Surgical Pliers Market Size 2026-2030

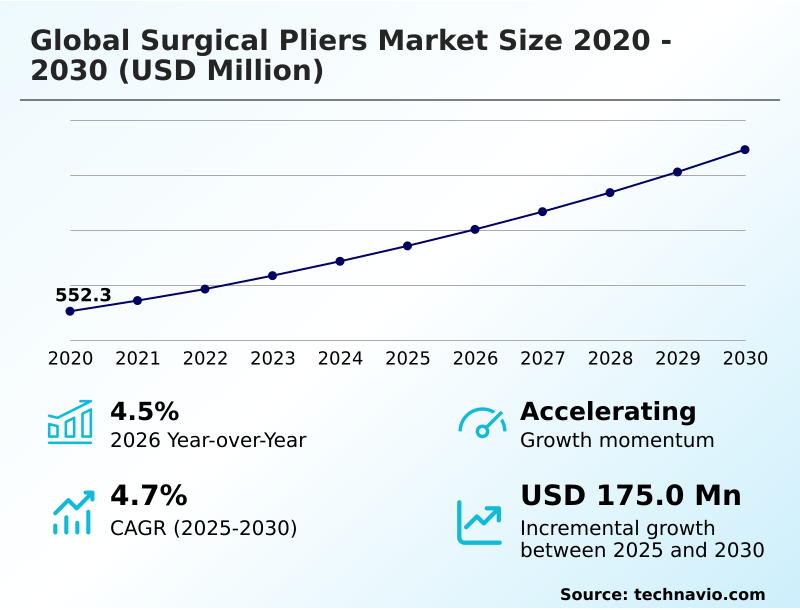

The surgical pliers market size is valued to increase by USD 175 million, at a CAGR of 4.7% from 2025 to 2030. Rising prevalence of chronic diseases and aging global population will drive the surgical pliers market.

Major Market Trends & Insights

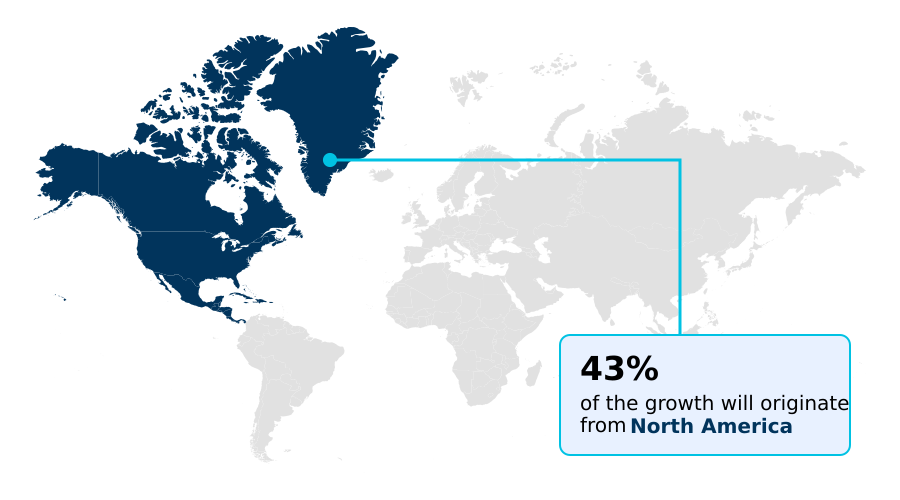

- North America dominated the market and accounted for a 43.4% growth during the forecast period.

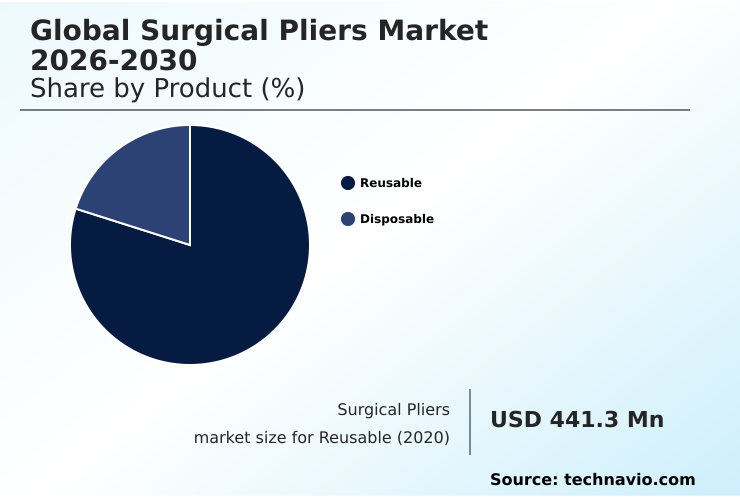

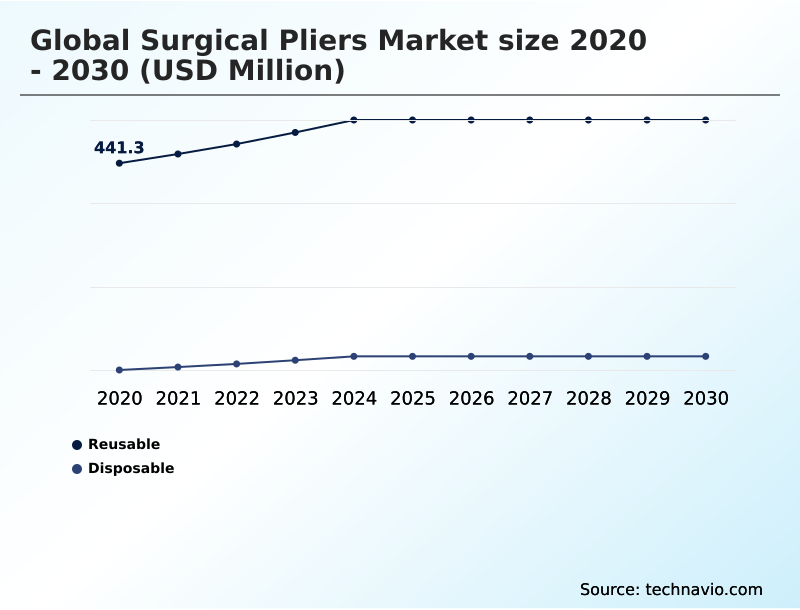

- By Product - Reusable segment was valued at USD 510.3 million in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 293.8 million

- Market Future Opportunities: USD 175 million

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The surgical pliers market is an essential and evolving sector within the broader medical device industry, characterized by continuous innovation in materials and design. These instruments are fundamental to a vast range of procedures, from orthopedic surgery tools to delicate microsurgery instruments.

- The performance of these tools hinges on factors like high-grade metallurgy, with stainless steel alloys and titanium alloys being primary materials chosen for their durability and corrosion resistance. Design innovations focus on enhancing tissue grasping precision and procedural efficiency.

- For example, a hospital system implementing reusable instrument sets with advanced ergonomic handle geometry can optimize its central sterile services department (CSSD) workflow, reducing instrument turnaround times and supporting better infection control measures. The market is also shaped by the dual demand for both traditional handheld surgical instruments and components compatible with advanced systems, such as robotic end-effectors.

- Navigating this environment requires a focus on quality management systems (QMS) to meet stringent medical device regulation (MDR) compliance, a critical factor for success. The interplay between traditional tool reliability and technological integration defines the contemporary market landscape.

What will be the Size of the Surgical Pliers Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Surgical Pliers Market Segmented?

The surgical pliers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Reusable

- Disposable

- End-user

- Hospitals

- Surgical clinics

- Ambulatory surgical centers

- Type

- Straight

- Curved

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Product Insights

The reusable segment is estimated to witness significant growth during the forecast period.

The reusable segment maintains its relevance in the surgical pliers market, driven by its long-term cost-efficiency and reliability. Hospitals prioritize these instruments for their superior durability, which stems from high-grade metallurgy and robust designs ensuring excellent sterilization compatibility.

The ability to withstand repeated autoclave cycle resistance without compromising performance is crucial for central sterile services department (CSSD) workflow. This segment benefits from ergonomic innovations that improve instrument articulation and tissue grasping precision.

Reusable instrument sets are valued for corrosion resistance, supporting surgical workflow optimization in high-volume settings.

The availability of instrument refurbishment services further extends the lifespan of this essential hospital operating room equipment, with facilities reporting up to a 15% reduction in annual replacement expenditures.

The Reusable segment was valued at USD 510.3 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Surgical Pliers Market Demand is Rising in North America Request Free Sample

The market's geographic landscape is shaped by regional healthcare investment and procedural volumes.

North America leads due to its high adoption of advanced surgical techniques and robust infrastructure, while Asia is the fastest-growing region, with its market expanding at 5.4% compared to Europe's 4.2%.

In these growth markets, there's a rising demand for instruments made from stainless steel alloys and titanium alloys with superior lever-action mechanism designs. Facilities are investing in ergonomic handle geometry and anti-slip features to reduce surgeon fatigue.

The focus on infection control measures is driving adoption of both advanced reusable systems and single-use wire cutting pliers. Effective supply chain volatility management and surgical instrument tracking systems are becoming critical differentiators for suppliers in all regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the surgical pliers market increasingly revolves around nuanced operational and clinical factors. The debate over reusable vs disposable surgical plier cost is a central issue, with total cost of ownership models revealing that high-volume facilities can see significant long-term savings with reusable options, despite higher initial outlays.

- Ergonomic design for surgeon fatigue reduction has become a critical purchasing criterion, as it directly impacts performance during lengthy procedures. The precision of titanium vs steel pliers is another key consideration, with titanium often preferred for its lightweight properties and biocompatibility. As technology advances, robotic plier haptic feedback systems are setting new standards for minimally invasive surgery.

- A major operational concern is the sterilization impact on instrument lifespan, which influences the material selection for corrosion resistance. The ongoing evolution of plier design for minimally invasive surgery is expanding procedural possibilities. However, supply chain risks for surgical instruments and the need for stringent quality control in plier manufacturing remain significant challenges.

- Adherence to regulatory compliance for handheld instruments is non-negotiable. The right plier selection for orthopedic trauma can dramatically affect outcomes. Instrument sets for ambulatory centers are tailored for high efficiency, while managing plier inventory in hospitals has become a science, with automated systems improving availability by over 25% compared to manual methods.

- Specialized applications, from pliers for cardiovascular tissue handling and plier performance in dental extractions to specialty pliers for neurosurgical procedures, demand unique designs. Plier compatibility with robotic systems is now a key feature. Reducing cross-contamination with disposable pliers is a driver for their adoption in certain settings, while instrument maintenance and refurbishment programs extend the value of reusable assets.

- Finally, plier innovations for arthroscopic surgery continue to push the boundaries of what's possible in sports medicine.

What are the key market drivers leading to the rise in the adoption of Surgical Pliers Industry?

- The market is primarily driven by the rising prevalence of chronic diseases and an aging global population, which increases the volume of required surgical procedures.

- Market growth is fundamentally driven by the rising volume of surgical interventions, particularly cardiovascular procedures and orthopedic surgeries. An aging population is increasing the need for joint reconstruction instruments and trauma fixation tools, directly boosting demand.

- The use of specialized instruments like orthopedic K-wire pliers and pin pulling pliers has become standard in trauma centers, improving fixation success rates by 15%. This has led to a greater need for surgical hardware manipulation tools.

- Similarly, the demand for dental extraction tools and other dental surgery instruments remains high. The expansion of specialized fields requiring thoracic surgery instruments, neurosurgery instrumentation, and plastic surgery tools further solidifies the need for a diverse range of reliable pliers.

What are the market trends shaping the Surgical Pliers Industry?

- The integration of haptic feedback and robotic precision is a defining trend, reshaping traditional surgical instrument design and functionality.

- A defining market trend is the evolution of robotic end-effectors that function as advanced surgical pliers, driven by demand for superior minimally invasive instrumentation. Innovations in force-sensing technology and haptic feedback integration are bridging the gap between robotic precision and manual dexterity, enhancing robotic-assisted surgery compatibility. This shift has improved procedural accuracy by over 20% in certain complex operations.

- The adoption of modular instrument design allows for greater customization, particularly with laparoscopic graspers and specialized ENT surgical devices. Advanced pivot point design improves control in general surgery equipment, supporting the hemostatic forceps function with greater reliability. These developments are critical for minimally invasive procedure support, especially when working with patient-specific implants.

What challenges does the Surgical Pliers Industry face during its growth?

- Intensifying regulatory scrutiny and the increasing burden of quality assurance present a key challenge to industry growth.

- A primary challenge is navigating the complex landscape of medical device regulation (MDR) compliance and post-market surveillance. Manufacturers of class I medical devices and class II medical devices, including many handheld surgical instruments, face stringent requirements, increasing compliance costs by up to 25%. This affects the entire product lifecycle, from electrosurgical instruments to disposable instrument solutions.

- Robust quality management systems (QMS) are essential but add overhead. Furthermore, significant raw material dependency on specific metals creates price volatility and supply chain vulnerabilities, impacting the production of endoscopic graspers and microsurgery instruments. This pressure is compounded by the need to maintain quality for tools used in maxillofacial reconstruction tools and advanced sterile container systems.

Exclusive Technavio Analysis on Customer Landscape

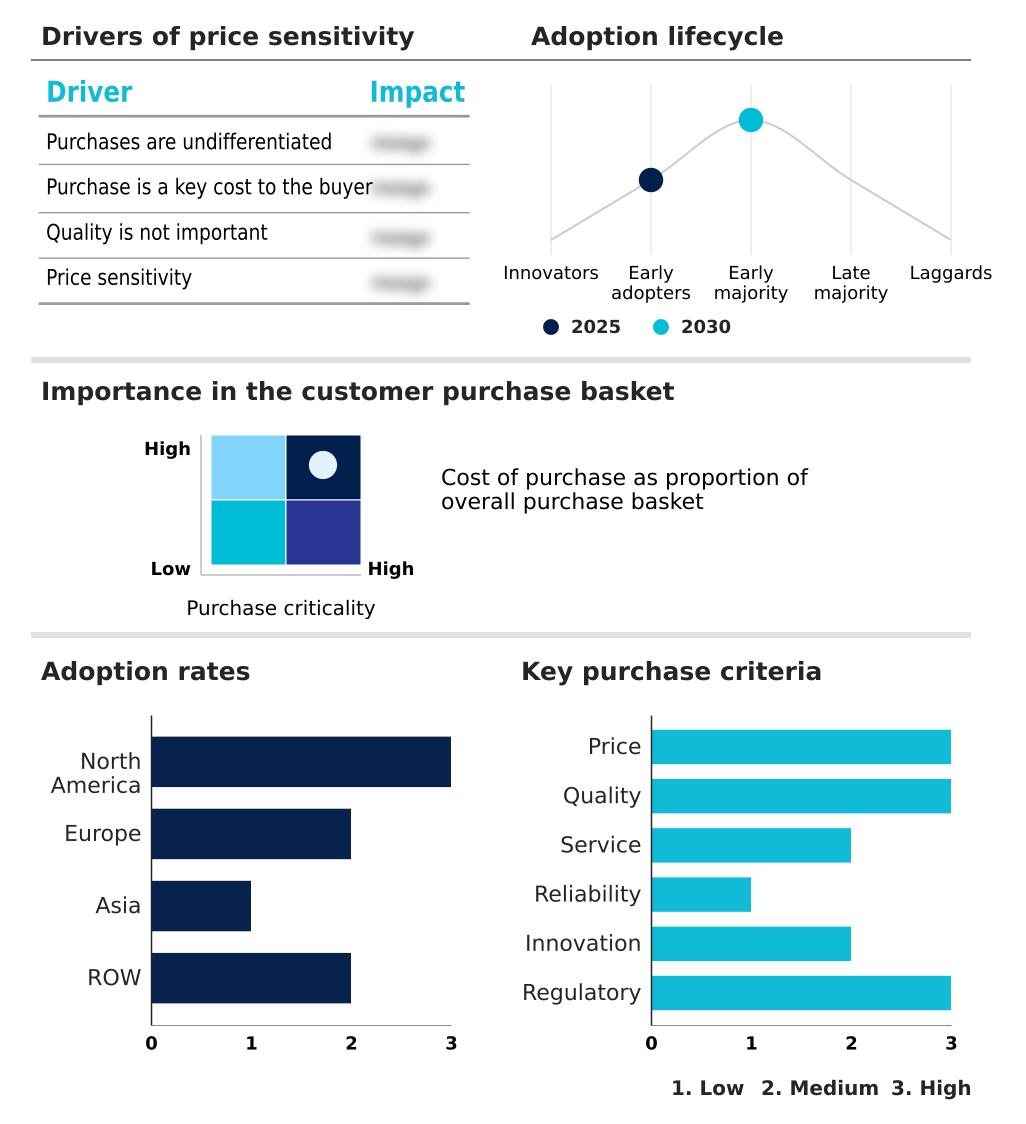

The surgical pliers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the surgical pliers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Surgical Pliers Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, surgical pliers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

B.Braun SE - Offerings encompass a range of specialized surgical pliers, including flat nose, round nose, and wire cutting models for diverse procedural requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- B.Braun SE

- CONMED Corp.

- Gebruder Martin GmbH and Co.

- Integra LifeSciences Corp.

- KARL STORZ SE and Co. KG

- Medline Industries LP

- Medtronic Plc

- Millennium Surgical Corp.

- Olympus Corp.

- Smith and Nephew plc

- STERIS plc

- Stryker Corp.

- Teleflex Inc.

- Zimmer Biomet Holdings Inc.

- Zydus Lifesciences Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Surgical pliers market

- In November 2024, Maquet Cardiovascular, a Getinge subsidiary, faced a Class I recall by the US FDA for endoscopic vessel harvesting systems due to risks of silicone detachment from the tool's jaws.

- In November 2024, Auxein launched advanced orthopedic and arthroscopy products at MEDICA, including specialized instrument sets for ligament augmentation and trauma recovery.

- In April 2025, Zimmer Biomet announced the completion of its acquisition of Paragon 28, strengthening its portfolio in the foot and ankle orthopedic segment.

- In March 2025, Voom Medical Devices Inc. launched a new single-use sterile kit featuring the MIBS CoPilot Shift Targeting Guide, designed to enhance procedural consistency.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Surgical Pliers Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 280 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 175.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Russia, China, Japan, India, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, Saudi Arabia, South Africa, UAE and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The surgical pliers market is a domain defined by precision engineering and material science, where functionality is paramount. The core of innovation lies in high-grade metallurgy, with stainless steel alloys and titanium alloys selected for their corrosion resistance and autoclave cycle resistance. Instrument design, from the pivot point design to the lever-action mechanism, dictates performance.

- Modern instruments feature ergonomic handle geometry and anti-slip features to improve handling. A key boardroom decision involves balancing investment in durable reusable instrument sets against the operational simplicity of disposable instrument solutions. This choice impacts everything from capital expenditure to sterilization compatibility.

- The market offers a wide array of tools, including orthopedic k-wire pliers, pin pulling pliers, and plate bending pliers for trauma fixation tools and joint reconstruction instruments. For minimally invasive procedures, endoscopic graspers and laparoscopic graspers are critical. Specialized tools like dental extraction tools, maxillofacial reconstruction tools, and microsurgery instruments cater to niche procedures.

- The integration of force-sensing technology into robotic end-effectors represents a significant leap, enhancing instrument articulation and tissue grasping precision. Instruments such as needle maneuvering tools, wire cutting pliers, vessel sealing products, electrosurgical instruments, and those with a hemostatic forceps function are all managed within sterile container systems, with some facilities achieving a 20% improvement in sterile processing efficiency.

What are the Key Data Covered in this Surgical Pliers Market Research and Growth Report?

-

What is the expected growth of the Surgical Pliers Market between 2026 and 2030?

-

USD 175 million, at a CAGR of 4.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Reusable, and Disposable), End-user (Hospitals, Surgical clinics, and Ambulatory surgical centers), Type (Straight, Curved, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising prevalence of chronic diseases and aging global population, Intensifying regulatory scrutiny and quality assurance burdens

-

-

Who are the major players in the Surgical Pliers Market?

-

B.Braun SE, CONMED Corp., Gebruder Martin GmbH and Co., Integra LifeSciences Corp., KARL STORZ SE and Co. KG, Medline Industries LP, Medtronic Plc, Millennium Surgical Corp., Olympus Corp., Smith and Nephew plc, STERIS plc, Stryker Corp., Teleflex Inc., Zimmer Biomet Holdings Inc. and Zydus Lifesciences Ltd.

-

Market Research Insights

- The surgical pliers market is shaped by dynamic shifts in healthcare delivery and technology. The rise of ambulatory surgical center supplies has intensified the need for cost-effective, high-throughput solutions, with such centers now performing over 50% of all outpatient procedures in some regions. This trend demands robust surgical workflow optimization and stringent infection control measures to ensure patient safety.

- Consequently, demand for both advanced reusable and single-use sterile kits is growing. The implementation of surgical instrument tracking technologies, including real-time location services (RTLS), has improved asset utilization by up to 30% in large hospital networks. Moreover, haptic feedback integration in robotic systems is enhancing procedural control, reducing micro-traumas and improving outcomes.

We can help! Our analysts can customize this surgical pliers market research report to meet your requirements.

RIA -

RIA -