GCC Refractory Materials For Steel Industry Market Size 2026-2030

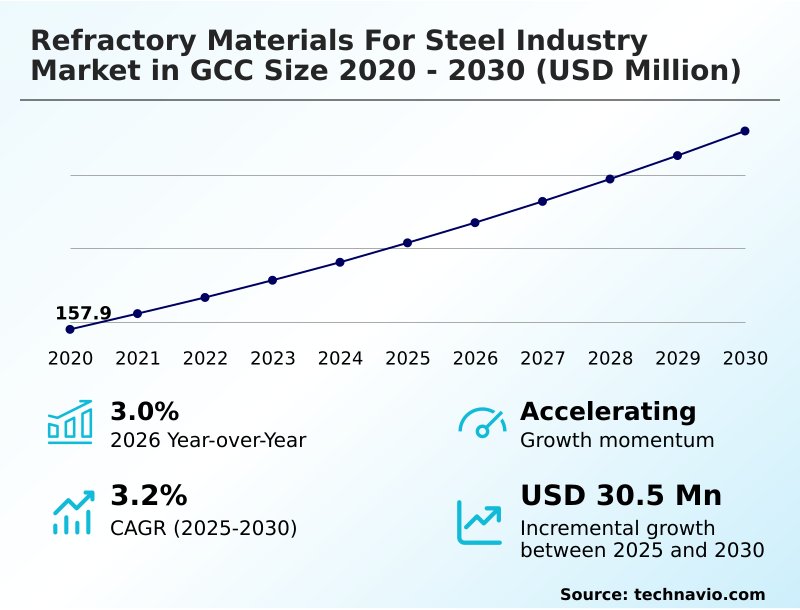

The gcc refractory materials for steel industry market size is valued to increase by USD 30.5 million, at a CAGR of 3.2% from 2025 to 2030. Growing steel production capacity across GCC countries will drive the gcc refractory materials for steel industry market.

Major Market Trends & Insights

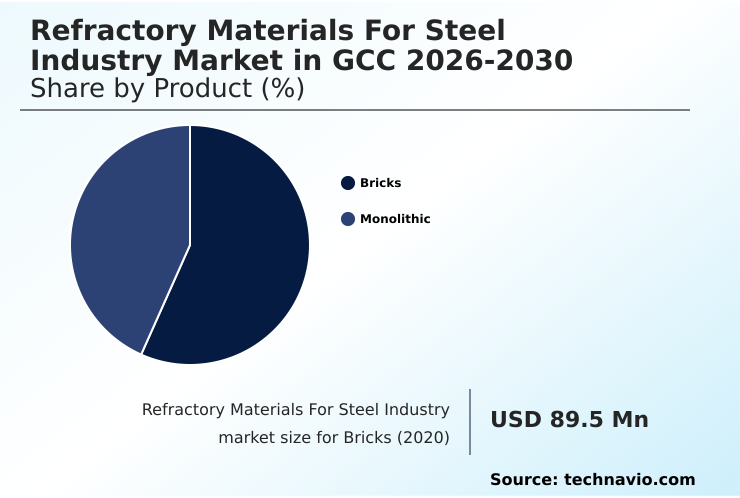

- By Product - Bricks segment was valued at USD 97.8 million in 2024

- By Type - Acidic and neutral segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 54.1 million

- Market Future Opportunities: USD 30.5 million

- CAGR from 2025 to 2030 : 3.2%

Market Summary

- The refractory materials for steel industry market in gcc is defined by a dynamic interplay of industrial expansion, technological advancement, and operational challenges. Growth is fundamentally tied to surging steel production, propelled by government-backed megaprojects that demand vast quantities of high-grade steel.

- This creates a consistent need for high-performance furnace linings and ladle linings capable of withstanding extreme thermal and chemical stress. A key trend shaping the landscape is the definitive shift from traditional shaped refractories toward versatile monolithic refractories.

- For instance, a steel plant involved in a critical infrastructure project can leverage advanced castables and gunning mixes for rapid furnace relining, significantly reducing maintenance downtime and accelerating project timelines. This pursuit of operational efficiency gains is balanced against persistent challenges, including the reliance on imported minerals like high-purity magnesia and graphite-based materials, which introduces supply chain volatility.

- Furthermore, the high energy consumption inherent in both refractory production and steelmaking puts continuous pressure on operational costs, driving demand for innovative materials that improve heat retention and support sustainable refractory solutions.

What will be the Size of the GCC Refractory Materials For Steel Industry Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the GCC Refractory Materials For Steel Industry Market Segmented?

The gcc refractory materials for steel industry industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

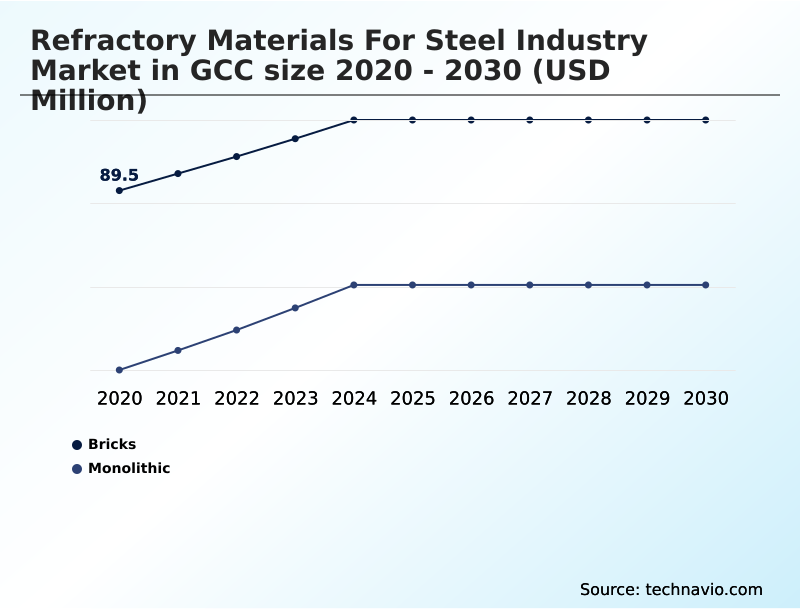

- Product

- Bricks

- Monolithic

- Type

- Acidic and neutral

- Basic

- Form factor

- Shaped refractories

- Unshaped refractories

- Geography

- GCC

By Product Insights

The bricks segment is estimated to witness significant growth during the forecast period.

The bricks segment is a foundational pillar within the refractory materials for steel industry market in gcc. These shaped refractories, including high-alumina bricks and magnesia-carbon bricks, are essential for the structural integrity of high-stress environments.

Demand is driven by expanding primary steel production, where predictable performance and long campaign lives are paramount for thermal management systems.

The integration of advanced manufacturing has enabled tighter tolerances, facilitating faster installation and superior resistance to slag penetration and molten metal flow engineering. This innovation is critical for steelmaking processes that prioritize purity and efficiency.

The market is shifting toward high-performance non-clay refractories, with advanced castables and binder systems improving operational uptime by up to 15% in secondary steelmaking processes.

The Bricks segment was valued at USD 97.8 million in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the refractory materials for steel industry market in gcc 2026-2030 hinges on a nuanced understanding of material performance, operational efficiency, and long-term cost. When evaluating acidic versus basic refractory selection criteria, steelmakers must consider the specific slag chemistry and thermal cycling of their processes.

- The growing preference for monolithic refractory installation techniques over traditional bricklaying is driven by the need for faster turnarounds and the benefits of joint-free monolithic linings. Key performance indicators focus on improving thermal shock resistance in refractories and enhancing refractory durability with new materials.

- For specialized applications, refractory solutions for electric arc furnaces and high-alumina brick applications in steelmaking remain critical areas of investment. Magnesia-carbon bricks for ladle linings are chosen based on their ability to mitigate refractory wear mechanisms in steel ladles.

- Challenges in refractory raw material sourcing are compelling firms to adopt predictive maintenance for furnace linings and explore robotic gunning for refractory repair. The impact of green steel on refractory demand is accelerating the adoption of sustainable practices in refractory manufacturing, supported by advanced castables for tundish applications.

- Forward-thinking companies utilize digital tools for refractory performance monitoring, with firms adopting this approach reporting maintenance planning accuracy that is twice that of those using traditional methods.

- Ultimately, a thorough lifecycle cost analysis of shaped refractories is essential to balance initial investment against long-term operational savings from energy savings with improved refractory insulation, aligning with the impact of slag chemistry on refractory choice.

What are the key market drivers leading to the rise in the adoption of GCC Refractory Materials For Steel Industry Industry?

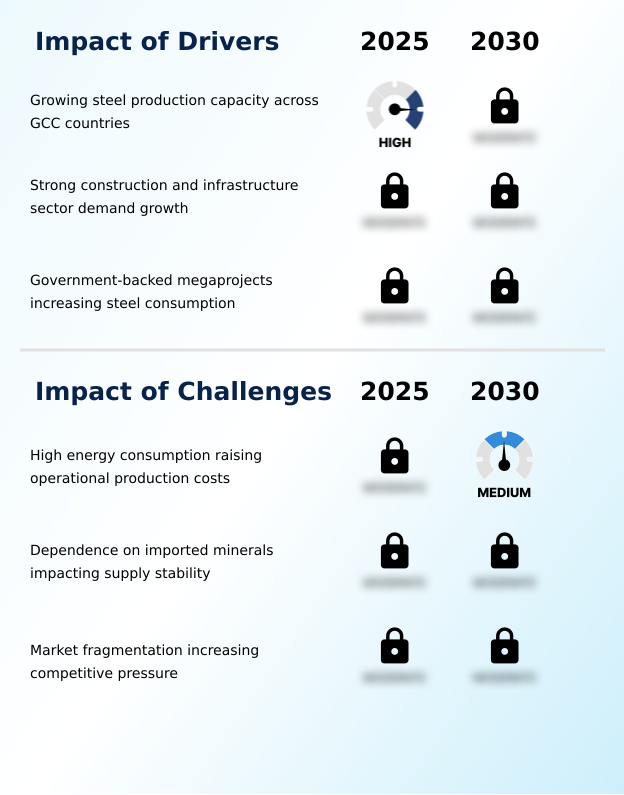

- The expansion of steel production capacity across GCC countries is a key driver fueling market growth.

- Market growth is primarily fueled by the aggressive expansion of steel production capacity, directly linked to government-backed megaprojects and infrastructure development.

- This surge in steel output, with some forecasts showing a consistent 5% year-over-year increase in demand, creates sustained consumption of refractory materials.

- Plant modernization efforts, focusing on energy-efficient processes and advanced furnace linings, are leading to a 15% improvement in thermal efficiency.

- The increasing prevalence of electric arc furnace (EAF) and direct reduced iron (DRI) technologies necessitates high-performance basic refractories and insulating firebricks.

- This demand for durable materials like magnesia-carbon bricks and advanced castables is a direct response to the need for greater furnace operational stability and reduced maintenance frequency in high-throughput environments.

What are the market trends shaping the GCC Refractory Materials For Steel Industry Industry?

- The increasing adoption of monolithic refractories over traditional bricks marks a significant upcoming trend in the market. This shift is driven by the pursuit of enhanced operational efficiency and superior lining performance.

- Key trends are reshaping the market, driven by the dual pursuit of operational efficiency and material longevity. The adoption of Industry 4.0 principles, including refractory lifecycle monitoring and predictive maintenance workflows, is enabling steelmakers to transition from reactive to proactive maintenance, reducing premature lining failures by up to 40%. Concurrently, material science advancements are delivering significant performance gains.

- New eco-friendly refractory formulations and monolithic refractories with superior thermal shock resistance and joint-free lining designs are cutting installation times by half compared to traditional bricklaying. This shift is supported by innovations in low-cement castables and binder systems, enhancing refractory durability and extending the service life of furnace linings and other high-temperature performance equipment.

What challenges does the GCC Refractory Materials For Steel Industry Industry face during its growth?

- High energy consumption, which elevates operational production costs, presents a key challenge to the industry's growth.

- The market faces significant headwinds from volatile operational expenditures and supply chain vulnerabilities. High energy consumption, a core aspect of both refractory manufacturing and steelmaking, is a major challenge, with energy price fluctuations contributing to a 20% variance in production costs for some producers.

- This financial pressure influences purchasing decisions, sometimes favoring lower-cost materials over those with better lining performance improvement. Additionally, the industry's dependence on imported raw materials like high-purity magnesia and graphite-based materials exposes it to geopolitical risks and logistical disruptions.

- These factors can extend raw material lead times by up to 60 days, impacting production schedules and challenging efforts to maintain consistent refractory wear and thermal management systems.

Exclusive Technavio Analysis on Customer Landscape

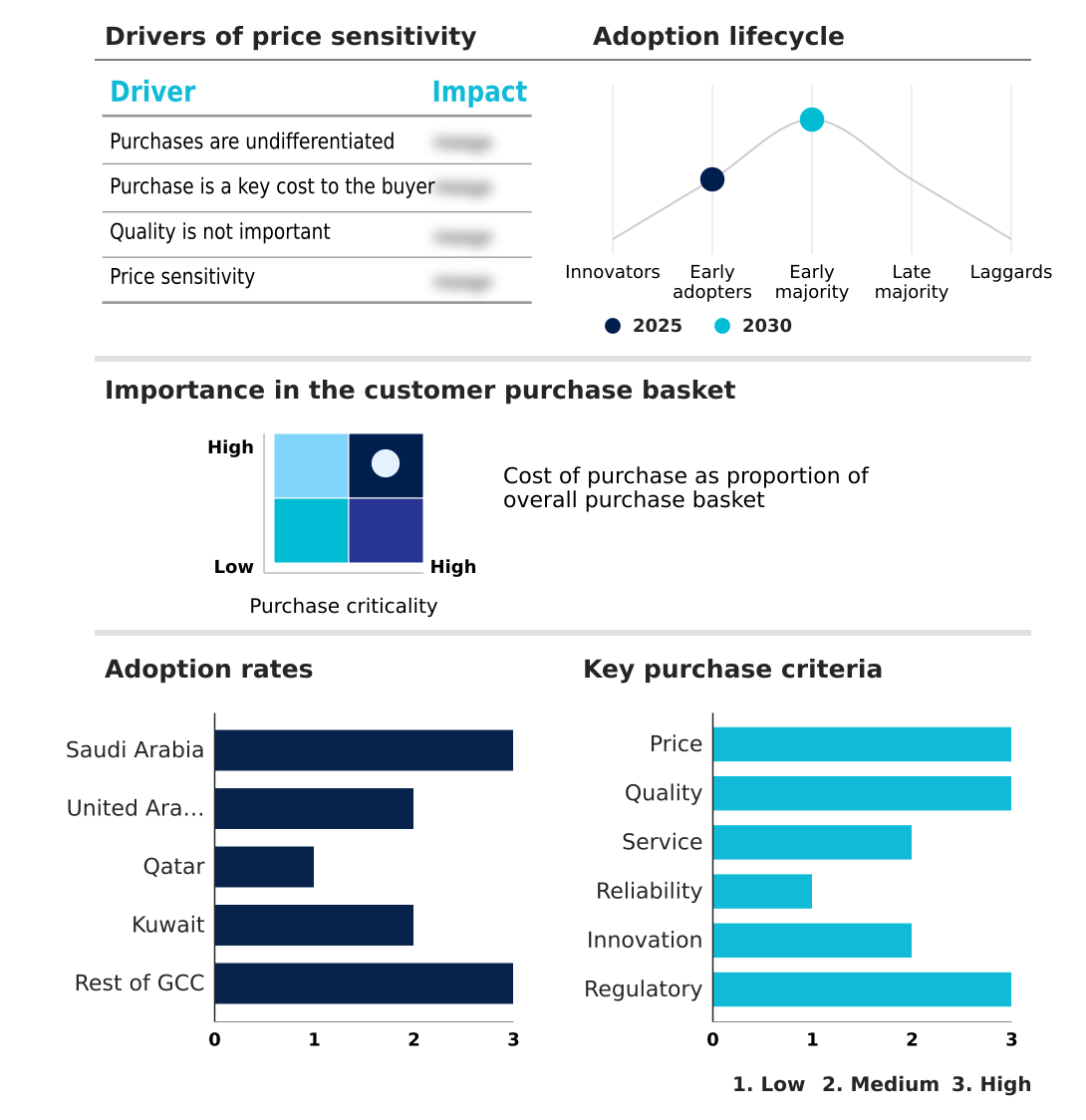

The gcc refractory materials for steel industry market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the gcc refractory materials for steel industry market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of GCC Refractory Materials For Steel Industry Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, gcc refractory materials for steel industry market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adani Group - Provides specialized refractory materials like castables and bricks, offering turnkey solutions for high-temperature industrial processes including steel manufacturing.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adani Group

- Allied Mineral Products LLC

- CALDERYS France SAS

- Compagnie de Saint Gobain SA

- HarbisonWalker International

- IFGL Refractories Ltd.

- Imerys S.A.

- INTOCAST AG

- Kanthal AB

- Krosaki Harima Corp.

- Magnezit Group

- Minerals Technologies Inc.

- Morgan Advanced Materials

- Refractarios ALFRAN SA

- Refratechnik Holding

- RHI Magnesita GmbH

- Shinagawa Refractories.

- Steuler Holding GmbH

- Trent Refractories Ltd

- Vesuvius Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Gcc refractory materials for steel industry market

- In January 2025, RHI Magnesita GmbH completed its acquisition of Resco Group, a US-based producer of alumina monolithics and clays, to expand its product portfolio and strengthen its local production footprint in North America.

- In November 2024, Calderys and Binzagr established a strategic partnership to construct a new refractory production plant in Saudi Arabia, aiming to localize supply for the region and enhance service capabilities.

- In March 2025, Imerys S.A. launched a cost adaptation plan, Project Horizon, designed to improve structural profitability and streamline production capacity in response to challenging market conditions.

- In May 2025, Vesuvius Plc announced the acquisition of PiroMet, a specialized manufacturer of pyrometry systems, to enhance its technological offerings in molten metal flow engineering and process control.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled GCC Refractory Materials For Steel Industry Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 202 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.2% |

| Market growth 2026-2030 | USD 30.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.0% |

| Key countries | Saudi Arabia, United Arab Emirates, Qatar, Kuwait and Rest of GCC |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The refractory materials for steel industry market in gcc is fundamentally shaped by the continuous pursuit of operational excellence and material innovation. The selection of advanced materials, such as monolithic refractories and high-alumina bricks, is no longer a simple procurement decision but a strategic imperative discussed at the boardroom level.

- Balancing the higher initial capital expenditure on premium refractory products against the long-term return on investment from extended furnace linings and ladle linings is critical. This involves a deep analysis of thermal shock resistance, corrosion resistance, and slag penetration to ensure furnace operational stability.

- The adoption of materials like magnesia-carbon bricks and advanced castables, used in secondary steelmaking process and direct reduced iron (DRI) plants, directly impacts productivity. By utilizing zirconia-based products and dolomite-based linings, steelmakers can achieve over a 10% reduction in energy consumption per ton of steel produced.

- This focus on durability and efficiency is driving advancements in binder systems, aggregate refinement, and overall thermal gradient management, making the choice between shaped refractories and monolithic solutions, including gunning mixes and ramming masses, a key factor in competitive positioning. The use of non-clay refractories and innovative ceramic fiber blankets also contributes to superior heat retention and performance.

What are the Key Data Covered in this GCC Refractory Materials For Steel Industry Market Research and Growth Report?

-

What is the expected growth of the GCC Refractory Materials For Steel Industry Market between 2026 and 2030?

-

USD 30.5 million, at a CAGR of 3.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Bricks, and Monolithic), Type (Acidic and neutral, and Basic), Form Factor (Shaped refractories, and Unshaped refractories) and Geography (GCC)

-

-

Which regions are analyzed in the report?

-

GCC

-

-

What are the key growth drivers and market challenges?

-

Growing steel production capacity across GCC countries, High energy consumption raising operational production costs

-

-

Who are the major players in the GCC Refractory Materials For Steel Industry Market?

-

Adani Group, Allied Mineral Products LLC, CALDERYS France SAS, Compagnie de Saint Gobain SA, HarbisonWalker International, IFGL Refractories Ltd., Imerys S.A., INTOCAST AG, Kanthal AB, Krosaki Harima Corp., Magnezit Group, Minerals Technologies Inc., Morgan Advanced Materials, Refractarios ALFRAN SA, Refratechnik Holding, RHI Magnesita GmbH, Shinagawa Refractories., Steuler Holding GmbH, Trent Refractories Ltd and Vesuvius Plc

-

Market Research Insights

- Market dynamics are increasingly shaped by the integration of digital technologies for enhanced operational oversight. The adoption of refractory lifecycle monitoring and data-driven refractory management is becoming standard practice, enabling predictive maintenance workflows that mitigate costly, unplanned shutdowns.

- This shift toward industrial automation systems allows operators to achieve superior lining performance improvement, with some facilities reporting a 25% reduction in furnace turnaround time through optimized maintenance scheduling. Furthermore, the use of sensor-enabled diagnostics provides real-time thermal behavior tracking and wear pattern analysis.

- This capability directly supports better inventory control and procurement strategies, improving material forecasting accuracy by over 30% and reducing operational costs associated with excess stock and waste.

We can help! Our analysts can customize this gcc refractory materials for steel industry market research report to meet your requirements.

RIA -

RIA -