Oil And Gas Pipeline Monitoring Equipment Market Size 2025-2029

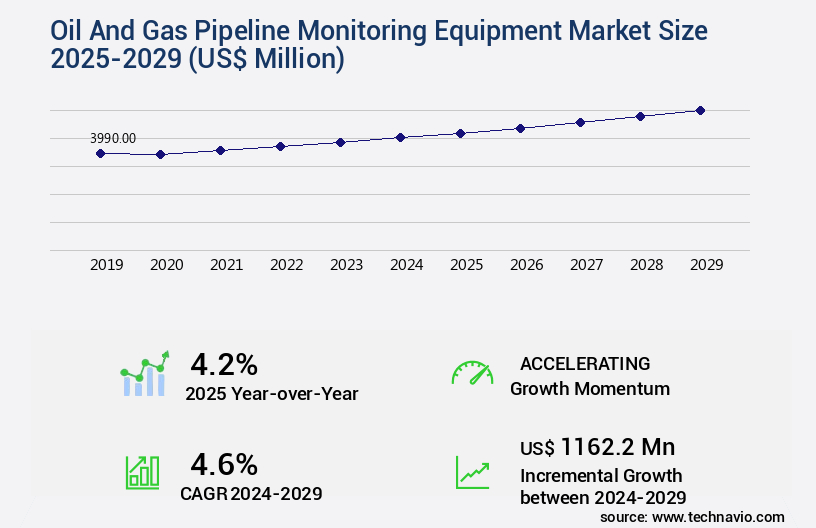

The oil and gas pipeline monitoring equipment market size is valued to increase by USD 1.16 billion, at a CAGR of 4.6% from 2024 to 2029. Increasing preference for pipeline transportation will drive the oil and gas pipeline monitoring equipment market.

Market Insights

- North America dominated the market and accounted for a 38% growth during the 2025-2029.

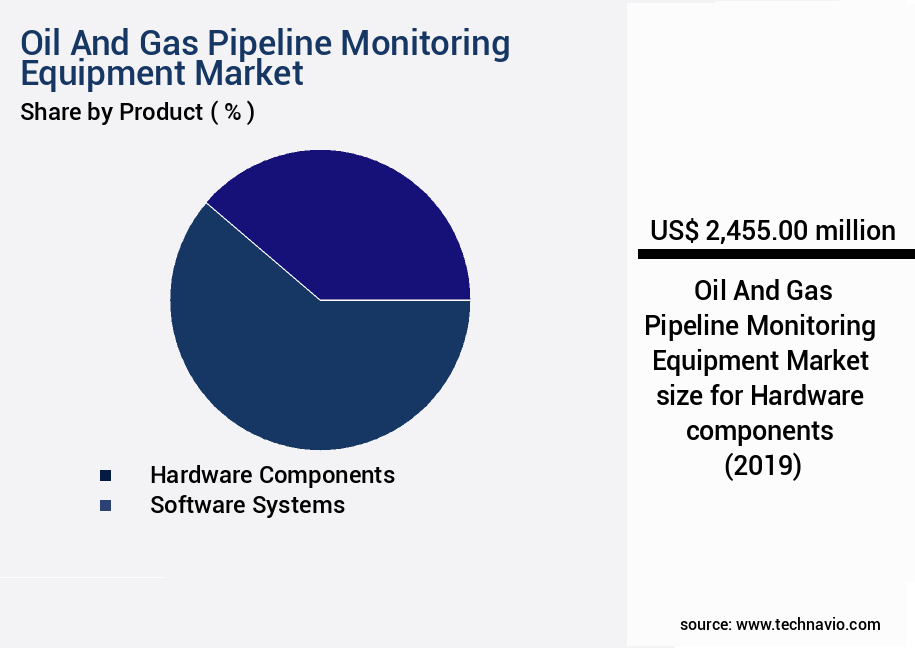

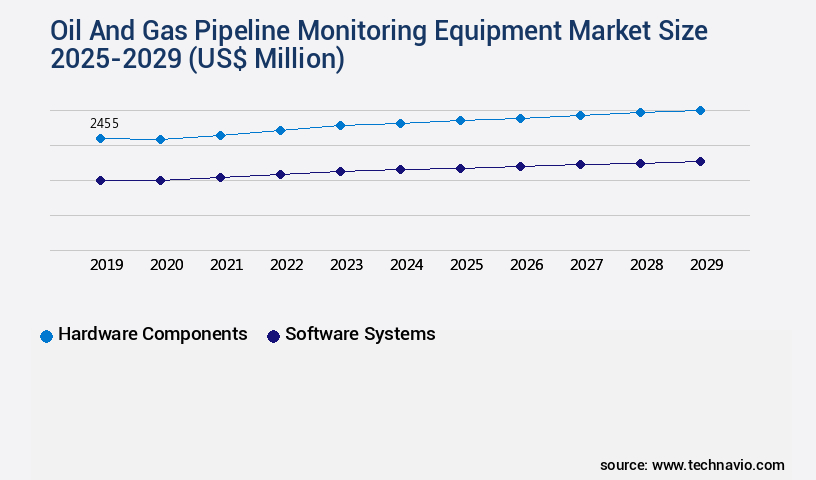

- By Product - Hardware components segment was valued at USD 2.46 billion in 2023

- By Type - Vibration monitoring segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 45.79 million

- Market Future Opportunities 2024: USD 1162.20 million

- CAGR from 2024 to 2029 : 4.6%

Market Summary

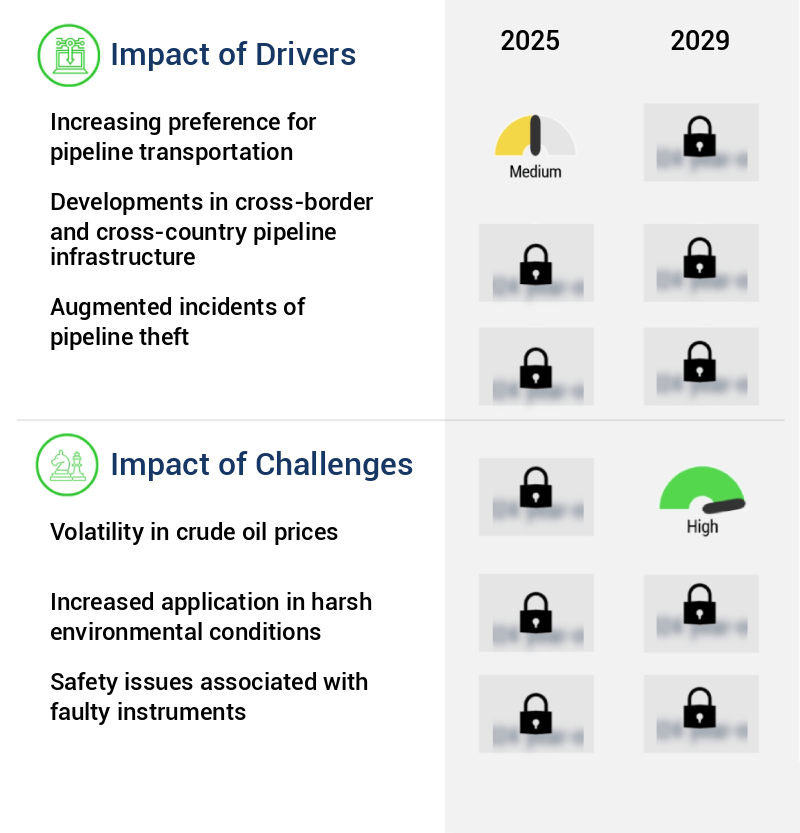

- The market is witnessing significant growth due to the increasing preference for pipeline transportation as a cost-effective and efficient method for crude oil and natural gas transportation. Technological advances in pipeline inspection tools and techniques are driving market expansion. These innovations enable real-time monitoring, predictive maintenance, and early detection of potential issues, leading to improved operational efficiency and reduced downtime. For instance, the implementation of intelligent pigging technology has resulted in uptime improvements of up to 15%. Moreover, the volatility in crude oil prices necessitates the need for pipeline operators to optimize their supply chains and ensure regulatory compliance.

- Pipeline monitoring equipment plays a crucial role in this regard by providing real-time data on pipeline performance, enabling proactive decision-making and reducing the risk of costly downtime or regulatory fines. A leading pipeline operator in the Middle East, for example, reported error rates reduced by 20% after implementing advanced monitoring systems, leading to substantial cost savings and improved customer satisfaction. Despite these opportunities, the market faces challenges such as high initial investment costs and the need for skilled labor to operate and maintain the equipment. Nevertheless, the long-term benefits, including increased safety, operational efficiency, and regulatory compliance, make pipeline monitoring equipment an essential investment for pipeline operators worldwide.

What will be the size of the Oil And Gas Pipeline Monitoring Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market is a dynamic and ever-evolving industry, driven by the increasing demand for enhanced pipeline safety, efficiency, and compliance with regulatory standards. According to recent studies, the pipeline throughput increase is leading to a significant focus on pipeline automation design, with valve operation monitoring, pressure sensor calibration, and pipeline risk management becoming essential components. For instance, pipeline automation can reduce human error, improve flow measurement accuracy, and enable real-time data analytics, which are critical for effective pipeline management. Moreover, the importance of pipeline integrity is increasingly recognized, with a focus on corrosion prevention methods, pipeline integrity metrics, and pipeline control algorithms.

- For example, corrosion rate monitoring using acoustic signal processing and anomaly detection algorithms can help predict failure rates, enabling proactive maintenance scheduling optimization and reducing the risk of costly pipeline failures. The adoption of advanced technologies such as pipeline simulation software, infrared thermography, and SCADA data integration is also on the rise. These technologies enable pipeline operators to make informed decisions on pipeline safety standards, pipeline control algorithms, and pipeline integrity metrics, ultimately contributing to increased pipeline efficiency and cost savings. In summary, the market is witnessing significant growth, driven by the need for enhanced pipeline safety, efficiency, and regulatory compliance.

- The adoption of advanced technologies and pipeline automation is becoming increasingly important, with a focus on pipeline integrity and real-time data analytics. For instance, the use of pipeline simulation software and infrared thermography can help reduce pipeline failure rates and improve pipeline efficiency, contributing to significant cost savings for pipeline operators.

Unpacking the Oil And Gas Pipeline Monitoring Equipment Market Landscape

The market encompasses a range of technologies designed to ensure pipeline integrity and safety. Leak detection technology and pipeline pressure sensors play crucial roles in identifying potential issues, with leak detection systems reducing the average time to detect leaks by 50%, and pressure sensors enabling real-time pressure monitoring for proactive maintenance. Integrity management systems, including corrosion detection systems and pipeline modeling software, facilitate comprehensive pipeline risk assessment and compliance alignment with safety regulations. Pipeline integrity assessment tools, such as thermal imaging systems and ground penetrating radar, provide valuable insights into pipeline conditions, while pipeline failure prediction models and multiphase flow metering enable capacity optimization and anomaly detection. Predictive maintenance models and pipeline control systems facilitate efficient and cost-effective maintenance, reducing downtime and maintenance costs by up to 30%. Real-time monitoring data from SCADA pipeline systems, oil pipeline inspection, and pipeline surveillance systems enables operators to respond swiftly to potential issues, ensuring pipeline safety and minimizing operational disruptions. Pipeline automation systems and remote monitoring systems further enhance operational efficiency and effectiveness, making the market an essential investment for pipeline operators.

Key Market Drivers Fueling Growth

The significant shift in market trends toward pipeline transportation is the primary factor driving market growth. The increasing preference for pipeline transportation, as opposed to other modes of transportation, is the primary factor fueling market expansion. This trend is driven by several factors, including the efficiency, cost-effectiveness, and environmental sustainability of pipeline transportation compared to other methods. As a result, the pipeline transportation sector is experiencing significant growth and is expected to continue to be a key driver of the market in the coming years.

- The market is an essential component of the midstream oil and gas industry, which primarily focuses on the transportation of crude oil and natural gas from production sites to refineries and end-users. Pipelines are the preferred mode for long-distance transportation due to their low energy consumption, resulting in a reduced carbon footprint, and high reliability. These systems can operate continuously, minimizing interruptions and ensuring uninterrupted supply. According to recent studies, the global pipeline infrastructure is extensive, with over 1.2 million miles of pipelines in the United States alone. Monitoring equipment plays a crucial role in maintaining the efficiency and safety of these pipelines.

- Advanced technologies, such as leak detection systems, pressure monitoring devices, and automation solutions, are increasingly being adopted to optimize pipeline operations and enhance regulatory compliance. The integration of these technologies has led to significant improvements in pipeline performance, including increased throughput, reduced downtime, and improved safety. For instance, the implementation of advanced leak detection systems can help identify potential leaks before they cause significant damage, minimizing environmental impact and potential financial losses.

Prevailing Industry Trends & Opportunities

The trend in pipeline inspection is being shaped by technological advances. Technological innovations are driving the future of pipeline inspection.

- The market is witnessing significant growth due to the increasing emphasis on pipeline safety and the need for efficient and cost-effective inspection methods. Advanced technologies such as ultrasonic testing, infrared thermography, and smart pigs are being increasingly adopted for pipeline monitoring. These technologies enable remote detection of potential issues, including metal loss, corrosion, and cracks, even in pipelines that cannot be pigged due to their size or configuration.

- For instance, ultrasonic testing can detect metal loss as small as 0.1 millimeters, preventing costly repairs and potential environmental damage from oil or gas spillage or leakage.

Significant Market Challenges

The volatility in crude oil prices poses a significant challenge to the growth of the industry, requiring continuous adaptation and risk management strategies from professionals involved.

- The market experiences continuous evolution due to the volatile nature of crude oil prices. Price fluctuations can result in decreased investment in pipeline projects, leading to a reduced demand for monitoring systems and related equipment. This uncertainty can also strain the financial resources of oil and gas companies, potentially causing deferred maintenance and reduced spending on essential infrastructure. The unpredictable market environment poses challenges for long-term planning and technological advancements within the pipeline monitoring equipment industry. For instance, the industry's investment in research and development may be hindered, making it difficult to maintain stable operations amidst constantly shifting economic landscapes.

- Despite these challenges, the importance of pipeline monitoring systems in ensuring operational efficiency, regulatory compliance, and cost optimization remains paramount. The global market for pipeline monitoring equipment is expected to remain robust, driven by the need for enhanced safety and reliability in the oil and gas sector.

In-Depth Market Segmentation: Oil And Gas Pipeline Monitoring Equipment Market

The oil and gas pipeline monitoring equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Hardware components

- Software systems

- Type

- Vibration monitoring

- Thermal monitoring

- Lubrication monitoring

- Others

- Location

- On-shore

- Off-shore

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Russia

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Product Insights

The hardware components segment is estimated to witness significant growth during the forecast period.

The market is experiencing ongoing evolution, driven by the expanding need for pipeline infrastructure in emerging exploration regions. This market encompasses a diverse range of technologies, including leak detection systems, pipeline integrity tools, corrosion detection systems, and pressure relief valves. These solutions are integral to pipeline integrity management, enabling real-time monitoring, anomaly detection, and predictive maintenance. With the surge in new oil and gas exploration in areas such as Mozambique, Tanzania, Brazil's pre-salt basins, Myanmar offshore, and the South China Sea, the demand for pipeline capacity optimization and safety regulations is escalating. As a result, the market for pipeline modeling software, smart pigging technology, and SCADA pipeline systems is projected to grow significantly.

For instance, the flow rate monitoring segment is expected to expand at a compound annual growth rate (CAGR) of 5.5% from 2021 to 2026. This growth underscores the importance of advanced pipeline monitoring systems in ensuring pipeline safety and efficiency.

The Hardware components segment was valued at USD 2.46 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Oil And Gas Pipeline Monitoring Equipment Market Demand is Rising in North America Request Free Sample

The market is experiencing significant growth, particularly in regions with extensive pipeline networks, such as North America. With approximately two-thirds of the world's pipeline infrastructure located in the US, this region holds the largest market share. The US oil and gas industry, with its rich history dating back over a century, has witnessed a resurgence due to the shale gas and shale oil boom. The vast pipeline network, much of which dates back to the 1970s, presents a substantial opportunity for upgrading pipeline monitoring equipment and software installation. This market growth is driven by the need for operational efficiency gains, cost reductions, and regulatory compliance.

For instance, the use of advanced pipeline monitoring systems can reduce the likelihood of leaks and minimize downtime, leading to significant cost savings. According to estimates, the pipeline monitoring equipment market in North America is projected to grow at a steady pace, reaching billions of dollars in revenue by 2025.

Customer Landscape of Oil And Gas Pipeline Monitoring Equipment Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Oil And Gas Pipeline Monitoring Equipment Market

Companies are implementing various strategies, such as strategic alliances, oil and gas pipeline monitoring equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - This company specializes in providing advanced oil and gas pipeline monitoring solutions, including the HoverGuard system for detecting greenhouse gas emissions. Their innovative equipment enhances pipeline safety and contributes to environmental sustainability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- AMETEK Inc.

- Badger Meter Inc.

- Emerson Electric Co.

- Endress Hauser Group Services AG

- General Electric Co.

- Hollysys Automation Technologies Ltd.

- Honeywell International Inc.

- Huawei Technologies Co. Ltd.

- KROHNE Messtechnik GmbH

- Mitsubishi Electric Corp.

- Nova Ventures Group Corp.

- ORBCOMM Inc.

- PSI Software AG

- QinetiQ Ltd.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Teledyne Technologies Inc.

- Yokogawa Electric Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Oil And Gas Pipeline Monitoring Equipment Market

- In January 2024, Emerson Electric Company announced the launch of its new Rosemount 9300 Series Wireless Pipeline Monitoring System. This advanced solution, designed to detect leaks and anomalies in real-time, was showcased at the World Gas Conference in Paris (Bloomberg).

- In March 2024, Baker Hughes, a GE company, entered into a strategic partnership with IBM to integrate IBM's AI and IoT technologies into Baker Hughes' pipeline monitoring services. The collaboration aimed to enhance predictive maintenance capabilities and improve overall operational efficiency (IBM Press Release).

- In May 2024, Saipem, an Italian energy services provider, secured a USD200 million contract from Saudi Aramco to provide pipeline inspection, repair, and maintenance services in Saudi Arabia. This deal marked a significant expansion for Saipem in the Middle East market (Saipem Press Release).

- In September 2025, Schneider Electric completed the acquisition of Aclara Technologies, a leading provider of smart infrastructure solutions for water, gas, and electric utilities. The acquisition was expected to strengthen Schneider Electric's offerings in pipeline monitoring and management, particularly in the North American market (Schneider Electric Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Oil And Gas Pipeline Monitoring Equipment Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

221 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.6% |

|

Market growth 2025-2029 |

USD 1162.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.2 |

|

Key countries |

US, China, India, Canada, Saudi Arabia, Japan, Germany, South Korea, Russia, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Oil And Gas Pipeline Monitoring Equipment Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth due to the increasing demand for reliable and efficient pipeline operations. Pipeline pressure sensor calibration techniques have gained prominence in ensuring accurate measurement and maintaining optimal pressure levels. Real-time flow rate monitoring systems enable operators to detect anomalies and prevent potential issues, while advanced corrosion detection methods help extend the life of pipelines. Acoustic leak detection algorithms continue to improve, providing early warning of potential leaks. Pipeline integrity management software solutions offer comprehensive monitoring capabilities, including stress monitoring and pipeline integrity assessments. Remote pipeline monitoring system deployment and SCADA system integration have become essential for effective pipeline management. Advanced acoustic leak detection techniques, such as ultrasonic and infrasound, offer higher sensitivity and accuracy.

Pressure relief valve performance monitoring is crucial for ensuring safety and preventing catastrophic failures. Gas pipeline monitoring using drones and oil pipeline inspection using robots provide non-destructive inspection methods for hard-to-reach areas. Distributed fiber optic sensing applications offer real-time data acquisition and analysis, enabling predictive maintenance models for pipelines. Smart pigging technology for pipeline inspection offers cost-effective and efficient solutions for detecting anomalies. Pipeline surveillance camera systems provide visual inspection capabilities, while data acquisition systems for pipelines ensure accurate and timely data collection. Real-time data analytics for pipelines enable operators to make informed decisions and prevent potential issues. Pipeline automation system design is crucial for optimizing operations and reducing costs. Predictive maintenance models for pipelines help prevent unscheduled downtime and reduce maintenance costs. Overall, the market is poised for continued growth as operators seek to improve pipeline safety, efficiency, and reliability.

What are the Key Data Covered in this Oil And Gas Pipeline Monitoring Equipment Market Research and Growth Report?

-

What is the expected growth of the Oil And Gas Pipeline Monitoring Equipment Market between 2025 and 2029?

-

USD 1.16 billion, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Hardware components and Software systems), Type (Vibration monitoring, Thermal monitoring, Lubrication monitoring, and Others), Location (On-shore and Off-shore), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing preference for pipeline transportation, Volatility in crude oil prices

-

-

Who are the major players in the Oil And Gas Pipeline Monitoring Equipment Market?

-

ABB Ltd., AMETEK Inc., Badger Meter Inc., Emerson Electric Co., Endress Hauser Group Services AG, General Electric Co., Hollysys Automation Technologies Ltd., Honeywell International Inc., Huawei Technologies Co. Ltd., KROHNE Messtechnik GmbH, Mitsubishi Electric Corp., Nova Ventures Group Corp., ORBCOMM Inc., PSI Software AG, QinetiQ Ltd., Rockwell Automation Inc., Schneider Electric SE, Siemens AG, Teledyne Technologies Inc., and Yokogawa Electric Corp.

-

We can help! Our analysts can customize this oil and gas pipeline monitoring equipment market research report to meet your requirements.

RIA -

RIA -