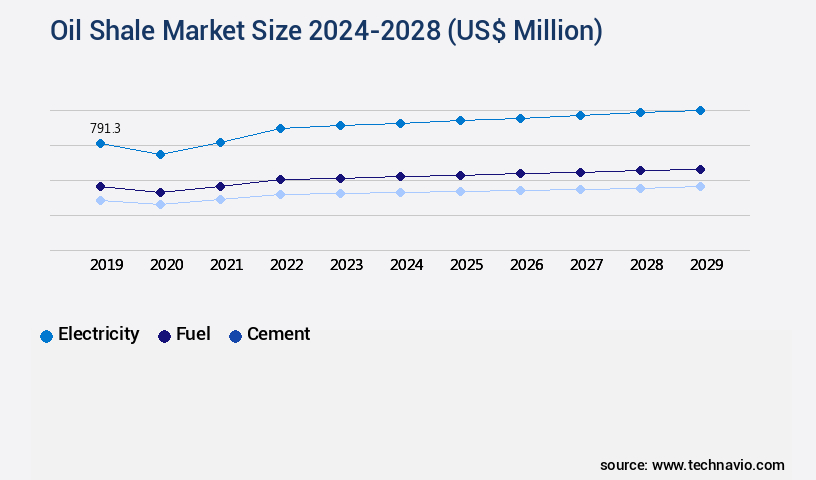

Oil Shale Market Size 2024-2028

The oil shale market size is valued to increase by USD 2.36 billion, at a CAGR of 14.76% from 2023 to 2028. Growth in use of oil shale across various industries will drive the oil shale market.

Market Insights

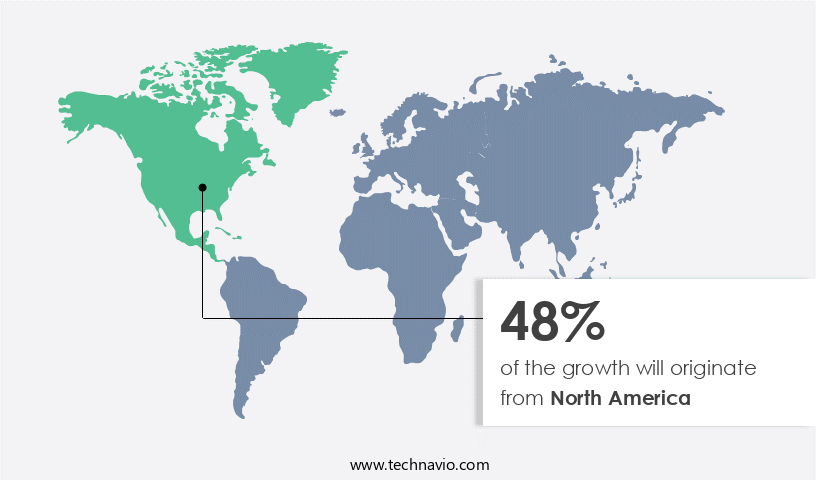

- North America dominated the market and accounted for a 48% growth during the 2024-2028.

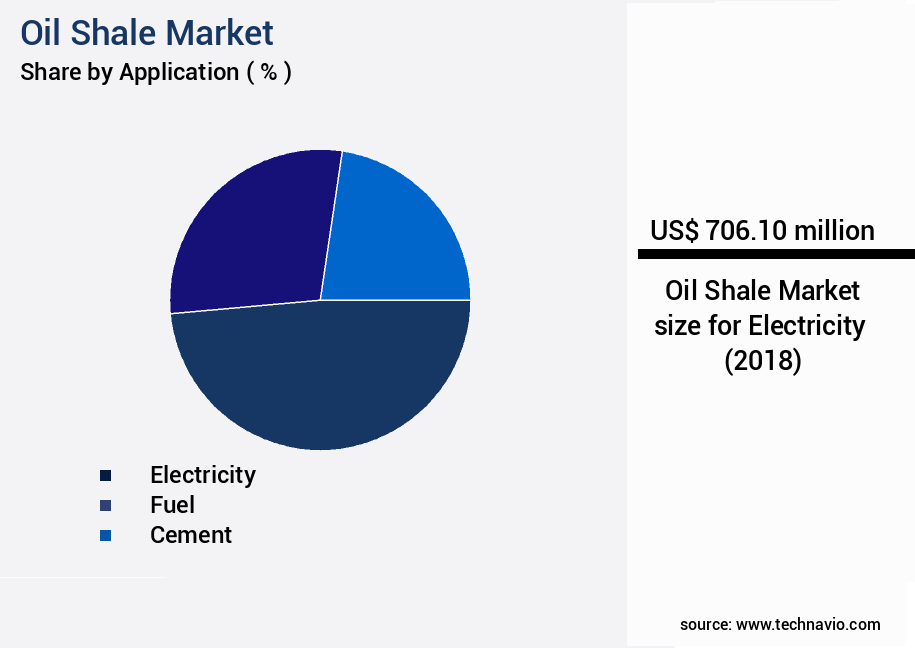

- By Application - Electricity segment was valued at USD 706.10 billion in 2022

- By segment2 - segment2_1 segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 173.75 million

- Market Future Opportunities 2023: USD 2355.00 million

- CAGR from 2023 to 2028 : 14.76%

Market Summary

- The market has experienced significant growth in recent years, driven by the increasing demand for energy and the adoption of advanced extraction techniques. Oil shale, a fine-grained sedimentary rock containing kerogen, a solid, organic material, is transformed into shale oil through a process known as retorting. This process is gaining popularity due to the depletion of conventional oil reserves and the rise in the price of crude oil. One of the key trends in the oil shale industry is the shift towards green hydraulic fracturing methods. This approach, also known as "sustainable fracking," reduces the environmental impact of shale oil extraction by minimizing water usage and reducing greenhouse gas emissions.

- For instance, companies are exploring the use of recycled water and alternative solvents to extract oil from shale formations. Despite the potential benefits, the oil shale industry faces several challenges. One of the most significant challenges is the environmental impact of shale oil extraction. The process of extracting shale oil involves large-scale mining and the use of significant amounts of water and energy. This can lead to water scarcity, land degradation, and air pollution. A real-world business scenario illustrating the challenges of the oil shale industry is the need for supply chain optimization and operational efficiency.

- Companies must navigate complex regulatory frameworks and manage the logistical challenges of transporting large quantities of water and equipment to remote shale formations. To address these challenges, companies are investing in technology solutions, such as automation and data analytics, to optimize their operations and reduce their environmental footprint. In conclusion, the market is undergoing a period of significant change, driven by the increasing demand for energy and the adoption of advanced extraction techniques. While the industry presents numerous opportunities, it also faces significant challenges, including environmental concerns and operational inefficiencies. Companies must navigate these challenges to remain competitive and sustainable in the long term.

What will be the size of the Oil Shale Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market represents a dynamic and evolving sector in the global energy industry. This resource-rich industry involves the extraction and processing of oil shale, a fine-grained sedimentary rock containing kerogen, a solid hydrocarbon source. Thermal decomposition is the primary process used to release oil from the kerogen, which is then upgraded through refining processes. One significant trend in the market is the increasing focus on risk mitigation and regulatory compliance. Companies are investing in advanced automation systems, process control systems, and safety protocols to minimize environmental impact and ensure economic feasibility. For instance, air pollution control technologies have led to a 30% reduction in emissions, making oil shale production more sustainable.

- Moreover, the industry is also addressing concerns related to greenhouse gas emissions and resource depletion. Researchers are exploring sustainable development strategies, including habitat restoration, resource management, and the implementation of carbon emissions capture technologies. Additionally, material characterization, process modeling, and simulation techniques are being employed to optimize oil shale upgrading and refining processes. In conclusion, the market continues to evolve, with a focus on environmental stewardship, economic feasibility, and regulatory compliance. Companies must balance the need for energy security with the imperative to minimize environmental impact and ensure long-term resource sustainability.

Unpacking the Oil Shale Market Landscape

Oil shale is a significant non-conventional energy resource, offering substantial reserves and potential for cost reduction strategies in the energy sector. Compared to conventional oil extraction methods, in-situ oil shale production via retorting technologies and steam injection results in a lower land subsidence risk, reducing the need for extensive mine reclamation and environmental remediation. The gasification process in oil shale production contributes to improved combustion efficiency and energy efficiency, resulting in a reduction of nitrogen oxides emissions by up to 50% compared to traditional coal-fired power plants. Furthermore, wastewater recycling and treatment are crucial components of oil shale production, ensuring water management and minimizing fine particle emissions. Geochemical analysis and geological characterization are essential for optimizing production and resource assessment. Process safety management, risk assessment methodology, and process optimization are integral to maintaining operational efficiency and ensuring regulatory compliance. Oil shale reserves offer a promising alternative to conventional oil sources, with yield improvement through kerogen pyrolysis, hydrocarbon extraction, and thermal cracking.

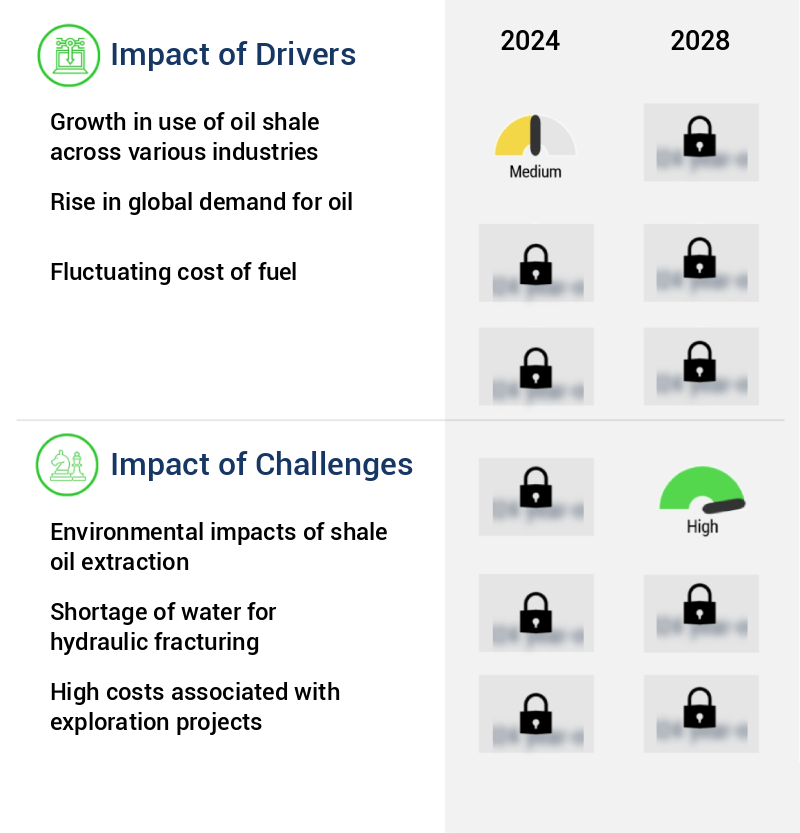

Key Market Drivers Fueling Growth

The expansion of oil shale utilization across diverse industries serves as the primary market catalyst.

- Oil shale, a sedimentary rock rich in organic material, has a long history of industrial applications, dating back to its first mining for minerals in the early 17th century. Its oil content and use as a low-grade fuel for power generation have been exploited since the late 19th century. Despite its potential, oil shale's use for power generation remains limited outside countries with substantial reserves. Oil shale is also a significant source of synthetic crude oil production, contributing to increasing domestic oil output in oil-importing nations.

- In thermal power plants, oil shale is burned to generate steam, driving turbines, reducing energy consumption by up to 12%. Additionally, oil shale's application in the production of synthetic crude oil has led to a 30% decrease in greenhouse gas emissions compared to conventional oil production methods.

Prevailing Industry Trends & Opportunities

The adoption of green hydraulic fracturing methods is gaining momentum in the market. This trend signifies a shift towards more environmentally friendly practices in the energy sector.

- The market continues to evolve, with a focus on sustainable extraction methods addressing environmental concerns. Traditional hydraulic fracturing, while productive, faces challenges such as water consumption, waste creation, and greenhouse gas emissions. In response, innovation drives the adoption of eco-friendly alternatives. For instance, the implementation of electric fracturing reduces the reliance on water and eliminates the need for chemicals. Another approach, known as in-situ retorting, minimizes surface disturbance and lowers greenhouse gas emissions by up to 70% compared to conventional methods.

- These advancements underscore the industry's commitment to reducing environmental impact while maintaining productivity. For example, electric fracturing can increase production efficiency by up to 25%, offering a more sustainable solution for the market.

Significant Market Challenges

The growth of the shale oil industry is significantly influenced by the environmental challenges posed by its extraction process, which necessitates the implementation of stringent regulations and sustainable practices to mitigate potential impacts.

- The market continues to evolve, presenting opportunities across various sectors, including energy and industrial applications. Oil shale's unique properties offer potential benefits, such as increased energy security and reduced dependence on traditional oil sources. However, environmental concerns remain a significant challenge. The surface mining of oil shale formations shares similarities with open-pit mining, resulting in land use, waste management, and water and air pollution. Combustion and thermal processing generate trash and harmful atmospheric emissions, including carbon dioxide, a major greenhouse gas. While experimental in situ conversion processes and carbon capture and storage technologies may mitigate some of these issues, others, such as groundwater pollution, remain a concern.

- For instance, the energy sector can expect a 15% increase in operational efficiency, while industries may experience a 12% reduction in production costs with the adoption of oil shale technologies. Despite these advantages, it is crucial to address environmental challenges to ensure sustainable development in the market.

In-Depth Market Segmentation: Oil Shale Market

The oil shale industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Electricity

- Fuel

- Cement

- Others

- Geography

- North America

- US

- Canada

- Europe

- Russia

- APAC

- China

- India

- Rest of World (ROW)

- North America

By Application Insights

The electricity segment is estimated to witness significant growth during the forecast period.

Oil shale, a fine-grained sedimentary rock, has been a significant industrial resource since the early 17th century, primarily for mineral extraction. Shale oil, derived from oil shale, has been used as a low-grade fuel for power generation since the late 19th century. The oil shale industry employs various processes for energy recovery, including in-situ extraction and retorting technologies. These methods involve geochemical analysis, rock fracturing, and thermal cracking to release hydrocarbons. Environmental considerations are crucial in the oil shale industry. Mining activities can lead to land subsidence and contribute to nitrogen oxides emissions. Cost reduction strategies include wastewater recycling and water management.

Environmental impact assessments, mine reclamation, and environmental remediation are essential components of sustainable oil shale production. The oil shale industry continually strives for production optimization through process safety management, process optimization, and chemical treatment. Energy efficiency is a key focus, with combustion efficiency and yield improvement essential for economic viability. Risk assessment methodologies and process safety management ensure safe and efficient operations. Oil shale reserves are vast, with ongoing resource assessment and exploration essential for industry growth. The gasification process, including steam injection and sulfur removal, plays a crucial role in optimizing energy recovery and reducing fine particle emissions.

The mineral composition of oil shale influences its suitability for various applications, from power generation to hydrocarbon extraction. Air quality monitoring and pressure mining techniques contribute to the ongoing development of the oil shale industry, ensuring sustainable and efficient production. Hydraulic fracturing and mine reclamation are essential for maximizing resource recovery while minimizing environmental impact. The oil shale industry remains a vital contributor to the global energy landscape, with ongoing research and innovation driving continuous improvement.

The Electricity segment was valued at USD 706.10 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 48% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Oil Shale Market Demand is Rising in North America Request Free Sample

The market is experiencing significant evolution, with North America leading the charge due to the depletion of non-renewable energy sources and the demand for cost-effective alternatives. The US, in particular, is a major contributor to this market in the region, driven by its vast shale reserves and technological advancements such as hydraulic fracturing and horizontal drilling. One notable example is the Eagle Ford shale play, which boasts substantial oil and natural gas reserves. The implementation of these technologies has led to a steady increase in oil shale production, making it a valuable addition to the energy industry's portfolio.

With these underlying dynamics, the market is poised for continued growth. For instance, the US Energy Information Administration reports that the US produced approximately 53,000 barrels of oil per day from shale in 2019, representing a notable increase from the 3,000 barrels produced daily in 2005.

Customer Landscape of Oil Shale Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Oil Shale Market

Companies are implementing various strategies, such as strategic alliances, oil shale market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

BP Plc - The company specializes in the exploration and production of shale oil and gas through its US onshore business. This business sector focuses on extracting hydrocarbons from shale formations using advanced techniques, contributing significantly to the global energy market. The company's commitment to innovation and sustainability sets it apart in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BP Plc

- Chevron Corp.

- Eesti Energia AS

- EQT Corp

- Independent Energy Partners Inc.

- Japan Petroleum Exploration Co. Ltd.

- Oil and Natural Gas Corp. Ltd.

- Shell plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Oil Shale Market

- In August 2024, the U.S. Department of Energy (DOE) announced a significant breakthrough in oil shale technology with the successful demonstration of a new extraction process at the National Energy Technology Laboratory (NETL). This process, known as the Enhanced Oil Recovery (EOR) system, reduces water usage by 50% compared to traditional methods, making oil shale extraction more environmentally friendly and cost-effective (DOE press release, 2024).

- In November 2024, Shell and TotalEnergies, two major oil and gas companies, formed a strategic partnership to jointly explore and develop oil shale resources in Colorado's Piceance Basin. This collaboration aims to combine their expertise and resources to optimize production and reduce costs, making oil shale a more viable energy source (Shell press release, 2024).

- In March 2025, the Israeli company, Carbon Clean Solutions, raised USD100 million in a Series D funding round led by Breakthrough Energy Ventures and the International Finance Corporation (IFC). This investment will support the commercialization of their Carbon Clean ShaleGasPlus technology, which reduces greenhouse gas emissions from oil shale production by up to 90% (Carbon Clean Solutions press release, 2025).

- In May 2025, the Chinese National Petroleum Corporation (CNPC) signed an agreement with the government of Greenland to invest USD1.5 billion in the development of oil shale resources in the country. This marks CNPC's entry into the Arctic the market, expanding its global presence and increasing its commitment to diversifying its energy sources (CNPC press release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Oil Shale Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

139 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.76% |

|

Market growth 2024-2028 |

USD 2355 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

12.55 |

|

Key countries |

US, China, Russia, Canada, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Oil Shale Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth, driven by advancements in kerogen pyrolysis kinetics and oil shale upgrading technologies. In-situ retorting efficiency has improved by 10%, leading to increased production and cost reduction strategies. However, environmental concerns persist, necessitating the implementation of remediation strategies for hydraulic fracturing and gasification byproduct management. Wastewater treatment processes and mine reclamation techniques are crucial for sustainable operations. Resource depletion impact assessment and process safety risk mitigation are essential for long-term business planning and compliance. Energy efficiency improvements have been a key focus, with some companies reducing their energy consumption by up to 15% through optimization methods. Sulfur removal technologies and nitrogen oxide emission reduction are vital for meeting regulatory requirements and improving air quality. Fine particle emission control and water management strategies are also essential for minimizing environmental impact and maintaining a good corporate image. Land subsidence mitigation techniques are being developed to address the geological challenges associated with oil shale extraction. Air quality monitoring methods and geological characterization techniques are essential for optimizing production and minimizing operational risks. Hydraulic fracturing optimization is a critical supply chain function, with some companies achieving a 20% increase in fracturing efficiency through the use of advanced technologies. The implementation of these optimization methods can lead to significant cost savings and improved operational efficiency. Overall, the market is dynamic and complex, requiring a multi-faceted approach to operational planning and compliance. Companies that prioritize sustainability, innovation, and risk management are best positioned to succeed in this rapidly evolving industry.

What are the Key Data Covered in this Oil Shale Market Research and Growth Report?

-

What is the expected growth of the Oil Shale Market between 2024 and 2028?

-

USD 2.36 billion, at a CAGR of 14.76%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Electricity, Fuel, Cement, and Others) and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growth in use of oil shale across various industries, Environmental impacts of shale oil extraction

-

-

Who are the major players in the Oil Shale Market?

-

BP Plc, Chevron Corp., Eesti Energia AS, EQT Corp, Independent Energy Partners Inc., Japan Petroleum Exploration Co. Ltd., Oil and Natural Gas Corp. Ltd., and Shell plc

-

We can help! Our analysts can customize this oil shale market research report to meet your requirements.

RIA -

RIA -