On-device AI Market Size 2026-2030

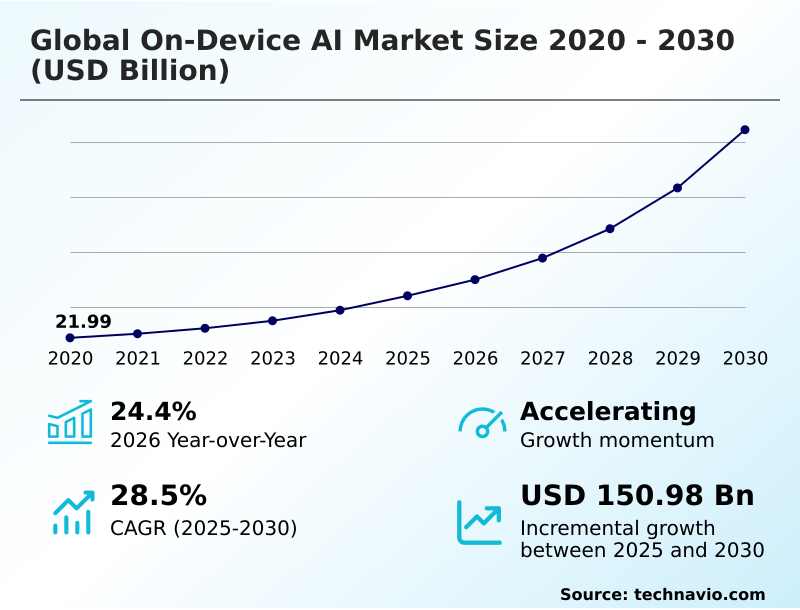

The on-device ai market size is valued to increase by USD 150.98 billion, at a CAGR of 28.5% from 2025 to 2030. Growing demand for enhanced data privacy and security will drive the on-device ai market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 47.1% growth during the forecast period.

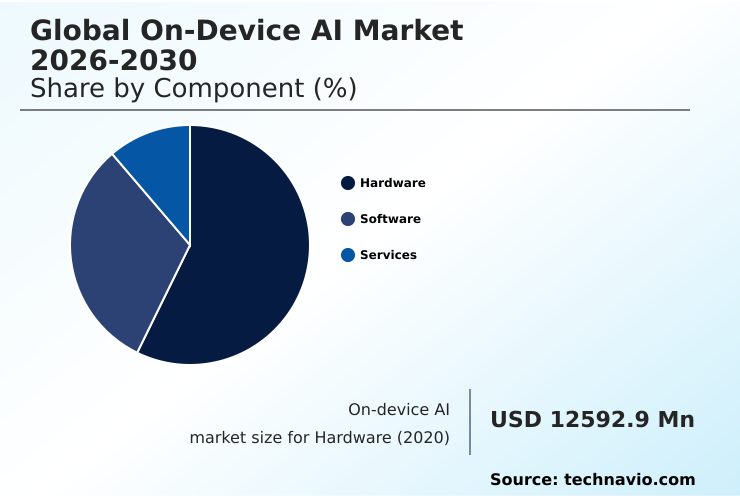

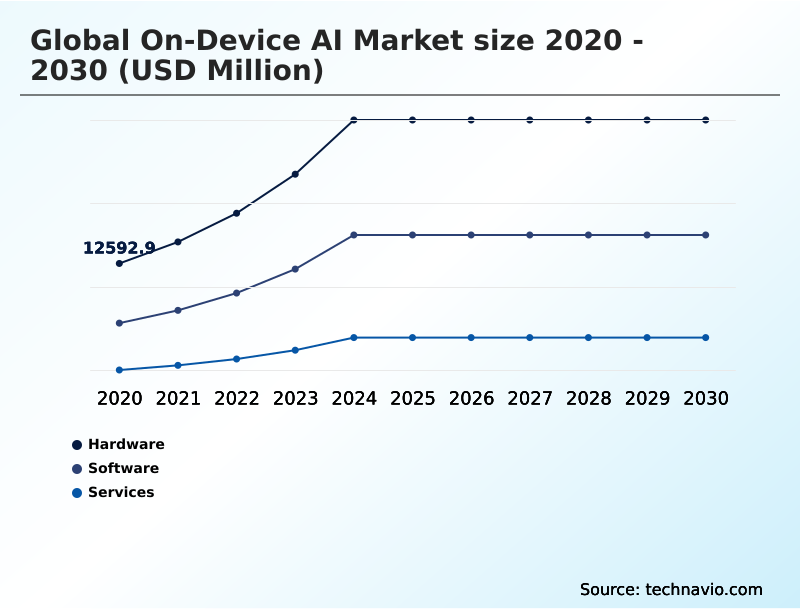

- By Component - Hardware segment was valued at USD 26.22 billion in 2024

- By Technology - 7 nm segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 189.18 billion

- Market Future Opportunities: USD 150.98 billion

- CAGR from 2025 to 2030 : 28.5%

Market Summary

- The on-device AI market is defined by the integration of sophisticated intelligence directly into hardware, eliminating the need for constant cloud connectivity. This shift is driven by the demand for real-time responsiveness, enhanced data privacy, and improved power efficiency in devices ranging from smartphones to industrial sensors.

- Key technologies such as AI-optimized silicon, including neural processing units and tensor processing cores, provide the necessary computational power for local inference. A significant trend is the development of small language models and on-device generative AI, which allow for complex tasks like text and image creation without sending data to external servers.

- For instance, in a connected vehicle, on-device AI processes sensor data for autonomous navigation, ensuring split-second decisions that are critical for safety, a task where latency from cloud processing would be unacceptable. However, the industry faces challenges related to power consumption, thermal management, and the complexity of model optimization for diverse hardware.

- As hardware and software co-design advances, the capabilities of on-device AI are expected to expand, further embedding intelligent, privacy-preserving features into everyday technology and enterprise systems.

What will be the Size of the On-device AI Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the On-device AI Market Segmented?

The on-device ai industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Hardware

- Software

- Services

- Technology

- 7 nm

- 10 nm

- 20 to 28 nm

- Application

- Smartphones

- Wearables

- Smart speakers

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment serves as the physical foundation for the global on-device AI market 2026-2030, comprising the essential semiconductor architectures that execute complex machine learning algorithms.

This includes neural processing units, tensor processing cores, and other forms of AI-optimized silicon integrated into a system-on-chip. These components are engineered for the parallel processing and matrix multiplication inherent in deep learning, enabling features like on-device generative AI.

Effective thermal management solutions are critical, as they prevent performance throttling during intensive workloads. By using techniques like weight sharing, these systems achieve high efficiency.

Innovations in this area have shown to improve inference speed by 25% in certain applications, facilitating real-time responsiveness and advanced local inference without constant cloud dependency.

The Hardware segment was valued at USD 26.22 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 47.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How On-device AI Market Demand is Rising in APAC Request Free Sample

The geographic landscape of the on-device AI market is diverse, with regional priorities shaping innovation and adoption. In APAC, the focus is on mass-market hardware manufacturing, integrating AI-optimized silicon and neural processing units into consumer electronics at scale.

North America leads in foundational research and development, pioneering hardware-software co-design and vertical integration to create high-performance systems for advanced applications.

The region's emphasis on local inference and low latency processing has resulted in systems that improve data throughput by over 40% compared to previous generations.

Europe distinguishes itself with a strong regulatory focus on data privacy, driving the adoption of privacy-preserving AI and hybrid AI architecture.

This has spurred the development of technologies compliant with strict data sovereignty laws, positioning the region as a leader in ethical AI model deployment.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the on-device AI market is increasingly defined by sophisticated, long-tail applications that demand specialized hardware and software integration. The development of on-device AI for autonomous navigation is a prime example, where real-time sensor data fusion is critical for safety and requires robust, low-latency processing.

- Similarly, the push for low latency AI in augmented reality is transforming user experiences by enabling seamless digital overlays without perceptible lag. At the core of these advancements is the pursuit of power-efficient deep learning inference, allowing complex neural networks to run on battery-powered devices.

- The complexity of edge AI deployment on embedded systems remains a significant focus, as developers work to bring intelligence to a wider range of connected products. In industrial settings, real-time video analysis at the edge has demonstrated more than double the defect detection accuracy compared to previous cloud-reliant models.

- The challenge of optimizing generative AI for mobile devices is being met with innovative model compression techniques. Furthermore, strategies for hybrid cloud-edge AI workload balancing are becoming essential for managing computational resources efficiently. This is complemented by a focus on secure on-device biometric processing, which enhances security without compromising user privacy.

- The market's trajectory is clearly toward more autonomous, responsive, and secure intelligent systems deployed directly at the data source.

What are the key market drivers leading to the rise in the adoption of On-device AI Industry?

- The growing demand for enhanced data privacy and security is a primary driver for the on-device AI market, as processing data locally mitigates risks associated with cloud transmission.

- Market growth is propelled by a confluence of factors addressing fundamental user and enterprise needs.

- The imperative for enhanced data privacy is a primary driver, as local inference on devices eliminates the need to transmit sensitive information, a method shown to reduce data breach risks by over 60%.

- Equally important is the demand for real-time responsiveness and low latency processing, which is non-negotiable for applications like autonomous systems and augmented reality. On-device processing can cut latency by more than 95% compared to round-trip cloud communication.

- This is made possible by advancements in AI-optimized silicon, including specialized system-on-chip designs that deliver high performance with lower power consumption. The proliferation of this technology is enabling a new generation of intelligent, responsive, and secure applications.

What are the market trends shaping the On-device AI Industry?

- The emergence of on-device generative AI and small language models signifies a key market trend. This development involves shrinking large architectures to run sophisticated AI locally on consumer hardware.

- Key market trends are centered on making AI more accessible and efficient at the edge. The emergence of on-device generative AI, powered by small language models, allows devices to perform creative and reasoning tasks locally.

- This is enabled by advanced techniques like model distillation and knowledge distillation, which have proven to reduce model size by up to 80% without significant accuracy loss. Another dominant trend is the shift to a hybrid AI architecture, combining the benefits of local inference with the power of the cloud.

- This approach optimizes workloads, with studies showing a 40% improvement in application responsiveness. Furthermore, hardware-software co-design and vertical integration have become critical, enabling companies to achieve performance gains of over 50% compared to using off-the-shelf components.

What challenges does the On-device AI Industry face during its growth?

- Significant challenges for the on-device AI market include managing power consumption and thermal management constraints inherent in portable, high-performance hardware.

- Despite strong drivers, the market faces significant technical and economic hurdles. Power consumption constraints and thermal management are primary challenges, as intensive AI workloads can reduce battery life by up to 40% in mobile devices and trigger performance-throttling. The complexity of AI model deployment is another major barrier.

- Optimizing models for fragmented hardware environments through techniques like quantization and pruning requires specialized expertise and can increase development time by 30%. Furthermore, the high development costs associated with custom silicon and software stacks limit market entry for smaller players, as the initial investment for a new chip design can be substantial, concentrating market power among a few large organizations.

Exclusive Technavio Analysis on Customer Landscape

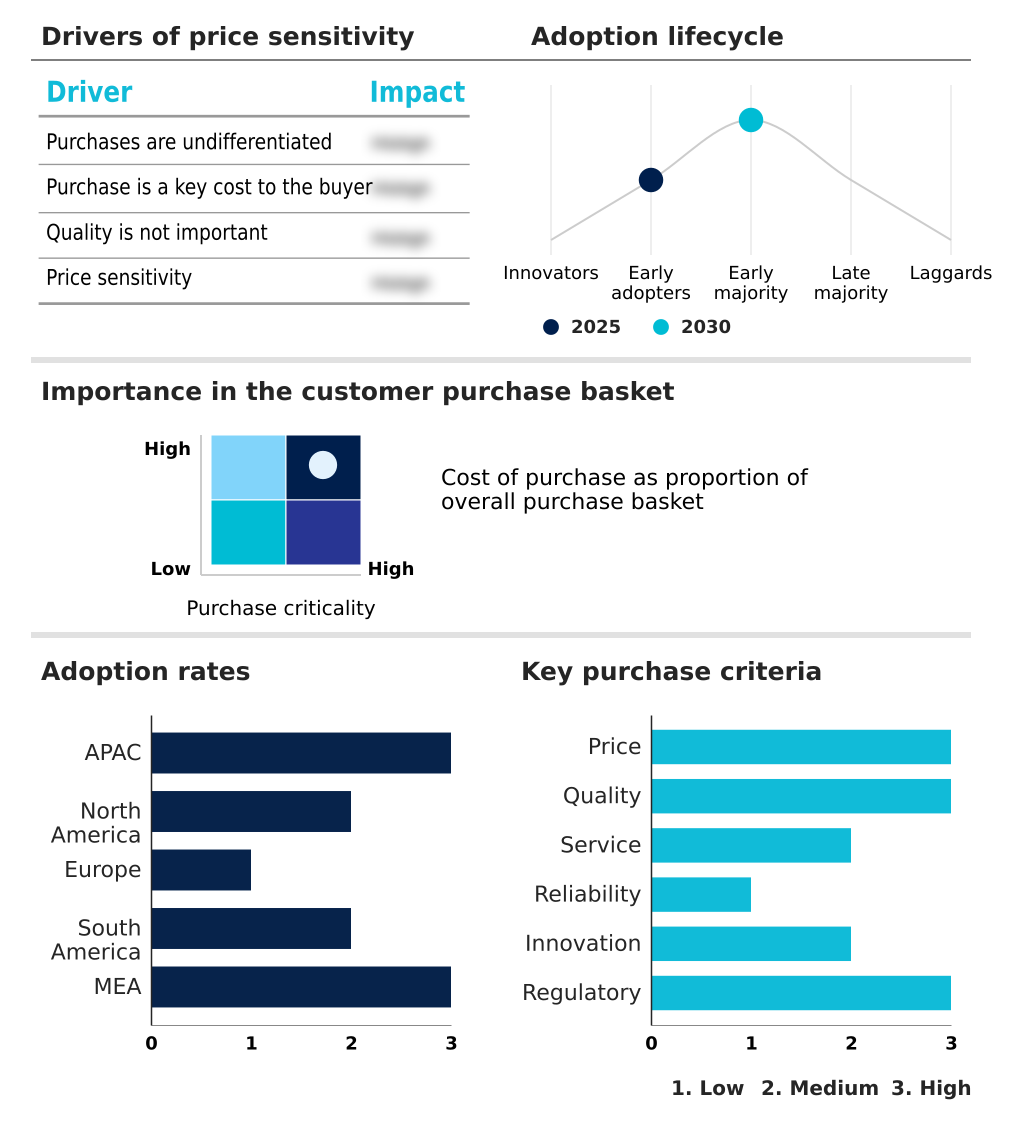

The on-device ai market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the on-device ai market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of On-device AI Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, on-device ai market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - The company offers on-device AI, including Ryzen AI processors, XDNA NPUs, and Radeon AI accelerators, designed for edge and local AI applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Ambarella Inc.

- Apple Inc.

- Google LLC

- Hailo Technologies Ltd.

- Huawei Technologies Co. Ltd.

- Infineon Technologies AG

- Intel Corp.

- MediaTek Inc.

- Microchip Technology Inc.

- Mythic Inc.

- NVIDIA Corp.

- NXP Semiconductors NV

- Qualcomm Inc.

- Renesas Electronics Corp.

- Samsung Electronics Co. Ltd.

- SiMa Technologies Inc.

- Sony Semiconductor Solutions

- STMicroelectronics NV

- Texas Instruments Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in On-device ai market

- In September 2024, Qualcomm Inc. announced its next-generation Snapdragon platform, featuring an upgraded Hexagon processor capable of running generative AI models with up to 20 billion parameters, enhancing on-device text-to-image generation.

- In November 2024, NVIDIA Corp. and a leading automotive manufacturer entered a strategic partnership to integrate the NVIDIA DRIVE platform into the automaker's 2027 vehicle lineup, enabling advanced driver-assistance systems powered by on-device AI.

- In February 2025, Apple Inc. acquired 'SynthEdge,' a startup specializing in ultra-low-power neural network models for an undisclosed amount, aiming to bolster its on-device processing capabilities for future products.

- In May 2025, Google LLC released an update to its TensorFlow Lite framework that improves model execution speed by 15% on NPUs through enhanced delegate support and optimized operators, expanding AI capabilities on mid-range devices.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled On-device AI Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 28.5% |

| Market growth 2026-2030 | USD 150980.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 24.4% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The on-device AI market is advancing through deep integration of hardware and software, a trend critical for achieving performance and efficiency gains. Innovations in AI-optimized silicon, including specialized neural processing units and tensor processing cores, are foundational.

- These components are not standalone solutions but are part of a vertical integration strategy where system-on-chip designs are co-developed with specialized compilers and runtime environments. This hardware-software co-design approach allows for superior optimization, addressing challenges like power consumption constraints and thermal management.

- For instance, companies that master this synergy have demonstrated a 30% reduction in processing time for complex AI tasks. This level of performance directly impacts boardroom decisions regarding product differentiation and market positioning. The process involves complex techniques such as model distillation, weight sharing, quantization, and pruning to shrink large models, like small language models, for local inference.

- This allows for the deployment of on-device generative AI while maintaining a responsive user experience, a key competitive advantage.

What are the Key Data Covered in this On-device AI Market Research and Growth Report?

-

What is the expected growth of the On-device AI Market between 2026 and 2030?

-

USD 150.98 billion, at a CAGR of 28.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Technology (7 nm, 10 nm, and 20 to 28 nm), Application (Smartphones, Wearables, and Smart speakers) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing demand for enhanced data privacy and security, Power consumption and thermal management constraints

-

-

Who are the major players in the On-device AI Market?

-

Advanced Micro Devices Inc., Ambarella Inc., Apple Inc., Google LLC, Hailo Technologies Ltd., Huawei Technologies Co. Ltd., Infineon Technologies AG, Intel Corp., MediaTek Inc., Microchip Technology Inc., Mythic Inc., NVIDIA Corp., NXP Semiconductors NV, Qualcomm Inc., Renesas Electronics Corp., Samsung Electronics Co. Ltd., SiMa Technologies Inc., Sony Semiconductor Solutions, STMicroelectronics NV and Texas Instruments Inc.

-

Market Research Insights

- Market dynamics are shaped by the strategic shift toward hybrid AI architectures, which balance local processing with cloud capabilities to optimize performance and efficiency. This approach has demonstrated an ability to reduce server-side operational costs by up to 30% while enhancing application responsiveness.

- The drive for low latency processing is particularly critical in autonomous systems, where a delay reduction of just 50 milliseconds can be the difference in operational safety. Concurrently, the adoption of privacy-preserving AI is a key differentiator, with systems that process data locally seeing a 40% higher trust rating in consumer surveys.

- As edge intelligence becomes more sophisticated, the focus on secure, efficient AI model deployment and local inference continues to intensify, pushing the boundaries of what is possible on connected devices.

We can help! Our analysts can customize this on-device ai market research report to meet your requirements.

RIA -

RIA -