Primary Battery Market Size 2025-2029

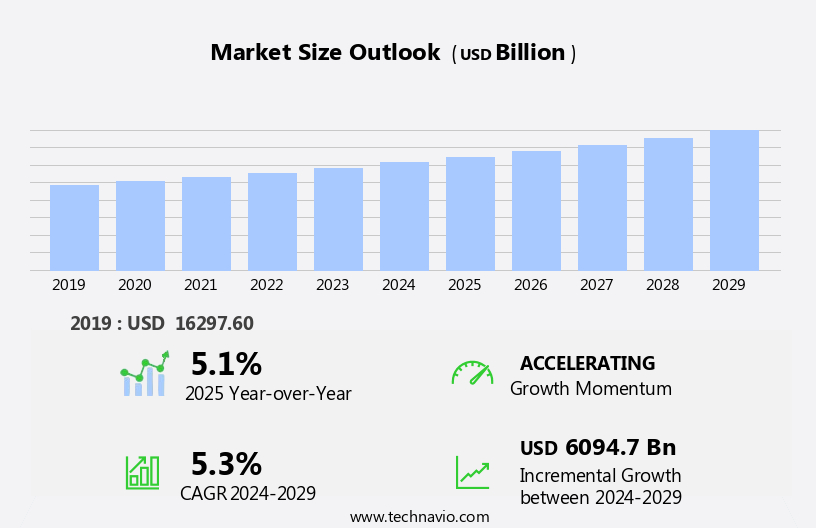

The primary battery market size is forecast to increase by USD 6,094.7 billion, at a CAGR of 5.3% between 2024 and 2029.

- The market is experiencing significant growth, driven by the increasing demand for portable medical equipment and the expanding use of primary batteries in various consumer electronics. However, the market faces challenges, including the threat from rechargeable hearing aid solutions, which are gaining popularity due to their cost-effectiveness and environmental benefits. Manufacturers of primary batteries must innovate to maintain their market share, exploring new applications and improving battery performance and sustainability. For instance, lithium-ion primary batteries are gaining traction due to their high energy density and long shelf life, making them suitable for use in smartwatches, wireless headphones, and other portable devices.

- Additionally, the development of primary batteries with longer lifespan and lower self-discharge rates is a promising area of research, addressing the challenges of frequent battery replacements and energy waste. The increased demand from the consumer electronics market, fueled by high consumer spending on devices such as smartphones, tablets, and wearables, is also driving the demand for primary batteries as power sources. Companies in the market must stay agile and adapt to these trends and challenges to capitalize on growth opportunities and maintain a competitive edge.

What will be the Size of the Primary Battery Market during the forecast period?

- The market encompasses a diverse range of applications, from consumer electronics and emergency power to grid storage and off-grid systems. Battery electrochemistry and chemistry play a crucial role in determining battery performance and longevity. Battery pack design, optimization, and integration are essential for maximizing energy density and power output. Emergency power and backup systems rely on reliable battery solutions for uninterrupted operation during power outages. Wireless power and battery optimization algorithms enable seamless charging and efficient energy management. Grid storage and renewable energy applications require advanced battery technology for effective energy storage and power backup.

- Off-grid applications, such as aerospace and military, demand high-performance batteries with extended life and safety features. Battery degradation mechanisms and failure modes are critical areas of research for improving battery reliability and safety. Battery engineering and design advancements focus on energy management, thermal management, and safety testing to meet the demands of various industries. Medical devices and portable power applications require compact, lightweight, and long-lasting batteries. Battery aging and degradation modeling are essential for predicting battery performance and optimizing maintenance schedules. Battery assembly, power management, and battery module design are key aspects of manufacturing and production processes. Battery applications continue to expand, with emerging trends in remote sensing, military applications, and battery safety testing driving innovation in the market. The legislative support for battery recycling is another key trend, as governments and industries focus on reducing environmental impact and promoting sustainable practices.

How is this Primary Battery Industry segmented?

The primary battery industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Defense

- Medical

- Others

- Type

- Alkaline battery

- Lithium battery

- Others

- Distribution Channel

- Offline

- Online

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

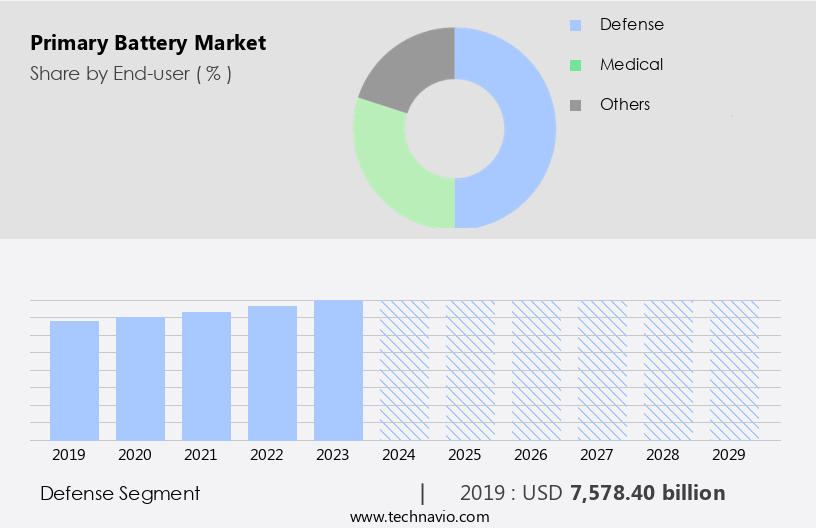

By End-user Insights

The defense segment is estimated to witness significant growth during the forecast period. Primary batteries play a crucial role in powering various military applications, particularly portable devices and weapon systems used by the US Department of Defense. The shift towards more efficient and lightweight batteries, such as the new generation of alkaline and lithium batteries, is gaining momentum due to their superior energy density and reduced weight. This is especially beneficial for soldiers carrying heavy loads, as they can carry more equipment and less batteries. The market dynamics for primary batteries are driven by several factors. Military techniques are evolving, leading to the demand for modern high-tech combat systems and increased reliance on mobile technologies and remotely piloted unmanned aerial vehicles.

Over the forecast period, military spending on advanced weaponry and the growing need for surveillance drones are expected to fuel the demand for these batteries. Battery innovations, such as improved charging technologies, battery recycling, and the circular economy, are also contributing to the growth of the market. Lithium batteries, with their high energy density and long shelf life, are becoming increasingly popular. However, lead-acid batteries, despite their lower energy density, continue to be used due to their reliability and affordability. Battery standards and certifications ensure the safety and performance of these batteries, while battery testing and monitoring help maintain their optimal condition.

The Defense segment was valued at USD 7,578.40 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

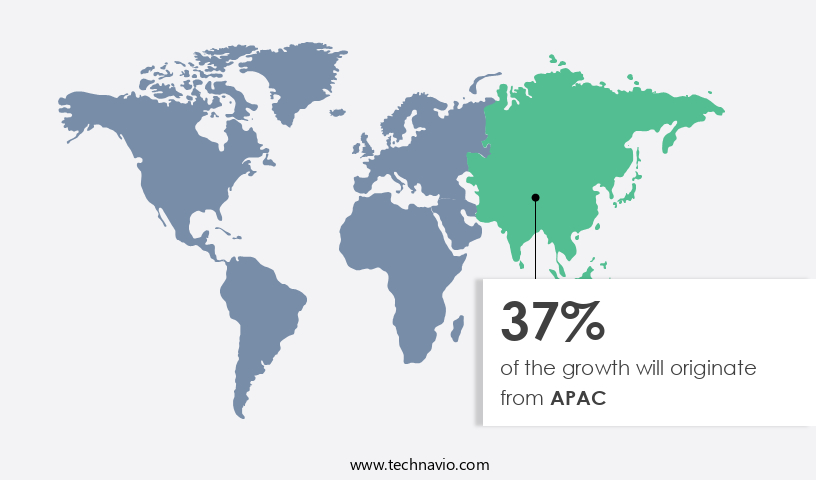

APAC is estimated to contribute 37% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in Asia Pacific (APAC) is experiencing significant growth. This will be due to the increasing consumption for high-drain applications such as digital cameras, toys, and utility metering. The region is projected to house the majority of the world's smart meters, driving the demand for primary batteries. The rise in per capita annual disposable income, particularly in countries like China, is a key factor fueling this growth. China's disposable income has been growing faster than its GDP, leading to increased purchases of high-end electronic devices. Primary batteries, with their high energy density and long shelf life, are expected to remain the preferred choice for these applications during the forecast period.

Battery technologies, including alkaline, zinc-carbon, lead-acid, nickel-cadmium, nickel-metal hydride, and lithium batteries, are continually evolving to meet the demands of various industries. Innovations in battery materials, charging methods, and battery management systems are enhancing battery performance, reliability, and safety. Battery recycling and circular economy initiatives are also gaining traction, reducing the environmental impact of battery production and disposal. Battery standards and certifications play a crucial role in ensuring battery safety and reliability. Regulations governing battery manufacturing, testing, and disposal are becoming increasingly stringent to mitigate risks associated with battery usage. Battery efficiency and capacity are essential factors in determining battery cost and battery life cycle.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Primary Battery market drivers leading to the rise in the adoption of Industry?

- The increasing requirement for portable medical equipment is the primary market motivator, driven by advancements in technology and the growing preference for convenient and efficient healthcare solutions. The market for primary batteries, particularly those utilizing advanced technologies like nickel-metal hydride and lithium, is experiencing significant growth due to the increasing demand for portable devices. While lithium batteries were initially used in pacemakers in the 1960s, they are now the primary power source for various medical devices such as surgical saws, drills, and infusion pumps. These batteries provide extended battery life and high energy density, making them ideal for powering high-end, sophisticated portable devices such as medical equipment like defibrillators and EKGs. Pulse power technology, which accumulates energy and releases it as needed, further enhances the capabilities of these batteries. Tadiran Batteries, a division of Saft, has made strides in this field with the development of a high-energy lithium battery that is smaller than traditional batteries.

- This innovation improves the efficiency of portable devices and extends their battery life beyond three decades. Lithium batteries have been in use since the 1960s, primarily in medical devices such as pacemakers. Today, they power a wide range of medical equipment, including surgical saws, drills, and infusion pumps. Battery manufacturing continues to evolve, with a focus on enhancing battery durability, battery discharge rate, and battery management systems. Stringent battery certifications ensure safety and reliability, making these batteries a preferred choice for various industries. Ongoing research and development efforts aim to further improve battery energy density and battery discharging efficiency.

What are the Primary Battery market trends shaping the Industry?

- The emerging market trend underscores the importance of securing legislative support for battery recycling. This crucial step will foster a sustainable and eco-friendly economy by promoting the circular use of valuable resources contained in used batteries. Primary batteries, a widely utilized power source for various applications, are subject to increasing regulatory focus due to the environmental impact of their disposal. Alkaline batteries, in particular, contain harmful materials that can contaminate groundwater if not recycled properly. To address this issue, governments worldwide are enacting regulations to encourage the recycling of these batteries. For instance, the European Union's Directive 2006/66/EC on batteries mandates that all member states reach a specified collection rate and convert at least 50% of the battery weight received for recycling into its post-consumer form. Companies like Retriev Technologies and Raw Materials Company are spearheading primary battery recycling efforts, mitigating production costs and reducing environmental impact.

- The importance of battery recycling extends beyond cost savings, as it also enhances battery efficiency and conserves natural resources. As battery technologies continue to evolve, innovations in battery materials and charging methods are expected to further optimize battery performance and sustainability.

How does Primary Battery market face challenges during its growth?

- The rechargeable hearing aid solution poses a significant challenge to the growth of the industry due to its increasing popularity and advanced capabilities. The market encompasses various types of batteries, including zinc-carbon and lithium batteries, each offering distinct advantages in terms of battery size, voltage, capacity, and performance. Zinc-carbon batteries, though not rechargeable, provide high energy output in a compact size, making them suitable for devices with exclusive power supply requirements, such as hearing aids. Despite their small size, zinc-carbon batteries can power these devices for several days. However, the manufacturing process for rechargeable batteries for such devices poses challenges due to their unique power requirements. The shift towards rechargeable devices and the ban on mercury-based batteries in 1996 have led to increased interest in rechargeable batteries.

- Although the commercialization of rechargeable hearing instruments is yet to be fully realized, lithium batteries, known for their sustainability and long battery life, are gaining popularity in this sector. The circular economy concept, which prioriizes battery reuse and recycling, is also becoming increasingly important in the battery industry, contributing to greater battery sustainability and reducing environmental impact. Battery reliability and battery life are crucial factors in the market, as consumers demand long-lasting, dependable power sources. Lithium batteries, with their high energy density and long life, are well-positioned to meet these demands. As the market evolves, advancements in battery technology are expected to further enhance battery performance and efficiency, catering to the diverse needs of various industries.

Exclusive Customer Landscape

The primary battery market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the primary battery market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, primary battery market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amara Raja Batteries Ltd. - The company specializes in providing high-performing primary batteries under the Powerstack, Amaron Sleek, and Amaron Volt brands. Our offerings deliver reliable power solutions for various applications, ensuring optimal efficiency and an extended life cycle.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amara Raja Batteries Ltd.

- Camelion Batteries GmbH

- Dongguan Large electronics Co. Ltd.

- EaglePicher Technologies LLC

- Energizer Holdings Inc.

- EnerSys

- EVE Energy Co. Ltd.

- Fujitsu Ltd.

- GP Industries Ltd.

- Hitachi Ltd.

- Integer Holdings Corp.

- Panasonic Holdings Corp.

- Samsung SDI Co. Ltd.

- Sony Group Corp.

- The Duracell Co.

- Toshiba Corp.

- TotalEnergies SE

- Ultralife Corp.

- VARTA AG

- Zhejiang Mustang Battery Co Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Primary Battery Market

- In January 2023, Panasonic Energy announced the expansion of its lithium-ion battery production capacity in Kansas, USA, by 30%, aiming to meet the growing demand for batteries in the electric vehicle (EV) market (Panasonic Energy press release, 2023). This expansion will add 1.3 GWh to the company's existing 4.3 GWh production capacity.

- In March 2024, Tesla and LG Energy Solution signed a long-term battery supply agreement, marking a significant strategic collaboration between the two companies. Tesla will receive battery cells from LG Energy Solution for its EVs, ensuring a stable supply chain and strengthening the partnership between the two industry leaders (Tesla press release, 2024).

- In May 2025, CATL, the world's largest lithium-ion battery manufacturer, raised USD 2.35 billion in a funding round. The funds will be used for research and development, as well as the expansion of production capacity to meet the increasing demand for batteries in the EV market (Reuters, 2025).

Research Analyst Overview

The market continues to evolve, shaped by a complex interplay of dynamic factors. Battery regulations, charging methods, and standards are continually evolving to address safety concerns and improve efficiency. Technological advancements in battery materials, innovations, and sustainability are shaping the landscape, with lithium batteries and nickel-metal hydride batteries gaining popularity for their high energy density and long life. Battery cost, weight, and size are key considerations, with ongoing efforts to optimize these factors for various applications. Battery efficiency and environmental impact are increasingly important, driving the circular economy and the exploration of battery recycling and reuse. Battery performance, reliability, and durability are essential for industries such as telecommunications, medical devices, and military applications.

The Primary Battery Market continues to expand, driven by advancements in nickel-cadmium batteries and growing demand for diverse primary battery applications. Key performance factors such as battery capacity, battery voltage, and battery current influence efficiency and usability. Manufacturers focus on optimizing battery shelf life and innovative battery packaging to meet consumer needs. Ongoing battery research and battery development enhance reliability and sustainability. Variations in battery shape impact product design and usability, while improving battery power and battery charging solutions remains a priority. Efficient battery storage, battery monitoring, and battery diagnostics ensure optimal performance. As technology advances, battery replacement solutions and strategies for battery end-of-life management are evolving, ensuring a more sustainable and efficient primary battery ecosystem.

The Primary Battery Market is evolving with advancements in battery chemistry and battery design, enhancing efficiency and sustainability. Rigorous battery performance testing and battery reliability analysis ensure quality and longevity. Researchers focus on battery degradation modeling to predict lifespan and optimize functionality. Effective battery energy management and battery thermal management improve efficiency and prevent overheating. Seamless battery integration supports diverse applications, including cutting-edge aerospace applications, where reliability is paramount.

Battery testing, monitoring, and management systems are crucial for ensuring optimal battery function and longevity. Zinc-carbon batteries and alkaline batteries remain relevant, offering affordability and reliability for certain use cases. Lead-acid batteries continue to dominate the industrial sector due to their robustness and cost-effectiveness. Battery prognosis and diagnostics are essential for predictive maintenance and ensuring battery health. Battery certifications and manufacturing standards ensure safety and quality. The battery market is a dynamic and ever-changing landscape, with ongoing research and development shaping its future.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Primary Battery Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

224 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.3% |

|

Market growth 2025-2029 |

USD 6,094.7 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.1 |

|

Key countries |

US, China, Germany, India, UK, Canada, Japan, Brazil, France, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Primary Battery Market Research and Growth Report?

- CAGR of the Primary Battery industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the primary battery market growth of industry companies

We can help! Our analysts can customize this primary battery market research report to meet your requirements.

RIA -

RIA -