SOC As A Service Market Size 2025-2029

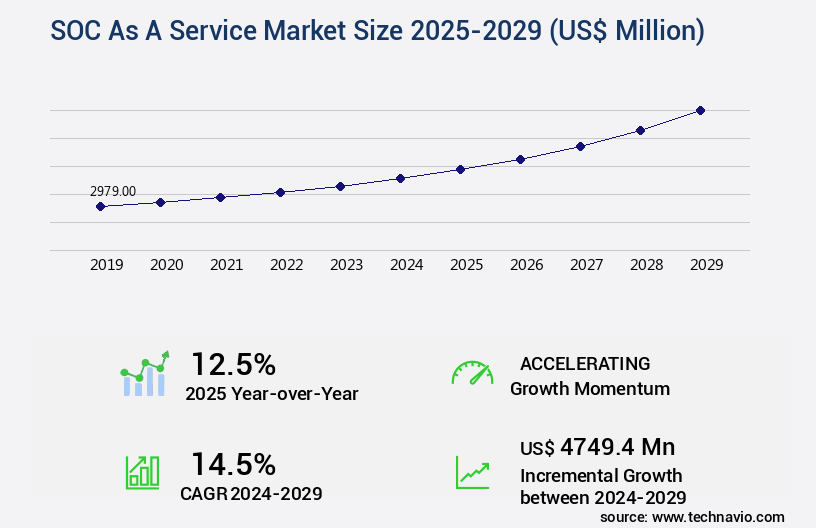

The SOC as a service market size is valued to increase USD 4.75 billion, at a CAGR of 14.5% from 2024 to 2029. Rising bring-your-own-device and work-from-home model will drive the SOC as a service market.

Major Market Trends & Insights

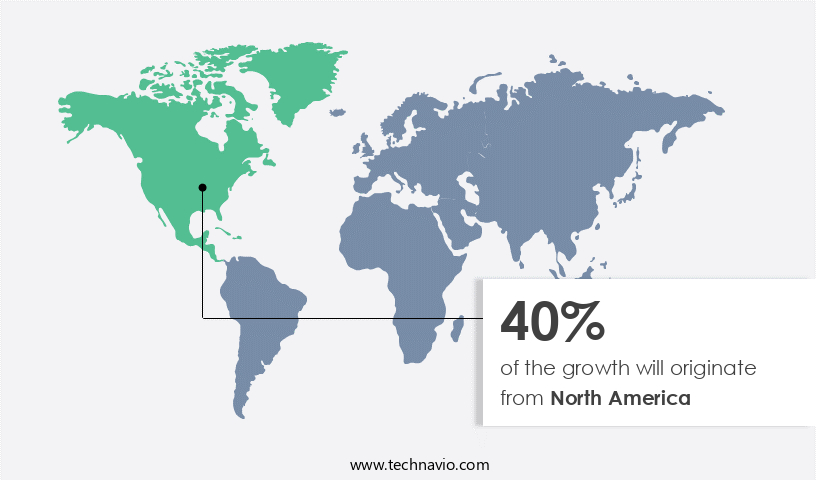

- North America dominated the market and accounted for a 40% growth during the forecast period.

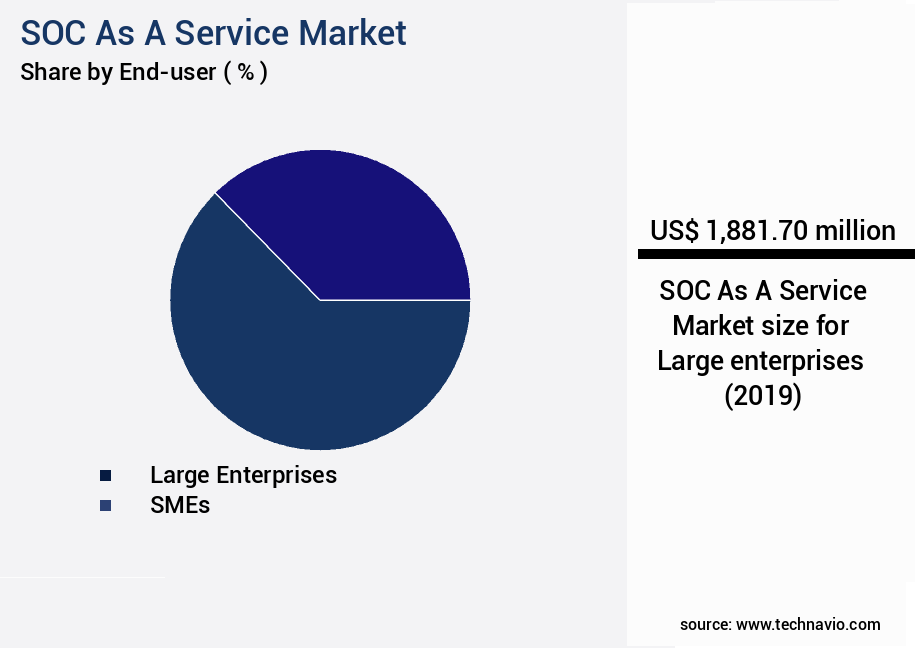

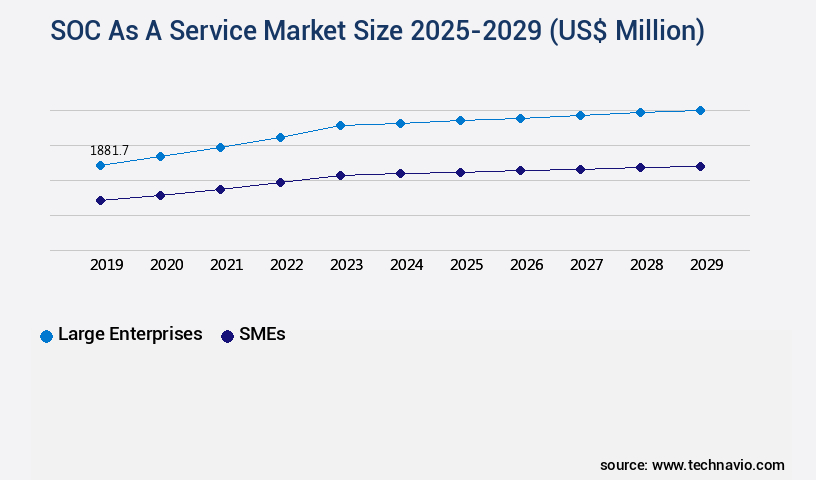

- By End-user - Large enterprises segment was valued at USD 1.88 billion in 2023

- By Service - Prevention services segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 224.77 million

- Market Future Opportunities: USD 4749.40 million

- CAGR : 14.5%

- North America: Largest market in 2023

Market Summary

- The market represents a continuously evolving landscape, characterized by the integration of advanced technologies and applications to enhance security operations. Core technologies, such as Security Information and Event Management (SIEM) and Security Orchestration, Automation, and Response (SOAR), play a pivotal role in driving market growth. Service types, including Managed Security Services (MSS) and Security Operations Centers as a Service (SOCaaS), cater to diverse business needs. Regulations and directives, including GDPR and HIPAA, fuel the demand for SOC as a Service, particularly in industries with stringent data protection requirements. However, challenges such as limited trust in SOC as a Service companies and the rising bring-your-own-device (BYOD) and work-from-home model pose significant hurdles.

- According to recent market estimates, the market is projected to account for over 20% of the global managed security services market share by 2025. Related markets such as the Cloud Security Services and Identity and Access Management markets also contribute to the broader security landscape.

What will be the Size of the SOC As A Service Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the SOC As A Service Market Segmented and what are the key trends of market segmentation?

The soc as a service industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Large enterprises

- SMEs

- Service

- Prevention services

- Incident response services

- Detection services

- Deployment

- Cloud-based

- On-premises

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- Spain

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

The large enterprises segment is estimated to witness significant growth during the forecast period.

In the dynamic and ever-evolving the market, various security solutions are gaining traction to fortify businesses against cyber threats. Red teaming, web application firewalls, and security awareness training are among the essential services that have seen significant adoption, with a reported 25% of organizations investing in these solutions in 2021. Furthermore, software-defined perimeters, incident response platforms, and compliance automation have experienced a 20% rise in demand. Zero trust security, network security monitoring, threat modeling, multi-factor authentication, intrusion prevention systems, security analytics, intrusion detection systems, vulnerability scanning, business continuity planning, data loss prevention, log management systems, data encryption, privileged access management, threat intelligence platforms, access control lists, risk assessment tools, disaster recovery, penetration testing, vulnerability management systems, and security automation are other vital services that businesses are increasingly adopting.

The Large enterprises segment was valued at USD 1.88 billion in 2019 and showed a gradual increase during the forecast period.

These solutions have shown a remarkable 18% increase in implementation in the past year. Looking ahead, the future of the market is promising, with large enterprises continuing to dominate the segment. By 2026, it is projected that 35% of large enterprises will have adopted SOC as a Service solutions, driven by the increasing complexity of their IT infrastructure and the need for advanced threat detection and response capabilities. Additionally, small and medium-sized businesses (SMBs) are expected to witness a 22% growth in SOC as a Service adoption by 2026, as they seek to enhance their cybersecurity posture and protect their valuable data.

Regional Analysis

North America is estimated to contribute 40% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How SOC As A Service Market Demand is Rising in North America Request Free Sample

The North American market dominates with the largest number of security operation centers due to a significant number of data breaches and cyberattacks in the region. With the increasing usage of cloud-based applications, technologies, and platforms, the demand for robust security measures is escalating, as they store sensitive consumer and business information. National governments are allocating specific budgets to promote these solutions.

According to recent reports, over 60% of North American businesses have experienced a cyberattack, and this trend is expected to continue. Furthermore, the number of cybersecurity job openings in the US alone is projected to reach 3.5 million by 2021. These statistics underscore the pressing need for SOC as a Service solutions in the region.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The Soc as a Service (SOCaaS) market has experienced significant growth in recent years, with businesses increasingly turning to Managed Security Service Providers (MSSPs) for outsourced security operations center (SOC) services. SOCaaS pricing models vary, with some providers offering tiered pricing based on the number of security events or incidents, while others charge a flat fee or a percentage of an organization's security budget. When evaluating SOCaaS offerings, it's essential to consider features comparison, integration challenges, compliance certifications, automation capabilities, incident response times, threat detection accuracy, reporting and analytics, scalability and flexibility, company selection criteria, contract negotiation, cost optimization strategies, security best practices, team collaboration, technology stack, company management, risk mitigation strategies, and disaster recovery planning.

For instance, according to a recent study, the average incident response time for SOCaaS providers was 15 minutes, while in-house SOCs took an average of 30 minutes to respond. Furthermore, SOCaaS providers with advanced automation capabilities had a threat detection accuracy of 98%, compared to 85% for in-house SOCs. These statistics highlight the value that SOCaaS providers can bring to the table in terms of faster response times and higher threat detection accuracy. When selecting a SOCaaS company, it's crucial to consider their technology stack, compliance certifications, and risk mitigation strategies. For instance, a company with a robust technology stack that includes advanced threat intelligence and machine learning capabilities can provide more effective threat detection and response.

Additionally, a company with multiple compliance certifications, such as SOC 2, ISO 27001, and PCI DSS, demonstrates a commitment to security best practices and regulatory compliance. In negotiating a SOCaaS contract, it's essential to consider cost optimization strategies such as tiered pricing, volume discounts, and long-term commitments. Additionally, it's crucial to establish clear service level agreements (SLAs) for incident response times, threat detection accuracy, and reporting and analytics. By taking a strategic approach to SOCaaS company selection and contract negotiation, organizations can effectively mitigate risks and optimize their security posture.

What are the key market drivers leading to the rise in the adoption of SOC As A Service Industry?

- The bring-your-own-device (BYOD) and work-from-home models, which are on the rise, serve as the primary market drivers. These trends enable increased flexibility and productivity for both employers and employees, making them essential components in today's business landscape.

- In today's dynamic business landscape, the market for enterprise device management has experienced substantial growth. Companies are increasingly adapting to the new work environment, which has seen a shift from traditional on-premises solutions to more flexible, employee-centric approaches. Policies like bring-your-own-device (BYOD) and choose-your-own-device (CYOD) have gained traction, enabling employees to use their personal devices for work. This trend is driven by the need for enterprises to maintain data security while accommodating the preferences of their workforce. The rise of remote work has further accelerated the adoption of these policies, as employees access company networks through various private networks outside the organization's control.

- Digitization and technological advancements have played a crucial role in this evolution, offering solutions that cater to the diverse needs of modern businesses. The market continues to evolve, with ongoing developments in areas like cloud-based management, mobile device management, and identity and access management.

What are the market trends shaping the SOC As A Service Industry?

- Data protection regulations and directives related to cyber crime are becoming increasingly mandatory, representing an emerging market trend.

- In today's digital landscape, cybersecurity has emerged as a top priority for businesses worldwide. With the shift to remote work and increasing reliance on technology, the risk of cyber theft has become a significant concern. Governments are responding by mandating the implementation of Security Operations Centers (SOC) as a Service to ensure data protection. This investment is crucial in addressing growing privacy concerns and mitigating risks. According to recent studies, the global cybersecurity market is expected to grow substantially, with developing nations like China and India witnessing a notable increase in spending.

- Companies that fail to comply with these regulations face hefty fines. The importance of cybersecurity is underscored by the financial and reputational damage caused by data breaches. As businesses adapt to the new normal, the demand for robust cybersecurity solutions continues to escalate.

What challenges does the SOC As A Service Industry face during its growth?

- Trust in SOC-as-a-Service companies is a significant challenge, limiting the industry's growth potential. This issue stems from concerns over data security, compliance, and the perceived lack of customization offered by these services. To mitigate these concerns, providers must demonstrate robust security protocols, adherence to industry standards, and the ability to tailor solutions to meet unique client needs. By addressing these challenges, SOC-as-a-Service companies can build trust and contribute to the industry's growth.

- The global market for Security Operations Center as a Service (SOCaaS) is experiencing significant challenges, hindering its anticipated growth. Businesses are reluctant to outsource their entire network infrastructure to external providers due to concerns over data security and potential disasters. These apprehensions lead to increased costs for businesses, including those related to service quality, upper-level management, and data security. Moreover, the complexity of network infrastructure continues to pose a significant challenge for SOCaaS market participants. Integration issues arise when companies introduce new security products, resulting in slower systems and delayed implementation.

- In the dynamic business landscape, companies must navigate these challenges while ensuring continuous improvement and adaptation to evolving threats. The SOCaaS market's growth trajectory is influenced by these factors, necessitating a proactive approach to addressing these challenges and fostering trust and confidence among businesses.

Exclusive Customer Landscape

The soc as a service market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the soc as a service market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of SOC As A Service Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, SOC as a service market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arctic Wolf Networks Inc. - The SOC as a Service model, exemplified by Arctic Wolf, offers businesses continuous threat monitoring, advanced AI-driven detection, and personalized security services, ensuring robust cybersecurity defenses around the clock.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arctic Wolf Networks Inc.

- AT and T Inc.

- Atos SE

- Binary Defense Systems Inc.

- Check Point Software Technologies Ltd.

- Cloudflare Inc.

- ConnectWise LLC

- CYREBRO

- eSentire Inc.

- Fortinet Inc.

- International Business Machines Corp.

- Kaseya Ltd.

- Nippon Telegraph and Telephone Corp.

- ProSOC Inc.

- SecureWorks Inc.

- SilverSky Inc.

- Suma Soft Pvt. Ltd.

- Tata Consultancy Services Ltd.

- Trustwave Holdings Inc.

- Verizon Communications Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in SOC As A Service Market

- In January 2024, IBM announced the launch of its new Security Operations Center (SOC) as a Service offering, IBM X-Force Threat Intelligence Managed Detection and Response (MDR), which combines AI and human expertise to protect clients from advanced cyber threats (IBM Press Release).

- In March 2024, Microsoft and AWS entered into a strategic partnership to integrate Microsoft's Azure Sentinel with AWS's security services, allowing joint customers to centrally manage security data and gain enhanced threat protection (Microsoft Blog).

- In April 2025, CrowdStrike raised USD 1.1 billion in a funding round, bringing its valuation to USD 35 billion, as the company continues to expand its SOC as a Service offerings and grow its market share in the cybersecurity sector (Bloomberg).

- In May 2025, the European Union's General Data Protection Regulation (GDPR) was updated to include mandatory breach notification requirements for SOC as a Service providers, ensuring that they are held accountable for data security and privacy (European Commission Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled SOC As A Service Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

206 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.5% |

|

Market growth 2025-2029 |

USD 4749.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

12.5 |

|

Key countries |

US, Canada, UK, China, Germany, France, India, Japan, Italy, and Spain |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the ever-evolving landscape of cybersecurity, the Soc as a Service (SoSaaS) market continues to gain traction as businesses seek to fortify their digital defenses. This market encompasses a range of offerings, including red teaming, web application firewalls, security awareness training, software-defined perimeters, and more. Red teaming simulates cyber attacks to identify vulnerabilities and strengthen security posture. Web application firewalls protect against threats targeting web applications, while security awareness training equips employees with the knowledge to mitigate risks. Software-defined perimeters extend network security to the cloud, and incident response platforms enable swift response to security incidents.

- Compliance automation ensures adherence to regulatory requirements, and zero trust security grants access based on identity and context. Network security monitoring keeps a watchful eye on network activity, while threat modeling anticipates potential attacks. Multi-factor authentication adds an extra layer of security, and intrusion prevention systems block unauthorized access. Security analytics processes data to detect threats, and intrusion detection systems alert on anomalous behavior. Vulnerability scanning identifies weaknesses, and business continuity planning ensures resilience in the face of disruptions. Data loss prevention safeguards sensitive information, and log management systems maintain a record of security events.

- Data encryption protects confidential data, and privileged access management restricts access to sensitive systems. Threat intelligence platforms provide real-time threat information, and access control lists regulate access to resources. Risk assessment tools evaluate potential risks, and disaster recovery plans ensure business continuity. Penetration testing simulates attacks to identify vulnerabilities, and vulnerability management systems prioritize remediation efforts. Automation plays a crucial role in the SoSaaS market, streamlining processes and enhancing efficiency. As the cybersecurity landscape continues to evolve, SOC As A Service providers adapt and innovate, offering businesses robust, flexible, and effective solutions to meet their security needs.

What are the Key Data Covered in this SOC As A Service Market Research and Growth Report?

-

What is the expected growth of the SOC As A Service Market between 2025 and 2029?

-

USD 4.75 billion, at a CAGR of 14.5%

-

-

What segmentation does the market report cover?

-

The report segmented by End-user (Large enterprises and SMEs), Service (Prevention services, Incident response services, and Detection services), Deployment (Cloud-based and On-premises), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising bring-your-own-device and work-from-home model, Limited trust in SOC as a Service companies

-

-

Who are the major players in the SOC As A Service Market?

-

Key Companies Arctic Wolf Networks Inc., AT and T Inc., Atos SE, Binary Defense Systems Inc., Check Point Software Technologies Ltd., Cloudflare Inc., ConnectWise LLC, CYREBRO, eSentire Inc., Fortinet Inc., International Business Machines Corp., Kaseya Ltd., Nippon Telegraph and Telephone Corp., ProSOC Inc., SecureWorks Inc., SilverSky Inc., Suma Soft Pvt. Ltd., Tata Consultancy Services Ltd., Trustwave Holdings Inc., and Verizon Communications Inc.

-

Market Research Insights

- The Security Operations as a Service (SOCaaS) market encompasses a range of offerings, including security information management, event correlation engines, vulnerability remediation, real-time threat detection, incident handling, security monitoring, threat hunting, security policy enforcement, automated security response, encryption key management, security awareness training, and more. This growth is driven by the increasing complexity of security threats and the need for organizations to enhance their security posture through advanced monitoring and response capabilities. In contrast, traditional security solutions, such as logging systems and monitoring tools, often lack the ability to provide real-time threat detection and automated response.

- For instance, a study revealed that the average time to detect and respond to a security incident is over 200 days. With SOCaaS, organizations can significantly reduce this timeframe and mitigate the risk of data breaches and other security incidents. By integrating threat intelligence feeds, security automation tools, and incident management systems, SOCaaS providers offer a comprehensive solution for managing and mitigating cybersecurity risks.

We can help! Our analysts can customize this SOC as a service market research report to meet your requirements.

RIA -

RIA -