Pallets Market Size 2024-2028

The pallets market size is forecast to increase by USD 22.43 billion at a CAGR of 5.3% between 2023 and 2028.

What will be the Size of the Pallets Market During the Forecast Period?

How is this Pallets Industry segmented and which is the largest segment?

The pallets industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Material

- Wood

- Plastic

- Metal

- Corrugated paper

- End-user

- Food and beverages

- Chemicals and pharmaceuticals

- Retail

- Construction

- Others

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- UK

- North America

- US

- Middle East and Africa

- South America

- APAC

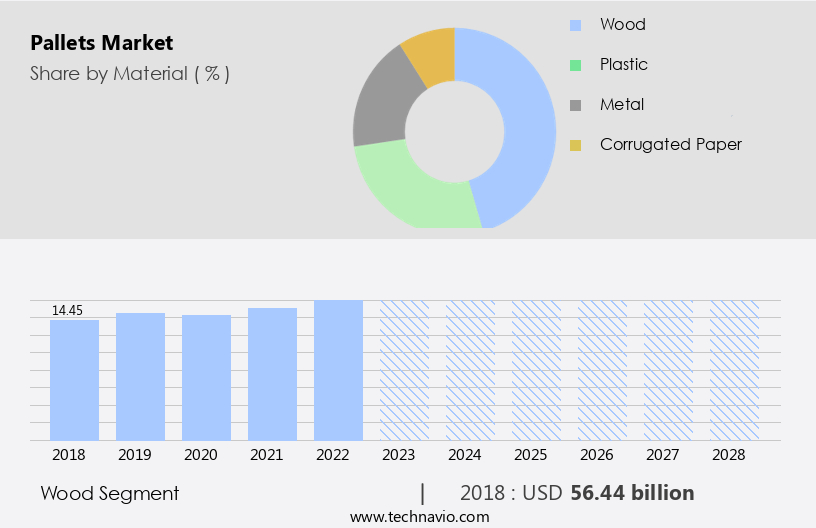

By Material Insights

The wood segment is estimated to witness significant growth during the forecast period. The market encompasses various material types, with wood being a prominent segment due to its cost-effectiveness and durability. Wooden pallets are extensively utilized in logistics and supply chain industries for transporting and storing goods in sectors such as construction and chemicals. The availability and affordability of wood make it an attractive choice for businesses aiming to minimize logistics expenses. Wood pellets exhibit high strength and resistance to damage, making them suitable for handling demanding supply chain operations, including food and beverage and retail industries. Sustainable packaging solutions, such as recycling techniques, are increasingly integrated into the market, with wood pellets offering eco-friendly alternatives.

Smart technologies, including RFID chips and GPS sensors, are also incorporated into pallets for enhanced tracking and automation, benefiting industries like pharmaceuticals and chemicals. Business expansion strategies, such as collaboration with sanitary, durable, and contamination-free material handling solutions providers, are essential for companies to remain competitive in this market. Wooden, plastic, composite wood, metal, corrugated, and other pallet types cater to diverse industry requirements, with plastic pallets offering lightweight and carbon footprint-reduced alternatives for big loads and standard temperatures. The market is influenced by factors such as international trade, logistics, and the global economy, with trade barriers and economic growth in developing nations impacting demand.

Disposable plastic pallets are used for transportation purposes and traded commodities, while rivers, cross-border trade, oceans, and global freight facilitate their movement. The market is expected to grow as businesses seek efficient, cost-effective, and sustainable material handling solutions.

Get a glance at the market report of various segments Request Free Sample

The Wood segment was valued at USD 56.44 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 49% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market In the APAC region is experiencing significant growth due to the region's industrialization and expanding supply chain networks. Wood is a prominent raw material In the APAC pellets market, with wood pellets being favored for their affordability, availability, and recyclability. Major contributors to this market include China and India, both of which have burgeoning manufacturing industries. For instance, China, a manufacturing hub, relies heavily on wooden pallets for transporting goods within its intricate supply chains. Smart technologies, such as RFID chips and GPS sensors, are increasingly being integrated into pallets for enhanced tracking and automation in material handling solutions.

The market caters to various industry verticals, including food and beverage, pharmaceutical, and chemical sectors, requiring sanitary, durable, and contamination-free pallets. Sustainable packaging, recycling techniques, and business expansion strategies are also driving the market's growth. Despite challenges like lockdowns and international trade disruptions, the market continues to adapt, with an emphasis on lightweight, carbon footprint-reducing materials like HDPE and other composites. The market's future lies In the adoption of advanced technologies, such as collaborative robots (cobots), to streamline logistics and improve efficiency. The market plays a crucial role In the global economy, facilitating the transportation of traded commodities via rivers, cross-border trade, and global freight networks.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Pallets Industry?

- Increasing adoption of automation and robotics to ease pallet use in manufacturing processes is the key driver of the market.The market is witnessing significant growth due to the increasing adoption of smart technologies, including RFID chips and GPS sensors, in logistics and industry verticals. Material types, such as wood, plastic, composite wood, metal, corrugated, and various other types, cater to diverse business needs. Wood pallets, known for their durability and sustainability, are being increasingly used In the food and beverage, pharmaceutical, and chemical sectors due to their sanitary and contamination-free properties. Automation and collaborative robots (cobots) are transforming the market. Automated systems, including forklifts, pallet jacks, and front loaders, are used for stacking and product storage. The integration of RFID tags and automation in pallet production enhances precision and consistency, ensuring high-quality products.

The demand for pallets is driven by the need for unitization, sustainable packaging, and recycling techniques. Plastic pallets, made from high-density polyethylene (HDPE) material, are lightweight and have a reduced carbon footprint. However, they may have reduced durability compared to wooden pallets, which absorb moisture and are prone to splinter breaking. Logistics and international trade, including rivers, cross-border trade, oceans, and global freight, require pallets for transportation purposes. Economic growth in developing nations and the eradication of poverty are fueling the expansion of businesses, leading to increased demand for pallets. Despite trade barriers, the world economy and global trade continue to drive market growth.

What are the market trends shaping the Pallets market?

- Increasing demand for nestable and stackable pallets is the upcoming market trend.Nestable and stackable pallets are essential material handling solutions in various industry verticals, including food and beverage, pharmaceutical, and chemical sectors. These pallets come in different materials such as wood, plastic, composite wood, metal, and corrugated. Nestable pallets, featuring a unique design, enable users to save space during transportation and storage by nesting inside one another. This results in reduced shipping and storage costs for businesses. In contrast, stackable pallets are designed for secure stacking, significantly decreasing loading and unloading time in distribution centers. The market dynamics for nestable and stackable pallets are influenced by several factors. The increasing demand for sustainable packaging and recycling techniques, smart technologies like RFID chips and GPS sensors, and business expansion strategies are key driving forces.

Logistics efficiency and supply chain optimization are crucial considerations, particularly In the context of international trade and the transportation of traded commodities via rivers, cross-border trade, and oceans. Material type plays a significant role In the selection of nestable and stackable pallets. For instance, plastic pallets offer lightweight, durable, and sanitary alternatives, while wooden pallets are known for their high strength and moisture absorption. Composite wood pallets provide a balance between the advantages of wood and plastic, and metal pallets offer superior strength and resistance to contamination. Automation technologies, such as collaborative robots (cobots), are increasingly being integrated into material handling processes, further enhancing the efficiency and productivity of operations involving nestable and stackable pallets.

The global economy and international trade are significant factors influencing the market, with developing nations contributing to economic growth and the eradication of poverty through increased integration into the global trade system.

What challenges does the Pallets Industry face during its growth?

- Fluctuating prices of raw materials used for manufacturing pallets is a key challenge affecting the industry growth.The global pellets market encompasses various material types, including wood, plastic, composite wood, and metal. Wood, as a primary raw material, is subject to price fluctuations due to weather conditions, logging restrictions, and international timber demand. For instance, the COVID-19 pandemic led to disrupted supply chains and a surge in lumber demand in construction, resulting in a drop in wood prices and subsequent impact on the pricing of wooden pellets. This affected industries such as food and beverage, construction, and retail, which heavily rely on wooden pellets, causing unexpected financial losses and operational challenges. Similarly, the price of plastic pellets, another preferred material for their durability and sustainability, is influenced by raw material costs.

Companies seeking unitization solutions, sustainable packaging, and recycling techniques must consider these market dynamics. Smart technologies like RFID chips, GPS sensors, and automation tools, including collaborative robots (cobots), are increasingly utilized to optimize logistics and improve industry verticals. The demand for pallets continues to grow, driven by factors like big loads, standard temperatures, and traded commodities transported via rivers, cross-border trade, and oceans. Companies expanding their businesses must consider the environmental impact, with options like lightweight, carbon footprint-reducing HDPE material, and the availability of disposable plastic pallets for transportation purposes. The global economy and international trade are interconnected, with trade barriers in developing nations potentially impacting economic growth, development, and the eradication of poverty.

Pallets play a crucial role in material handling solutions, including stacking, product storage, and lifting equipment like forklifts, pallet jacks, and front loaders.

Exclusive Customer Landscape

The pallets market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the pallets market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, pallets market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

AUER GmbH - The company specializes in providing a range of pallet solutions, including lightweight, medium, and cleanroom options, catering to various industries and applications. These pallets are engineered for optimal durability, weight capacity, and sanitation standards, ensuring efficient material handling and logistics operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AUER GmbH

- Brambles Ltd.

- CABKA Group GmbH

- Canada Pallet Source

- Cargopak Ltd.

- Casadei Pallets Srl

- Craemer GmbH

- Dolav

- Falkenhahn AG

- HG Timber Ltd.

- Imbal Legno Snc

- Nefab AB

- Pallet Management Group Inc.

- PGS Group

- Sacchi Pallets Srl

- Schoeller Allibert

- TESER SNC

- Toscana Pallets Srl

- UFP Industries Inc.

- Van Leyen Pallets

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a diverse range of products utilized for unitization and material handling in various industries. The primary materials used in pallet manufacturing include RFID chips integrated into different types of pallets such as wood, plastic, composite wood, metal, corrugated, and various other materials. These smart technologies enable efficient tracking and management of inventory, enhancing logistics and supply chain operations. The pallets industry caters to numerous industry verticals, including logistics, food and beverage, pharmaceutical, chemical, and others. The demand for pallets is driven by the need for efficient material handling solutions, particularly in sectors where sanitary, durable, and contamination-free pallets are essential.

Pallets come in various forms, including stackable, nestable, rackable, and display pallets, each designed to cater to specific application requirements. Wooden pallets, known for their durability and strength, have been a long-standing choice for material handling. However, they are susceptible to moisture absorption, reduced durability, and splinter breaking, leading to the increasing popularity of alternative materials. Plastic pallets, made from HDPE material, offer several advantages, such as lightweight design, reduced carbon footprint, and resistance to moisture and contamination. They are particularly suitable for big loads and standard temperatures. However, disposable plastic pallets are often used for transportation purposes and traded commodities, while reusable plastic pallets are preferred for long-term use in industries.

The market is influenced by several factors, including international trade, economic growth, and development in developing nations. The integration of countries into the global economy and the eradication of poverty have led to increased demand for pallets in various sectors. Automation and advanced technologies, such as collaborative robots (cobots), RFID tags, and GPS sensors, have revolutionized the pallets industry, enabling more efficient and accurate material handling. Business expansion strategies In the market are focused on offering eco-friendly and sustainable packaging solutions, reducing the carbon footprint, and implementing recycling techniques. The market is a critical component of global freight and trade, with pallets being used extensively In the transportation of goods via rivers, cross-border trade, and oceans.

The market dynamics are influenced by global economic conditions, trade barriers, and the overall state of the world economy. In conclusion, the market is a dynamic and evolving industry, driven by the need for efficient material handling solutions and the integration of advanced technologies. The market caters to various industries and application requirements, with a focus on sustainability and eco-friendly practices.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

162 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.3% |

|

Market growth 2024-2028 |

USD 22.43 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.11 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Pallets Market Research and Growth Report?

- CAGR of the Pallets industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the pallets market growth of industry companies

We can help! Our analysts can customize this pallets market research report to meet your requirements.

RIA -

RIA -