Third-Party Logistics (3PL) Market Size 2025-2029

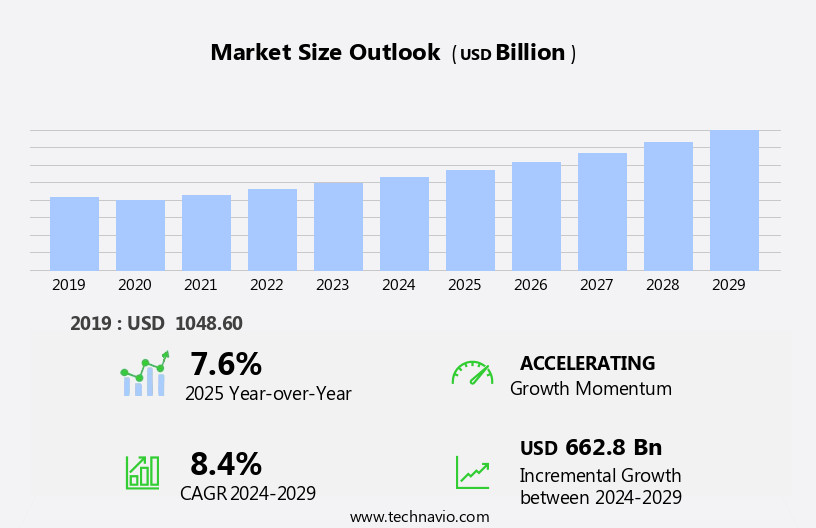

The third-party logistics (3pl) market size is forecast to increase by USD 662.8 billion, at a CAGR of 8.4% between 2024 and 2029.

- The market is experiencing significant growth due to the surge in e-commerce and the increasing demand for integrated shipping services. As consumers continue to prefer online shopping, businesses are turning to 3PL providers to manage their supply chain and fulfill orders efficiently. This trend is expected to continue, presenting a lucrative opportunity for 3PL providers. Another key driver in the market is the emergence of big data analytics. The use of advanced analytics tools is enabling 3PLs to optimize their operations, improve customer service, and gain a competitive edge. However, the market also faces challenges, with high operational costs and competitive pricing being major obstacles.

- To remain competitive, 3PLs must find ways to reduce costs while maintaining quality and service levels. This may involve implementing automation, leveraging technology, and optimizing their networks. Companies seeking to capitalize on market opportunities and navigate challenges effectively should focus on innovation, operational efficiency, and customer service.

What will be the Size of the Third-Party Logistics (3PL) Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, with dynamic market activities shaping its landscape. Seamless integration of network design, API integrations, customs brokerage, labor management, returns processing, load planning, dock scheduling, freight forwarding, dedicated contract carriage, and supply chain optimization are essential elements of this complex system. Real-time visibility and order accuracy are critical components of modern logistics, enabling businesses to effectively manage inventory and optimize costs. Capacity planning and freight consolidation are ongoing processes, ensuring efficient use of resources and reducing unnecessary transportation costs. Route optimization and yard management are essential for streamlining operations and minimizing transportation time. Data analytics and business intelligence provide valuable insights, enabling predictive analytics and demand forecasting to optimize supply chain performance.

Technology integration, including warehouse automation and AI-powered logistics, plays a pivotal role in enhancing efficiency metrics and reducing risk. Carbon footprint and fleet management are increasingly important considerations, with sustainability becoming a key focus for many organizations. E-commerce logistics, reverse logistics, and last-mile delivery are growing sectors, requiring specialized solutions for pick and pack, order fulfillment, and on-time delivery. Contract logistics and distribution centers are integral to the supply chain, providing essential services such as sorting systems and risk management. The 3PL market is characterized by continuous change and innovation, with ongoing developments in technology, regulations, and customer expectations driving the need for adaptability and flexibility.

How is this Third-Party Logistics (3PL) Industry segmented?

The third-party logistics (3pl) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Transportation services

- Warehousing and distribution services

- Others

- End-user

- Manufacturing

- Retail

- Consumer goods

- Healthcare

- Others

- Mode Of Transportation

- Roadways

- Seaways

- Railways

- Airways

- Multimodal transport

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

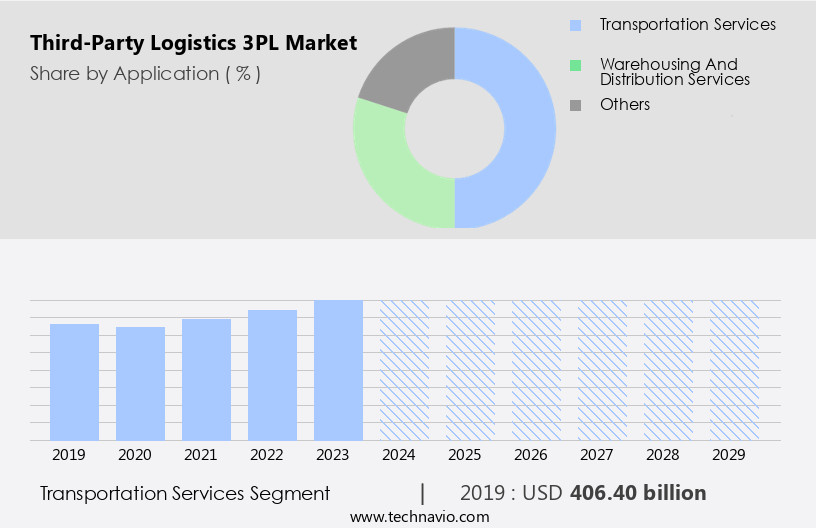

By Application Insights

The transportation services segment is estimated to witness significant growth during the forecast period.

The market's transportation services segment is a significant contributor to the industry's growth. This segment specializes in various transportation modes, including road, rail, air, and sea, to move goods efficiently. Outsourcing cargo and freight transportation to 3PL providers is increasingly popular due to the substantial investment and expertise required. The transportation services segment offers additional benefits, such as freight forwarding, project logistics, network planning, cargo insurance, optimization, and customs brokerage. Technological advancements are driving innovation in the transportation services segment. Real-time visibility, capacity planning, and route optimization are crucial elements that enhance supply chain efficiency. Data analytics and predictive analytics facilitate demand forecasting and inventory management, ensuring accurate order fulfillment.

Fleet management systems optimize vehicle utilization and reduce carbon footprint. Yard management systems streamline loading and unloading processes, while technology integration enables seamless data exchange between systems. Efficiency metrics, risk management, and labor management are essential components of the transportation services segment. Warehouse automation, contract logistics, and order fulfillment are integral to the overall supply chain optimization. Reverse logistics, e-commerce logistics, and last-mile delivery are emerging trends that cater to evolving customer demands. The integration of artificial intelligence and machine learning in logistics processes further enhances operational efficiency and accuracy. In conclusion, the transportation services segment in the third-party logistics market is a dynamic and evolving sector that offers numerous benefits to businesses.

Its ability to adapt to technological advancements and changing market trends positions it as a vital player in the global supply chain landscape.

The Transportation services segment was valued at USD 406.40 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

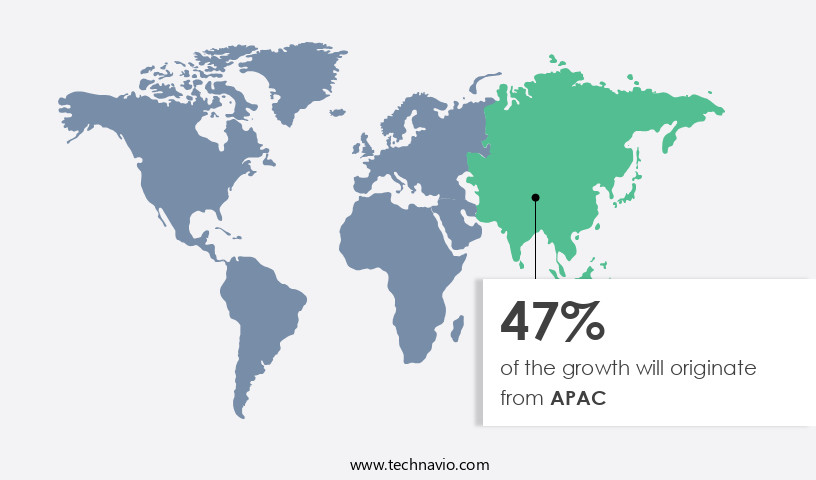

APAC is estimated to contribute 47% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in APAC is experiencing significant growth due to the increasing volume of international trade. The region's economic expansion, particularly in China and the automobile industries in Japan and India, presents substantial opportunities for 3PL service providers. However, the Indian logistics sector, which is largely unorganized, faces challenges such as high logistics costs, affecting both domestic and international competitiveness. To address these challenges, 3PLs are implementing advanced technologies such as real-time visibility, capacity planning, freight consolidation, route optimization, yard management, inventory management, data analytics, predictive analytics, and demand forecasting. These solutions improve efficiency, reduce costs, and enhance supply chain visibility.

Additionally, 3PLs are focusing on cost optimization, risk management, technology integration, network design, and api integrations to streamline operations and provide customized services. Moreover, sustainability is becoming a critical consideration in the 3PL industry. Companies are implementing carbon footprint reduction strategies, fleet management, and warehouse automation to minimize their environmental impact. Furthermore, the integration of AI-powered logistics, e-commerce logistics, reverse logistics, and last-mile delivery solutions is enabling 3PLs to cater to evolving customer demands and stay competitive. Overall, the 3PL market in APAC is dynamic, with a focus on innovation, efficiency, and customer satisfaction.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a dynamic and essential segment of the global supply chain industry. 3PL providers offer outsourced logistics solutions, expertly managing inventory, transportation, warehousing, and fulfillment for businesses seeking to streamline operations and focus on core competencies. Integrating advanced technologies like warehouse management systems (WMS), transportation management systems (TMS), and automation, 3PLs ensure efficient and cost-effective supply chain management. Flexible contract structures, scalability, and customized services cater to businesses of all sizes, from small startups to large enterprises. Strategic partnerships with carriers, technology providers, and other logistics players further enhance 3PLs' capabilities. Sustainability initiatives, regulatory compliance, and data analytics are key priorities, driving innovation and continuous improvement in the 3PL market.

What are the key market drivers leading to the rise in the adoption of Third-Party Logistics (3PL) Industry?

- The expansion of e-commerce and the resulting demand for seamless shipping solutions are primary market catalysts.

- The market has experienced significant growth due to the surge in e-commerce businesses and the increasing demand for efficient and cost-effective supply chain management. E-commerce companies require swift delivery systems, advanced inventory management, and streamlined freight forwarding to meet customer expectations and maintain operational success. 3PL providers offer business intelligence solutions, including predictive analytics and demand forecasting, to optimize inventory levels and minimize stockouts. Carbon footprint reduction is also a priority, with fleet management systems and sorting systems designed to improve efficiency metrics and reduce transportation costs. Risk management is crucial in this sector, with technology integration enabling real-time monitoring and automated responses to potential disruptions.

- Efficient inventory management and quick delivery are essential in the e-commerce industry, making the need for advanced logistics solutions more pressing. The integration of technology, such as automated sorting systems and real-time tracking, has revolutionized the 3PL market, enabling businesses to make data-driven decisions and respond to market trends more effectively. In conclusion, the 3PL market is evolving to meet the demands of e-commerce businesses, offering advanced solutions for inventory management, freight forwarding, and risk management. The integration of technology, including predictive analytics and fleet management systems, is driving innovation and improving operational efficiency. The focus on sustainability and reducing carbon footprint is also a significant trend, with 3PL providers implementing strategies to minimize their environmental impact.

What are the market trends shaping the Third-Party Logistics (3PL) Industry?

- The emergence of big data analytics is a significant market trend, gaining increasing importance in today's data-driven business landscape. This trend signifies the growing recognition of the value in analyzing large and complex data sets to derive meaningful insights and inform strategic decision-making.

- In the logistics sector, third-party logistics (3PL) providers and shippers are utilizing big data analytics to extract valuable insights from extensive data sets, thereby gaining a competitive edge. Big data analytics solutions facilitate the customization of services, expedite market demand, and inspire new business models based on agility. However, the implementation of big data analytics in logistics is still in its infancy due to substantial IT disparities. Big data analytics plays a pivotal role in three primary domains within the logistics industry: operational efficiency, customer experience, and new business models. By optimizing core activities, such as labor management, load planning, dock scheduling, freight forwarding, customs brokerage, and returns processing, logistics companies can enhance operational efficiency.

- Moreover, big data analytics enables the provision of personalized services to customers, thereby improving customer experience. Lastly, the application of big data analytics can lead to the creation of innovative business models that prioritize flexibility and responsiveness. Additionally, big data analytics offers the optimization of essential logistics activities, including resource utilization, delivery time, and geographical coverage. Network design, API integrations, and dedicated contract carriage are some areas that can significantly benefit from big data analytics. By harnessing the power of big data analytics, logistics companies can streamline their operations, foster customer satisfaction, and maintain a competitive edge in the market.

What challenges does the Third-Party Logistics (3PL) Industry face during its growth?

- The convergence of high operational costs and competitive pricing poses a significant challenge to the industry's growth trajectory.

- The market is experiencing significant competition due to the increasing demand for value-added services and specialized solutions. However, rising fuel prices add to the operational costs, putting pressure on providers to maintain low prices for their customers. In response, businesses are seeking lower rates when renewing contracts and requesting additional services at the same price. Consequently, 3PL companies face cost pressures related to the pricing of their services. E-commerce logistics, including pick and pack and order fulfillment, are driving market growth.

- Warehouse automation and AI-powered logistics solutions are also gaining popularity to enhance efficiency and accuracy. Reverse logistics and last-mile delivery are other areas of focus to meet customer demands for seamless returns and on-time delivery. Despite these challenges, 3PL companies are adapting by offering innovative solutions to reduce costs and improve overall supply chain efficiency.

Exclusive Customer Landscape

The third-party logistics (3pl) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the third-party logistics (3pl) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, third-party logistics (3pl) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agility Public Warehousing Co. K.S.C.P - Third-party logistics provider offers global freight forwarding, contract logistics, warehousing, and specialized solutions for industries including chemicals, aerospace, and retail. Services ensure efficient supply chain management and enhanced market access. Solutions tailored to meet unique industry requirements. Expertise in international trade regulations and customs procedures. Innovative technology integration for streamlined operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agility Public Warehousing Co. K.S.C.P

- AP Moller Maersk AS

- Baltic Logistics Group

- BDP International Inc.

- Burris Logistics Co.

- C H Robinson Worldwide Inc.

- CEVA Logistics SA

- DB Schenker

- Deutsche Bahn AG

- Deutsche Post AG

- FedEx Corp.

- GEODIS

- Hub Group Inc.

- J B Hunt Transport Services Inc.

- Kintetsu Group Holdings Co. Ltd.

- Kuehne Nagel Management AG

- Nippon Express Holdings Inc.

- Sinotrans Ltd

- United Parcel Service Inc.

- XPO Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Third-Party Logistics (3PL) Market

- In January 2024, DHL Supply Chain, a leading third-party logistics (3PL) provider, announced the launch of its new Robotic Picking Solution in partnership with Swisslog, enhancing their order fulfillment capabilities (DHL press release). This technological advancement aimed to improve efficiency and reduce errors in the picking process.

- In March 2024, UPS Logistics and DB Schenker, two major 3PL players, joined forces to offer integrated freight forwarding and contract logistics services, expanding their combined market reach and capabilities (UPS press release). This strategic partnership aimed to provide more comprehensive logistics solutions to their clients.

- In May 2025, Kuehne + Nagel, a global 3PL company, secured a significant investment of USD500 million from Blackstone Group to strengthen its digital transformation and expand its logistics network (Bloomberg). This funding round demonstrated the growing interest in digitalization and innovation within the 3PL sector.

- In the same month, FedEx Logistics received approval from the European Commission to acquire TNT Express, a leading European express and logistics company, marking a significant geographic expansion for FedEx (FedEx press release). This acquisition allowed FedEx to strengthen its European market presence and broaden its service offerings.

Research Analyst Overview

- The 3PL market encompasses various logistics services, including drop shipping, parcel delivery, and international logistics. A notable trend is the rise of direct-to-consumer (DTC) logistics, requiring efficient omni-channel fulfillment and returns management. Warehouse optimization and inventory control are crucial for managing stock levels and reducing carrying costs. Hazardous materials transportation and special commodity handling pose unique challenges, necessitating strict regulations and specialized expertise. Temperature-controlled transportation and cold chain logistics are essential for industries dealing with perishable goods. Value-added services, such as kitting and packaging, are increasingly popular, helping businesses save time and resources. Multimodal transportation, including truckload (TL), less-than-truckload (LTL), rail freight, intermodal transportation, and air freight, offers flexibility and cost savings.

- Logistics software plays a pivotal role in managing complex supply chains, ensuring supply chain resilience and demand planning. Oversized load transportation and waste management are essential components of the 3PL market, catering to industries with large and bulky goods or waste disposal needs. In the realm of global logistics, international freight forwarding and ocean freight are vital for businesses engaging in international trade. Regional logistics networks facilitate efficient and cost-effective distribution within specific geographic areas. Consignment inventory and small parcel shipping are integral parts of the 3PL market, catering to businesses with varying logistics needs. Regardless of the specific logistics services required, the 3PL market continues to evolve, driven by the need for flexibility, efficiency, and innovation.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Third-Party Logistics (3PL) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

236 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.4% |

|

Market growth 2025-2029 |

USD 662.8 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.6 |

|

Key countries |

US, China, Japan, India, Brazil, South Korea, Germany, Canada, UK, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Third-Party Logistics (3PL) Market Research and Growth Report?

- CAGR of the Third-Party Logistics (3PL) industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the third-party logistics (3pl) market growth of industry companies

We can help! Our analysts can customize this third-party logistics (3pl) market research report to meet your requirements.

RIA -

RIA -