Phosphate Esters Market Size 2026-2030

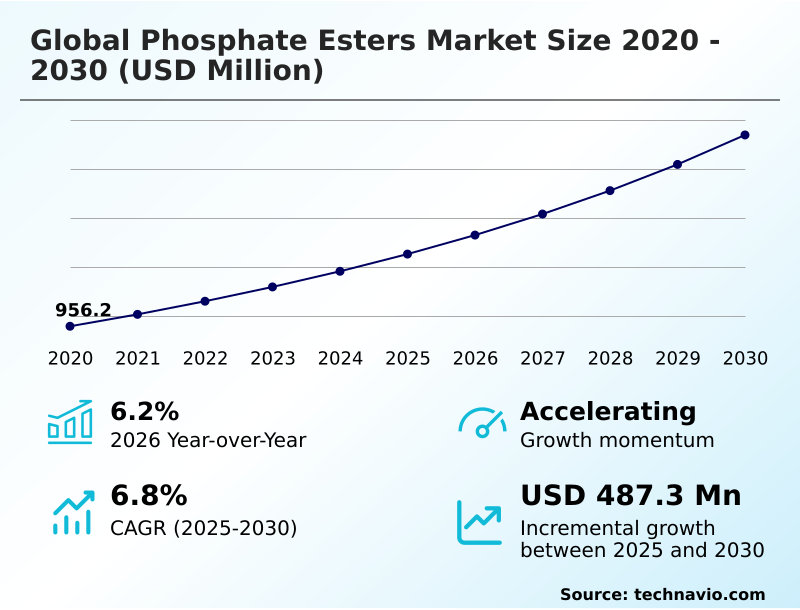

The phosphate esters market size is valued to increase by USD 487.3 million, at a CAGR of 6.8% from 2025 to 2030. Rising application as fire retardant will drive the phosphate esters market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 44% growth during the forecast period.

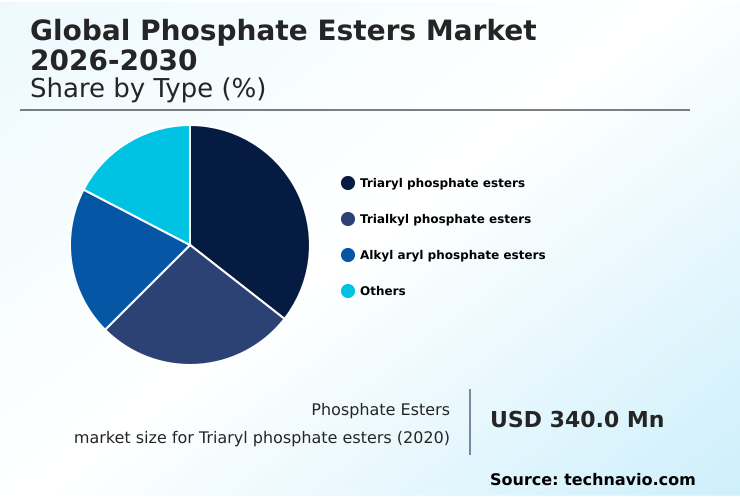

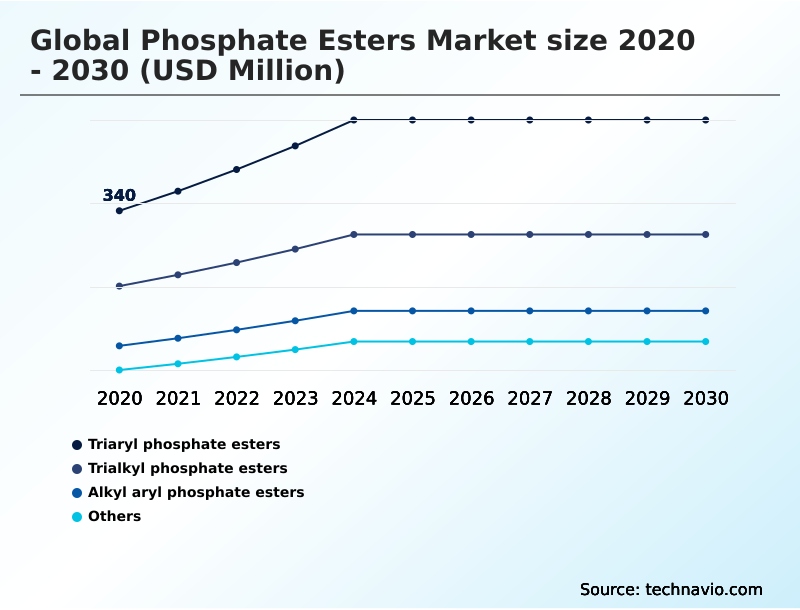

- By Type - Triaryl phosphate esters segment was valued at USD 439.2 million in 2024

- By Material - Alcohol based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 782.6 million

- Market Future Opportunities: USD 487.3 million

- CAGR from 2025 to 2030 : 6.8%

Market Summary

- The phosphate esters market is foundational to numerous industrial sectors, providing critical functionalities such as fire resistance, lubricity, and plasticization. These phosphorus-based chemicals are indispensable in applications ranging from aviation hydraulic fluids to flame-retardant polymers in electronics and construction.

- A key driver is the increasing regulatory pressure for safer, more effective fire retardants, pushing industries away from traditional halogenated options toward halogen-free formulations where phosphate esters excel. Concurrently, the trend toward high-performance and long-life lubricants in the automotive and industrial machinery sectors fuels demand for esters with superior thermal stability and anti-wear properties.

- However, the market faces challenges related to environmental persistence and toxicity concerns for certain ester types, prompting ongoing research into more biodegradable alternatives.

- For instance, a lubricant manufacturer might need to reformulate its industrial gear oil to comply with new environmental standards, replacing a traditional additive with a novel, bio-based phosphate ester that improves oxidation resistance by 15% while meeting stringent eco-toxicity requirements, showcasing the market's continuous push toward performance and sustainability.

What will be the Size of the Phosphate Esters Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Phosphate Esters Market Segmented?

The phosphate esters industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Triaryl phosphate esters

- Trialkyl phosphate esters

- Alkyl aryl phosphate esters

- Others

- Material

- Alcohol based

- Ethoxylated alcohol based

- Ethoxylated phenol based

- Application

- Lubricants

- Fire retardants

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The triaryl phosphate esters segment is estimated to witness significant growth during the forecast period.

The triaryl phosphate esters segment is defined by its superior performance in demanding industrial environments. These organophosphate compounds, which include specialty polymer additives and corrosion inhibitors, are integral to high-performance polymers and composite materials.

Their molecular structure provides exceptional thermal stability and fire resistance, making them essential for sectors requiring high-reliability components.

The fire retardant mechanism of these esters involves promoting char formation, which helps materials achieve up to a 40% reduction in flame propagation under controlled test conditions.

This functional excellence sustains their market position, as industries increasingly adopt advanced materials for safety and durability. Key applications in hydraulic fluid components and lubricant base oils further underscore their importance in modern industrial and transportation systems.

The Triaryl phosphate esters segment was valued at USD 439.2 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

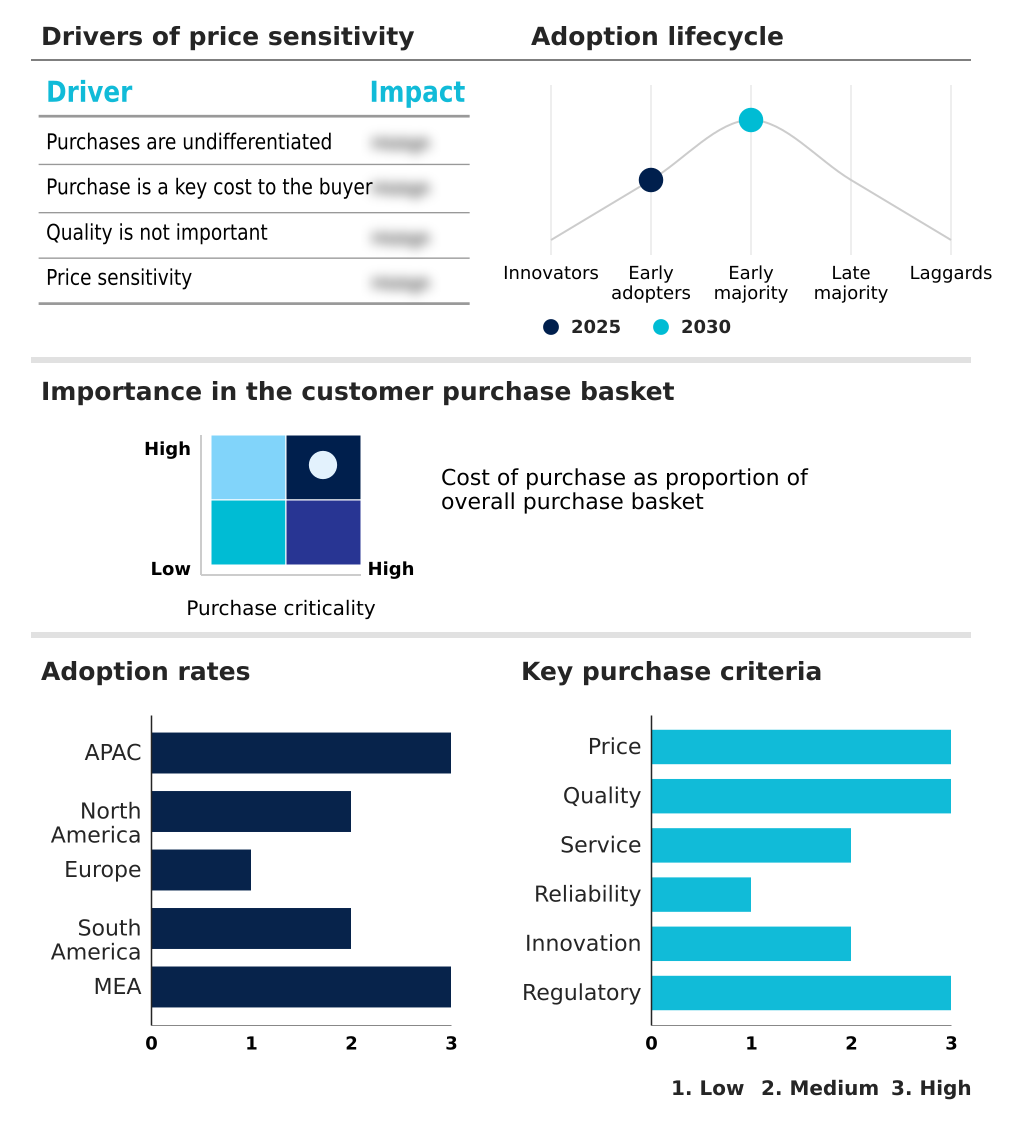

APAC is estimated to contribute 44% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Phosphate Esters Market Demand is Rising in APAC Request Free Sample

The geographic landscape is dominated by APAC, which accounts for 44% of the market's incremental growth, driven by rapid industrialization.

Countries in this region are significant consumers of phosphorus-based chemicals and trialkyl phosphate esters for applications in electronics and automotive manufacturing.

The region's market is expanding at a rate nearly 1.5 times that of North America, where the focus is on high-performance hydraulic fluid components and lubricant base oils.

In Europe, stringent regulations on industrial intermediates have spurred innovation in specialty polymer additives, with a focus on environmental compliance.

Adherence to these standards has led to a 20% increase in the adoption of eco-friendly plasticizer additives and metalworking fluids compared to regions with less stringent oversight, highlighting the global divergence in market priorities.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global phosphate esters market 2026-2030 is characterized by its diverse applications and the continuous need for performance enhancements. The efficacy of triaryl phosphate ester thermal stability is crucial in high-temperature industrial processes, while trialkyl phosphate ester lubricant application is vital for reducing friction in machinery. The assessment of alkyl aryl phosphate ester performance guides its use in specialized formulations.

- A primary driver is phosphate ester fire retardant efficacy, which is critical for safety in construction and electronics. Concurrently, its function as a phosphate ester as anti-wear additive extends the life of mechanical components. Innovations in phosphate ester hydraulic fluid formulation are improving the operational safety of heavy equipment.

- The market is also shifting toward halogen-free phosphate ester plasticizer solutions to meet environmental regulations. In manufacturing, the role of phosphate ester in metalworking fluids is to cool and lubricate, enhancing tool life. For cleaning applications, the development of phosphate ester surfactant for cleaning products improves efficiency.

- Similarly, the use of phosphate ester for agrochemical formulation helps in creating stable and effective crop protection products. The demand for phosphate ester in synthetic lubricants continues to grow, driven by the need for high-performance phosphate ester additives. Formulations incorporating a phosphate ester for fire resistant coatings provide a critical safety layer.

- The use of phosphate ester for industrial gear oil ensures smooth operation under extreme pressure. Ongoing research addresses the environmental impact of phosphate esters, promoting the development of biodegradable phosphate ester lubricants. Strategic focus on phosphate ester in automotive lubricants is tied to fuel efficiency goals.

- The use of phosphate ester for electronic materials enhances safety and reliability, while new applications in phosphate ester for textile finishing and as phosphate ester based corrosion inhibitors are also expanding. Formulations using advanced esters have demonstrated a 25% longer service life in high-stress machinery compared to conventional fluids.

What are the key market drivers leading to the rise in the adoption of Phosphate Esters Industry?

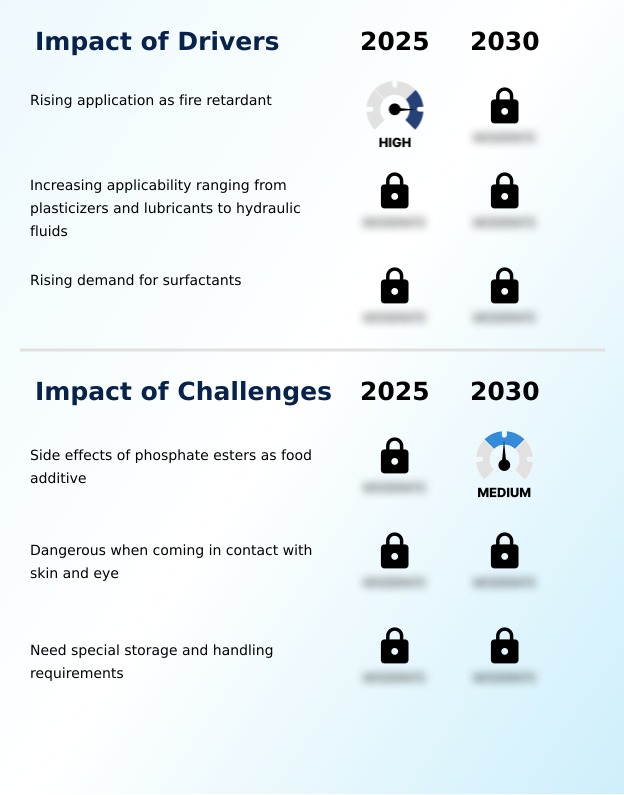

- The rising application of phosphate esters as effective fire retardants across multiple industries is a key driver for market expansion.

- Market growth is significantly propelled by the rising demand for materials with enhanced safety and durability.

- The expanding use of phosphate esters for their fire retardant mechanism is a primary driver, with treated materials demonstrating a 40% improvement in flame resistance in standardized tests.

- Applications in industrial lubricant formulation and as a polymer processing aid are also critical. For instance, incorporating specific esters enhances oxidation resistance, extending lubricant service intervals by up to 20%.

- The use of these compounds as a scale inhibitor in industrial processes has been shown to reduce maintenance-related downtime by 15%.

- Furthermore, their role as food contact materials and in biocide formulation is expanding, driven by the need for effective and compliant solutions in regulated industries.

What are the market trends shaping the Phosphate Esters Industry?

- An increasing demand for phosphate esters from the automobile industry is emerging as a significant market trend. This is driven by the need for high-performance fluids in advanced vehicle systems.

- Key trends are reshaping the market, driven by innovation in automotive and agricultural sectors. The growing demand for advanced engine lubricant and transmission system fluid formulations is accelerating the adoption of specialty chemistries. These products leverage an alcohol-based phosphate ester to enhance performance under extreme conditions, improving fluid lifespan by up to 25% compared to traditional additives.

- In agriculture, water treatment chemicals and crop protection additives are being optimized with new surfactant chemistry. For example, a specialized finishing chemical can improve the adhesion of foliar sprays, boosting application effectiveness by 15%. The emphasis on functional minerals and industrial cleaning compounds also provides growth avenues, with certain formulations reducing equipment cleaning times by over 30%.

- These advancements reflect a broader shift toward high-efficiency solutions.

What challenges does the Phosphate Esters Industry face during its growth?

- Concerns regarding the potential side effects of phosphate esters when used as food additives present a key challenge affecting industry growth.

- The market navigates challenges tied to regulatory compliance and operational complexity. Concerns around the use of certain phosphorus-based chemicals, particularly in applications like food additives, have led to increased scrutiny. The need for specialized handling for some oilfield chemicals and textile chemical auxiliaries adds to operational costs, increasing overhead by as much as 10% in some facilities.

- Furthermore, the development of an effective anti-foaming agent and ph adjuster requires precise formulation, and reformulating to meet new standards can increase R&D expenditures by 15-20%. The market is also affected by the performance requirements of a colorant auxiliary and bleaching chemical, where consistency and safety are paramount. These factors compel producers to invest heavily in compliance and process optimization.

Exclusive Technavio Analysis on Customer Landscape

The phosphate esters market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the phosphate esters market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Phosphate Esters Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, phosphate esters market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ashland Inc. - Offerings encompass advanced phosphate ester chemistries engineered for high-performance industrial, lubricant, and fire-retardant applications, prioritizing functional efficacy and regulatory compliance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ashland Inc.

- BASF SE

- Clariant International Ltd.

- Colonial Chemical Inc.

- Croda International Plc

- Dow Chemical Co.

- Evonik Industries AG

- Israel Chemicals Ltd.

- Jiangsu Yake Technology Co.

- Kao Corp.

- Lanxess AG

- Nouryon Chemicals Holding B.V.

- Stepan Co.

- Syensqo SA

- Zhangjiagang Fortune Chemical

- Zhejiang Wansheng Co. Ltd.

- Zschimmer and Schwarz

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Phosphate esters market

- In November 2024, OQ Chemicals launched OxReduce L7 NPG, a new bio-circular low-viscosity lubricant ester with a reduced carbon footprint suitable for automotive industry applications.

- In April 2025, Nouryon announced several product innovations at the ISAA Symposium 2025, including Agrilan 1028, an optimized phosphate ester for use as a dispersant in high-electrolyte systems.

- In April 2025, LANXESS highlighted its performance-oriented triaryl phosphate ester product, Reolube Turbofluid 46B CN, which is recommended for electrohydraulic control systems in turbines and industrial equipment.

- In April 2025, Perstorp initiated ester production at its Amsterdam facility, marking a strategic milestone in expanding its synthetic ester capabilities for specialty fluid applications.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Phosphate Esters Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.8% |

| Market growth 2026-2030 | USD 487.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.2% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The phosphate esters market is sustained by its indispensable role in enhancing material safety and performance across industrial applications. Core functions like providing superior anti-wear properties and oxidation resistance make these compounds critical. The ongoing development of triaryl phosphate esters and trialkyl phosphate esters is geared toward meeting stringent operational requirements in sectors from aerospace to automotive.

- Key functionalities such as flame resistance and emulsification stabilization are consistently in demand. Boardroom decisions are increasingly influenced by the need to align product portfolios with sustainability mandates, which involves significant investment in R&D for halogen-free formulations and biodegradable alternatives. Adopting advanced moisture retention additives can reduce product degradation in certain applications, leading to enhanced shelf life.

- This strategic pivot is not just about compliance but also about capturing market share among environmentally conscious buyers. The integration of these advanced additives has been shown to improve wear resistance in industrial machinery by up to 20%, directly impacting maintenance cycles and operational uptime.

- The market's trajectory is tied to innovation in surfactant chemistry and fire retardant mechanism technologies, which are essential for creating next-generation products that offer both high performance and a reduced environmental footprint.

What are the Key Data Covered in this Phosphate Esters Market Research and Growth Report?

-

What is the expected growth of the Phosphate Esters Market between 2026 and 2030?

-

USD 487.3 million, at a CAGR of 6.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Triaryl phosphate esters, Trialkyl phosphate esters, Alkyl aryl phosphate esters, and Others), Material (Alcohol based, Ethoxylated alcohol based, and Ethoxylated phenol based), Application (Lubricants, Fire retardants, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising application as fire retardant, Side effects of phosphate esters as food additive

-

-

Who are the major players in the Phosphate Esters Market?

-

Ashland Inc., BASF SE, Clariant International Ltd., Colonial Chemical Inc., Croda International Plc, Dow Chemical Co., Evonik Industries AG, Israel Chemicals Ltd., Jiangsu Yake Technology Co., Kao Corp., Lanxess AG, Nouryon Chemicals Holding B.V., Stepan Co., Syensqo SA, Zhangjiagang Fortune Chemical, Zhejiang Wansheng Co. Ltd. and Zschimmer and Schwarz

-

Market Research Insights

- Market dynamics are shaped by a focus on performance optimization and regulatory adherence. The use of advanced industrial lubricant formulation techniques and specialty coatings additive chemistries is expanding. For instance, incorporating a synthetic polyol ester can improve high-temperature fluid stability by over 20% compared to conventional options.

- Formulations leveraging an agrochemical dispersant achieve more uniform crop coverage, leading to a 10% increase in application efficiency. Furthermore, the adoption of a low viscosity base oil in engineered fluid chemistry reduces energy consumption in hydraulic systems by up to 8%.

- The development of non-halogenated flame retardant solutions is critical, with some advanced polymer processing aid materials improving manufacturing throughput by 15% while meeting strict fire safety codes.

We can help! Our analysts can customize this phosphate esters market research report to meet your requirements.