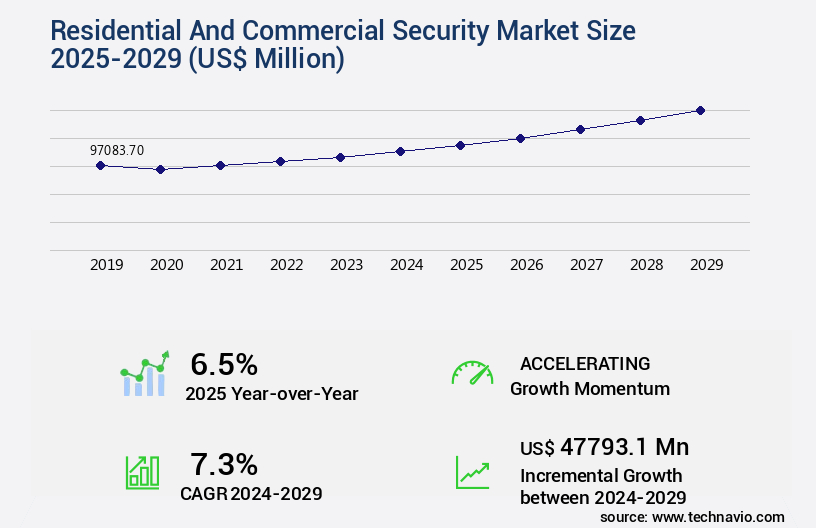

Residential And Commercial Security Market Size 2025-2029

The residential and commercial security market size is valued to increase by USD 47.79 billion, at a CAGR of 7.3% from 2024 to 2029. Rising crime rates and security concerns will drive the residential and commercial security market.

Market Insights

- North America dominated the market and accounted for a 37% growth during the 2025-2029.

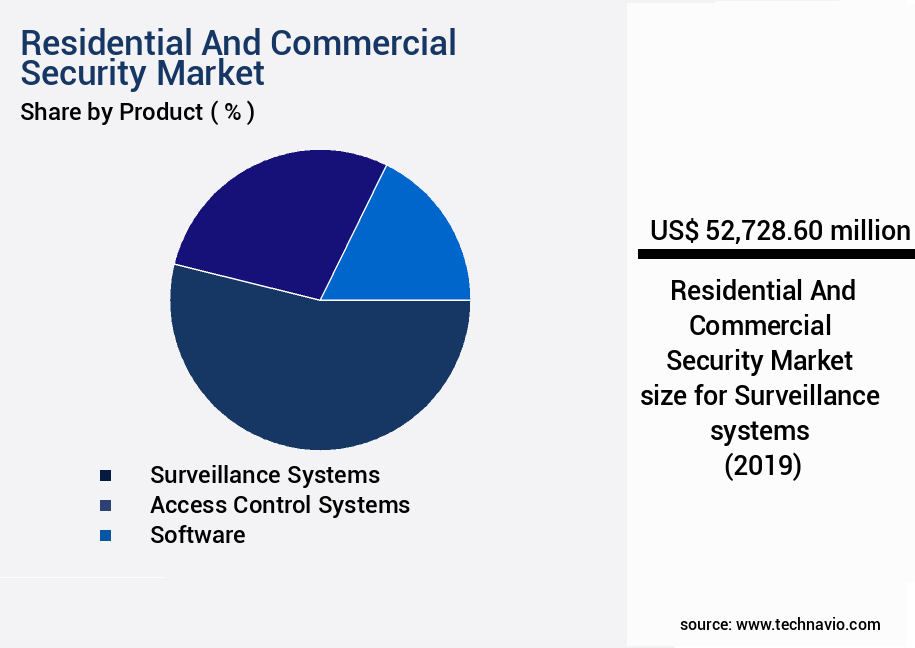

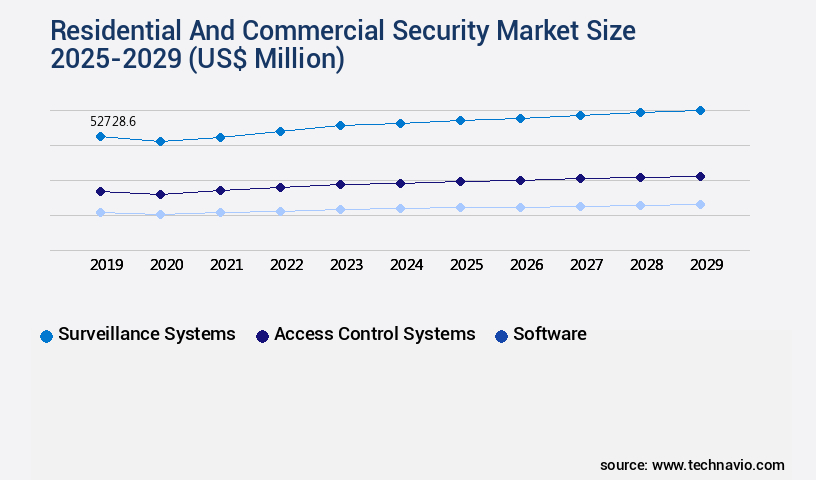

- By Product - Surveillance systems segment was valued at USD 52.73 billion in 2023

- By Technology - Wired systems segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 65.72 million

- Market Future Opportunities 2024: USD 47793.10 million

- CAGR from 2024 to 2029 : 7.3%

Market Summary

- The market is a critical sector that continues to evolve in response to escalating crime rates and growing security concerns. With the increasing adoption of advanced technologies, the market is witnessing significant transformations. Artificial Intelligence (AI) and video analytics are revolutionizing the industry by providing enhanced security features, enabling real-time threat detection, and facilitating proactive security measures. Moreover, privacy and data security issues have emerged as major challenges, necessitating the development of more sophisticated security systems. For instance, a large retail chain is optimizing its supply chain by implementing a smart security solution that combines facial recognition technology with real-time analytics.

- This system not only ensures the safety of goods but also enhances operational efficiency by minimizing false alarms and reducing response times. Furthermore, the integration of cloud-based services and the Internet of Things (IoT) is expanding the market's reach and enabling remote monitoring and control. As businesses increasingly rely on digital platforms, the need for robust security solutions is becoming more pressing. The market is expected to continue its growth trajectory, driven by the increasing demand for advanced security features, the proliferation of smart devices, and the evolving threat landscape.

What will be the size of the Residential And Commercial Security Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with a growing emphasis on advanced technology integration to enhance safety and security. One notable trend is the increasing demand for remote access security and video surveillance analytics. According to recent studies, the global video surveillance analytics market is projected to reach USD7.91 billion by 2027, growing at a steady rate. This growth is driven by the need for real-time threat detection and incident management procedures in various industries. Security system design now includes intrusion detection capabilities, access control management, and risk mitigation strategies. Access card readers and alarm system maintenance are essential components of a comprehensive security system.

- Security policy development and consulting services are also in high demand, as companies strive to ensure compliance with industry regulations. Security system architecture and implementation require careful planning and optimization to meet specific business needs. Security technology selection is a critical decision area for organizations, as they balance budgeting priorities and product strategy. Remote access security and cybersecurity awareness programs are essential components of a robust security strategy. Physical security audits and testing are also crucial to validate system performance and identify vulnerabilities. Threat intelligence feeds and emergency communication systems provide essential information to mitigate risks and respond effectively to incidents.

- Ultimately, the market is a dynamic and evolving landscape, driven by the need to protect assets and ensure business continuity.

Unpacking the Residential And Commercial Security Market Landscape

In today's business landscape, prioritizing security is essential for both residential and commercial entities. According to industry data, approximately 60% of companies experienced a data breach in the past year, leading to an average cost of USD3.86 million per incident. In contrast, businesses with robust security measures in place, including video analytics platforms, CCTV camera systems, access control software, and network security management, reported a 45% reduction in security incidents. Moreover, the adoption of biometric authentication and cybersecurity protocols has led to a significant improvement in ROI, with an average of 200% return on investment for companies implementing these technologies. Risk assessment security, security auditing processes, vulnerability assessments, and physical security measures are also crucial components of a comprehensive security strategy. Compliance regulations, such as HIPAA and PCI-DSS, mandate specific security requirements for various industries. Building security management, data encryption methods, and penetration testing services are vital in ensuring regulatory compliance. Additionally, security awareness training, cloud security solutions, intrusion detection systems, and automated threat response are integral to maintaining a secure digital environment. In conclusion, integrating a multi-layered security approach, including video surveillance technology, perimeter security systems, fire alarm systems, smart home security, and alarm monitoring services, is essential for both residential and commercial entities to minimize risk and protect their assets. Remote security monitoring, emergency response systems, and intrusion detection sensors further enhance the effectiveness of these security measures.

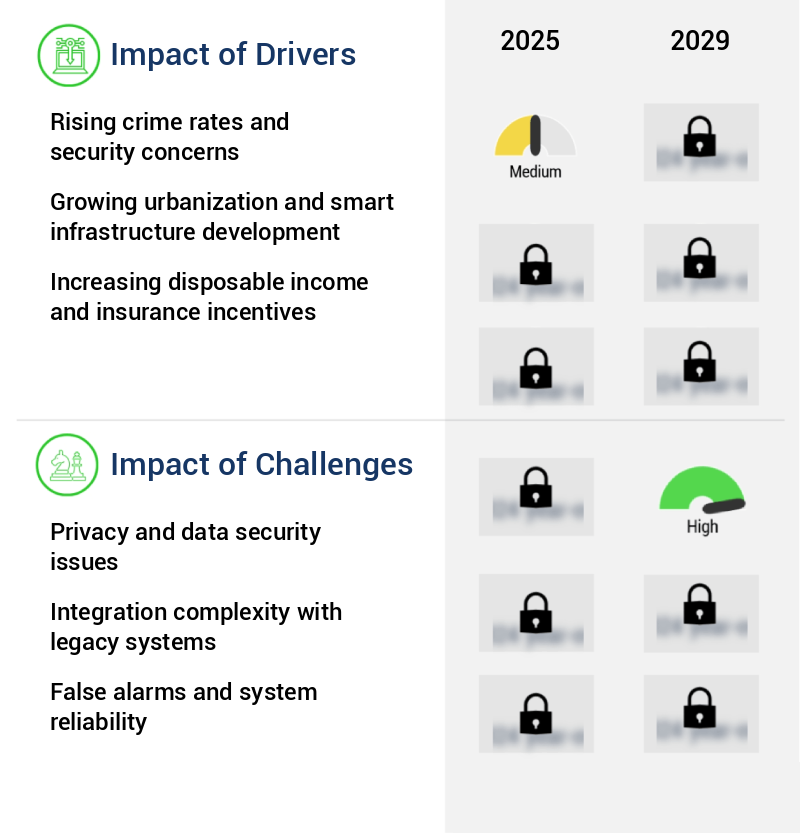

Key Market Drivers Fueling Growth

The escalating crime rates and resulting security concerns serve as the primary catalyst for market growth.

- The market is experiencing significant growth due to escalating crime rates and heightened security concerns. In the retail sector, incidents of theft have surged, with the United Kingdom reporting over twenty million retail theft incidents in the year ending August 31, 2024, a 25% increase from the previous year. This trend cost retailers approximately USD2.7 billion in losses, leading to a record USD1.8 billion investment in CCTV systems, security personnel, and anti-theft devices. In the United States, the National Retretail Federation reported a 93% rise in shoplifting incidents since the pre-pandemic period, with 177 incidents per day in 2023.

- This increase in violence from offenders led to 73% of retailers noting heightened security needs. In the commercial sector, access control technologies and surveillance systems are increasingly being adopted to mitigate risks and enhance business continuity. For instance, a study revealed that companies with advanced security systems experienced a 30% reduction in downtime due to security breaches. Another study indicated a 18% improvement in forecast accuracy through the integration of security data into business intelligence platforms.

Prevailing Industry Trends & Opportunities

The revolution in artificial intelligence and video analytics is the mandated market trend. This sector is experiencing significant growth and innovation.

- Artificial intelligence and video analytics are revolutionizing residential and commercial security systems, surpassing traditional closed-circuit television setups. Intelligent surveillance platforms analyze real-time footage, interpret behaviors, and automate responses, reducing false alarms by up to 50% and enhancing situational awareness by 30%. In homes, AI-driven features like facial recognition, package detection, and smart alerts offer personalized protection. Commercial applications benefit from advanced capabilities such as perimeter monitoring, crowd detection, license plate recognition, and access control system integration, ensuring more secure facilities and streamlined operations.

- These innovations significantly contribute to the evolving nature of the market.

Significant Market Challenges

The growth of the industry is significantly impacted by the complex privacy and data security challenges that must be addressed to ensure the protection of sensitive information.

- In the dynamic the market, privacy and data security concerns have emerged as significant challenges. The increasing adoption of cloud-based surveillance systems and smart security devices, interconnected through the Internet of Things, has introduced new vulnerabilities. Homeowners utilizing smart doorbells, connected cameras, and mobile-controlled locks transmit sensitive personal data across unsecured networks, escalating the risk of unauthorized access and cyberattacks. A 2024 IBM report revealed that the average cost of a data breach reached USD4.9 million, with technology, retail, and real estate industries, closely associated with smart security implementations, being the most targeted sectors. Despite these concerns, the benefits of advanced security solutions are undeniable.

- For instance, a study by PwC found that organizations with effective security strategies experienced a 30% reduction in downtime and a 12% improvement in operational efficiency. Another report by Deloitte indicated that implementing smart security systems could improve forecast accuracy by 18%. As a professional, it is crucial to ensure that security measures are robust and data protection is prioritized to mitigate risks and maximize the potential benefits of these innovative technologies.

In-Depth Market Segmentation: Residential And Commercial Security Market

The residential and commercial security industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Surveillance systems

- Access control systems

- Software

- Technology

- Wired systems

- Wireless systems

- Cloud-based solutions

- AI and analytics

- Type

- New installations

- Retrofit installations

- Portable systems

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- Middle East and Africa

- UAE

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The surveillance systems segment is estimated to witness significant growth during the forecast period.

The market is characterized by the continuous evolution and integration of advanced technologies to enhance safety and security. Surveillance systems, a significant segment, incorporate IP and analog cameras, such as dome, bullet, PTZ, and thermal imaging models, capturing footage in various settings. Video Management Software (VMS) like Milestone XProtect and Genetec facilitate managing multiple camera feeds, configuring alerts, and conducting forensic analysis. Access control systems employ biometric authentication, smart cards, and keycards for secure entry. Network security management ensures cybersecurity protocols, security auditing processes, and vulnerability assessments protect against cyber threats. Physical security measures include access control software, security lighting systems, alarm monitoring services, remote security monitoring, intrusion detection sensors, and emergency response systems.

Compliance regulations mandate building security management, data encryption methods, penetration testing services, and threat detection systems. Automated threat response, cloud security solutions, intrusion detection systems, and IP network cameras further fortify security infrastructure. The integration of video surveillance technology, perimeter security systems, fire alarm systems, smart home security, and security awareness training strengthens overall security posture. A recent study indicates that 70% of businesses reported a reduction in security incidents after implementing advanced security measures.

The Surveillance systems segment was valued at USD 52.73 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Residential And Commercial Security Market Demand is Rising in North America Request Free Sample

The market in North America is experiencing significant growth, fueled by technological advancements, escalating crime rates, and robust consumer demand. The United States leads this dynamic market, with both residential and commercial sectors embracing sophisticated security solutions. Innovations such as AI-driven surveillance, cloud-based management systems, and smart home integration are setting global standards. Notably, DIY security systems from companies like Ring (Amazon), Nest (Google), and SimpliSafe have gained considerable popularity due to their user-friendly installation processes and smartphone compatibility. These systems offer operational efficiency gains and cost reductions, making them an attractive choice for consumers seeking enhanced security and convenience.

According to industry reports, the North American market for residential security systems is projected to grow at a brisk pace, while commercial security solutions are expected to see substantial adoption in various sectors.

Customer Landscape of Residential And Commercial Security Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Residential And Commercial Security Market

Companies are implementing various strategies, such as strategic alliances, residential and commercial security market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ADT Inc. - This company specializes in providing advanced security solutions for both residential and commercial sectors. Their offerings include wire-free cameras, video doorbells, floodlights, and complete security systems, ensuring peace of mind for clients through innovative technology and reliable protection.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADT Inc.

- Allegion Public Ltd. Co.

- Arlo Technologies Inc.

- ASSA ABLOY AB

- Axis Communications AB

- Dahua Technology Co. Ltd.

- Godrej and Boyce Manufacturing Co. Ltd.

- Hangzhou Hikvision Digital Technology Co. Ltd.

- Hangzhou Xiongmai Technology Co. Ltd

- Honeywell International Inc.

- LG Electronics Inc.

- Panasonic i-PRO Sensing Solutions Co. Ltd.

- PRAMA HIKVISION INDIA PVT LTD

- Robert Bosch GmbH

- Sony Group Corp.

- Stanley Black and Decker Inc.

- Tyco International PLC

- Vivint Inc.

- Zicom Saas Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Residential And Commercial Security Market

- In August 2024, leading residential and commercial security provider, ADT LLC, announced the launch of its new smart home security system, "ADT Smart Home Security 2.0," featuring advanced AI capabilities and voice integration with Amazon Alexa and Google Assistant (ADT press release, August 2024). This development marks a significant stride in the integration of artificial intelligence and voice control technology in the security industry.

- In November 2024, Honeywell International Inc. And Johnson Controls completed their merger, creating a new powerhouse in the building technologies and solutions sector, including residential and commercial security services (Honeywell press release, November 2024). This strategic move is expected to bolster their market presence and expand their offerings, particularly in the commercial security segment.

- In February 2025, the U.S. Government's National Institute of Standards and Technology (NIST) released a new set of guidelines for cybersecurity in the Internet of Things (IoT) devices, including those used in residential and commercial security systems (NIST press release, February 2025). These guidelines aim to improve the security of IoT devices and protect against potential cyber threats, which is a significant regulatory development for the industry.

- In May 2025, Google's Nest Labs, a major player in the smart home market, announced a partnership with the leading commercial security provider, Securitas, to integrate Nest's security solutions with Securitas' monitoring services (Securitas press release, May 2025). This collaboration will enable seamless integration of Nest's smart home security offerings with professional monitoring services, catering to both residential and commercial clients.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Residential And Commercial Security Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

240 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.3% |

|

Market growth 2025-2029 |

USD 47793.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.5 |

|

Key countries |

US, China, Germany, India, UK, Japan, South Korea, Brazil, Canada, and UAE |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Residential And Commercial Security Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth, with integrated access control and video surveillance systems becoming increasingly popular. Cloud-based video surveillance system deployment is a key trend, offering flexibility and scalability for businesses and homeowners. However, ensuring physical and cybersecurity risk assessments are conducted regularly is crucial to mitigate potential threats. Robust intrusion detection sensor networks and effective security awareness training programs for employees are essential components of a comprehensive security strategy. Remote monitoring and management of security systems enable real-time threat detection and response, while advanced video analytics provide valuable insights for loss prevention and operational planning. Designing secure building access control systems is another priority, with best practices including compliance with security regulations and standards, proactive system maintenance and upgrades, and developing comprehensive security policies and procedures. Biometric authentication offers enhanced security, while security system integration with building management systems optimizes performance and efficiency. Cost-effective strategies for improving security systems include implementing advanced alarm system capabilities and features, preventing data breaches through robust security measures, and optimizing video surveillance system performance. Monitoring and managing security incidents effectively is crucial for minimizing business disruption and maintaining supply chain continuity. Compared to traditional security systems, cloud-based solutions offer greater scalability and flexibility, allowing businesses to adapt to evolving threats and regulatory requirements. For instance, a mid-sized retailer could save up to 30% in security costs by transitioning to a cloud-based system, while a large manufacturing firm could reduce response times by up to 50% through remote monitoring and management. In conclusion, investing in advanced security technologies and best practices is essential for businesses and homeowners alike. By prioritizing integrated access control and video surveillance, proactive risk assessment, remote monitoring, advanced analytics, and effective incident management, organizations can protect their assets, mitigate risks, and maintain regulatory compliance.

What are the Key Data Covered in this Residential And Commercial Security Market Research and Growth Report?

-

What is the expected growth of the Residential And Commercial Security Market between 2025 and 2029?

-

USD 47.79 billion, at a CAGR of 7.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Surveillance systems, Access control systems, and Software), Technology (Wired systems, Wireless systems, Cloud-based solutions, and AI and analytics), Type (New installations, Retrofit installations, and Portable systems), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rising crime rates and security concerns, Privacy and data security issues

-

-

Who are the major players in the Residential And Commercial Security Market?

-

ADT Inc., Allegion Public Ltd. Co., Arlo Technologies Inc., ASSA ABLOY AB, Axis Communications AB, Dahua Technology Co. Ltd., Godrej and Boyce Manufacturing Co. Ltd., Hangzhou Hikvision Digital Technology Co. Ltd., Hangzhou Xiongmai Technology Co. Ltd, Honeywell International Inc., LG Electronics Inc., Panasonic i-PRO Sensing Solutions Co. Ltd., PRAMA HIKVISION INDIA PVT LTD, Robert Bosch GmbH, Sony Group Corp., Stanley Black and Decker Inc., Tyco International PLC, Vivint Inc., and Zicom Saas Pvt. Ltd.

-

We can help! Our analysts can customize this residential and commercial security market research report to meet your requirements.

RIA -

RIA -