Service Integration And Management Market Size 2026-2030

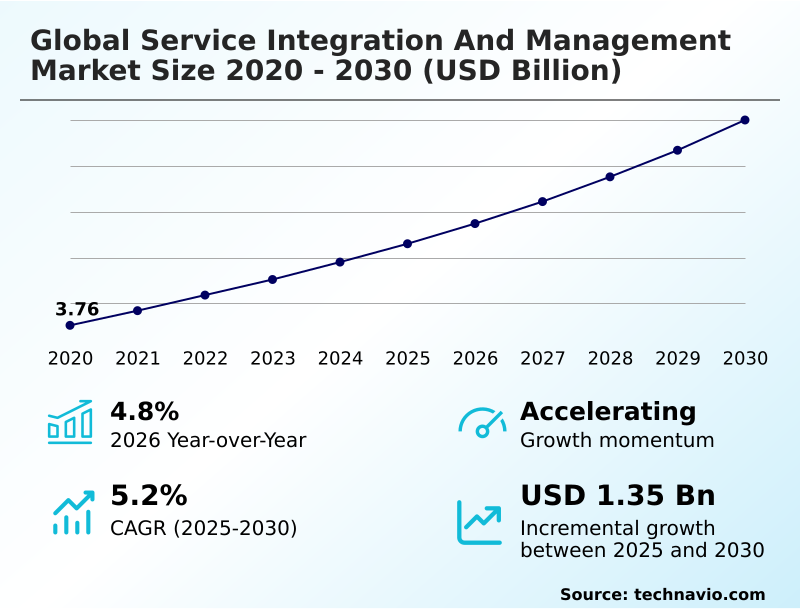

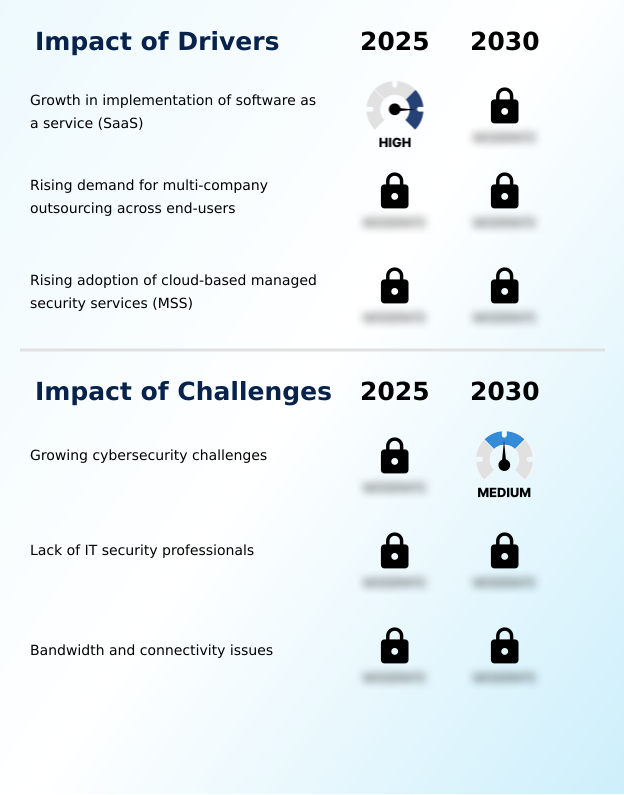

The service integration and management market size is valued to increase by USD 1.35 billion, at a CAGR of 5.2% from 2025 to 2030. Growth in implementation of software as a service (SaaS) will drive the service integration and management market.

Major Market Trends & Insights

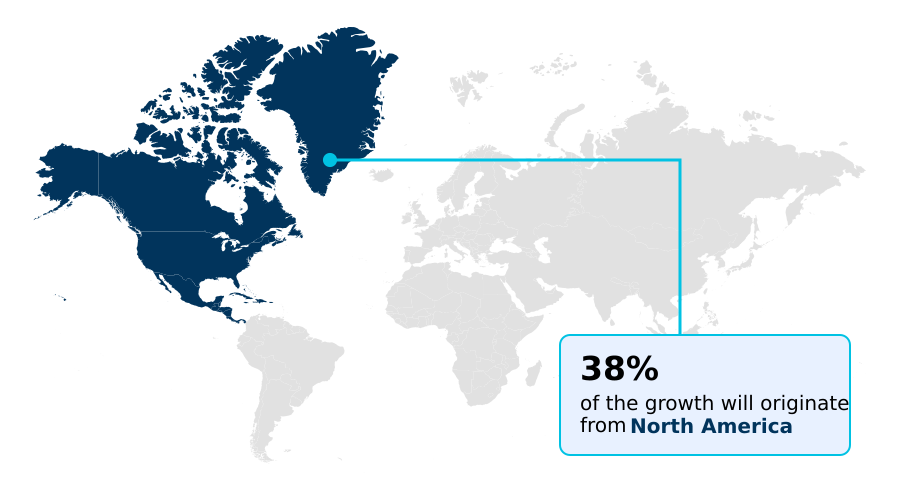

- North America dominated the market and accounted for a 38.4% growth during the forecast period.

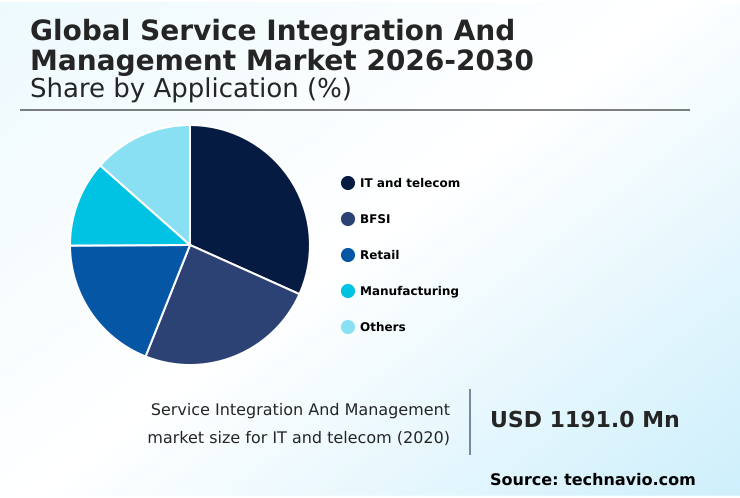

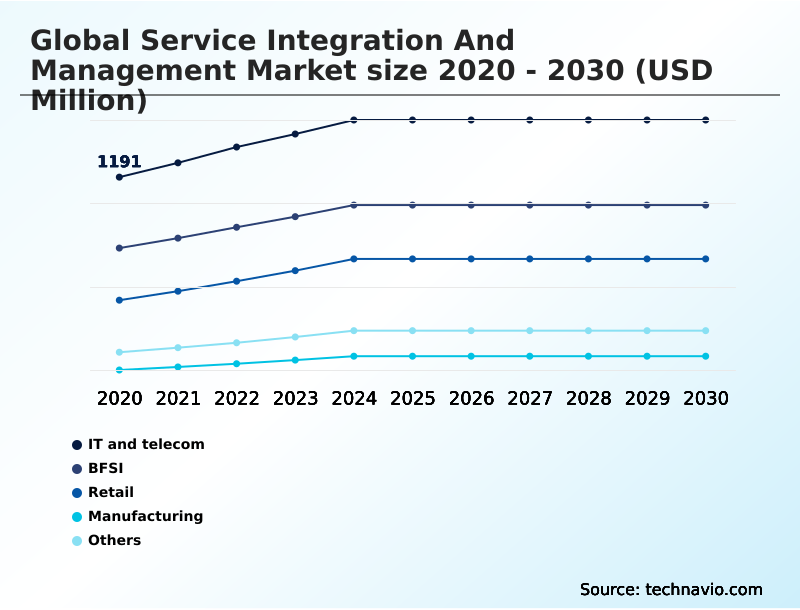

- By Application - IT and telecom segment was valued at USD 1.41 billion in 2024

- By Component - Services segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.24 billion

- Market Future Opportunities: USD 1.35 billion

- CAGR from 2025 to 2030 : 5.2%

Market Summary

- The service integration and management market is defined by the enterprise need to impose order on complex, multi-vendor IT environments. As organizations increasingly source specialized capabilities from different providers, a structured framework becomes essential for maintaining operational coherence and achieving business objectives.

- Key drivers include the proliferation of hybrid cloud architectures and the adoption of best-of-breed SaaS applications, which fragment the IT landscape. A primary trend involves leveraging AI-driven platforms for predictive service management, enabling proactive issue resolution.

- For instance, a financial services firm managing multiple fintech partners utilizes a service integration model to enforce uniform security protocols and ensure seamless data flow, which is critical for meeting stringent regulatory compliance standards. This approach provides a unified view of performance, ensuring all suppliers, from cloud hosting to payment processing, contribute to a consistent end-user experience.

- However, the inherent complexity of aligning diverse service level agreements and managing data security across numerous third parties remains a significant challenge, requiring robust governance and cross-functional collaboration.

What will be the Size of the Service Integration And Management Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Service Integration And Management Market Segmented?

The service integration and management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- IT and telecom

- BFSI

- Retail

- Manufacturing

- Others

- Component

- Services

- Solutions

- Service type

- Single‑provider model

- Hybrid‑provider model

- Internal service integrator model

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Application Insights

The it and telecom segment is estimated to witness significant growth during the forecast period.

The information technology and telecommunications sector represents a substantial part of the market, driven by the complexity of modern network infrastructures and the shift to multi-cloud environments.

Telecom operators transitioning to 5G and open radio access networks must manage a disaggregated IT supply chain, making a cohesive service delivery model essential.

This requires a robust service integrator layer for multi-sourcing service integration to maintain service level agreement management and ensure interoperability. The demand management process for new services and asset management across vendors must be centralized.

An effective IT operating model with strong multi-sourcing governance is critical, as it enhances IT supply chain efficiency and supports service transition management.

This structured approach, rooted in ITIL process alignment, improves service continuity planning and has been shown to boost service delivery consistency by over 20%.

The IT and telecom segment was valued at USD 1.41 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Service Integration And Management Market Demand is Rising in North America Request Free Sample

Geographically, the market is led by North America, which accounts for over 38% of demand due to the early adoption of advanced IT operating models and a high concentration of managed service providers.

The region's mature approach to a business outcome-based model is evident, with enterprises actively consolidating fragmented IT environments.

The primary driver is the aggressive shift to hybrid architectures, which demands a robust service delivery framework for managing distinct service level agreements.

The integration of generative AI into a centralized service desk has also accelerated demand for next-gen models that prioritize automation, with some organizations reporting a 20% reduction in mean time to resolution.

Meanwhile, APAC is the fastest-growing region, fueled by rapid digitalization and the increasing complexity of the IT value chain integration, reflecting a global trend toward more structured digital transformation journeys.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Successfully navigating the complexities of modern IT requires a strategic approach to managing multiple vendors in IT. The journey often begins with the realization that an ad-hoc approach is unsustainable, pushing organizations toward establishing centralized governance for IT services. The primary goal is improving IT service delivery quality while reducing operational costs with SIAM.

- The role of the service integrator function is pivotal, acting as the central point of control and coordination. Adhering to SIAM implementation best practices is crucial for realizing the full benefits of multi-sourcing integration. A key distinction arises when comparing the SIAM framework vs traditional ITSM; the former is specifically designed to handle the challenges in a multi-vendor environment.

- The process of selecting the right SIAM provider demands careful evaluation of capabilities and cultural fit. Organizations are focused on measuring the success of SIAM implementation through clear metrics tied to business goals. Service orchestration in multi-cloud settings has become a critical capability, necessitating a flexible governance model for IT outsourcing.

- This includes automating service level agreement tracking to ensure compliance. For businesses wondering how to build a SIAM model, the focus should be on achieving end-to-end visibility in IT services. This helps in aligning suppliers with business goals and efficiently managing contracts in a multi-vendor setup, ultimately creating a single source of truth.

- Enterprises that formalize this process report vendor alignment rates that are nearly twice as effective as those that do not.

What are the key market drivers leading to the rise in the adoption of Service Integration And Management Industry?

- The accelerated implementation of Software-as-a-Service (SaaS) models across enterprises stands as a key driver fueling the market's expansion.

- The proliferation of SaaS applications is a primary market driver, creating a complex multi-provider management challenge that necessitates a formal service orchestration framework.

- As enterprises adopt best-of-breed tools, an effective tooling integration strategy becomes critical for maintaining operational cohesion and ensuring data sovereignty compliance.

- This has led to an uptick in the use of api-driven integration and robotic process automation to connect disparate systems, with leading firms automating up to 40% of routine service requests.

- A cohesive IT sourcing strategy is now essential for managing this ecosystem. Advanced provider collaboration tools and a unified approach to enterprise service management enable organizations to harness the full potential of their software investments.

- This focus on process orchestration improves service delivery automation, helping achieve over 99.5% uptime for critical business applications.

What are the market trends shaping the Service Integration And Management Industry?

- A primary market trend is the increasing demand for low-cost IT infrastructure. This shift is compelling organizations to adopt more efficient and cost-effective service delivery models.

- A significant trend shaping the market is the enterprise-wide drive for IT cost optimization, compelling a shift toward more agile and lean operational frameworks. Organizations are leveraging hybrid cloud governance to balance performance with expenditure, using a sophisticated service portfolio management approach to rationalize applications and infrastructure. This enables better end-to-end service delivery across a multi-vendor landscape.

- By implementing a unified service catalog, businesses can achieve greater transparency, with some reporting a 15% reduction in redundant IT spending. Furthermore, a robust IT governance model supported by a chargeback and showback model enhances accountability.

- This strategic focus not only helps in vendor lock-in mitigation but also strengthens operational resilience, ensuring that cost-saving measures do not compromise service quality or availability in the long term.

What challenges does the Service Integration And Management Industry face during its growth?

- The continuous escalation of sophisticated cybersecurity threats presents a significant challenge to the industry's growth and stability.

- A primary challenge is ensuring robust information security management across a distributed supplier ecosystem management. With multiple vendors comes a fragmented security posture, increasing the attack surface and complicating contractual obligation tracking for compliance. Establishing a comprehensive performance management framework that includes security metrics is essential for mitigating risks.

- This requires intense cross-functional collaboration and a strong relationship management framework between the client and each provider. An effective IT service management framework must extend beyond technical performance to include security governance, yet organizations report that aligning security policies across vendors can increase onboarding time by up to 25%.

- Without ecosystem orchestration for security and a clear operational level agreement for incident response, the risk of breaches rises, impacting end-user experience monitoring and overall business continuity.

Exclusive Technavio Analysis on Customer Landscape

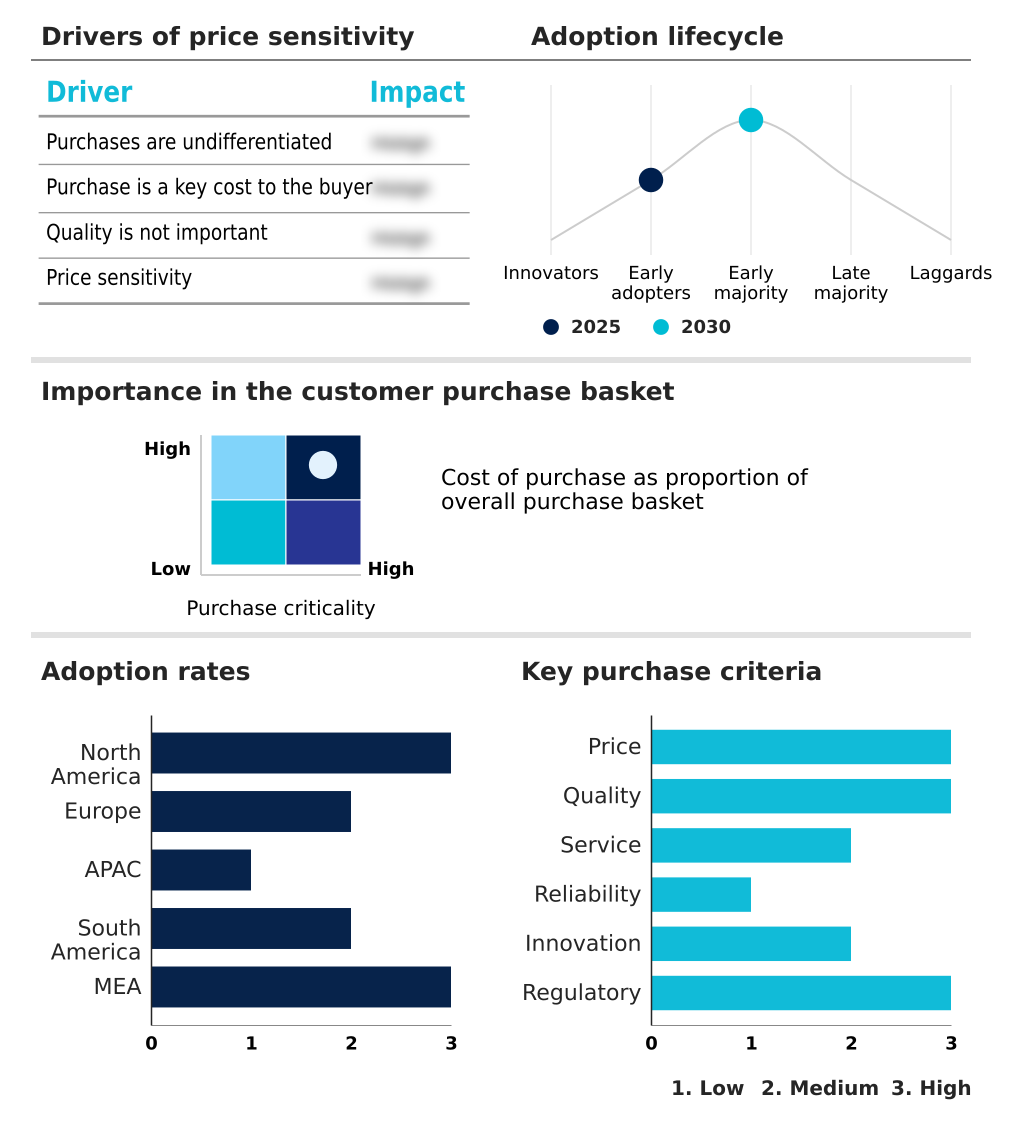

The service integration and management market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the service integration and management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Service Integration And Management Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, service integration and management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Atos SE - Provides multi-sourcing service integration solutions engineered to streamline and optimize the management of complex, multi-provider service ecosystems for enhanced operational efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Atos SE

- BAE Systems Plc

- Capgemini Service SAS

- CGI Inc.

- Cisco Systems Inc.

- DXC Technology Co.

- Fujitsu Ltd.

- HCL Technologies Ltd.

- IBM Corp.

- Infosys Ltd.

- NTT DATA Corp.

- ServiceNow Inc.

- Tata Consultancy Services

- Tietoevry

- Wipro Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Service integration and management market

- In September 2024, IBM announced its definitive agreement to acquire HashiCorp, a strategic move designed to enhance its portfolio with advanced multi-cloud infrastructure automation capabilities, which are fundamental to modern service integration.

- In November 2024, Kyndryl and Google Cloud announced an expanded partnership to develop generative AI solutions, aiming to help customers accelerate data-driven business transformations through enhanced service visibility and integration.

- In February 2025, ServiceNow launched its new platform release, which includes advanced AI-powered features for intelligent automation, designed to streamline complex workflows and improve coordination across multi-vendor IT environments.

- In April 2025, Oracle and Palantir Technologies formed a partnership to offer secure cloud and AI solutions aimed at government and defense clients, creating complex ecosystems that require advanced service integration frameworks for governance.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Service Integration And Management Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.2% |

| Market growth 2026-2030 | USD 1345.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.8% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The service integration and management market provides a structured it service management framework essential for organizations navigating complex, multi-vendor environments. This operational process governance enables end-to-end service delivery by creating a cohesive service integrator layer that manages a diverse supplier ecosystem management.

- It facilitates the it value chain integration and ensures that the overall service delivery model aligns with strategic business objectives through robust business service management. A key trend is the shift from manual oversight to an intelligent it governance model powered by AI, a boardroom-level topic influencing investment in it process automation.

- This move toward a sophisticated tooling integration strategy and service orchestration allows for predictive issue resolution and it cost optimization. Leading adopters have achieved a 30% reduction in incident escalation by leveraging a multi-vendor integration platform for proactive monitoring.

- The framework incorporates key processes like incident management, change management, and service catalog management, enabling effective hybrid cloud governance and ensuring data sovereignty compliance while driving cross-functional collaboration and a strong performance management framework.

What are the Key Data Covered in this Service Integration And Management Market Research and Growth Report?

-

What is the expected growth of the Service Integration And Management Market between 2026 and 2030?

-

USD 1.35 billion, at a CAGR of 5.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (IT and telecom, BFSI, Retail, Manufacturing, and Others), Component (Services, and Solutions), Service Type (Single‑provider model, Hybrid‑provider model, and Internal service integrator model) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growth in implementation of software as a service (SaaS), Growing cybersecurity challenges

-

-

Who are the major players in the Service Integration And Management Market?

-

Atos SE, BAE Systems Plc, Capgemini Service SAS, CGI Inc., Cisco Systems Inc., DXC Technology Co., Fujitsu Ltd., HCL Technologies Ltd., IBM Corp., Infosys Ltd., NTT DATA Corp., ServiceNow Inc., Tata Consultancy Services, Tietoevry and Wipro Ltd.

-

Market Research Insights

- Market dynamics are shifting as organizations increasingly adopt a business outcome-based model, moving beyond simple cost metrics to focus on value delivery. A unified service catalog is becoming standard for improving service discovery, with adoption rates increasing by 30% in mature enterprises.

- Effective supplier performance management, supported by robust provider collaboration tools, is critical for operational excellence, helping firms achieve a 15% improvement in vendor compliance alignment. The use of a centralized service desk within a broader enterprise service management strategy ensures consistent support.

- This approach, which emphasizes ecosystem orchestration and a clear service delivery framework, allows businesses to realize greater returns on their IT investments while enhancing overall operational resilience and agility in a competitive landscape.

We can help! Our analysts can customize this service integration and management market research report to meet your requirements.