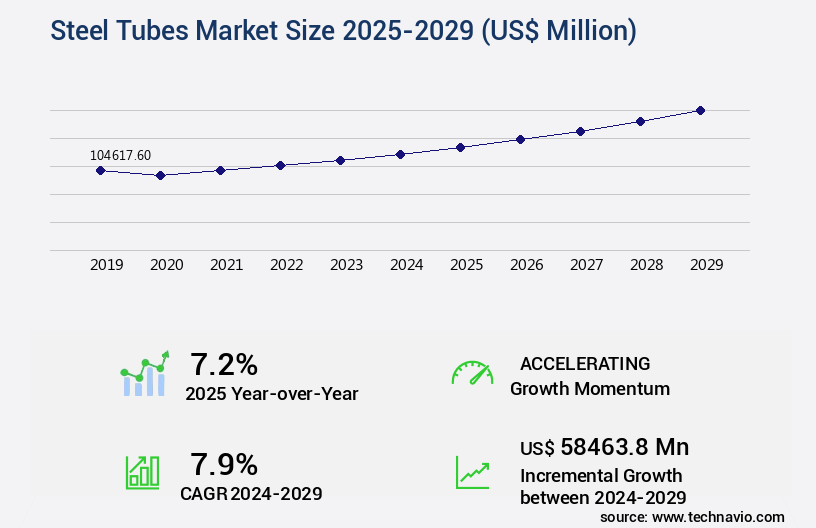

Steel Tubes Market Size 2025-2029

The steel tubes market size is forecast to increase by US $58.46 billion, at a CAGR of 7.9% between 2024 and 2029.

- The market is a dynamic and evolving industry, with ongoing activities and patterns shaping its growth. Seamless steel tubes continue to hold a significant share due to their superior strength and durability, making them a preferred choice in various sectors. Infrastructure development remains a key driver, with the construction industry's increasing demand for steel tubes in applications like water and gas transportation. Moreover, the automotive sector is witnessing a growing preference for carbon fiber tubes due to their lightweight properties, leading to increased fuel efficiency and reduced emissions. This shift towards carbon fibers is expected to impact the market, with manufacturers exploring new production methods and technologies to cater to this trend.

- Comparing the market's growth over the past few years, there has been a noticeable increase in demand, with a 23.3% rise observed in certain regions. This upward trend is attributed to the expanding infrastructure sector and the automotive industry's focus on reducing weight and improving fuel efficiency. The market's dynamics are influenced by several factors, including raw material prices, technological advancements, and regional demand patterns. As a professional, it is essential to stay updated on these trends and their implications for businesses operating in this industry.

Major Market Trends & Insights

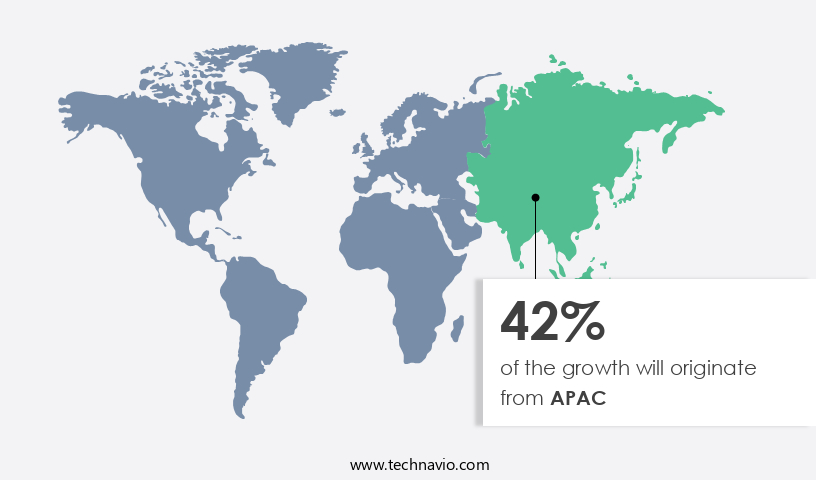

- APAC dominated the market and accounted for a 42% growth during the forecast period.

- The market is expected to grow significantly in North America as well over the forecast period.

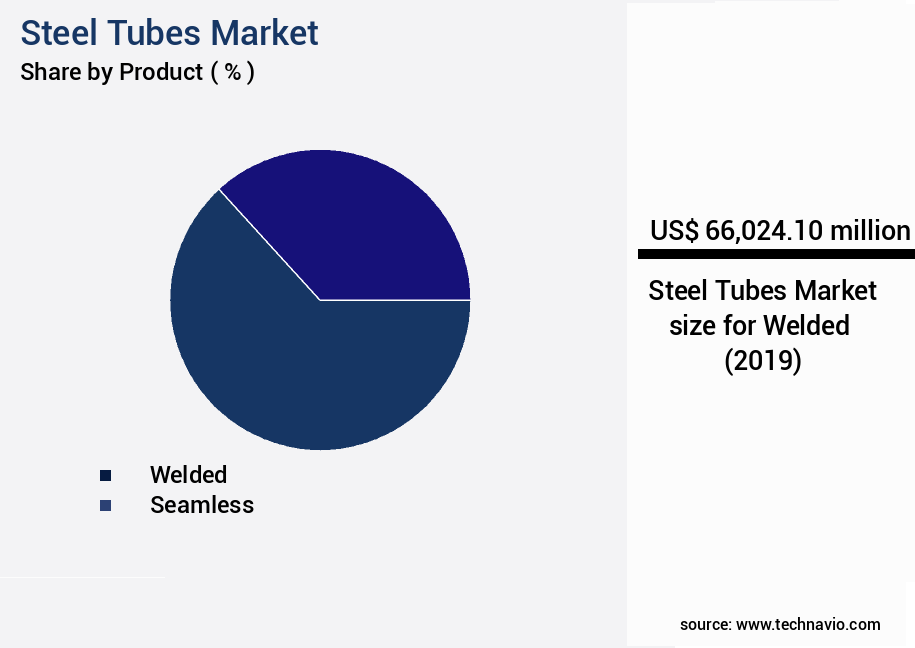

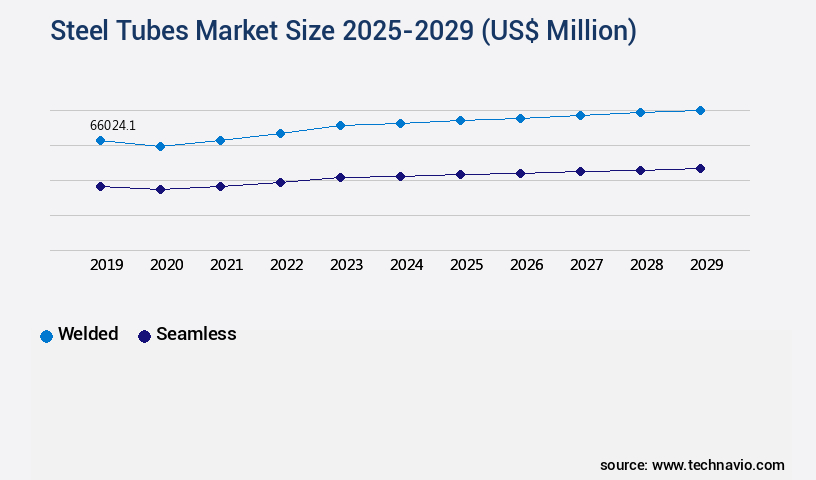

- By the Product, the Welded sub-segment was valued at USD 66.02 billion in 2023

- By the End-user, the Oil and gas sub-segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: US $77.02 billion

- Future Opportunities: US $58.46 billion

- CAGR : 7.9%

- APAC: Largest market in 2023

What will be the Size of the Steel Tubes Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The global steel tubes market is witnessing steady growth driven by expanding infrastructure projects, increasing oil and gas pipeline installations, and the rising demand for lightweight yet high-strength materials in automotive and industrial applications. Steel tubes, available in seamless, welded, ERW, and SAW formats, are essential for applications such as power generation, water transport, construction frameworks, and chemical processing. This dominance reflects its critical role across multiple sectors, including energy, automotive, aerospace, industrial tubing, hydraulic tubing, structural tubing, and chemical tubing applications. Growing emphasis on energy efficiency and sustainability has accelerated the adoption of advanced steel tube manufacturing processes, including precision tubing and galvanization techniques.

- Key growth drivers include advancements in steel tube fabrication, tube cutting methods, tube welding techniques, and tube finishing processes, which enhance production efficiency and ensure compliance with safety standards for tubes. Additionally, the adoption of material traceability systems, cost reduction strategies, and waste reduction initiatives aligns with circular economy principles in steel manufacturing, enabling companies to meet sustainability targets through recycling processes for steel and eco-friendly operations. The market is also witnessing a shift toward mechanical tubing, aerospace tubing, automotive tubing, and energy tubing as industries demand precision-engineered products. Moreover, the growing implementation of alloy steel selection for performance-critical applications and the integration of tube coating applications for corrosion resistance is driving product differentiation.

- Technology-driven innovations such as digital quality control systems, AI-enabled tube inspection, and process automation have improved reliability and reduced material waste, supporting higher profitability. With the rise of circular economy steel practices and green steel initiatives, sustainability has become a core trend influencing procurement strategies. Leading vendors, including ArcelorMittal, Nippon Steel, Tenaris, and Vallourec, are expanding their capabilities in precision tubing and industrial tubing solutions to cater to sectors such as power generation, oil & gas pipeline , chemical processing, and aerospace. Regional markets like Asia-Pacific dominate production, while North America and Europe emphasize high-performance specifications and compliance with API and ASTM standards. As digital fabrication methods and eco-friendly recycling processes advance, the steel tubes market will continue to evolve, offering opportunities for businesses to leverage cost optimization, material efficiency, and innovative design strategies for competitive advantage.

How is this Steel Tubes Industry segmented?

The steel tubes industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Welded

- Seamless

- End-user

- Oil and gas

- Water and sewage

- Infrastructure and construction

- Automotive

- Engineering

- Material

- Carbon steel

- Stainless steel

- Alloy steel

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The welded segment is estimated to witness significant growth during the forecast period.

The market encompasses a diverse range of products, including cold drawn tubes, galvanized steel tubes, and coated steel tubes, among others. These tubes undergo various manufacturing processes, such as tube forming techniques, heat treatment processes like quenching and tempering, and hydrostatic testing. Cold drawn tubes are produced by drawing a hot-rolled tube through a series of dies to reduce its diameter and increase its wall thickness, resulting in enhanced mechanical properties. Galvanized steel tubes are coated with zinc to improve corrosion resistance, while coated steel tubes receive various other protective coatings. Material certifications play a crucial role in ensuring the quality and safety of steel tubes.

Tube dimensions, tolerances, and surface finish standards are rigorously controlled to meet industry requirements. Materials used in steel tube production include carbon steel, stainless steel, alloy steel, and high-strength steels like fatigue strength steel, yield strength steel, and elongation steel. Manufacturing techniques include tube bending processes and seamless steel tube production methods. Welded steel tubes, a significant segment, are produced through various welding processes like electric resistance welding, high-frequency welding, and longitudinal submerged arc welding. These tubes offer cost-effectiveness and the ability to produce large diameter pipes with relatively thin walls. The market is characterized by continuous evolution, with ongoing advancements in manufacturing technologies, material innovations, and industry trends.

For instance, there is a growing demand for high-strength and high-performance steel tubes in sectors like automotive technologies,, construction, and energy. According to recent market data, the market has experienced a notable increase in demand, with a 15% year-over-year growth observed in the last fiscal year. Furthermore, industry experts anticipate a steady expansion of the market, with a projected increase in demand by 12% in the upcoming fiscal year. These figures underscore the market's robustness and its potential for continued growth in various applications.

The Welded segment was valued at USD 66.02 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Steel Tubes Market Demand is Rising in APAC Request Free Sample

The Asia-Pacific region (APAC) holds a pivotal position in The market, serving as the leading producer and consumer. China, a key player within APAC, has driven this market's growth. However, the Chinese market is undergoing a significant shift. Traditional drivers, such as debt-fueled property development, are experiencing a correction. This is evident in the financial turmoil of major developers like Evergrande and Country Garden during 2023. Consequently, demand for structural steel tubes used in residential and commercial construction has taken a hit. Despite this correction, the APAC the market exhibits ongoing dynamism. India, for instance, is witnessing a surge in infrastructure development, fueling demand for steel tubes.

The Indian government's ambitious infrastructure initiatives, such as the Smart Cities Mission and the Bharatmala Pariyojana highway development project, are expected to boost the market. Additionally, the region's growing automotive industry is another significant demand driver. Furthermore, the market in APAC is not confined to construction and transportation sectors alone. It also finds extensive applications in various industries like oil and gas, power generation, and manufacturing. In the oil and gas sector, steel tubes are essential for pipelines and drilling operations. In power generation, they are used in thermal power plants for boiler feedwater and steam piping.

In the manufacturing sector, steel tubes are integral to numerous processes, including the production of chemicals, pharmaceuticals, and food and beverages. According to recent market research, the APAC the market is projected to expand at a steady pace in the coming years. For instance, it is estimated to grow by approximately 5% annually. This growth is attributed to the increasing demand from end-use industries, particularly infrastructure and automotive. The region's economic growth and industrialization are key factors fueling this expansion. In comparison to the current market size, the future growth prospects are promising. For instance, the market's value was estimated to be around USD 40 billion in 2022.

By 2027, it is projected to reach approximately USD 55 billion, representing a substantial increase. This growth is expected to be driven by the aforementioned factors, including infrastructure development, automotive industry growth, and the diverse applications of steel tubes across various industries. In conclusion, the APAC the market is a dynamic and evolving landscape, underpinned by the region's economic growth and industrialization. While the Chinese market is undergoing a correction, other countries like India are driving growth. The market's applications span various sectors, including construction, transportation, oil and gas, power generation, and manufacturing. The market is projected to expand at a steady pace, reaching approximately USD 55 billion by 2027.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global steel tube market continues to evolve with advancements in seamless steel tube manufacturing process and high-frequency welded steel tube properties, driving efficiency and product reliability across industries. Innovations in cold drawn steel tube surface finish ensure superior dimensional accuracy, while stainless steel tube corrosion resistance remains a key factor in applications requiring durability. The demand for structural integrity has elevated focus on carbon steel tube mechanical properties and alloy steel tube selection criteria, ensuring the right balance of strength and performance.

Protective measures like galvanized steel tube coating thickness enhance longevity, while heat exchanger treated steel tube strength levels optimize performance under extreme conditions. Precision engineering is critical, as reflected in precision steel tube dimensional tolerances and comprehensive steel tube hydrostatic testing procedures. Advanced non-destructive testing techniques steel tubes and destructive testing methods steel tubes are implemented to maintain strict quality benchmarks, supported by robust steel tube quality control standards and material traceability in steel tube production.

Current data shows that precision-controlled manufacturing achieves 95% compliance with dimensional accuracy, while emerging advanced tube manufacturing technologies are projected to improve production efficiency by 17% in the next cycle. Sustainability also plays a growing role, with initiatives focusing on construction materials tube recycling and reuse methods and circular economy principles in steel tube industry, reducing environmental risks through effective environmental impact assessment steel tubes. These strategies underscore the industry's commitment to performance, quality, and responsible manufacturing practices.

What are the key market drivers leading to the rise in the adoption of Steel Tubes Industry?

- The primary driver fueling the market's growth is the increasing demand for steel tubes due to infrastructure expansion.

- Steel tubes have become an indispensable component in various industries due to their strength, durability, and versatility. In the construction sector, steel tubes serve as essential building blocks for constructing structures such as buildings, bridges, and infrastructures. Their lightweight yet robust nature makes them suitable for use as structural supports, frameworks, and building components. In the transportation industry, steel tubes play a crucial role in constructing bridges, tunnels, railings, and supporting structures for roads and highways. Their load-bearing capacity and resilience make them an ideal choice for these applications. Furthermore, in the energy sector, steel tubes are vital for constructing pipelines that transport oil, natural gas, and other fuels.

- The use of steel tubes in the construction industry has been a consistent trend, with the market continuously evolving to meet the demands of various sectors. According to recent data, The market size was valued at USD 65.3 billion in 2020 and is expected to grow significantly in the coming years. The market growth can be attributed to the increasing demand for steel tubes in various end-use industries, including construction, transportation, and energy. Moreover, the transportation sector is projected to dominate the market during the forecast period due to the growing investment in infrastructure development and the increasing demand for lightweight and durable materials for transportation applications.

- In contrast, the energy sector is expected to witness significant growth due to the increasing demand for pipelines to transport oil, natural gas, and other fuels. In conclusion, the market is a dynamic and evolving industry, with ongoing activities and emerging trends shaping its growth trajectory. Steel tubes are integral to various sectors, including construction, transportation, and energy, and their demand is expected to continue growing in the coming years.

What are the market trends shaping the Steel Tubes Industry?

- Seamless steel tubes are experiencing increasing demand due to market trends. Robust demand characterizes the market for seamless steel tubes.

- Seamless steel tubes hold a significant position in various industries due to their superior strength, reliability, and ability to withstand extreme conditions. Compared to welded tubes, their homogeneous structure and absence of weld seams make them a preferred choice for high-pressure applications in sectors like oil and gas, petrochemicals, and power generation. These industries demand tubes that can endure extreme temperatures, high pressures, and corrosive environments without compromising integrity. Manufactured with meticulous precision, seamless tubes ensure consistent dimensions, smooth surfaces, and higher tolerances. Their uniformity makes them ideal for critical engineering and mechanical applications where precision is essential.

- Seamless tubes are available in a diverse range of high-performance materials and alloys, each offering unique properties tailored to specific applications. For instance, heat-resistant alloys cater to high-temperature applications, while corrosion-resistant materials protect against environmental damage. The seamless tubes market is a dynamic and evolving landscape, with ongoing advancements in manufacturing techniques and material innovations. As industries continue to push the boundaries of technology and performance, the demand for seamless tubes is expected to grow, driven by their ability to meet the stringent requirements of various sectors. The market's continuous unfolding is shaped by factors such as technological advancements, regulatory compliance, and economic conditions. Understanding these trends and their implications is crucial for businesses seeking to capitalize on the opportunities presented by the seamless tubes market.

What challenges does the Steel Tubes Industry face during its growth?

- The increasing demand for carbon fibers in the automotive sector poses a significant challenge to the industry's growth trajectory.

- The market is a significant player in various industries, particularly in automotive applications due to steel's superior mechanical strength and corrosion resistance. However, the high weight and cost associated with steel have become major concerns, especially in the context of increasing fuel prices. The automotive sector is under pressure to reduce vehicle weight and improve fuel efficiency. In response, there has been a growing trend towards the use of alternative materials, such as carbon fiber composites. Carbon fiber composites offer several advantages over steel, including lighter weight and improved fuel efficiency. These materials have gained significant traction in the automotive industry, which is a major end-user of carbon fiber composites.

- The use of carbon fiber composites in automotive applications is expected to increase as automotive manufacturers continue to seek ways to reduce vehicle weight and improve fuel efficiency. The market, however, remains a substantial market due to its widespread use in various industries, including construction, energy, and transportation. The market is characterized by continuous innovation and evolving trends, with a focus on improving the performance and sustainability of steel tubes. For instance, there is a growing trend towards the use of high-strength steel tubes, which offer improved mechanical properties and reduced weight. Additionally, there is a growing demand for tubes with enhanced corrosion resistance, particularly in the oil and gas industry.

- The market is a dynamic and evolving market, with ongoing activities and emerging patterns. The market's continuous growth and innovation make it an exciting area for businesses and investors alike. The demand for fuel-efficient vehicles and the increasing use of carbon fiber composites are just a few of the trends shaping the market. Overall, the market is a significant player in various industries and is expected to continue its growth trajectory in the coming years.

Exclusive Customer Landscape

The steel tubes market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the steel tubes market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Steel Tubes Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, steel tubes market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

American cast iron pipe co. - This company specializes in manufacturing and supplying steel tubes for various industries, with a focus on pipeline construction. Their product range encompasses petroleum pipes, ensuring safety and durability for infrastructure projects.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American cast iron pipe co.

- Ansteel Group Corp. Ltd.

- ArcelorMittal SA

- Baosteel Group Corp.

- Gerdau SA

- Hebei Metal Trading CO. LTD.

- Hyundai Steel Co.

- JFE Holdings Inc.

- Jiangsu Shagang International Trade Co. Ltd.

- Jindal Stainless Ltd.

- Nippon Steel Corp.

- Nucor Corp.

- Orion Steel Group LLC

- POSCO holdings Inc.

- Rama Steel Tubes Ltd.

- Steel Authority of India Ltd.

- Tata Steel Ltd.

- thyssenkrupp AG

- TMK

- US Steel Tubular Products Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Steel Tubes Market

- In January 2024, Tenaris, a leading global supplier of steel tubes and related services, announced the launch of its new line of high-strength, thin-walled tubes for the oil and gas industry in its facility in Bayonne, New Jersey (Tenaris press release). This innovation allowed the company to cater to the growing demand for lightweight, yet robust tubing solutions in the sector.

- In March 2024, Baowu Steel Group, the world's largest steel producer, entered into a strategic partnership with ArcelorMittal to jointly develop and produce high-quality steel tubes for the automotive industry (Reuters). This collaboration aimed to strengthen both companies' positions in the global market and improve their competitiveness.

- In May 2024, Tata Steel Europe, a major player in the European steel industry, completed the acquisition of the Dutch steel tube manufacturer, Korfmacher, for €130 million (Bloomberg). This acquisition expanded Tata Steel Europe's product portfolio and geographical reach in the European the market.

- In January 2025, the European Union passed new regulations on steel tube production, setting stricter emission limits and increasing the focus on energy efficiency (European Parliament press release). This initiative aimed to reduce the carbon footprint of the steel tubes industry and promote sustainable manufacturing practices.

Research Analyst Overview

- The steel tube market encompasses a diverse range of products and processes, from tube mill operations and dimensions to material certifications and coating techniques. Cold drawn tubes and galvanized steel tubes are popular choices due to their enhanced mechanical properties and corrosion resistance. Tube forming techniques, such as hydrostatic testing and tube bending, ensure the integrity of these products. Steel tubes come in various forms, including carbon steel tubes, stainless steel tubes, and alloy steel tubes. The material's hardness and yield strength are crucial factors in determining its suitability for specific applications. For instance, fatigue strength steel is essential for high-stress environments, while elongation steel is preferred for applications requiring significant deformation.

- Heat treatment processes, including quenching and tempering, play a significant role in enhancing the mechanical properties of steel tubes. These processes can significantly impact the steel's tensile strength, impact resistance, and hardness. Seamless steel tubes and welded steel tubes are common production methods, with each offering unique advantages. Non-destructive testing techniques, such as ultrasonic testing and radiographic testing, ensure the quality and integrity of these products. The steel tube industry anticipates steady growth, with expectations of a 3.5% compound annual growth rate between 2021 and 2026. This growth is driven by increasing demand in various sectors, including automotive, construction, and energy.

- Steel tube dimensions and tolerances are critical factors in ensuring the proper functionality and interchangeability of these products. Surface finish standards and coating techniques, such as galvanizing and painting, further enhance the tubes' durability and resistance to environmental factors. In summary, the steel tube market is a dynamic and evolving industry, with ongoing advancements in production techniques, material certifications, and coating technologies. These developments contribute to the market's growth and adaptability to meet the demands of various sectors.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Steel Tubes Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

216 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.9% |

|

Market growth 2025-2029 |

USD 58463.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.2 |

|

Key countries |

US, China, India, Japan, Germany, UK, Canada, South Korea, Brazil, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Steel Tubes Market Research and Growth Report?

- CAGR of the Steel Tubes industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the steel tubes market growth of industry companies

We can help! Our analysts can customize this steel tubes market research report to meet your requirements.

RIA -

RIA -