Testing Inspection and Certification Market in North America Size 2024-2028

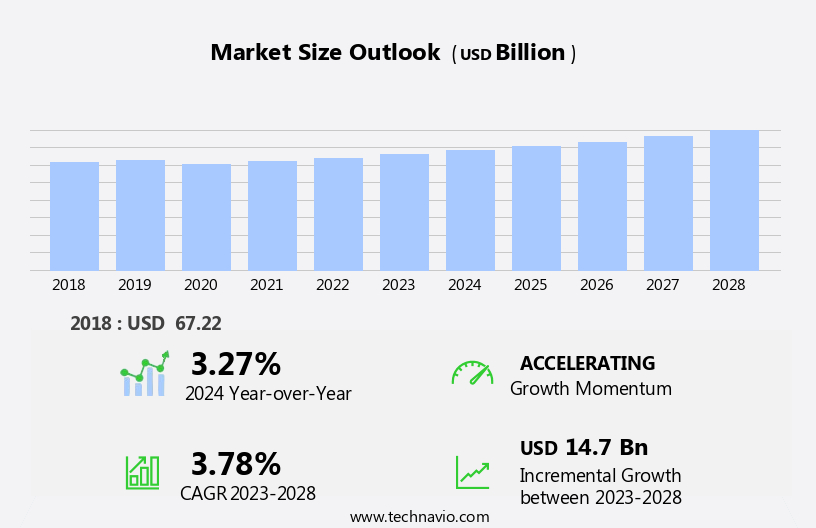

The testing inspection and certification market in North America size is forecast to increase by USD 14.7 billion, at a CAGR of 3.78% between 2023 and 2028.

- The market is witnessing significant growth, driven by the increasing adoption of remote inspections and audits. This shift towards digital solutions enables businesses to streamline their operations, reduce costs, and ensure continuity during disruptions. Another key trend is the rise in strategic mergers and acquisitions (M&A) for testing inspection and certification services, as companies seek to expand their offerings and enhance their market presence. However, the market faces challenges related to data security and confidentiality of testing inspection and certification.

- With the growing digitization of processes, ensuring the protection of sensitive information is paramount for market participants. Companies must invest in robust cybersecurity measures and adhere to stringent regulatory requirements to mitigate these risks and maintain customer trust. To capitalize on opportunities and navigate challenges effectively, market players must stay informed of the latest industry trends and best practices.

What will be the Size of the Testing Inspection and Certification Market in North America during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the diverse needs of various sectors and the ever-changing regulatory landscape. Entities offering services such as third-party certification, compliance testing, process certification, chemical testing, inspection services, environmental testing, manufacturing process analysis, data analysis, quality assurance, and inspection agencies play integral roles in ensuring adherence to industry and regulatory standards. These entities provide crucial services, including material testing, regulatory compliance assessment, performance testing, failure analysis, system certification, and personnel certification. They employ advanced testing equipment and techniques, such as destructive testing, non-destructive testing (NDT), safety testing, electrical testing, and mechanical testing, to deliver accurate and reliable results.

The market's continuous dynamism is reflected in the ongoing development of new testing methodologies and technologies, as well as the expansion of services to address emerging industry trends. For instance, risk assessment and root cause analysis have gained increased importance in the supply chain, with testing laboratories offering these services to help clients mitigate risks and improve product quality. ISO standards and ASTM standards serve as essential guidelines for various industries, ensuring consistent quality and safety. Certification bodies and inspection agencies play a vital role in granting certifications based on these standards, providing clients with a recognized mark of excellence and compliance.

How is this Testing Inspection and Certification in North America Industry segmented?

The testing inspection and certification in North America industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Service

- Testing

- Inspection

- Certification

- Source

- In-house

- Outsourced

- End-User

- Manufacturing

- Construction

- Healthcare

- Food and Beverage

- Automotive

- Application

- Product Testing

- Quality Assurance

- Compliance Testing

- Environmental Testing

- Geography

- North America

- US

- Canada

- Mexico

- North America

By Service Insights

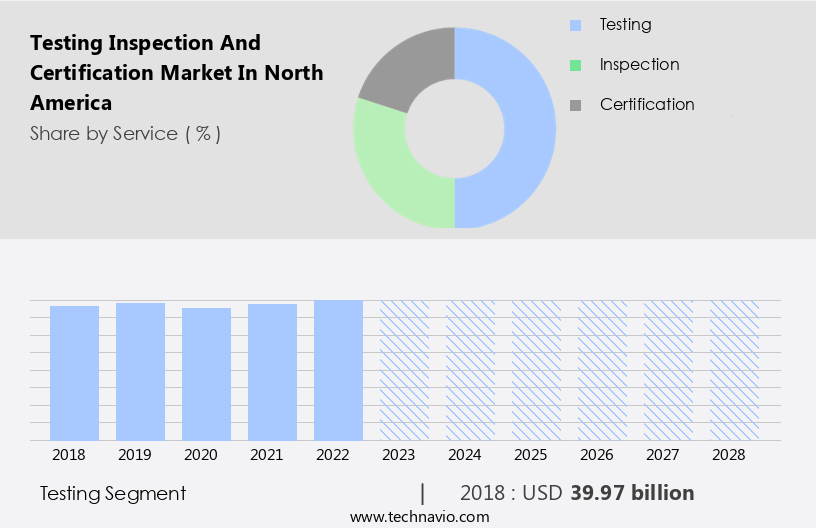

The testing segment is estimated to witness significant growth during the forecast period.

In North America, industries including healthcare, pharmaceuticals, automotive, aerospace, consumer goods, and environmental protection adhere to stringent regulations and standards. Compliance with these rules necessitates companies to engage in various testing services. These offerings help businesses ensure product safety, quality, environmental impact, and public health conformity. Prioritizing product reliability is essential for maintaining customer satisfaction, brand reputation, and market competitiveness. Testing services play a pivotal role in quality assurance, identifying defects, verifying performance, and maintaining consistency in manufacturing processes and product characteristics. By addressing potential issues early in the product development lifecycle, companies can mitigate risks associated with product failures, safety hazards, regulatory non-compliance, and liability claims.

Material testing, including destructive and non-destructive methods, is crucial for understanding product characteristics and identifying weaknesses. Performance testing evaluates how products function under various conditions, while failure analysis helps determine the root cause of product malfunctions. System certification ensures that integrated systems meet specifications, while third-party certification provides external validation of compliance. Regulations also mandate process certification, chemical testing, inspection services, environmental testing, and data analysis. Quality control measures include personnel certification, inspection agencies, inspection equipment, and first-party certification. Laboratory services, product testing, and risk assessment are essential for ensuring product safety and performance. ISO standards and safety testing are crucial in various industries, with electrical testing and product certification being particularly important for electronics and electrical equipment.

Certification bodies and report generation are integral parts of the testing services ecosystem, providing valuable documentation for regulatory compliance and stakeholder communication. Testing equipment and certification services are essential for maintaining the integrity of testing processes and ensuring accurate results. Overall, testing services play a vital role in helping businesses navigate the complex regulatory landscape and maintain a competitive edge in their respective industries.

The Testing segment was valued at USD 39.97 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

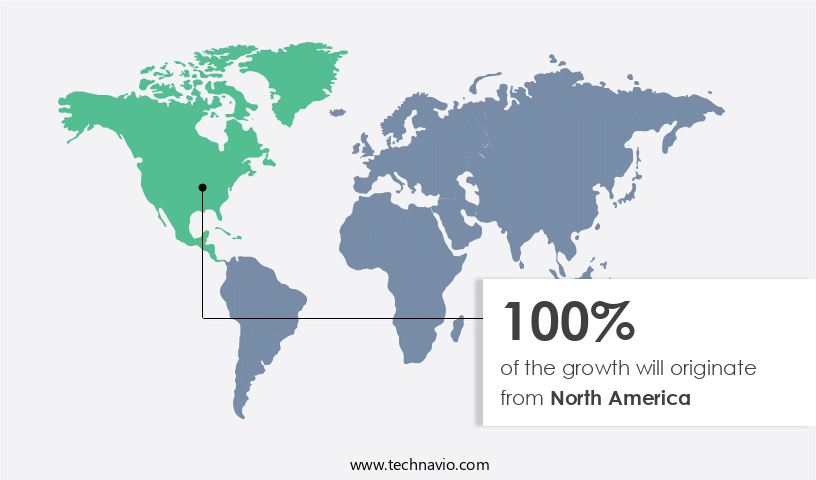

North America is estimated to contribute 100% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the dynamic US market, adherence to stringent regulatory requirements is a priority across various sectors, including food safety, environmental protection, healthcare, and consumer products. This necessitates rigorous testing and certification processes to ensure compliance. The technological landscape is evolving rapidly, with new products and services emerging in sectors like IoT devices, electric vehicles, renewable energy systems, and advanced medical devices. These innovations necessitate testing and certification to meet safety, quality, and performance standards. The US, as a major player in global trade, relies on testing, inspection, and certification services to facilitate cross-border commerce and comply with international regulations.

Material testing, destructive and performance testing, failure analysis, system certification, third-party certification, compliance testing, process certification, chemical testing, inspection services, environmental testing, data analysis, quality assurance, inspection agencies, personnel certification, inspection equipment, first-party certification, quality control, laboratory services, product testing, root cause analysis, testing laboratories, risk assessment, mechanical testing, and non-destructive testing (NDT) are integral to this market. ISO standards, safety testing, electrical testing, product certification, and certification bodies play crucial roles in generating reports and providing certification services. The testing equipment and services industry continue to innovate, ensuring the market remains harmonious and immersive, emphasizing continuous improvement and risk mitigation.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The projects growth, driven by TIC market trends 2024-2028 in North America. B2B TIC service solutions leverage smart testing technologies for accuracy. TIC North America growth opportunities 2025 include TIC for food safety and TIC for manufacturing, ensuring compliance. TIC management software optimizes operations, while TIC market competitive analysis highlights key providers. Sustainable TIC practices align with eco-friendly certification trends. TIC regulations 2024-2028 shapes TIC demand in North America 2025. Automated TIC testing solutions and premium TIC market insights boost demand. TIC for automotive industry and customized TIC services target niches. TIC market challenges and solutions address regulatory complexity, with direct procurement strategies for TIC and TIC pricing strategy optimization enhancing profitability. Data-driven TIC market analytics and digital TIC trends drive innovation.

What are the key market drivers leading to the rise in the adoption of Testing Inspection and Certification in North America Industry?

- The increasing implementation of remote inspections and audits is the primary catalyst fueling market growth. This shift towards digital processes is driven by the benefits they offer, such as increased efficiency, cost savings, and enhanced safety measures. As businesses continue to prioritize these advantages, the adoption of remote inspections and audits is expected to expand significantly.

- The Testing, Inspection, and Certification (TIC) market in North America is experiencing significant growth due to the increasing emphasis on regulatory compliance and industry standards. ASTM standards and other industry regulations drive the demand for material testing, performance testing, destructive testing, and failure analysis services. Second-party certification is also gaining popularity as a means to ensure quality and trust in supply chains. The COVID-19 pandemic has accelerated the adoption of remote inspections and audits, enabling organizations to maintain business continuity while adhering to social distancing guidelines and travel restrictions. These methods offer cost and time savings compared to traditional on-site visits, as they eliminate the need for travel, accommodation, and logistical arrangements.

- Furthermore, remote testing services enable faster turnaround times, allowing for more efficient data collection and reporting. System certification is another crucial aspect of the TIC market, ensuring that complex systems meet performance and safety requirements. Testing and certification providers offer a range of services, from initial design reviews to final certification, ensuring that products and processes meet regulatory requirements and industry standards. In conclusion, the TIC market in North America is driven by the need for regulatory compliance, industry standards, and the increasing adoption of remote testing methods. Providers of testing, inspection, and certification services offer a range of services, from material testing and performance analysis to system certification and remote inspections, enabling organizations to maintain quality and trust in their products and processes.

What are the market trends shaping the Testing Inspection and Certification in North America Industry?

- The trend in the testing, inspection, and certification market is marked by an increasing number of strategic mergers and acquisitions (M&A). This growth is a reflection of the industry's dynamic nature and the continuous pursuit of innovation and expansion.

- The North American testing, inspection, and certification market is driven by the increasing demand for third-party certification and compliance testing in various industries. Process certification, chemical testing, inspection services, environmental testing, and data analysis are key service offerings in this market. Quality assurance is a significant focus, with inspection agencies playing a crucial role in ensuring manufacturing processes meet required standards. Mergers and acquisitions (M&A) contribute to market consolidation, enabling larger providers to offer a broader range of services and better serve clients. These transactions allow for the acquisition of specialized expertise, technology platforms, or industry-specific knowledge, enabling testing inspection and certification providers to address a wider range of client needs and capitalize on growth opportunities in emerging sectors.

- For instance, Bureau Veritas SA's acquisition of IMPACTIVA GROUP SA expanded its supply chain services for the footwear and apparel industry. Overall, the market benefits from increased competition, economies of scale, and enhanced service offerings.

What challenges does the Testing Inspection and Certification in North America Industry face during its growth?

- The growth of the industry is significantly impacted by the complex challenges posed by data security and confidentiality concerns in testing, inspection, and certification processes. Ensuring the protection of sensitive information is a critical priority that demands the attention and resources of industry professionals.

- Testing inspection and certification companies play a crucial role in ensuring product quality and safety for businesses. They offer services such as personnel certification, inspection equipment calibration, first-party certification, and laboratory services, including product testing, root cause analysis, and risk assessment. These companies utilize testing laboratories for mechanical testing and other quality control measures. Protecting sensitive client information, including proprietary data, trade secrets, and intellectual property, is essential. Confidentiality agreements are often signed to safeguard information shared during testing, inspection, and certification processes.

- Breaches of these agreements can result in severe legal and reputational consequences. Moreover, testing inspection and certification companies are vulnerable to cybersecurity threats, including data breaches, ransomware attacks, phishing scams, and malware infections. Ensuring robust cybersecurity measures is vital to mitigate these risks and maintain client trust.

Exclusive Customer Landscape

The testing inspection and certification market in North America forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the testing inspection and certification market in North America report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, testing inspection and certification market in North America forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ALS Ltd. - This company specializes in providing testing, inspection, and certification services for various crane types, including mobile, articulated, telescopic, lattice, bridge, and gantry cranes. Solutions encompass visual inspections and load tests to ensure safety and compliance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ALS Ltd.

- Applus Services S.A.

- British Standards Institution

- Bureau Veritas SA

- DEKRA SE

- DNV Group AS

- Dynamic Research Inc.

- Element Materials Technology Group Ltd.

- Eurofins Scientific SE

- Intertek Group Plc

- LRQA Group Ltd.

- Mistras Group Inc.

- NSF International

- RINA Spa

- SGS SA

- The Smithers Group Inc.

- TUV NORD AG

- TUV Rheinland AG

- TUV SUD AG

- UL Solutions Inc.

- HOLDING SOCOTEC S.A.S.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Testing Inspection And Certification Market In North America

- In January 2024, Intertek, a leading global total quality and inspection, testing, certification, and advisory organization, announced the acquisition of QPS, a renowned provider of testing, inspection, and certification services for the renewable energy industry in North America. This strategic move expanded Intertek's presence in the renewable energy sector and strengthened its offering in the North American market (Intertek Press Release, 2024).

- In March 2024, SGS, the world's leading inspection, verification, testing, and certification company, launched its new digital platform, mySGS, in North America. This innovative solution offers clients real-time access to their testing and certification data, enhancing transparency and efficiency (SGS Press Release, 2024).

- In May 2025, TÃV SÃD, a global testing, inspection, and certification organization, entered into a strategic partnership with the National Renewable Energy Laboratory (NREL) in the United States. This collaboration aimed to accelerate the development and market introduction of innovative renewable energy technologies (TÃV SÃD Press Release, 2025).

- In the same month, Bureau Veritas, a global leader in testing, inspection, and certification services, announced a significant investment in its North American laboratories. This multi-million-dollar investment was aimed at enhancing the company's testing capabilities and expanding its capacity to meet the growing demand for testing and certification services in the region (Bureau Veritas Press Release, 2025).

Research Analyst Overview

- The North American testing, inspection, and certification market encompasses various sectors, including forensic engineering, process capability analysis, software validation, legal compliance, and more. In the realm of manufacturing, lean manufacturing and six sigma methodologies drive the need for sampling methods, quality control charts, calibration standards, and equipment maintenance to ensure continuous improvement and process improvement. Product liability and due diligence necessitate rigorous testing methods and analytical services to prevent product recalls and maintain data integrity. Legal compliance, occupational safety, and industrial safety are essential areas where contract negotiation and risk management play a significant role.

- In the realm of software validation, data acquisition and data integrity are crucial for ensuring product liability and consumer safety. Environmental protection and failure prevention are also critical aspects, requiring reference materials, test methods, and supply chain security. The market trends reflect a growing emphasis on risk management, with an increasing focus on process improvement, quality metrics, and control charts. The integration of lean manufacturing, six sigma, and continuous improvement methodologies has led to a heightened need for effective contract negotiation and project management. The importance of product recalls and consumer safety has also highlighted the significance of failure prevention, material characterization, and analytical services.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Testing Inspection and Certification Market in North America insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

148 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.78% |

|

Market growth 2024-2028 |

USD 14.7 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.27 |

|

Key countries |

US, Canada, Mexico, and North America |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Testing Inspection and Certification Market in North America Research and Growth Report?

- CAGR of the Testing Inspection and Certification in North America industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the testing inspection and certification market in North America growth of industry companies

We can help! Our analysts can customize this testing inspection and certification market in North America research report to meet your requirements.

RIA -

RIA -