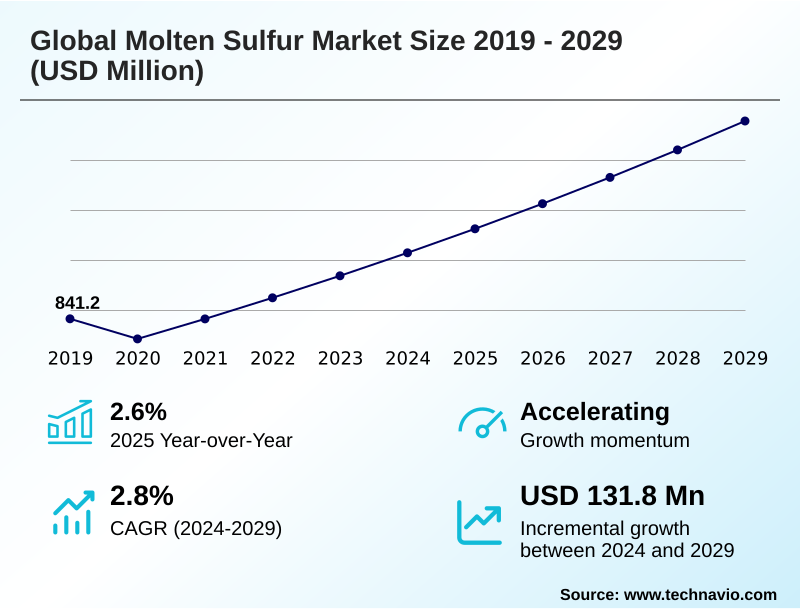

Molten Sulfur Market Size 2025-2029

The molten sulfur market size is valued to increase by USD 131.8 million, at a CAGR of 2.8% from 2024 to 2029. Stringent environmental regulations on hydrocarbon desulfurization will drive the molten sulfur market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 47.3% growth during the forecast period.

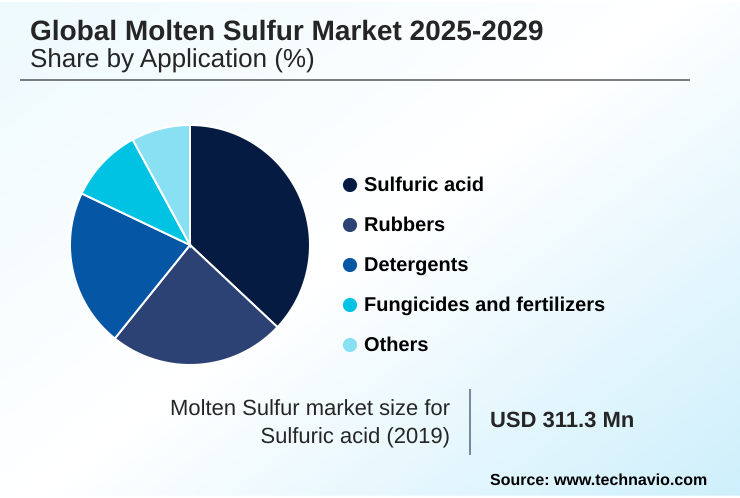

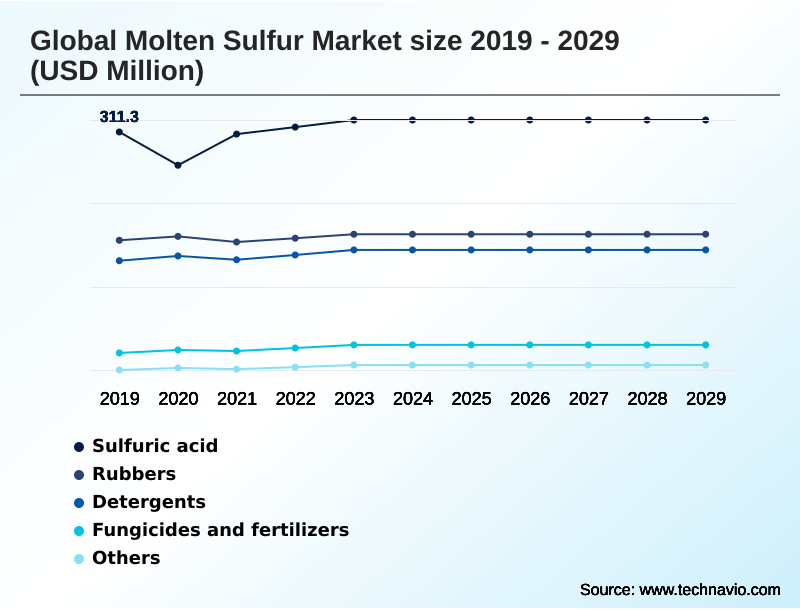

- By Application - Sulfuric acid segment was valued at USD 323.6 million in 2023

- By End-user - Fertilizer and agro-chemicals segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 197.8 million

- Market Future Opportunities: USD 131.8 million

- CAGR from 2024 to 2029 : 2.8%

Market Summary

- The molten sulfur market operates on a unique paradigm where supply is an involuntary consequence of environmental compliance rather than a response to direct demand. Stringent regulations requiring hydrocarbon desulfurization in oil and gas processing are the primary force behind production, making the market's volume contingent on energy sector activities.

- This creates a fundamental disconnect from its main consumption driver: the agricultural industry's need for sulfuric acid to produce phosphate fertilizers. The resulting dynamic is characterized by strategic regional supply-demand imbalances, fostering a complex global trade network.

- For instance, a major fertilizer manufacturer in a region with limited refining capacity must secure long-term contracts with producers in energy-rich regions, navigating volatile freight costs and geopolitical risks to ensure a steady supply of elemental sulfur recovery.

- This necessitates sophisticated logistics and risk management, as any disruption in the energy supply chain, such as a cut in crude oil production, directly curtails the availability of molten sulfur, irrespective of agricultural demand.

What will be the Size of the Molten Sulfur Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Molten Sulfur Market Segmented?

The molten sulfur industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Sulfuric acid

- Rubbers

- Detergents

- Fungicides and fertilizers

- Others

- End-user

- Fertilizer and agro-chemicals

- Chemicals and petrochemicals

- Oil and gas refining

- Mining and metallurgy

- Others

- Technology

- Claus process

- Granulation

- Shell process

- Frasch process

- Resublimed process

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Application Insights

The sulfuric acid segment is estimated to witness significant growth during the forecast period.

Sulfuric acid production is the principal application, driven by its foundational role in chemical synthesis and industrial processing.

This non-discretionary byproduct supply originates from oil and gas operations, creating a market dynamic intrinsically tied to energy sector output rather than end-user demand.

The logistical complexity of moving this material requires a robust heated transport infrastructure, including specialized railcars and vessels. Its use extends to mining and metallurgy use, where it is a key reagent.

Innovations focus on creating value-added products like sulfur derivative chemicals and sulfur-bentonite blends for agricultural applications. Effectively managing supply inelasticity is a primary strategic focus, necessitating sophisticated strategic inventory management and a move toward a circular economy in sulfur.

Long-term supply agreements are crucial for stability, while accurate byproduct stream valuation helps refiners optimize their operations, with some achieving a 10% improvement in byproduct revenue.

The Sulfuric acid segment was valued at USD 323.6 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

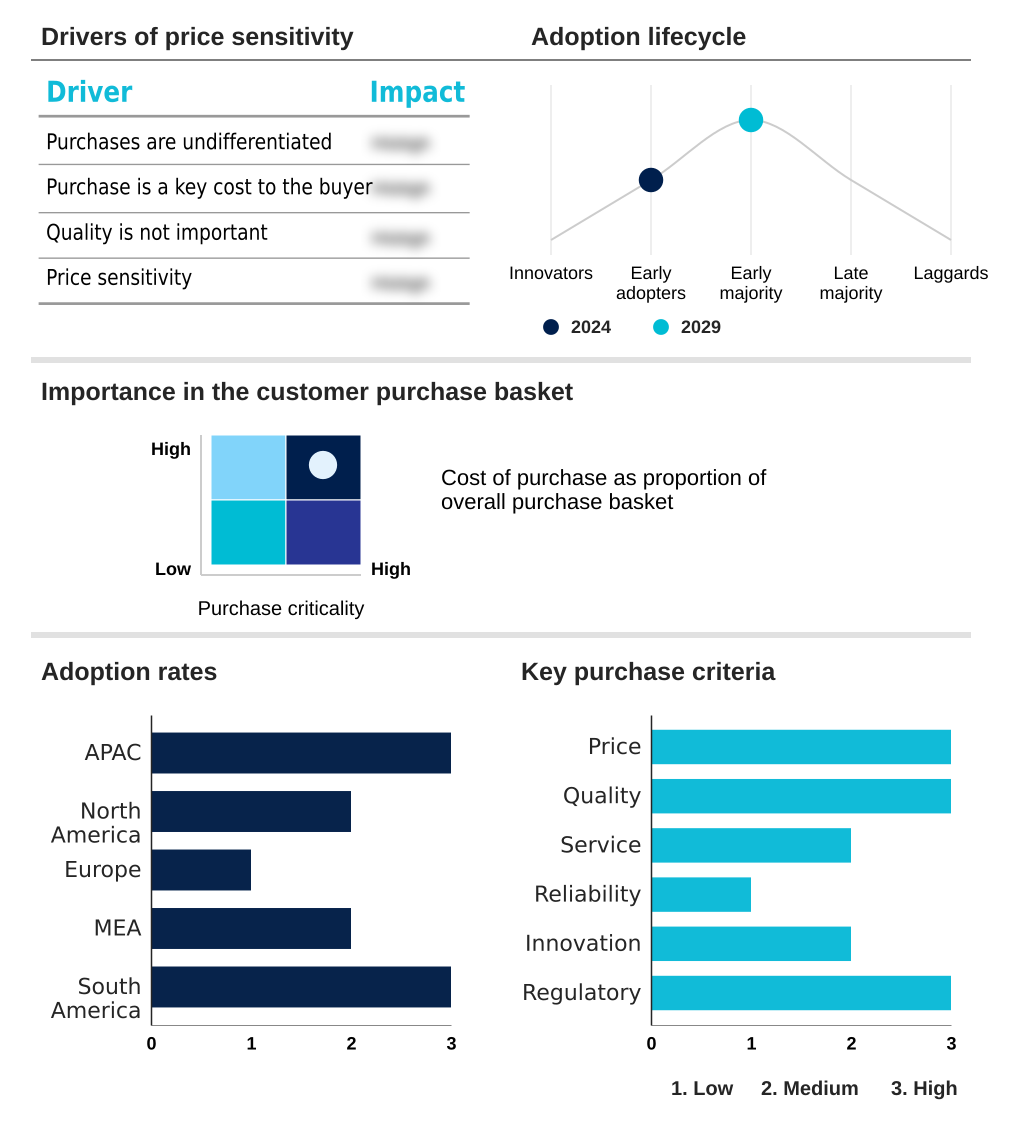

APAC is estimated to contribute 47.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Molten Sulfur Market Demand is Rising in APAC Request Free Sample

The geographic landscape is defined by a dislocation between production and consumption centers.

Regions like the Middle East and North America are net exporters due to extensive refining operations, while APAC, with a 3.2% growth rate, is the largest demand hub, driven by agricultural sulfur demand.

The effective implementation of environmental compliance technology is universal, mandating the reduction of sulfur dioxide emissions globally. This requires robust sulfur handling systems and advanced process control software to manage refinery-grade sulfur output.

Investment in this capital-intensive infrastructure is critical; facilities with modern catalyst formulations for sulfur report a 5% higher recovery rate.

Molten material handling safety remains a top priority, influencing the sulfur quality for acid production and overall operational viability, with APAC accounting for 47.3% of the incremental growth.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global molten sulfur market 2025-2029 operates within a complex framework where technology for molten sulfur transportation and storage is as critical as production itself. The economic impact of geopolitical risk on sulfur trade is significant, as the impact of opec cuts on byproduct sulfur supply can create immediate shortages.

- The role of molten sulfur in the phosphate fertilizer industry remains the primary demand driver, making the cost-benefit of heated tanker vessel investment a key strategic calculation for logistics providers. On the supply side, optimizing claus process for higher sulfur recovery is a constant objective for refiners.

- A molten sulfur vs solid sulfur logistics comparison consistently shows that liquid transport is more cost-effective for large volumes, despite higher initial investment. This influences decisions on managing price volatility in the molten sulfur market. Regulatory drivers for hydrocarbon desulfurization ensure a steady, if inflexible, supply.

- The challenges of supply inelasticity in chemical markets necessitate strategic sourcing of sulfur for sulfuric acid plants. This is amplified by the growth of sulfur demand in mining and metallurgy. Consequently, the importance of logistics in sulfur arbitrage trading cannot be overstated.

- Improving safety in molten sulfur handling operations is paramount, as is understanding byproduct sulfur quality from different refining processes. The impact of environmental policy on sulfur production, alongside the future of sulfur recovery from industrial waste streams, will continue to shape the market.

- A regional analysis of sulfur supply and demand reveals that facilities with modernized port infrastructure handle nearly 50% more volume. Finally, the molten sulfur applications in specialty chemicals and the analysis of sulfur derivatives market trends represent emerging growth frontiers.

What are the key market drivers leading to the rise in the adoption of Molten Sulfur Industry?

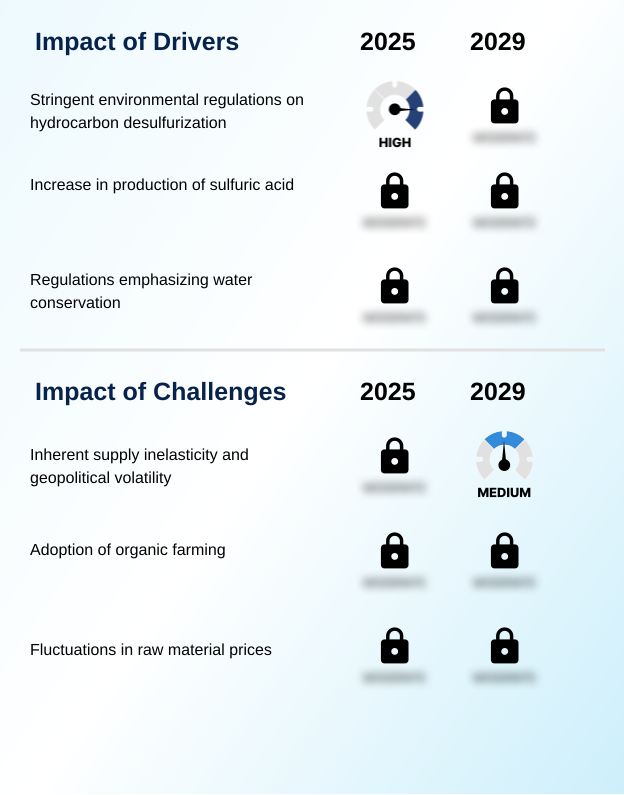

- Stringent environmental regulations mandating hydrocarbon desulfurization are the primary driver for the market's supply-side dynamics.

- The market's primary driver is the non-negotiable regulatory mandate for desulfurization, making byproduct sulfur from refining a constant output of the energy sector. This involuntary supply from sour gas processing is managed through energy sector byproduct management strategies.

- The largest consumer remains the sulfuric acid manufacturing industry, which links market dynamics directly to the agricultural commodity prices link. Even the rubber vulcanization process relies on this steady supply.

- The logistical chain, including heated storage tanks, is critical, as molten sulfur transportation costs can constitute a significant portion of the final delivered price, sometimes up to 40%.

- The inherent sulfur supply chain volatility, often influenced by the geopolitical impact on sulfur supply, creates a challenging environment where supply security, rather than price alone, dictates purchasing decisions.

What are the market trends shaping the Molten Sulfur Industry?

- Strategic regional supply-demand imbalances are creating significant opportunities for logistical arbitrage. This is becoming a defining trend within the market.

- The market's most significant trend is the intensification of strategic regional supply-demand imbalance, which is driving sophisticated logistical responses. This dynamic elevates the importance of molten sulfur logistics and makes intercontinental sulfur trade a critical component of market stability.

- Investment in sulfur export infrastructure in production-heavy regions has increased by over 20% in recent years, matched by expansions in sulfur import logistics at consumption hubs. The core of this activity stems from hydrocarbon desulfurization activities and the efficiency of claus process technology. As a result, molten sulfur price dynamics are increasingly tied to freight costs and arbitrage opportunities.

- This trend is further supported by the growing use of sulfur-based agrochemicals and the need for reliable elemental sulfur recovery, with optimized shipping routes reducing delivery times by an average of 15%.

What challenges does the Molten Sulfur Industry face during its growth?

- Inherent supply inelasticity, compounded by geopolitical volatility, presents a key challenge to industry growth and stability.

- Inherent supply inelasticity remains the market's greatest challenge, as production is divorced from demand dynamics. This condition is intensified by geopolitical volatility, making long-term supply agreements essential for stability. For instance, disruptions can cause price spikes of over 30% in a single quarter.

- The market's reliance on specialized tanker vessels and complex inland distribution networks makes the entire supply chain vulnerable. Key industrial sulfur applications, such as phosphate fertilizer production, are directly impacted by this fragility. Ensuring consistent sulfur purity standards during transit adds another layer of complexity.

- As a result, market participants are increasingly focused on sulfur recovery rate optimization and securing access to reliable port reception facilities. Investments in granulation technology are also considered a hedge, allowing conversion to solid form during periods of logistical constraint, which can reduce storage costs by 15% compared to maintaining molten inventory.

Exclusive Technavio Analysis on Customer Landscape

The molten sulfur market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the molten sulfur market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Molten Sulfur Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, molten sulfur market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

A. J. Edmond Company - Specialized polycyclamine lining systems are offered to ensure containment and transport integrity for high-solids molten materials.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A. J. Edmond Company

- Abu Dhabi National Oil Co.

- Akzo Nobel NV

- Chemtrade Logistics Income Fund

- Chevron Corp.

- Eidon Ionic Minerals

- H.J. Baker and Bro. LLC.

- Hindustan Petroleum Corp. Ltd.

- Kuwait National Petroleum Co.

- Marathon Petroleum Corp.

- Martin Midstream Partners L.P.

- Moeve, S.A.

- Montana Sulphur and Chemical Co.

- QUADRIMEX CHEMICAL

- Repsol SA

- Sasol Ltd.

- Sikko Industries Ltd.

- Suncor Energy Inc.

- Teck Resources Ltd.

- Tengizchevroil LLP

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Molten sulfur market

- In September 2024, Chemtrade Logistics Income Fund announced the completion of an upgrade to its North American terminal network, increasing its molten sulfur storage capacity by 15% to better manage regional supply-demand imbalances, according to a company press release.

- In November 2024, a strategic partnership was formed between Marathon Petroleum Corp. and a leading agricultural cooperative to establish a dedicated supply chain for delivering molten sulfur directly to new fertilizer production facilities in the US Midwest, as reported by Reuters.

- In February 2025, Suncor Energy Inc. secured a key patent for a new-generation heated tanker design that reduces energy consumption for temperature maintenance by up to 20%, enhancing the efficiency and environmental profile of long-haul sulfur transport.

- In April 2025, Sasol Ltd. completed the divestment of its non-core chemical assets to focus on its primary energy and chemicals portfolio, a move that included the sale of a regional sulfur distribution network to a specialized logistics provider, aiming to streamline operations.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Molten Sulfur Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 311 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 2.8% |

| Market growth 2025-2029 | USD 131.8 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 2.6% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The molten sulfur market is fundamentally shaped by its status as a non-discretionary byproduct supply, primarily from sour gas processing and hydrocarbon desulfurization. Its trajectory is dictated by environmental compliance technology rather than direct market demand, with the claus process technology being central to elemental sulfur recovery.

- A key boardroom consideration is navigating the logistics, as the material requires heated transport infrastructure, including heated storage tanks and specialized tanker vessels. The market's primary offtake is for sulfuric acid manufacturing, crucial for phosphate fertilizer production and a growing range of industrial sulfur applications. The rubber vulcanization process also represents a steady demand source.

- Volatility is inherent due to the link between supply and refinery operations, compelling consumers to secure refinery-grade sulfur with consistent sulfur purity standards. For producers, decisions around granulation technology for solidifying surplus are weighed against the economics of maintaining molten sulfur logistics. For consumers in agriculture, demand for sulfur-based agrochemicals and sulfur-bentonite blends is rising to address soil deficiencies.

- In mining and metallurgy use, sulfur is critical for leaching operations. Firms that have optimized their supply chains have achieved a 20% improvement in supply chain predictability, a critical advantage in this market.

What are the Key Data Covered in this Molten Sulfur Market Research and Growth Report?

-

What is the expected growth of the Molten Sulfur Market between 2025 and 2029?

-

USD 131.8 million, at a CAGR of 2.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Sulfuric acid, Rubbers, Detergents, Fungicides and fertilizers, and Others), End-user (Fertilizer and agro-chemicals, Chemicals and petrochemicals, Oil and gas refining, Mining and metallurgy, Others), Technology (Claus process, Granulation, Shell process, Frasch process, and Resublimed process) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Stringent environmental regulations on hydrocarbon desulfurization, Inherent supply inelasticity and geopolitical volatility

-

-

Who are the major players in the Molten Sulfur Market?

-

A. J. Edmond Company, Abu Dhabi National Oil Co., Akzo Nobel NV, Chemtrade Logistics Income Fund, Chevron Corp., Eidon Ionic Minerals, H.J. Baker and Bro. LLC., Hindustan Petroleum Corp. Ltd., Kuwait National Petroleum Co., Marathon Petroleum Corp., Martin Midstream Partners L.P., Moeve, S.A., Montana Sulphur and Chemical Co., QUADRIMEX CHEMICAL, Repsol SA, Sasol Ltd., Sikko Industries Ltd., Suncor Energy Inc., Teck Resources Ltd. and Tengizchevroil LLP

-

Market Research Insights

- The market is shaped by a delicate balance between involuntary supply and robust industrial demand, creating distinct arbitrage opportunities. The molten sulfur price dynamics are heavily influenced by the cost of intercontinental sulfur trade and logistics. Managing this regional supply-demand imbalance requires significant investment in both sulfur export infrastructure and specialized sulfur import logistics.

- Firms leveraging advanced analytics for optimizing routes have documented molten sulfur transportation costs reductions of up to 12%. Furthermore, the inherent sulfur supply chain volatility, driven by energy sector byproduct management, has prompted over 30% of major consumers to diversify their supplier portfolios to mitigate geopolitical impact on sulfur supply.

- This strategic realignment is also tied to the agricultural commodity prices link, where demand forecasting accuracy has improved by nearly 15% through integrated market data.

We can help! Our analysts can customize this molten sulfur market research report to meet your requirements.

RIA -

RIA -