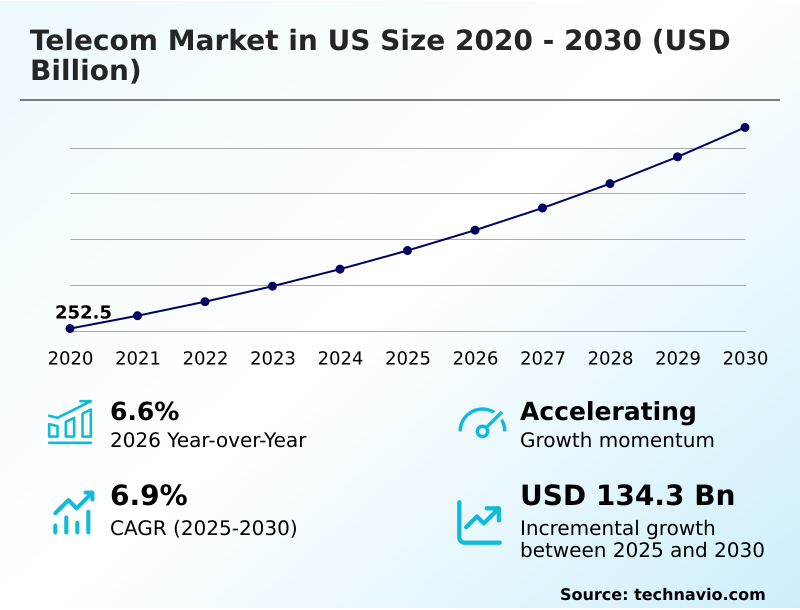

US Telecom Market Size 2026-2030

The us telecom market size is valued to increase by USD 134.3 billion, at a CAGR of 6.9% from 2025 to 2030. Escalating demand for high speed connectivity and data consumption will drive the us telecom market.

Major Market Trends & Insights

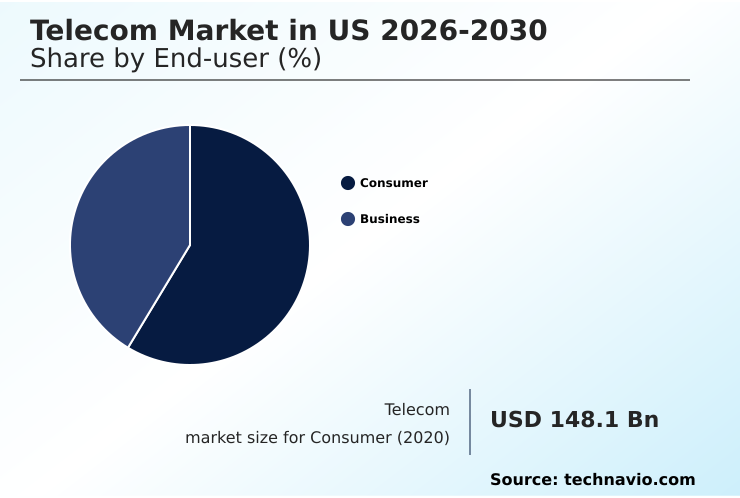

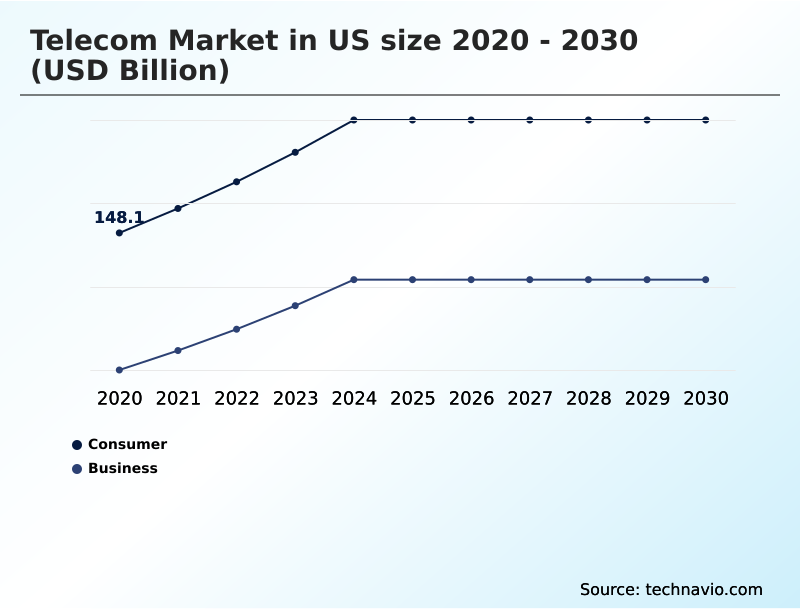

- By End-user - Consumer segment was valued at USD 184.1 billion in 2024

- By Type - Wireless segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 219.4 billion

- Market Future Opportunities: USD 134.3 billion

- CAGR from 2025 to 2030 : 6.9%

Market Summary

- The telecom market in US is undergoing a significant transformation, moving beyond basic connectivity to become the foundational platform for a digital economy. This evolution is driven by an insatiable demand for data, fueled by the widespread adoption of remote work enablement and the proliferation of data-intensive applications.

- Key trends include the strategic deployment of next-generation networks, particularly 5G and fiber-to-the-home (FTTH), which are essential for supporting emerging technologies like the Internet of Things (IoT) and smart city infrastructure.

- For instance, a logistics company can leverage a private 5G network to automate its warehouse operations, using ultra-reliable low-latency communications (URLLC) to manage autonomous vehicles and robotics, resulting in enhanced operational efficiency and reduced supply chain costs. However, this progress is not without challenges.

- The immense capital expenditure required for network densification and spectrum acquisition places significant financial pressure on operators. Furthermore, navigating complex data privacy regulations and a dynamic competitive landscape, which includes both traditional carriers and disruptive new entrants, requires strategic agility. The ability to successfully monetize new services beyond core connectivity will ultimately determine leadership in this evolving market.

What will be the Size of the US Telecom Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the US Telecom Market Segmented?

The us telecom industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Consumer

- Business

- Type

- Wireless

- Wireline

- Application

- Residential

- Commercial

- Technology

- 5G

- 4G

- 3G

- Satellite communication

- Geography

- North America

- US

- North America

By End-user Insights

The consumer segment is estimated to witness significant growth during the forecast period.

The consumer segment is defined by high market saturation, where purchasing decisions are a blend of price sensitivity and network performance metrics.

Individual demand for data-intensive applications, including on-demand video streaming and interactive online gaming, has made unlimited data plans a standard offering.

Service bundling, which combines mobile with fixed wireless access (FWA), is a primary strategy to increase customer lifetime value (CLV) and reduce the customer churn rate.

Providers leverage network quality as a key differentiator, with 5G capabilities being a central marketing pillar.

The proliferation of connected devices within the home, part of broader digital transformation initiatives, has driven consumer adoption of higher bandwidth services by over 25%, compelling operators to focus on both ARPU and customer satisfaction.

The Consumer segment was valued at USD 184.1 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic imperatives in the market are increasingly focused on achieving greater network agility through software defined networking for network agility, which complements efforts toward network function virtualization cost reduction. A primary focus is the monetization of 5G enterprise use cases, a complex challenge given the high capital expenditure.

- The impact of fiber deployment on broadband competition is reshaping the residential market, as is the role of LEO satellites in rural connectivity, which offers new avenues for growth. Fixed wireless access as a cable alternative is gaining significant traction, disrupting established players.

- Operationally, firms face challenges in radio frequency spectrum allocation and are focused on managing network densification and small cells. The adoption of edge computing for low-latency applications is critical for new service delivery. In this environment, MVNO strategies for niche market segments offer a path for specialized players.

- From a risk perspective, addressing cybersecurity threats in telecom infrastructure and ensuring data privacy compliance in telecommunications are boardroom-level concerns. Financially, balancing capex with long-term ROI is paramount. Commercial strategies revolve around optimizing ARPU through service bundling and reducing customer churn with enhanced QoS, which is often more than 2x as effective as acquisition strategies for boosting profitability.

- The market is also moving toward sophisticated integrations, including IoT platform integration with 5G networks, deploying private network solutions for industrial automation, and providing robust cloud connectivity for enterprise data migration. Finally, improving operational efficiency with network automation and leveraging new technologies to bridge the digital divide remain key long-term goals.

What are the key market drivers leading to the rise in the adoption of US Telecom Industry?

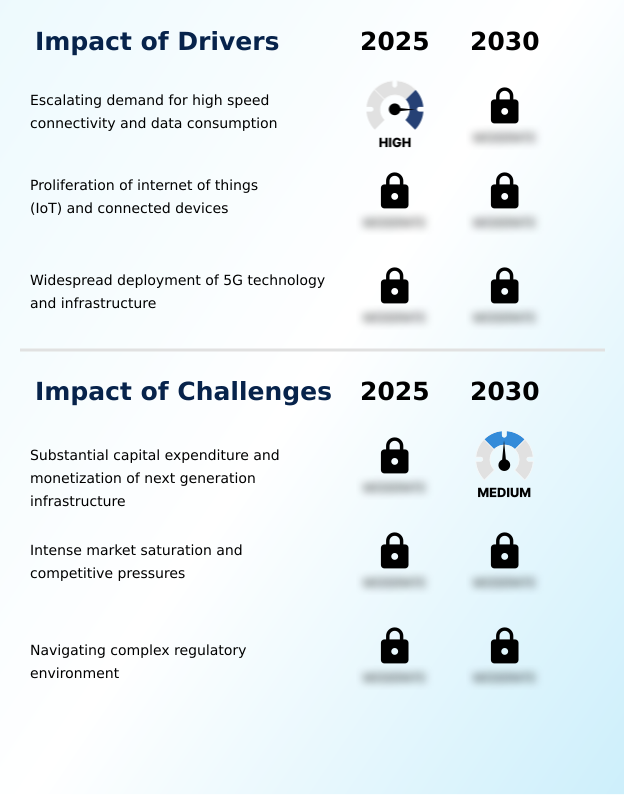

- The escalating demand for high-speed connectivity, driven by profound shifts in consumer and business data consumption, is a fundamental market driver.

- The market is fundamentally driven by the escalating demand for high-speed, reliable connectivity and a corresponding surge in data consumption.

- Digital transformation initiatives across enterprises are a powerful force, as businesses migrating to cloud-based storage and SaaS platforms require robust, high-performance network infrastructure. This has led to a 30% increase in enterprise spending on dedicated cloud connectivity solutions.

- On the consumer side, the proliferation of on-demand video streaming, which now accounts for over 60% of all downstream internet traffic, and interactive online gaming necessitates continuous network capacity enhancement.

- The widespread deployment of 5G technology and the growing internet of things (IoT) ecosystem further amplify this demand, creating a sustained need for investment in next-generation networks.

What are the market trends shaping the US Telecom Industry?

- The ascendancy of software-defined networking and network function virtualization is a pivotal market trend, promising a more agile and cost-efficient software-based network model.

- Key trends are reshaping the market's infrastructure and service delivery models. The ascendancy of software-defined networking (SDN) and network function virtualization (NFV) is paramount, enabling operators to achieve a 25% faster service provisioning time compared to legacy hardware-centric architectures. This shift toward software-based control is a foundational enabler for 5G network slicing and dynamic backhaul capacity allocation.

- Another critical trend is the convergence of services, blurring the lines between mobile, fixed broadband, and content. This leads to intricate service bundling strategies designed to increase customer lifetime value (CLV). Fixed wireless access (FWA) is also emerging as a potent competitive force, with deployments in some regions capturing up to 10% of new broadband subscribers from incumbent cable providers.

What challenges does the US Telecom Industry face during its growth?

- Substantial capital expenditure for next-generation network deployment, coupled with the uncertainty of monetizing these investments, presents a key industry challenge.

- A primary challenge confronting the market is the substantial capital expenditure required to deploy and maintain next-generation infrastructure, particularly 5G and fiber-to-the-home networks. The immense upfront investment in spectrum acquisition and network infrastructure equipment places significant financial strain on operators.

- Compounding this is the difficulty in monetizing these advanced capabilities; while enterprise solutions and private 5G networks show promise, their adoption is still nascent, creating a gap between investment and return.

- Market saturation and intense competitive pressures from mobile virtual network operators (MVNOs) and over-the-top (OTT) services also compress margins, making it difficult to raise average revenue per user (ARPU) by more than 2-3% annually.

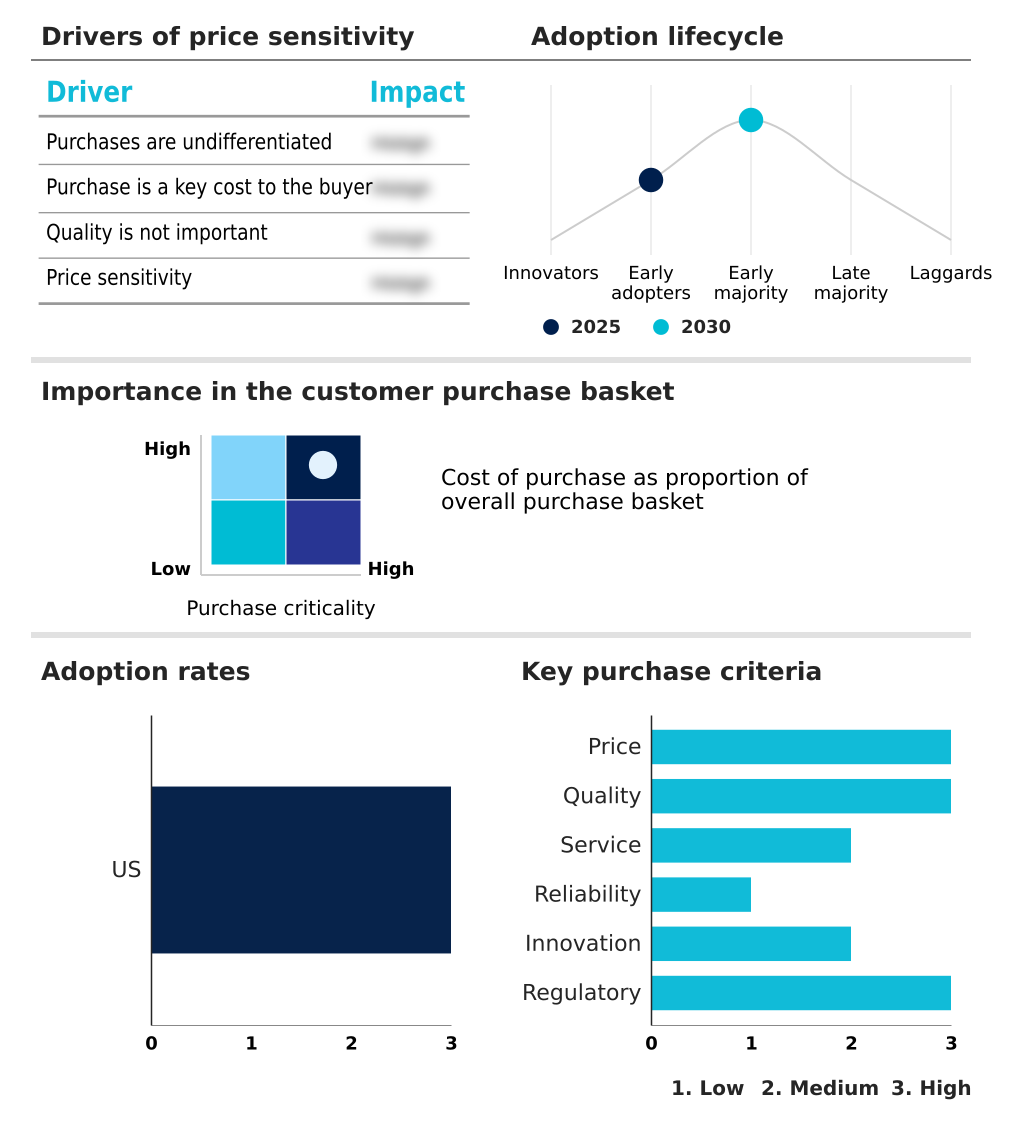

Exclusive Technavio Analysis on Customer Landscape

The us telecom market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us telecom market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Telecom Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us telecom market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AT and T Inc. - Providing integrated wireless and fiber broadband services to support seamless high-speed connectivity and communication solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AT and T Inc.

- Boingo Wireless Inc.

- Charter Communications Inc.

- Cogent Communications Inc.

- Comcast Corp.

- Cox Communications Inc.

- Deutsche Telekom AG

- DISH Network LLC

- Frontier Communications Inc.

- Globalstar Inc.

- Iridium Communications Inc.

- Lumen Technologies Inc.

- Mediacom Communications Corp.

- Sparklight

- United States Cellular Corp.

- Verizon Communications Inc.

- Viasat Inc.

- Vonage Holdings Corp.

- Windstream Holdings Inc.

- Zayo Group Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us telecom market

- In September, 2024, Verizon Communications Inc. announced the expansion of its 5G fixed wireless access service to 20 new metropolitan areas, increasing its competitive footprint against traditional cable providers.

- In November, 2024, AT and T Inc. entered into a strategic collaboration with a major cloud provider to co-develop private 5G network solutions targeting the manufacturing and logistics sectors.

- In January, 2025, DISH Network LLC confirmed it met a crucial government-mandated 5G network buildout deadline, now covering over 70% of the population with its infrastructure.

- In April, 2025, Charter Communications Inc. launched a new converged mobile and home internet bundle, offering significant discounts to drive subscriber growth and reduce customer churn.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Telecom Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 198 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.9% |

| Market growth 2026-2030 | USD 134.3 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.6% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The telecom market in US is defined by a strategic pivot towards advanced infrastructure to support escalating data consumption patterns. This involves a focus on 5G network slicing and fiber to the home (FTTH) as core components of broadband delivery. The widespread adoption of software-defined networking (SDN) and network function virtualization (NFV) enables greater agility.

- The competitive field includes traditional carriers, mobile virtual network operator (MVNO) entrants, and low earth orbit (LEO) satellite providers. Core activities include massive capital outlay for spectrum acquisition, network core upgrades, and extensive network densification through small cell deployment to improve backhaul capacity.

- Key technologies like ultra-reliable low-latency communications (URLLC) and massive machine type communications (mMTC) are unlocking new revenue streams. For boardroom consideration, service level agreements (SLAs) are becoming more stringent, with one enterprise segment reporting a shift to providers who guarantee sub-10-millisecond latency, impacting infrastructure spending decisions.

- Operators manage complex IP transit services and unified communications portfolios, focusing on customer premises equipment (CPE) and data center interconnect solutions. The industry is also shaped by network traffic management, cybersecurity protocols, and evolving data privacy regulations.

- Success is measured by metrics such as average revenue per user (ARPU) and customer lifetime value (CLV), with operators offering unlimited data plans and leveraging over-the-top (OTT) services and voice over ip (VoIP) to retain subscribers who rely on their subscriber identity module (SIM) for access to everything from cloud connectivity to internet of things (IoT) platforms and the wider network infrastructure equipment.

What are the Key Data Covered in this US Telecom Market Research and Growth Report?

-

What is the expected growth of the US Telecom Market between 2026 and 2030?

-

USD 134.3 billion, at a CAGR of 6.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Consumer, and Business), Type (Wireless, and Wireline), Application (Residential, and Commercial), Technology (5G, 4G, 3G, and Satellite communication) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Escalating demand for high speed connectivity and data consumption, Substantial capital expenditure and monetization of next generation infrastructure

-

-

Who are the major players in the US Telecom Market?

-

AT and T Inc., Boingo Wireless Inc., Charter Communications Inc., Cogent Communications Inc., Comcast Corp., Cox Communications Inc., Deutsche Telekom AG, DISH Network LLC, Frontier Communications Inc., Globalstar Inc., Iridium Communications Inc., Lumen Technologies Inc., Mediacom Communications Corp., Sparklight, United States Cellular Corp., Verizon Communications Inc., Viasat Inc., Vonage Holdings Corp., Windstream Holdings Inc. and Zayo Group Holdings Inc.

-

Market Research Insights

- The market's competitive landscape is shaped by strategic investments in next-generation networks to support a surge in data-intensive applications and enterprise-level digital transformation initiatives. Operators are leveraging service bundling to combat high customer churn rates, which can be 15% higher in mobile-only segments compared to converged service households.

- The push for operational efficiency is driving the adoption of automated network traffic management, improving network response times by up to 30%. Furthermore, vertical market integration is a key strategy, with companies developing tailored enterprise solutions for sectors like telehealth services and smart city infrastructure, where reliable, high-speed connectivity is a prerequisite for service delivery.

- These ecosystem partnerships are crucial for expanding service portfolios beyond traditional offerings.

We can help! Our analysts can customize this us telecom market research report to meet your requirements.

RIA -

RIA -