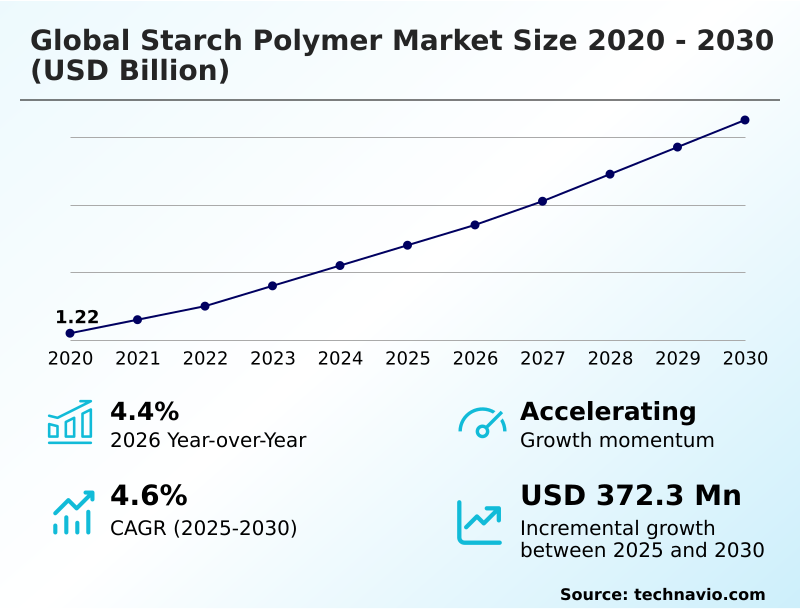

Starch Polymer Market Size 2026-2030

The starch polymer market size is valued to increase by USD 372.3 million, at a CAGR of 4.6% from 2025 to 2030. Escalating regulatory mandates and legislative bans on conventional plastics will drive the starch polymer market.

Major Market Trends & Insights

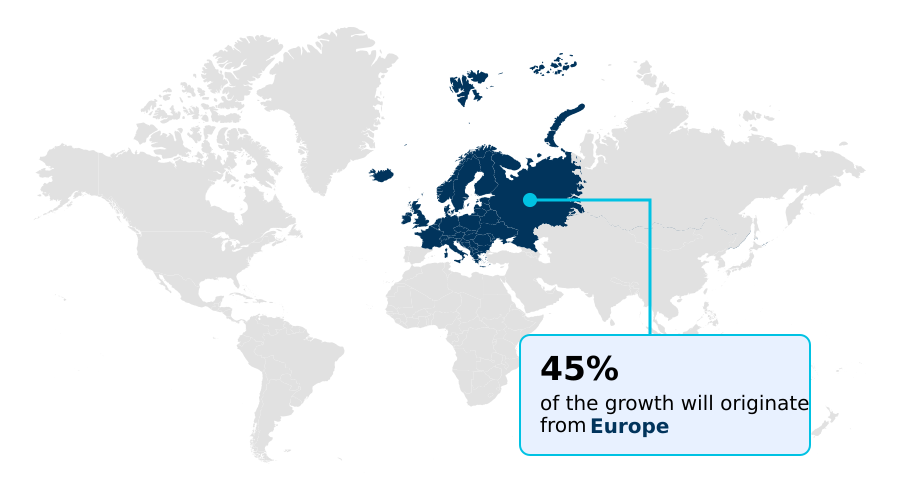

- Europe dominated the market and accounted for a 44.7% growth during the forecast period.

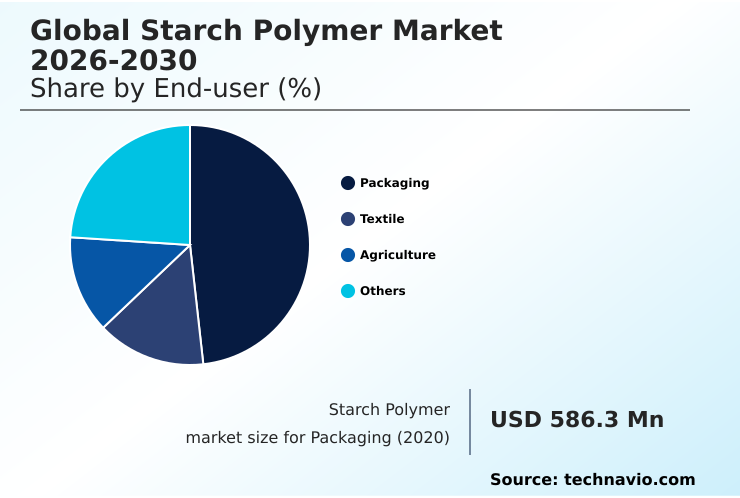

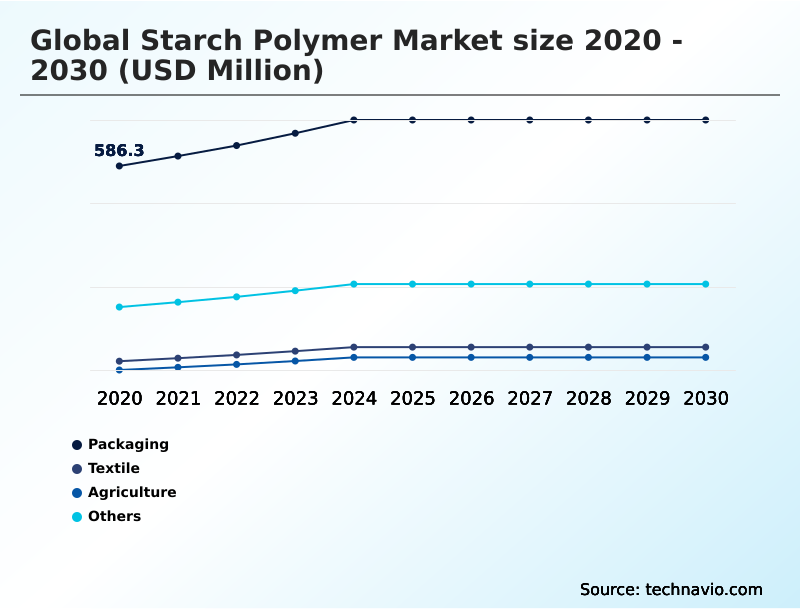

- By End-user - Packaging segment was valued at USD 682.4 million in 2024

- By Source - Corn starch segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 633.9 million

- Market Future Opportunities: USD 372.3 million

- CAGR from 2025 to 2030 : 4.6%

Market Summary

- The starch polymer market is undergoing a significant transformation, driven by the escalating need for sustainable alternatives to petroleum-based plastics. Innovations in starch modification techniques are creating high-performance bio-based polymers suitable for a wide range of uses, from compostable packaging materials to biodegradable mulch films.

- A key trend is the development of biopolymer composites that offer enhanced moisture barrier properties and greater tensile strength, addressing historical limitations. However, the industry faces challenges related to the biopolymer supply chain, where volatility in agricultural feedstock prices can impact manufacturing costs.

- For instance, a food packaging company transitioning to starch-based bioplastics must balance the benefits of a lower carbon footprint against potential supply inconsistencies, requiring sophisticated sourcing strategies to maintain production stability and competitive pricing for their sustainable packaging solutions.

What will be the Size of the Starch Polymer Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Starch Polymer Market Segmented?

The starch polymer industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Packaging

- Textile

- Agriculture

- Others

- Source

- Corn starch

- Cassava starch

- Potato starch

- Wheat starch

- Type

- Bio-degradable

- Durable

- Geography

- Europe

- Germany

- France

- UK

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- Europe

By End-user Insights

The packaging segment is estimated to witness significant growth during the forecast period.

The packaging segment dominates starch polymer applications, driven by the shift toward sustainable materials and advances in bio-based material science. Demand for certified compostable products, particularly in food service and retail, is accelerating the adoption of renewable polymer technology.

This transition is supported by a growing focus on agricultural bioplastics for applications like mulch films. For instance, optimized material formulations have improved processing efficiency by over 15%, reducing waste.

As companies prioritize sustainable material sourcing, starch-based solutions are becoming integral to corporate environmental strategies, moving from niche alternatives to mainstream packaging components that meet both performance and ecological standards.

The Packaging segment was valued at USD 682.4 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 44.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Starch Polymer Market Demand is Rising in Europe Request Free Sample

The geographic landscape is characterized by varying adoption rates influenced by regional regulatory frameworks and industrial capabilities. Europe leads in starch polymer research and deployment, with an incremental growth opportunity of nearly 45%.

Its focus on eco-friendly packaging materials has created a robust market for food-grade bioplastics. In contrast, North America and APAC are rapidly scaling capabilities in bioplastic injection molding and refining starch blend formulations.

These regions leverage deep knowledge of thermoplastic starch properties to expand into non-packaging sectors, contributing significantly to market diversification and the global supply chain.

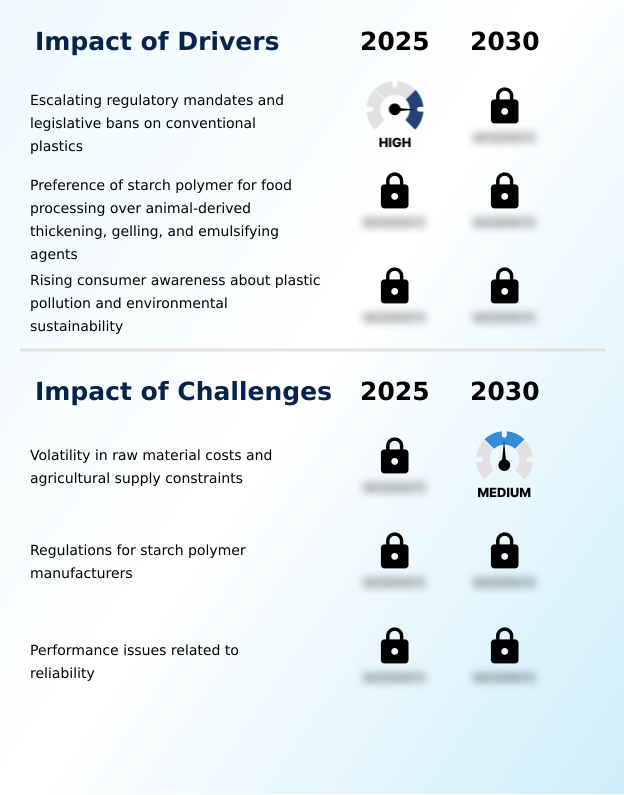

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the starch polymer market requires a deep understanding of material performance and manufacturing processes. A key consideration involves the starch polymer vs pla performance comparison, where factors like tensile strength and thermal properties are critical.

- For packaging applications, improving moisture barrier in starch films is a primary research focus, directly impacting the shelf life of starch-based food packaging. The development and application of starch-based nanocomposites are enabling new functionalities, though balancing the cost-effectiveness of thermoplastic starch remains essential. The regulatory landscape, especially the specific regulations for compostable food packaging, dictates design and end-of-life pathways.

- In agriculture, the use of starch polymer for agricultural mulch films offers a sustainable alternative to conventional plastics. The biodegradable cutlery manufacturing process is being optimized using advanced injection molding with starch biopolymers. For flexible film applications, creating a durable starch blend for flexible packaging film is paramount.

- This involves enhancing the tensile strength of bioplastics and understanding the thermal properties of thermoplastic starch. Firms successfully blending starch with other biopolymers report processing cycle times reduced by over 10%. Overcoming the challenges of starch polymer production, including sourcing corn starch for bioplastics, is crucial for scalability.

- This also involves exploring diverse feedstocks, with significant interest in potato starch in biodegradable packaging and unique cassava starch based biopolymer uses. Similarly, the role of wheat starch in sustainable materials is expanding. Innovations are even extending to niche areas, with firms developing certified home compostable starch plastics and using starch polymer in 3d printing filaments, showcasing the material's versatility.

What are the key market drivers leading to the rise in the adoption of Starch Polymer Industry?

- The market's growth is primarily driven by escalating regulatory mandates and widespread legislative bans on conventional plastics, which accelerates the adoption of bio-based alternatives.

- Growth is accelerated by stringent regulations on single-use plastics and a global push for reducing plastic pollution. This creates significant demand for circular economy materials and pushes companies toward sustainable material sourcing.

- Starch as a renewable feedstock is central to this transition, offering one of the most viable biodegradable plastic alternatives.

- Despite some challenges in bioplastic adoption, regulatory pressures are forcing industries to innovate, with regions enforcing bans showing adoption rates over 40% higher than those without.

What are the market trends shaping the Starch Polymer Industry?

- The market is witnessing a key trend toward the integration of advanced biopolymer blends and nanotechnology. This is driven by the need to enhance the barrier properties of starch-based materials for demanding applications.

- The market is defined by rapid plant-based packaging innovation, where the focus is on developing advanced biocomposite materials. These materials offer enhanced performance, including the creation of heat-resistant bioplastics suitable for more demanding uses. A key area of development involves improving bioplastic durability, with new formulations increasing material longevity by over 30%.

- Advances in green polymer chemistry are enabling the production of high-barrier bioplastic films that extend product shelf life by up to 20%, shaping the future of sustainable plastics.

What challenges does the Starch Polymer Industry face during its growth?

- A primary challenge affecting industry growth is the inherent volatility in raw material costs and supply chain constraints associated with key agricultural feedstocks.

- Navigating the starch-based resin market requires overcoming key hurdles. A primary concern is the inherent moisture sensitivity of bioplastics, which can limit applications without advanced formulation. The biopolymer supply chain is also subject to agricultural volatility, impacting the overall cost of biodegradable plastics and creating price fluctuations of up to 15%.

- Continuous bioplastic performance enhancement is necessary to compete with conventional polymers, driving investment in biodegradable polymer manufacturing technologies to improve process efficiency by at least 10%.

Exclusive Technavio Analysis on Customer Landscape

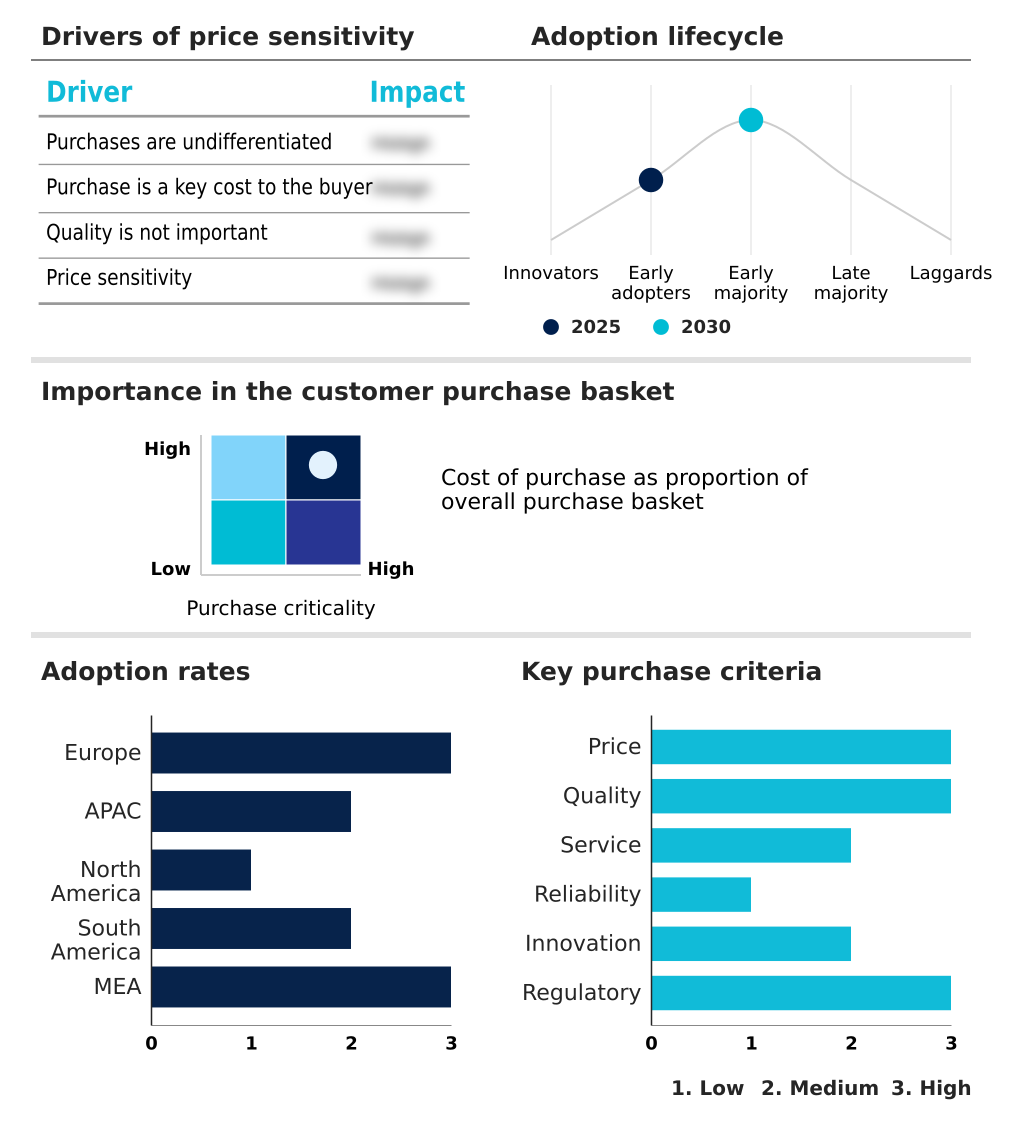

The starch polymer market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the starch polymer market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Starch Polymer Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, starch polymer market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AGRANA Beteiligungs AG - Offerings include biodegradable starch-based polymers engineered for high-performance packaging and agricultural film applications, aligning with sustainability mandates and functional requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGRANA Beteiligungs AG

- Biome Bioplastics Ltd.

- Biotec GmbH Co. and KG

- Braskem SA

- Corbion N.V.

- DuPont de Nemours Inc.

- Fkur Kunststoff GmbH

- Green Dot Bioplastics Inc.

- JAPAN CORN STARCH CO., LTD.

- KURARAY Co. Ltd.

- Mitsubishi Chemical Corp.

- NatureWorks LLC

- Novamont S.p.A.

- SPAC Starch Products Ltd.

- Toray Industries Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Starch polymer market

- In August 2024, Roquette announced the expansion of its line of functional starches designed for the biopolymer industry, aiming to improve water resistance and mechanical properties.

- In January 2025, TotalEnergies Corbion unveiled a collaborative project with a major retail organization to implement starch-polylactic acid blends in reusable shopping bags to enhance durability.

- In March 2025, NatureWorks LLC announced a collaboration with a biotechnology laboratory to integrate starch-derived nanofibers into their high-performance Ingeo biopolymer line for enhanced heat resistance.

- In May 2025, Cargill entered into a strategic agreement with a biotechnology firm to develop next-generation starch-based resins for high-value applications in the electronics industry.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Starch Polymer Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.6% |

| Market growth 2026-2030 | USD 372.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.4% |

| Key countries | Germany, France, UK, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Kenya |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The starch polymer market is shaped by advances in sustainable polymer science, focusing on bio-based polymers to meet decarbonization goals. A key area is the development of thermoplastic starch (tps) and other starch-based bioplastics, driven by demand for sustainable packaging solutions. Innovations in starch modification techniques and the reactive extrusion process are enhancing material properties.

- For example, controlling the amylose and amylopectin ratio and the starch gelatinization process improves retrogradation resistance. This allows for superior biopolymer composites and starch-nanocomposites with improved moisture barrier properties and thermal stability of biopolymers. The focus on high-amylose starch enables the creation of high-performance bio-based films.

- Boardroom decisions are now heavily influenced by the need to increase renewable material content, with some firms achieving a 30% improvement in material efficiency. Bioplastic resin manufacturing is scaling up, producing injection molding grade starch and extrusion grade biopolymer for applications like flexible film packaging and rigid bioplastic containers.

- Products such as biodegradable mulch films and biodegradable cutlery must meet stringent compostability standards. The development of biodegradable polymer blends and certified compostable polymer materials with enhanced gas barrier films is critical. This includes engineering water-soluble polymers and understanding plasticizer effects on starch to improve the tensile strength of bioplastics, ultimately contributing to carbon footprint reduction with each bio-based resin.

What are the Key Data Covered in this Starch Polymer Market Research and Growth Report?

-

What is the expected growth of the Starch Polymer Market between 2026 and 2030?

-

USD 372.3 million, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Packaging, Textile, Agriculture, and Others), Source (Corn starch, Cassava starch, Potato starch, and Wheat starch), Type (Bio-degradable, and Durable) and Geography (Europe, APAC, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, APAC, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating regulatory mandates and legislative bans on conventional plastics, Volatility in raw material costs and agricultural supply constraints

-

-

Who are the major players in the Starch Polymer Market?

-

AGRANA Beteiligungs AG, Biome Bioplastics Ltd., Biotec GmbH Co. and KG, Braskem SA, Corbion N.V., DuPont de Nemours Inc., Fkur Kunststoff GmbH, Green Dot Bioplastics Inc., JAPAN CORN STARCH CO., LTD., KURARAY Co. Ltd., Mitsubishi Chemical Corp., NatureWorks LLC, Novamont S.p.A., SPAC Starch Products Ltd. and Toray Industries Inc.

-

Market Research Insights

- The market is evolving beyond simple substitution, driven by intensive starch polymer research aimed at tangible bioplastic performance enhancement. The push for compostable food packaging, for example, has led to new formulations that improve material strength by 20% while maintaining certified biodegradability.

- Companies that integrate these circular economy materials into their supply chains report a reduction in end-of-life management costs by up to 30%. These advancements demonstrate a shift toward creating high-value, functional bioplastics that meet both sustainability mandates and rigorous industrial standards.

We can help! Our analysts can customize this starch polymer market research report to meet your requirements.