US Defense Market Size 2025-2029

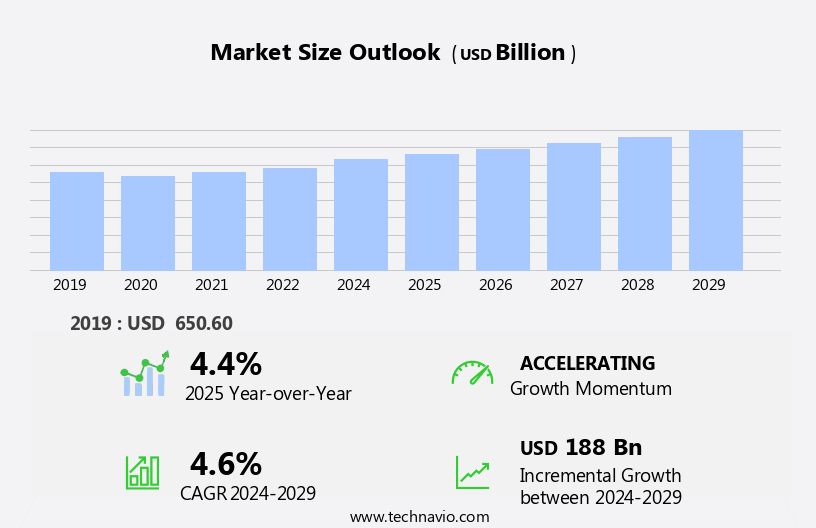

The US defense market size is forecast to increase by USD 188 billion at a CAGR of 4.6% between 2024 and 2029.

- The Defense Market is experiencing significant growth, driven by the increasing demand for advanced unmanned aerial vehicles in the US military. This trend is fueled by the need for enhanced surveillance, reconnaissance, and precision in defense operations. Furthermore, the defense industry is witnessing technological innovation, with advancements in areas such as artificial intelligence, cybersecurity, and autonomous systems. However, market expansion is not without challenges. Regulatory hurdles, including complex certification processes and stringent compliance requirements, impact adoption and increase costs for defense technology providers. Additionally, the defense industry in the US faces a shortage of skilled labor, particularly in areas such as cybersecurity and engineering. One of the most notable trends is the increasing demand for unmanned aerial vehicles (UAVs), which are becoming increasingly essential for surveillance and reconnaissance missions.

- This labor crunch can hinder the implementation of new technologies and limit the growth potential of the market. To capitalize on opportunities and navigate these challenges effectively, companies must invest in workforce development and collaborate with educational institutions to build a pipeline of skilled talent. Furthermore, they should prioritize regulatory compliance and seek partnerships with regulatory bodies to streamline certification processes. Another trend is the continuous technological innovation in the defense industry, leading to advancements in areas such as cybersecurity, artificial intelligence, and autonomous systems. By addressing these challenges, defense technology providers can seize market opportunities and maintain a competitive edge in the rapidly evolving defense landscape.

What will be the size of the US Defense Market during the forecast period?

- The global defense market is characterized by dynamic military alliances and evolving military doctrines. Military aid and defense agreements shape the strategic partnerships that underpin these alliances. Combat readiness remains a top priority, with cyber warfare and information warfare increasingly shaping military policy. Image intelligence and security assistance play crucial roles in force structure and supply chain management. Defense reform continues to be a focus, with the integration of unmanned aerial vehicles, hypersonic weapons, and directed energy weapons into military capabilities. FDI investors are drawn to the sector due to its consistent demand for advanced aircraft, helicopters, battle force ships, aircraft carriers, and auxiliary equipment.

- Security policy and military intelligence are essential components of modern defense, alongside military training and joint operations. Multi-domain operations, space situational awareness, psychological operations, and open-source intelligence are also key areas of investment. Ballistic missile defense, signals intelligence, and human intelligence remain vital components of defense strategy. Military logistics and strategic partnerships ensure the effective implementation of these capabilities.

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

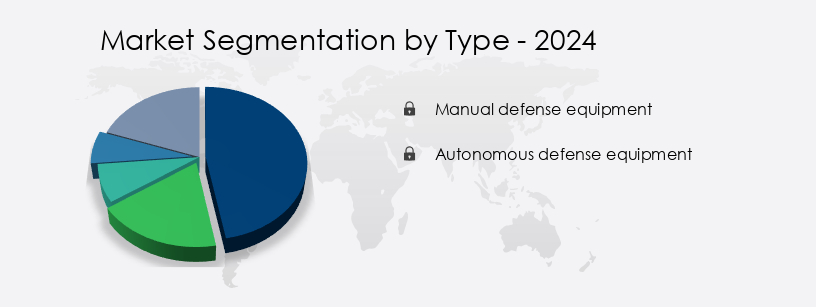

- Type

- Manual defense equipment

- Autonomous defense equipment

- Platform

- Airborne

- Land

- Naval

- End-user

- Military

- Government agencies

- Defense contractors

- Geography

- North America

- US

- North America

By Type Insights

The manual defense equipment segment is estimated to witness significant growth during the forecast period. The US defense market encompasses a diverse range of manual and advanced technologies, from communications systems and sensors to missiles and rockets, shaping defense strategy and military capabilities. Defense contractors play a pivotal role in the industry's innovation, developing cyber defense solutions, cyber threats countermeasures, and artificial intelligence for defense electronics. Military equipment, including weapons systems and combat aircraft, are essential components of force projection and combat operations. Data security and network security are crucial in the digital age, with defense procurement prioritizing advanced technologies like machine learning and big data analytics for defense research and intelligence surveillance reconnaissance.

Get a glance at the market share of various segments Request Free Sample

The Manual defense equipment segment was valued at USD 436.50 billion in 2019 and showed a gradual increase during the forecast period. Space capabilities, including satellites and Space Force initiatives, are crucial for intelligence gathering, communication, and navigation. Defense exports and imports influence the industry's dynamics, while defense alliances and national security collaborations foster international security. Logistics and support, humanitarian aid, and disaster relief are essential aspects of defense systems, demonstrating the industry's multifaceted role in military readiness and operational effectiveness. Military training, aerospace and defense, and defense systems research drive military tactics and capabilities, with force projection, electronic warfare, and combat operations at the forefront. Command and control, missiles and rockets, and sensors and detectors are integral to defense strategy and military innovation. Weapons systems, military vehicles, and naval vessels are essential components of defense modernization and operational effectiveness, while defense budget and spending shape the industry's growth trajectory. Emerging threats necessitate continuous innovation in defense technologies, leading to investments in radar, SONARs, and overhaul services. Defense cooperation and strategic planning are vital for autonomous systems, defense trade, and defense industry development.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Defense in US Industry?

- The significant increase in demand for unmanned aerial vehicles (UAVs) in the United States serves as the primary market driver. The defense market in the US is experiencing significant growth due to several key factors. Increased military spending and the rising demand for advanced surveillance solutions are driving the market forward. The threat of terrorism and insurgency, as well as the need for enhanced security, have led to increased investment in defense technologies. Unmanned aerial vehicles (UAVs), also known as drones, are becoming increasingly popular in defense applications. The integration of autonomy, artificial intelligence, and sensor technologies is enabling the creation of self-contained UAVs for surveillance, reconnaissance, logistics, and other defense purposes. Furthermore, the growing importance of cyber defense and data security has led to increased demand for defense electronics, communications systems, sensors and detectors, and cyber defense solutions.

- Missiles and rockets continue to play a crucial role in defense, with ongoing research and development in this area focusing on improving accuracy, range, and payload capacity. The US defense budget, with significant budget authority from the President, facilitates the acquisition of advanced aircraft, submarines, and naval vessels, among other strategic resources. Military innovation is a key driver of market growth, with a focus on developing advanced technologies to address evolving security threats. Machine learning and other emerging technologies are also expected to have a significant impact on the defense market in the coming years.

What are the market trends shaping the Defense in US Industry?

- The defense industry is experiencing a significant increase in technological innovation, which is currently shaping market trends. This upward trend in technological advancements is a key focus for professionals in the industry. The defense market in the US is driven by technological innovation, with government investment and industry collaboration playing a pivotal role. Advanced technologies, such as artificial intelligence, big data analytics, and network security, are transforming the defense industry. Military capabilities are being enhanced through the integration of these technologies into logistics and support systems, military equipment, and defense strategies. Aerospace companies in the US are at the forefront of this technological evolution, developing advanced aircraft designs that prioritize fuel efficiency, emissions reduction, and increased performance. These improvements enable aerospace and defense platforms to complete missions more efficiently, driving up demand for these products and services.

- Innovative solutions, such as additive manufacturing, energy-efficient propulsion systems, and advanced sensor technologies, are addressing changing customer needs and emerging defense challenges. Moreover, the defense industry is leveraging data analytics to gain insights into operational efficiency, threat detection, and predictive maintenance. Network security and information security are also critical areas of focus, as the defense sector becomes increasingly reliant on digital technologies. Defense alliances and partnerships are also driving growth in the market, as countries collaborate to develop and deploy advanced military capabilities. Overall, the defense market in the US is poised for continued growth, as technological innovation and strategic partnerships shape the future of defense and security solutions.

What challenges does the Defense in US Industry face during its growth?

- The defense industry in the United States faces significant growth challenges due to a scarcity of skilled labor. This workforce shortage poses a substantial obstacle to the industry's expansion. The defense market in the US faces challenges due to a shortage of skilled labor, which may impede its growth during the forecast period. This labor shortage hinders defense companies' ability to innovate and develop new technologies, as they lack a sufficient workforce of skilled engineers, technicians, and researchers. Consequently, businesses may experience delays in project timelines for defense programs, leading to product development, testing, and deployment delays, negatively impacting market expansion. The high demand for skilled labor in the defense sector results in elevated labor costs as companies compete for talent. The defense market in the US is influenced by the labor market dynamics, with the shortage of skilled labor posing a significant challenge to market growth.

- This situation necessitates a focus on defense research, force projection, electronic warfare, combat operations, defense systems, military training, aerospace and defense, and intelligence, surveillance, and reconnaissance to address the labor shortage and maintain a competitive edge in the global defense industry. Submarines and Nuclear Submarines are also a significant focus, as are armored vehicles, Missiles, Tanks, and light weapons.

Exclusive Customer Landscape

The defense market in US forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the defense market in US report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, defense market in US forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - The company specializes in defense solutions, providing advanced technology for combat aircraft such as the Eurofighter Typhoon and multi-role airlifters, including the A400M, C295, and CN235.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- BAE Systems Plc

- Elbit Systems Ltd.

- General Dynamics Corp.

- General Electric Co.

- General Motors Co.

- Honeywell International Inc.

- Huntington Ingalls Industries Inc.

- Kongsberg Gruppen ASA

- L3Harris Technologies Inc.

- Lockheed Martin Corp.

- Northrop Grumman Corp.

- Oshkosh Corp.

- Polaris Inc.

- QinetiQ Ltd.

- RTX Corp.

- Smith and Wesson Brands Inc

- Textron Inc.

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Defense Market In US

- In February 2024, Lockheed Martin Corporation, a leading defense contractor, announced the successful integration of the Advanced Extremely High Frequency (AEHF) satellite into the U.S. Military's communications network. This strategic development significantly enhances secure military communications, as reported by Lockheed Martin's press release.

- In October 2024, Northrop Grumman Corporation received a USD13.3 billion contract from the U.S. Navy for the production of the Columbia-class submarine, the next generation of ballistic missile submarines. This major contract, as stated in a U.S. Department of Defense press release, demonstrates the ongoing commitment to modernizing the U.S. Nuclear deterrent.

- In January 2025, Israel Aerospace Industries (IAI) and Elbit Systems announced a strategic partnership to develop and produce unmanned aerial systems (UAS) for the global defense market. According to the IAI press release, this collaboration will leverage the companies' combined expertise to offer advanced UAS solutions to meet the growing demand for unmanned systems in defense applications.

Research Analyst Overview

The defense market continues to evolve, with dynamic market dynamics shaping the industry across various sectors. National security and international security remain the primary drivers, necessitating ongoing innovation in naval vessels, military vehicles, military training, aerospace and defense, defense systems, defense research, force projection, electronic warfare, combat operations, defense technology, intelligence surveillance reconnaissance, and more. Cyber threats and communications systems are critical areas of focus, with defense electronics and sensors and detectors playing pivotal roles in cyber defense. Machine learning and artificial intelligence are transforming data security, while humanitarian aid and logistics and support are essential components of defense strategy. FDI investors play a role in defense market growth, particularly in advanced aircraft and satellite production.

Military innovation is a continuous process, with defense contractors at the forefront of developing advanced technologies, including big data analytics and autonomous systems. Defense procurement and defense trade are significant aspects of defense modernization, with defense budgets and spending a constant consideration for strategic planning. Defense alliances and cooperation are vital in ensuring military capabilities remain effective, with force projection and combat aircraft essential components of military readiness. Command and control, weapons systems, and combat operations are all areas undergoing significant advancements, with electronic warfare and intelligence surveillance reconnaissance playing crucial roles in maintaining operational effectiveness. In the ever-changing defense landscape, defense research and development are ongoing, with ongoing unfolding of market activities and evolving patterns.

The defense industry continues to adapt and innovate, ensuring national and international security remains a priority.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Defense Market in US insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.6% |

|

Market growth 2025-2029 |

USD 188 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.4 |

|

Key countries |

US |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks, |

What are the Key Data Covered in this Defense Market in US Research and Growth Report?

- CAGR of the Defense in US industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the defense market in US growth of industry companies

We can help! Our analysts can customize this defense market in US research report to meet your requirements.

RIA -

RIA -