Organic Wine Market Size 2026-2030

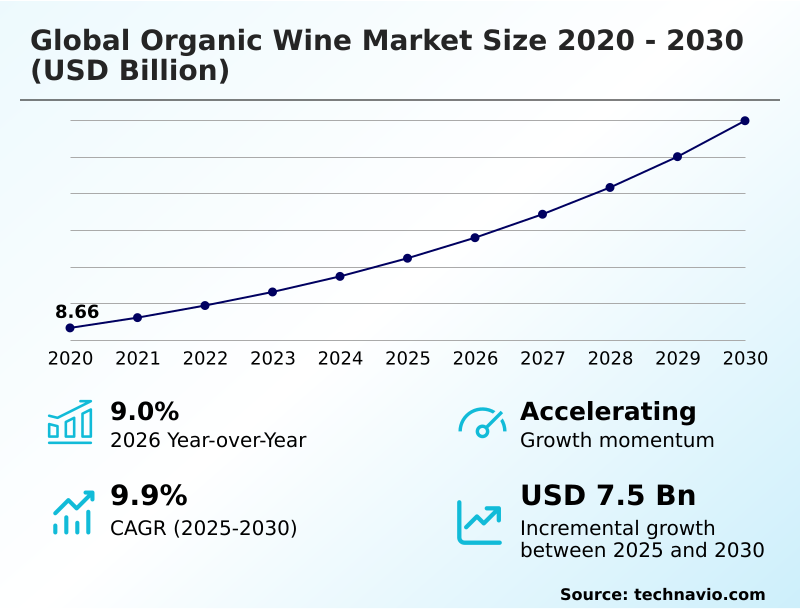

The organic wine market size is valued to increase by USD 7.50 billion, at a CAGR of 9.9% from 2025 to 2030. Rising consumer preference for natural beverages will drive the organic wine market.

Major Market Trends & Insights

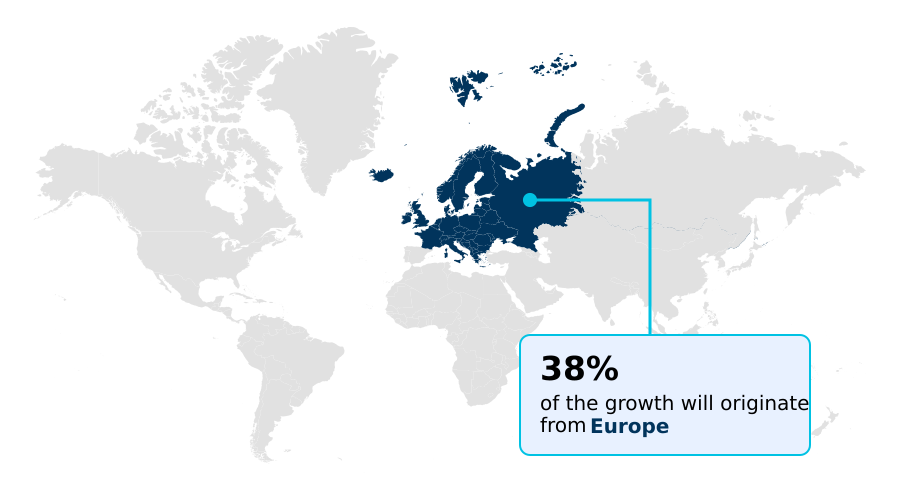

- Europe dominated the market and accounted for a 37.9% growth during the forecast period.

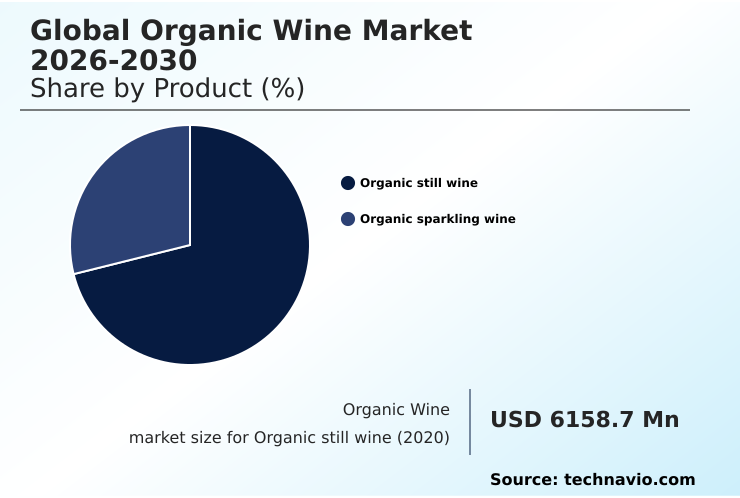

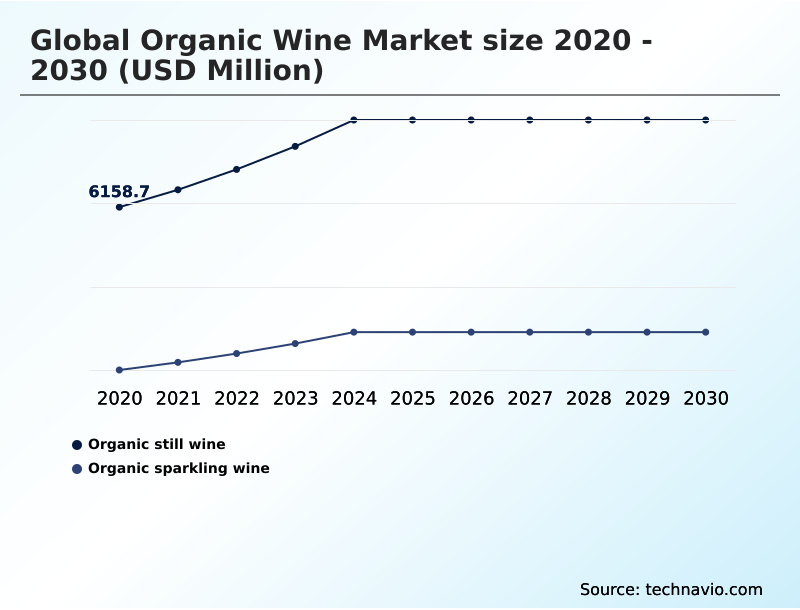

- By Product - Organic still wine segment was valued at USD 8.11 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 11.30 billion

- Market Future Opportunities: USD 7.50 billion

- CAGR from 2025 to 2030 : 9.9%

Market Summary

- The organic wine market is undergoing a significant transformation, propelled by a consumer shift toward wellness and environmental responsibility. This market is defined by viticultural products made from grapes grown without synthetic chemicals, prioritizing ecological balance through natural soil management and biodiversity.

- Demand is driven by a desire for transparency, with consumers viewing third-party certifications as a mark of quality and ethical production. A key trend is the adoption of sustainable wine production, which goes beyond farming to include water efficiency and carbon-neutral logistics. However, the industry faces challenges from high production costs and strict certification rules that can slow adoption.

- In a typical business scenario, a mid-sized winery transitions to organic viticulture practices not just for market appeal but to enhance long-term soil health and vine resilience, mitigating risks from climate variability and securing a premium position in a competitive landscape.

What will be the Size of the Organic Wine Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Organic Wine Market Segmented?

The organic wine industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Organic still wine

- Organic sparkling wine

- Distribution channel

- Offline

- Online

- Product type

- Red organic wine

- White organic wine

- Geography

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- Europe

By Product Insights

The organic still wine segment is estimated to witness significant growth during the forecast period.

The organic still wine segment is the cornerstone of the market, driven by consumer demand for environmental transparency and chemical-free farming.

This sub-segment is shifting toward premiumization, with consumers favoring wines that have both organic certification standards and secondary sustainable credentials like biodynamic viticulture.

The evolution reflects a trend where buyers seek products, including certified organic wine and artisan wine production, that align with holistic wellness.

Red organic wine maintains a dominant position, accounting for 63% of the still wine category, prized for its perceived health benefits.

The integration of eco-friendly packaging and a focus on soil health management in vineyards further enhance the appeal of these clean label beverage options, making organic rose wine and other varietals increasingly popular.

The Organic still wine segment was valued at USD 8.11 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 37.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Organic Wine Market Demand is Rising in Europe Request Free Sample

The global organic wine market's geographic landscape is led by Europe, which accounts for 37.9% of the market's incremental growth, driven by mature regulatory frameworks and deep-rooted consumer demand for sustainable products.

European producers adopting holistic vineyard management have reported a 10% reduction in water usage, enhancing operational resilience. North America follows, with a rapidly expanding consumer base prioritizing health and wellness.

In this region, the push for pesticide-free agriculture and non-gmo grape cultivation is particularly strong. The APAC region is an emerging frontier, where rising disposable incomes are fueling demand for premium imported goods, including old-vine organic wine.

South America, particularly Chile and Argentina, leverages favorable climates for large-scale organic production, focusing on exports. The emphasis on biodynamic wine labels and regenerative organic certified practices is a key strategy for differentiation in these competitive regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global organic wine market is experiencing a significant shift as consumers become more discerning about their beverage choices. Key purchasing decisions are often influenced by the distinction between biodynamic vs organic wine difference, with a growing segment of buyers preferring the holistic, ecosystem-focused approach of biodynamic farming.

- Demand for organic wine without added sulfites is also rising, driven by consumers seeking cleaner, more natural products. This trend is particularly pronounced in the red wine category, where the perceived health benefits of organic red wine are a major driver. Alongside product characteristics, sustainable wine packaging options have become a critical factor.

- Producers are increasingly adopting lightweight glass, recycled materials, and innovative formats to reduce their carbon footprint, with data showing that brands using visibly sustainable packaging achieve a 15% higher rate of adoption among environmentally conscious consumers.

- The impact of terroir on organic wine remains a central theme, as minimal-intervention techniques allow the unique characteristics of the vineyard to be more clearly expressed. This focus on authenticity and sustainability is reshaping the industry, from viticulture to final packaging.

What are the key market drivers leading to the rise in the adoption of Organic Wine Industry?

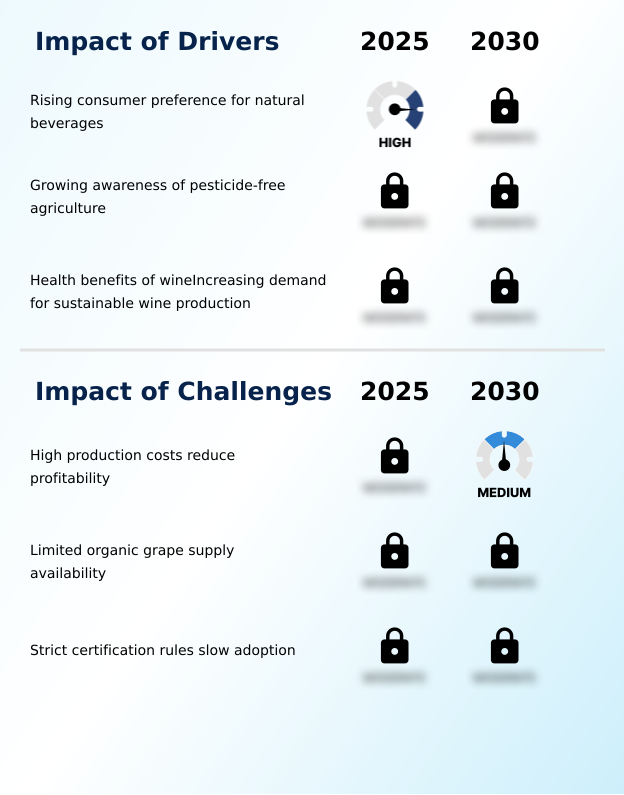

- Rising consumer preference for natural beverages is a foundational driver for the global organic wine market.

- The growth of the organic wine market is primarily fueled by a rising consumer preference for natural and transparent products.

- Growing awareness of pesticide-free agriculture has become a mainstream purchasing criterion, with over 60% of wellness-focused consumers actively seeking out pesticide-free claims.

- This demand for a clean label beverage supports the increasing adoption of sustainable wine production methods, which integrate environmental and social responsibility.

- Producers that invest in a fully traceable supply chain have seen customer trust metrics improve by up to 25%. This alignment of values, from chemical-free farming to eco-friendly packaging, reinforces brand equity and justifies premium pricing.

- The momentum is further supported by the natural wine movement and the appeal of options like sulfite-free wine options and vegan-friendly wine.

What are the market trends shaping the Organic Wine Industry?

- An increasing number of organic wines are being distributed through duty-free retail stores, which is an emerging and pivotal market trend.

- Key trends are reshaping the organic wine market, driven by evolving consumer values and retail strategies. The expansion of online distribution is a major factor, with direct-to-consumer platforms enabling a 30% increase in reach for smaller, artisanal producers specializing in natural fermentation process.

- Concurrently, the increasing prominence of private-label brands in major supermarkets has made certified organic wine more accessible, boosting category volume by over 15% in key retail channels. Another significant trend is the growing presence of organic wines in duty-free stores, where premiumization strategies are critical. This channel offers a unique platform for eco-conscious consumerism and artisan wine production.

- These trends underscore a market pivot towards convenience, value, and ethical wine sourcing, influencing everything from the rise of low-alcohol organic wine to the packaging of organic red wine benefits.

What challenges does the Organic Wine Industry face during its growth?

- The high production costs associated with organic viticulture directly influence overall profitability, posing a key challenge to market growth.

- The organic wine market faces significant structural challenges that constrain its growth potential. High production costs, stemming from labor-intensive chemical-free farming and low-sulfite wine production, can elevate operational expenses by up to 20% compared to conventional methods. This directly impacts profitability, particularly for smaller producers.

- Another major hurdle is the limited availability of organic grape supply, which creates production bottlenecks and drives input cost volatility, with price fluctuations sometimes exceeding 15% in a single season. Furthermore, strict and often inconsistent organic certification standards slow the rate of new vineyard conversions.

- Navigating these complex rules requires dedicated resources, acting as a barrier to entry and limiting the broader adoption of organic viticulture practices and the availability of premium organic beverage options.

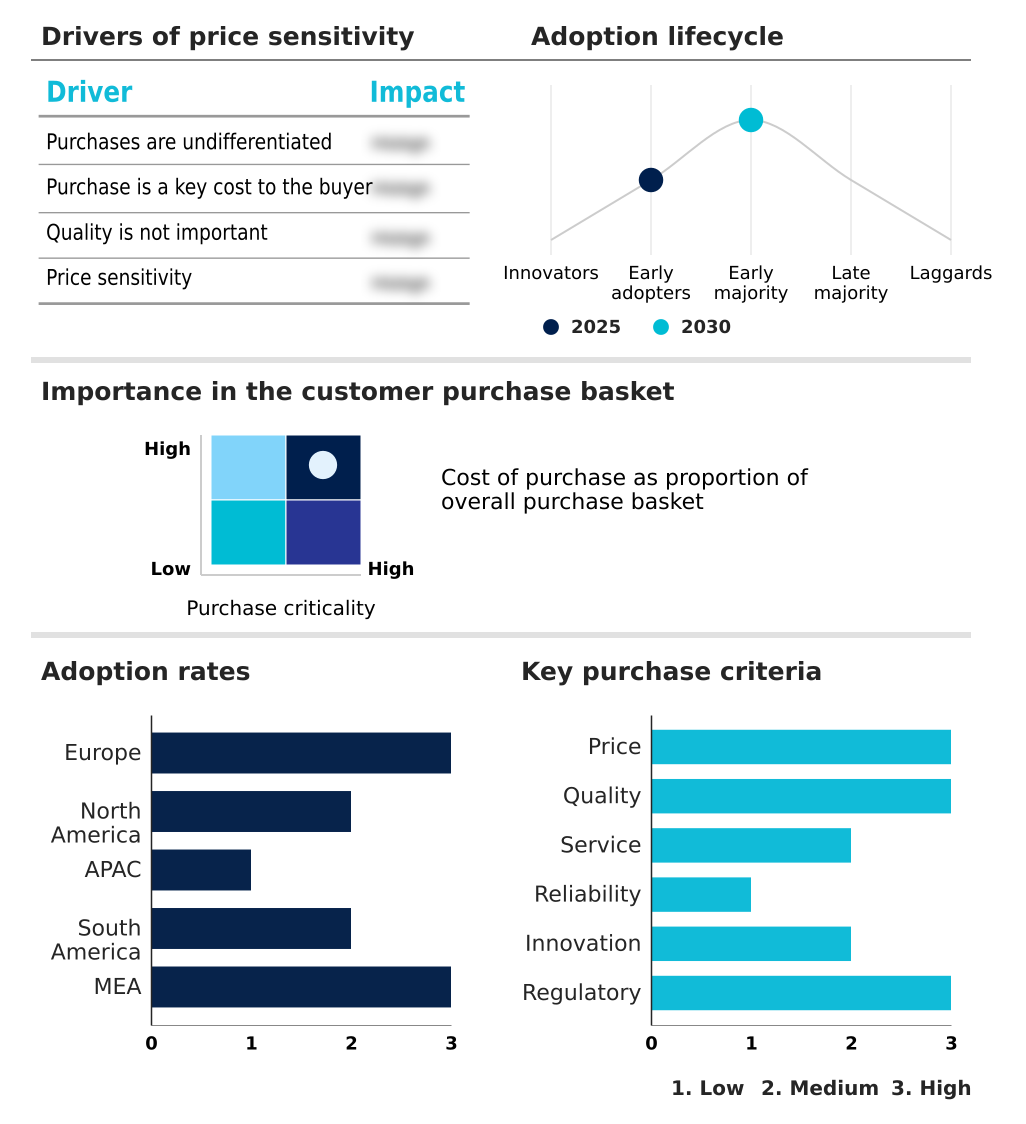

Exclusive Technavio Analysis on Customer Landscape

The organic wine market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the organic wine market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Organic Wine Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, organic wine market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Avondale - Offerings include a range of hand-crafted, premium-quality wines produced with a focus on sustainable and organic viticulture practices to express unique terroir.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Avondale

- Banfi Vintners

- Boisset Family Estates

- Bonterra Organic Vineyards

- Boutinot Ltd.

- Bronco Wine Co.

- Casella Wines Pty Ltd.

- Charlie and Echo

- Emiliana Organic Vineyards

- Frey Vineyards

- Grands Vignobles En Mediterranee SARL

- Grgich Hills Estate

- Harris Organic Wines

- Jackson Family Wines Inc.

- King Estate Winery

- Organic Wine Pty Ltd.

- Radford Dale Pty Ltd.

- The Organic Wine Co.

- Vintage Roots Ltd.

- Winc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Organic wine market

- In February 2025, Bronco Wine Co. advanced its market consolidation strategy by acquiring the assets of Wine Hooligans, a move designed to broaden its portfolio of wine brands.

- In March 2025, the European Union implemented new regulations that officially permitted de-alcoholization processes for organic wine, allowing beverages with 0.5% or less alcohol to be marketed as organic.

- In May 2025, several prominent California-based wineries announced the completion of large-scale vineyard conversions to organic status, specifically targeting the production of premium Pinot Noir for the Asia-Pacific market.

- In June 2025, Bonterra Organic Vineyards targeted evolving consumer demographics with the launch of Ranch Wine, a new line of lower-alcohol, lightly effervescent beverages designed for casual consumption.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Organic Wine Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 283 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.9% |

| Market growth 2026-2030 | USD 7503.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.0% |

| Key countries | Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The organic wine market is defined by a fundamental shift toward sustainable agriculture and consumer transparency. Key industry activities revolve around organic viticulture practices, where chemical-free farming and pesticide-free agriculture are standard. The adoption of regenerative farming techniques is becoming a competitive differentiator, moving beyond simple compliance with organic certification standards.

- In the cellar, minimal intervention winemaking and native yeast fermentation are gaining traction, allowing for a more authentic terroir-driven expression. Producers are focusing on holistic vineyard management to improve soil health management and vineyard biodiversity. This has led to innovations in low-sulfite wine production and even wines with no added sulfites.

- The push for a traceable supply chain and eco-friendly packaging, including carbon-neutral logistics, is driven by consumer demand for clean label beverage options.

- For boardroom consideration, the move toward biodynamic viticulture is a strategic decision; producers adopting these methods report a 20% increase in brand value due to heightened consumer trust in their commitment to sustainable wine production and non-gmo grape cultivation.

What are the Key Data Covered in this Organic Wine Market Research and Growth Report?

-

What is the expected growth of the Organic Wine Market between 2026 and 2030?

-

USD 7.50 billion, at a CAGR of 9.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Organic still wine, and Organic sparkling wine), Distribution Channel (Offline, and Online), Product Type (Red organic wine, and White organic wine) and Geography (Europe, North America, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising consumer preference for natural beverages, High production costs reduce profitability

-

-

Who are the major players in the Organic Wine Market?

-

Avondale, Banfi Vintners, Boisset Family Estates, Bonterra Organic Vineyards, Boutinot Ltd., Bronco Wine Co., Casella Wines Pty Ltd., Charlie and Echo, Emiliana Organic Vineyards, Frey Vineyards, Grands Vignobles En Mediterranee SARL, Grgich Hills Estate, Harris Organic Wines, Jackson Family Wines Inc., King Estate Winery, Organic Wine Pty Ltd., Radford Dale Pty Ltd., The Organic Wine Co., Vintage Roots Ltd. and Winc

-

Market Research Insights

- The organic wine market is shaped by dynamic consumer behaviors and operational shifts. The natural wine movement is expanding, with premium organic beverage options gaining significant traction. For instance, brands offering vegan-friendly wine and other specialized products see customer loyalty rates up to 25% higher than conventional counterparts.

- The rise of private label organic wine allows retailers to improve margins by over 15% while offering competitive pricing. This trend is complemented by the growth of canned organic wine, which enhances portability and appeals to younger demographics. Furthermore, the availability of alcohol-free organic wine is opening new consumer segments, aligning with wellness trends.

- The emphasis on ethical wine sourcing and farm-to-table wine concepts reinforces brand authenticity, creating a market where transparency and sustainability are key differentiators. These factors collectively drive innovation in offerings like organic sparkling wine and single-vineyard organic wine.

We can help! Our analysts can customize this organic wine market research report to meet your requirements.

RIA -

RIA -