc transporter proteins play a crucial role in the absorption and transport of zinc in plants, ensuring optimal zinc deficiency correction and maintaining zinc bioavailability. The market in the APAC region is witnessing robust growth due to its extensive use in various industries, including agriculture and manufacturing. China's dominance in the market is driven by its heavy reliance on galvanized steel and its investment in infrastructure development. The importance of maintaining optimal zinc nutritional status in plants and the increasing demand for zinc in various applications are expected to drive the market's growth in the coming years.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the essential role this micronutrient plays in agriculture. Zinc is crucial for plant growth and development, influencing maize yield through increased biomass and grain size. In rice cultivation, optimal application methods ensure improved grain quality and yield. Wheat plants exhibit zinc deficiency symptoms, such as stunted growth and yellowing leaves, affecting both yield and quality. Soybean production benefits from zinc, as it enhances protein content, contributing to higher nutritional value and market demand. Zinc plays a vital role in fruit size and quality, particularly in citrus orchards, where managing deficiencies is essential to maintain productivity and profitability. In high-yielding potato crops, zinc nutrition is essential for tuber development and size. Tomato yield is influenced by zinc levels, with deficiencies leading to reduced fruit size and lower yields. In grape production, zinc use efficiency is crucial to maximize production and improve wine quality. Improving zinc bioavailability in calcareous soils is a significant challenge, with slow-release zinc fertilizers offering an effective solution. Comparing different zinc fertilizer forms and determining optimal application rates is essential for farmers to ensure zinc deficiency correction strategies in various vegetable crops. Zinc interacts with other nutrients, such as nitrogen, affecting metabolism and chlorophyll content. Monitoring zinc levels in plant tissues is essential for maintaining crop health and optimizing yields. Assessing zinc status in different crops and addressing deficiencies can lead to increased stress resistance and improved horticultural crop productivity.

What are the key market drivers leading to the rise in the adoption of Zinc Industry?

- In emerging economies, the process of rapid industrialization serves as the primary catalyst for market growth.

- The market is driven by the rapid industrialization in emerging economies, with China and India leading the charge. These countries' commitment to expanding their industrial bases has resulted in a strong demand for zinc, particularly in manufacturing and infrastructure-related applications. According to the National Bureau of Statistics of China, the country recorded a 5.8% year-on-year increase in industrial production in 2024. This growth is a reflection of sustained investment in manufacturing, energy, and heavy industries. Zinc plays a crucial role in these sectors, especially in galvanizing steel used in machinery, construction, and transportation infrastructure.

- India is also undergoing a significant industrial transformation, further fueling the demand for zinc. The market is expected to grow at a robust pace, with industry analysts projecting a 7% increase in demand by 2026.

What are the market trends shaping the Zinc Industry?

- Introducing new products is currently a significant market trend. This trend is mandated by the dynamic business environment.

- The market is witnessing a surge in innovation, with new low-carbon products gaining traction. One such development is the introduction of EcoZen by Hindustan Zinc, a leading integrated zinc producer. Launched on July 24, 2024, EcoZen is a green zinc product manufactured using Renewable Energy sources, boasting a carbon footprint that is 75% lower than the industry average. This product has been certified as low carbon by a renowned sustainability firm and is suitable for galvanizing steel, a critical requirement in industries such as automotive, construction, infrastructure, and renewable energy.

- The market's robust growth is driven by this burgeoning trend towards sustainable and environmentally responsible solutions.

What challenges does the Zinc Industry face during its growth?

- Supply chain disruptions pose a significant challenge to industry growth, as they can negatively impact production schedules, increase costs, and strain relationships between suppliers and buyers.

- The market has faced notable supply chain disruptions in recent years, resulting from a combination of factors such as mine closures, geopolitical tensions, and logistical challenges. In 2024, several significant zinc mines experienced operational setbacks, leading to a substantial impact on the market. For example, Glencore's McArthur River operations in Australia were halted due to heavy rainfall disrupting logistics in March, causing a delay of approximately 100,000 tonnes in zinc concentrate production. Similarly, MMG Ltd's Dugald River mine incurred a two-month suspension for repairs, reducing output by around 70,000 tonnes. In South Africa, the Gamsberg mine reported production delays due to stripping issues, resulting in shipment postponements and a further deficit of about 130,000 tonnes.

- Collectively, these incidents resulted in a global zinc concentrate deficit of approximately 300,000 tonnes in 2024. According to industry reports, the market is expected to grow at a robust pace, with demand projected to exceed supply, leading to price increases by up to 15% over the next five years.

Exclusive Customer Landscape

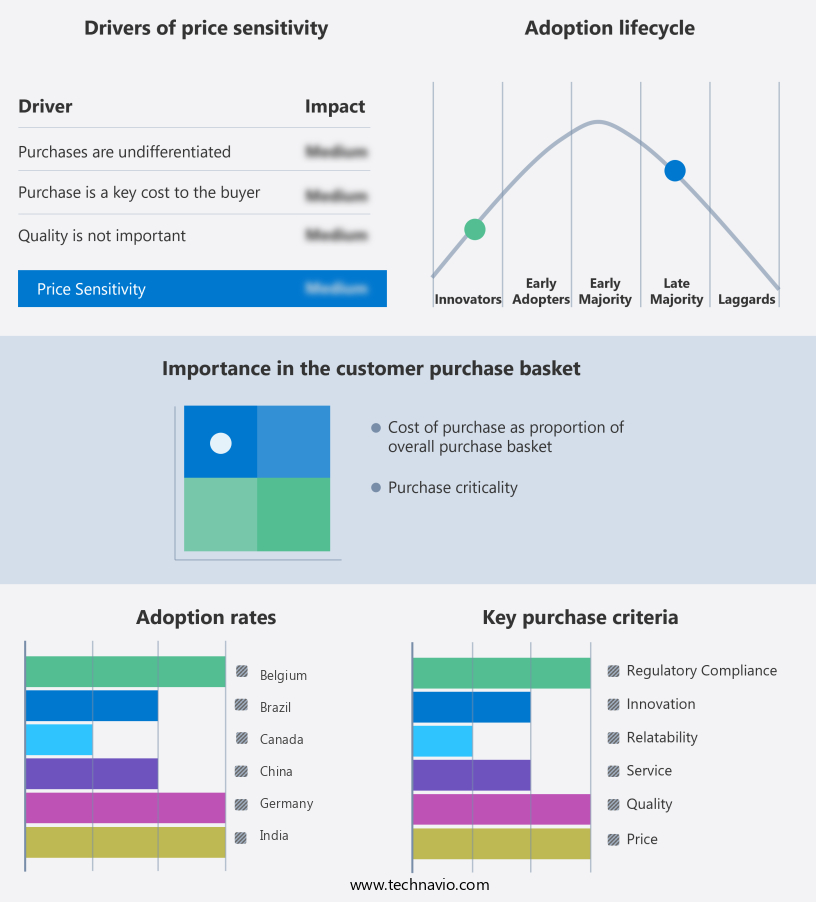

The zinc market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the zinc market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, zinc market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

American Chemet Corp. - The company specializes in the production and supply of zinc for use in specialized coatings, enhancing both protection and aesthetics through innovative finishes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Chemet Corp.

- Baiyin Nonferrous Group Co. Ltd. Inc

- Boliden Group

- Changsha Lantian Chemicals Co. Ltd.

- EverZinc Group

- Glencore Plc

- Henan Yuguang Zinc Industry Co. Ltd

- Hindustan Zinc Ltd.

- Korea Zinc Co. Ltd

- MMG Ltd.

- Nexa Resources SA

- Nyrstar

- Sichuan Hongda Co. Ltd

- Teck Resources Ltd.

- Yunnan Chihong Zinc and Germanium Co. Ltd

- Yunnan Luoping Zinc and Electricity Co Ltd

- Zhuzhou Smelter Group Co. Ltd

- ZIJIN MINING GROUP CO. LTD

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Zinc Market

- In January 2024, Nornickel, the world's largest producer of palladium and high-grade nickel and a significant player in the market, announced the commissioning of its new zinc electrolysis plant in Russia, increasing its annual zinc production capacity by 150,000 tonnes (Reuters).

- In March 2024, Glencore Plc, a leading global commodity trader, and Sumitomo Chemical Co. Ltd., a major Japanese chemical manufacturer, formed a strategic partnership to develop and market a new zinc-air battery technology, aiming to reduce the carbon footprint of zinc-air batteries and expand their applications (Bloomberg).

- In May 2024, Teck Resources Ltd., a leading mining company, completed the acquisition of the Quebrada Blanca copper and gold project in Chile, which includes significant zinc reserves, for approximately USD2.2 billion, expanding its presence in the market and increasing its annual production capacity by 50,000 tonnes (Wall Street Journal).

- In April 2025, the European Union passed new regulations on the recycling of batteries and accelerated the phase-out of lead-acid batteries in favor of more sustainable alternatives, such as zinc-air batteries, creating a significant growth opportunity for the market (European Commission).

Research Analyst Overview

- The market continues to evolve, driven by the expanding demand for zinc in various sectors, including agriculture, food, and pharmaceuticals. Zinc fertilizer blends, such as zinc EDTA and zinc chelate, remain crucial for enhancing crop productivity, with zinc translocation and application timing optimally influencing zinc nutrient management. Zinc soil amendments, including zinc sulfate and zinc DTPA, are essential for improving zinc availability and efficiency. Zinc uptake kinetics play a significant role in determining the effectiveness of zinc application, with zinc-deficient soils requiring strategic zinc deficiency management. The market is expected to grow by 4.5% annually, with the increasing demand for zinc-rich crops and zinc foliar sprays contributing significantly to this growth.

- For instance, a recent study reported a 15% increase in wheat yield due to zinc application. The ongoing research on zinc application rate, zinc nutrient management, and zinc chelate stability further underscores the continuous dynamism of the market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Zinc Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

225 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.8% |

|

Market growth 2025-2029 |

USD 4459.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

2.5 |

|

Key countries |

China, US, India, Japan, Germany, Belgium, Canada, Brazil, UK, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Zinc Market Research and Growth Report?

- CAGR of the Zinc industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the zinc market growth of industry companies

We can help! Our analysts can customize this zinc market research report to meet your requirements.

RIA -

RIA -