Polyurea Market Size 2025-2029

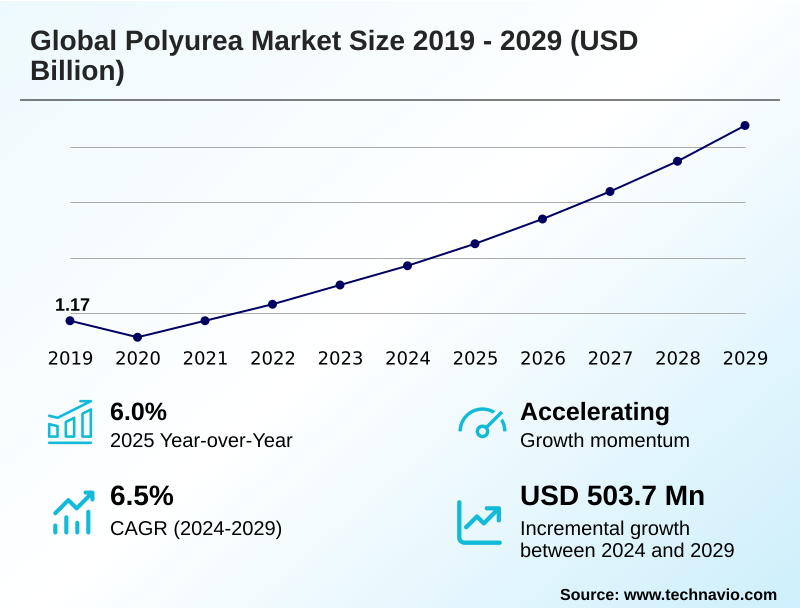

The polyurea market size is valued to increase by USD 503.7 million, at a CAGR of 6.5% from 2024 to 2029. Accelerated expansion of the global construction industry will drive the polyurea market.

Major Market Trends & Insights

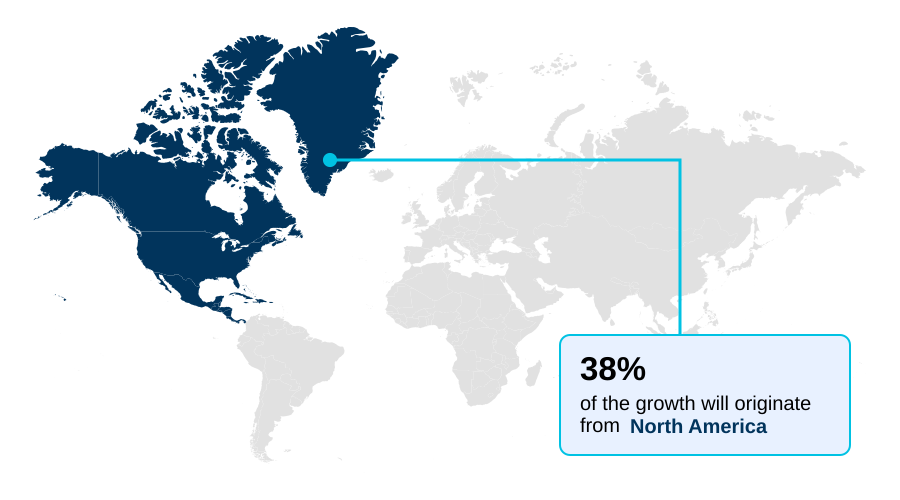

- North America dominated the market and accounted for a 37.5% growth during the forecast period.

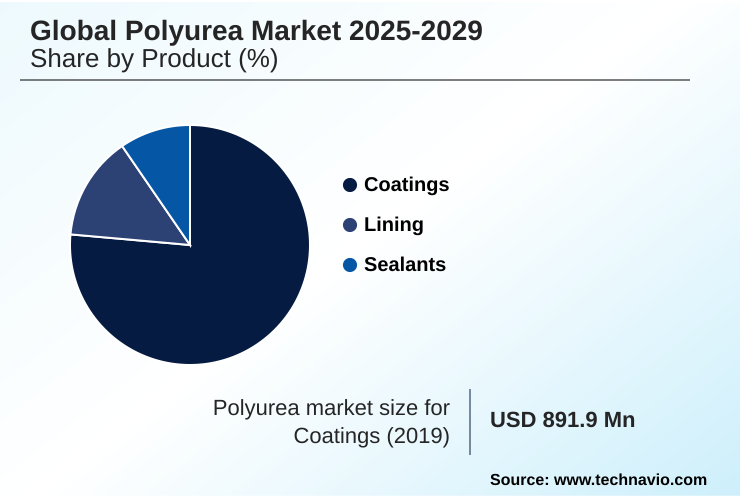

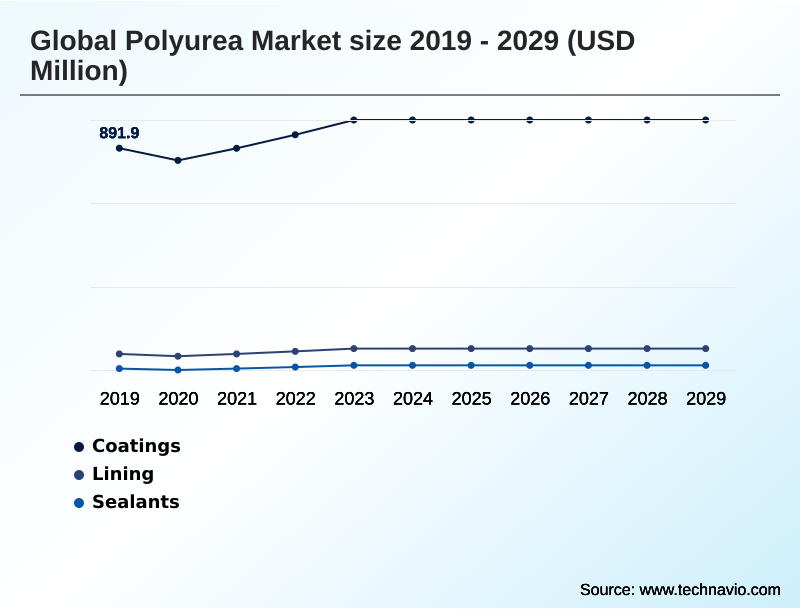

- By Product - Coatings segment was valued at USD 991.8 million in 2023

- By Raw Material - Aliphatic segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 708.5 million

- Market Future Opportunities: USD 503.7 million

- CAGR from 2024 to 2029 : 6.5%

Market Summary

- The polyurea market is defined by its high-performance elastomeric coatings, which are derived from the reaction of an isocyanate component with an amine-terminated resin blend. This step-growth polymerization process yields materials with exceptional high tensile strength, crack-bridging capabilities, and moisture insensitivity, making them ideal for demanding applications.

- Key drivers include the expansion of the global construction industry and the increasing adoption in the automotive sector for applications like durable truck bed liners. A significant trend is the industry's pivot toward sustainability, with the development of bio-based polyurea and low-VOC formulations.

- For instance, a project manager for a major bridge rehabilitation project must weigh the higher initial investment for a polyurea system, which offers rapid curing and long-term durability, against a lower-cost epoxy system that requires longer downtime and more frequent maintenance. This decision highlights the trade-offs between upfront capital expenditure and long-term operational efficiency.

- Challenges such as volatile raw material pricing and competition from alternative technologies like polyaspartic topcoats persist, pushing vendors toward innovation in both chemistry and polyurea application technology to maintain a competitive edge and expand into new sectors.

What will be the Size of the Polyurea Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Polyurea Market Segmented?

The polyurea industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Coatings

- Lining

- Sealants

- Raw material

- Aliphatic

- Aromatic

- Type

- Hot polyurea

- Cold polyurea

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Product Insights

The coatings segment is estimated to witness significant growth during the forecast period.

The market is segmented by product, raw material, and type, with coatings representing a primary application. Innovations in plural-component systems are enhancing product capabilities, including superior chemical resistance. Formulations with low-VOC content are gaining traction, driven by environmental standards.

For instance, the integration of nano-silica has been shown to improve abrasion resistance by up to 35%, expanding use cases in high-wear environments.

The development of advanced polyurea application technology allows for the creation of a seamless membrane ideal for industrial flooring solutions and protective linings for tanks.

Both aliphatic isocyanates and aromatic isocyanates are used, influencing properties like UV stability and cost, which are critical for applications from roof coating restoration to marine and offshore coatings.

The Coatings segment was valued at USD 991.8 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Polyurea Market Demand is Rising in North America Request Free Sample

The geographic landscape of the polyurea market is diverse, with North America representing the largest share at approximately 37.5% of the market, driven by extensive infrastructure rehabilitation and industrial maintenance.

The region's demand is centered on applications like bridge deck waterproofing and secondary containment liners. In contrast, the APAC region is the fastest-growing market, contributing over 25.6% and expanding at a more rapid pace than mature markets.

This growth is fueled by large-scale construction and manufacturing activities in countries like China and India, where there is a high demand for fast-curing flooring systems and protective linings for tanks.

Europe focuses on sustainable solutions, promoting low-VOC formulations and cold-applied polyurea repair products. The Middle East shows strong potential due to mega-projects requiring vast quantities of high-performance coatings.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the polyurea market often revolves around a detailed cost analysis of polyurea vs epoxy flooring, where factors like long-term durability and the benefits of fast-curing flooring systems must be considered.

- The choice between aliphatic vs aromatic polyurea for outdoor use is another critical consideration, with aliphatic variants offering superior UV resistance for applications like spray-applied waterproofing for commercial roofs and polyurea for rv roof leak prevention. For interior or protected applications, aromatic systems are a cost-effective choice.

- Innovations are also making solutions more accessible, such as cold-applied polyurea for diy garage floors. For industrial settings, the discussion shifts to technical specifications. Using polyurea for secondary containment compliance is essential in regulated industries, while polyurea lining for potable water tanks requires certified, non-toxic formulations.

- The material's versatility is highlighted when choosing the right polyurea for bridge decks, which demands exceptional crack-bridging and waterproofing. In the energy and defense sectors, specialized formulas are used for blast mitigation projects. Hand-applied polyurea for waterproofing repairs offers a practical solution for smaller jobs, contrasting with high-pressure systems used for large-scale projects like mining equipment protection.

- Polyurea performance in marine environments is tested by constant exposure to corrosive elements, necessitating robust formulations. The fundamental polyurea versus polyurethane coating differences lie in cure time and moisture sensitivity, with polyurea offering a distinct advantage in rapid-return-to-service scenarios, often reducing project schedules by more than 50% compared to traditional systems, directly impacting operational planning and labor costs.

What are the key market drivers leading to the rise in the adoption of Polyurea Industry?

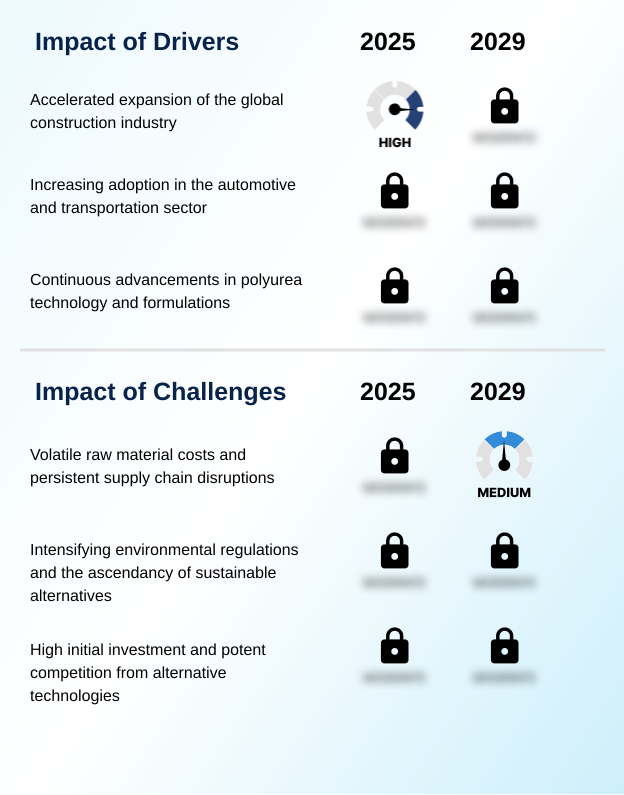

- The accelerated expansion of the global construction industry serves as a key driver for market growth.

- Robust growth in the global construction and automotive sectors serves as a primary driver for the market.

- In construction, polyurea is specified for its rapid curing times and ability to form a durable, seamless membrane, essential for waterproofing and protecting infrastructure.

- The material's high tensile strength and chemical resistance are critical for applications such as concrete surface preparation and linings.

- In the automotive industry, which saw global production exceed 93 million units, polyurea is used for durable truck bed liners and protective underbody coatings. Continuous innovation in formulations is also expanding the market.

- For example, research into nano-silica integration has demonstrated a 35% improvement in abrasion resistance, creating more resilient surfaces for industrial flooring solutions and parking garage deck coatings, thereby opening new opportunities and ensuring sustained demand.

What are the market trends shaping the Polyurea Industry?

- An intensified focus on sustainable and eco-friendly formulations is emerging as a significant market trend. This shift is driven by increasing regulatory pressures and growing demand for greener material solutions.

- A significant trend shaping the market is the expansion into specialized, high-performance applications driven by technological advancements. The electric vehicle sector, for instance, represents a major new frontier, with demand for protective coatings for EV batteries growing as global sales approach 15 million units annually. These coatings leverage polyurea's excellent insulation and impact resistance.

- Concurrently, the industry is making strides in sustainability, exemplified by the development of bio-based polyurea formulations containing up to 30% renewable content without compromising performance. This aligns with the demand for greener building materials and low-VOC formulation products.

- Innovations in polyurea application technology, including more efficient high-pressure spray systems, are making these advanced materials more accessible for large-scale projects like wastewater treatment tank linings and commercial kitchen flooring, enhancing both productivity and finish quality.

What challenges does the Polyurea Industry face during its growth?

- Volatile raw material costs and persistent supply chain disruptions present a key challenge affecting industry growth.

- A primary challenge for the market is the high initial investment in plural-component systems and specialized equipment, which can be a significant barrier for smaller contractors. These costs, sometimes exceeding conventional systems by a factor of three, are compounded by the need for skilled technicians trained in specific polyurea application technology.

- Furthermore, intense competition from alternative technologies like epoxy and polyurethane coatings, which are often perceived as more cost-effective for less demanding applications, constrains market penetration.

- The market also grapples with raw material price volatility, with key inputs like isocyanates experiencing price swings that can exceed 20% in a single quarter, directly impacting the cost of elastomeric coatings and high-solids coatings and making it difficult to maintain stable pricing for end-users.

Exclusive Technavio Analysis on Customer Landscape

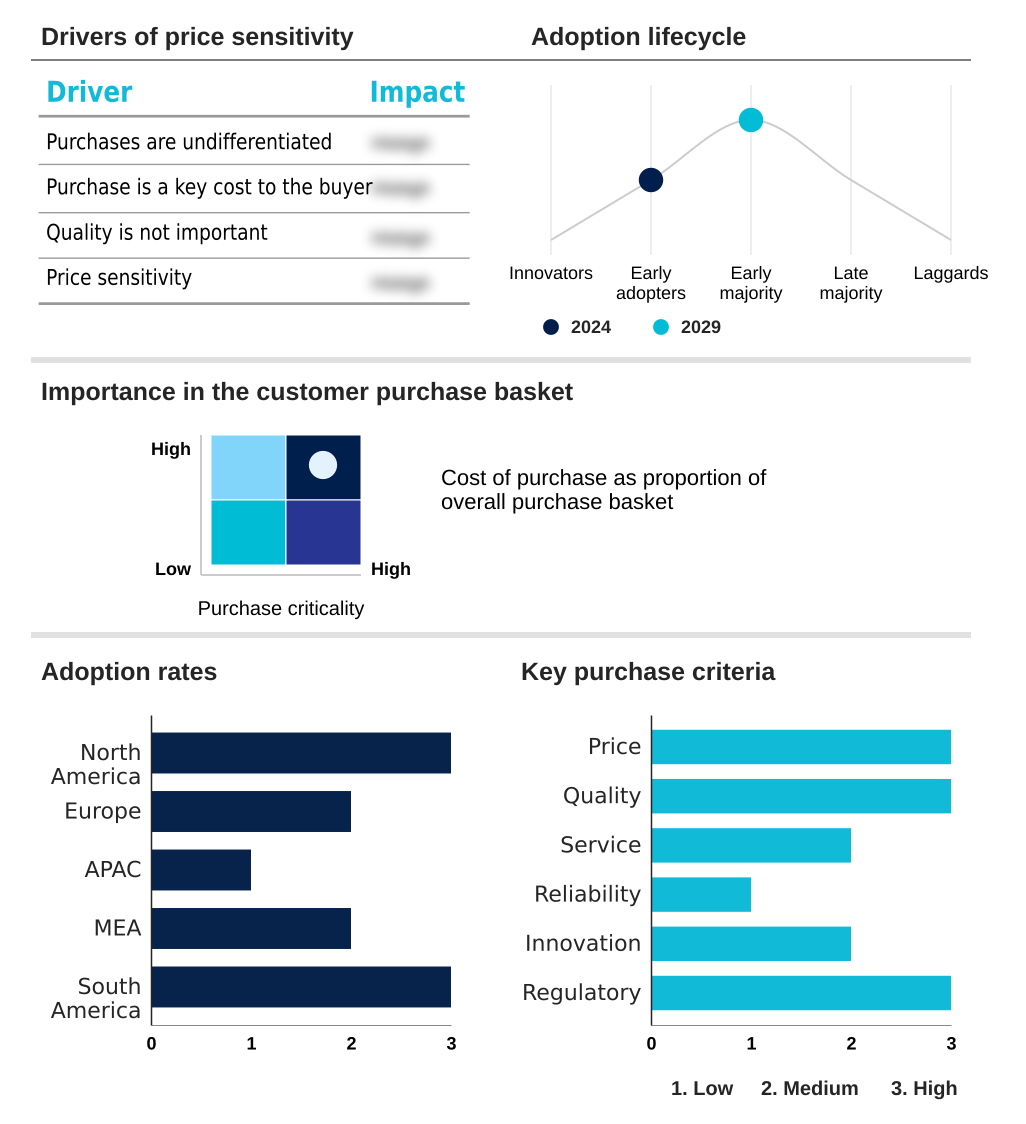

The polyurea market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the polyurea market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Polyurea Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, polyurea market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

American Polymers Corp. - The company offers specialized protective coatings, linings, and joint fillers, focusing on pure polyurea and hybrid elastomer technologies for demanding industrial and commercial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Polymers Corp.

- ArmorThane USA Inc.

- BASF SE

- Covestro AG

- Dorf Ketal Chemicals India Pvt. Ltd.

- Huntsman International LLC

- Krypton Chemical S.L.

- Marvel Coatings

- Nukote Coating Systems Intl.

- POLYFLEX AND WASSER

- PPG Industries Inc.

- Rhino Linings Corp.

- Scorpion Protective Coatings Inc.

- Specialty Products Inc.

- Sprayroq Inc.

- TECNOPOL SISTEMAS S.L.

- Teknos Group Oy

- The Sherwin Williams Co.

- VersaFlex Inc.

- VIP Coatings International GmbH and Co. KG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Polyurea market

- In September, 2024, Delta Coatings International announced a strategic expansion into Vietnam and the broader Southeast Asian region, signaling confidence in the region's growth potential for high-performance coatings.

- In September, 2024, Sika launched Sikaflex-403 Tank and Silo, an advanced sealant developed to offer outstanding resistance to chemicals and organic acids for sealing bolted steel tanks and silos.

- In November, 2024, PPG secured its 50th order for the electrostatic application of its marine fouling control coatings, which will utilize a polyurea-based product on a large oil tanker in Oman.

- In February, 2025, a strategic alliance was formed between UAE and Italian firms to revolutionize water infrastructure development across the Middle East and Africa, focusing on desalination and treatment plants where corrosion protection is paramount.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Polyurea Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 289 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.5% |

| Market growth 2025-2029 | USD 503.7 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 6.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Australia, Saudi Arabia, UAE, South Africa, Qatar, Egypt, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The polyurea market is characterized by continuous innovation in material science, focusing on enhancing performance attributes such as abrasion resistance and flame retardancy. The use of both aliphatic isocyanates and aromatic isocyanates allows for a broad spectrum of applications, from aesthetically critical topcoats to robust base layers.

- A key technological advancement involves the integration of nano-silica into plural-component systems, which has been shown to increase abrasion resistance by 35%. This drive for enhanced durability is pivotal as the material finds use in demanding environments requiring blast and impact protection or geotextile reinforcement.

- Boardroom decisions are increasingly influenced by sustainability, pushing R&D toward bio-based polyurea and low-VOC formulation development. These elastomeric coatings create a seamless membrane with exceptional crack-bridging capabilities and high tensile strength, ideal for everything from potable water-certified lining to fast-cure coatings for industrial floors.

- The development of hybrid polyurea systems and ceramic-reinforced polyurea further expands the application scope, while techniques like electrostatic application improve efficiency. This focus on advanced, specialized materials with properties like moisture insensitivity underscores the industry's direction toward high-value, performance-driven solutions.

What are the Key Data Covered in this Polyurea Market Research and Growth Report?

-

What is the expected growth of the Polyurea Market between 2025 and 2029?

-

USD 503.7 million, at a CAGR of 6.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Coatings, Lining, and Sealants), Raw Material (Aliphatic, and Aromatic), Type (Hot Polyurea, and Cold Polyurea) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Accelerated expansion of the global construction industry, Volatile raw material costs and persistent supply chain disruptions

-

-

Who are the major players in the Polyurea Market?

-

American Polymers Corp., ArmorThane USA Inc., BASF SE, Covestro AG, Dorf Ketal Chemicals India Pvt. Ltd., Huntsman International LLC, Krypton Chemical S.L., Marvel Coatings, Nukote Coating Systems Intl., POLYFLEX AND WASSER, PPG Industries Inc., Rhino Linings Corp., Scorpion Protective Coatings Inc., Specialty Products Inc., Sprayroq Inc., TECNOPOL SISTEMAS S.L., Teknos Group Oy, The Sherwin Williams Co., VersaFlex Inc. and VIP Coatings International GmbH and Co. KG

-

Market Research Insights

- Market dynamics are heavily influenced by the push for advanced material performance and efficiency. Formulations incorporating aliphatic isocyanates offer superior UV stability, crucial for outdoor applications, while aromatic systems provide a cost-effective solution for uses not exposed to sunlight.

- Innovations in polyurea application technology, including high-pressure spray systems, enable rapid installation of protective coatings for EV batteries and waterproofing membranes for roofing, reducing project timelines significantly. The development of bio-based polyurea with up to 30% renewable content caters to rising sustainability mandates.

- Furthermore, research has shown that integrating nano-additives can increase abrasion resistance by 35%, enhancing durability for industrial flooring solutions. The versatility is evident in applications ranging from corrosion protection for pipelines to flexible joint fillers and spray-applied structural rehabilitation, demonstrating the material's adaptability to diverse industrial needs.

We can help! Our analysts can customize this polyurea market research report to meet your requirements.

RIA -

RIA -