Mobile Middleware Market Size 2026-2030

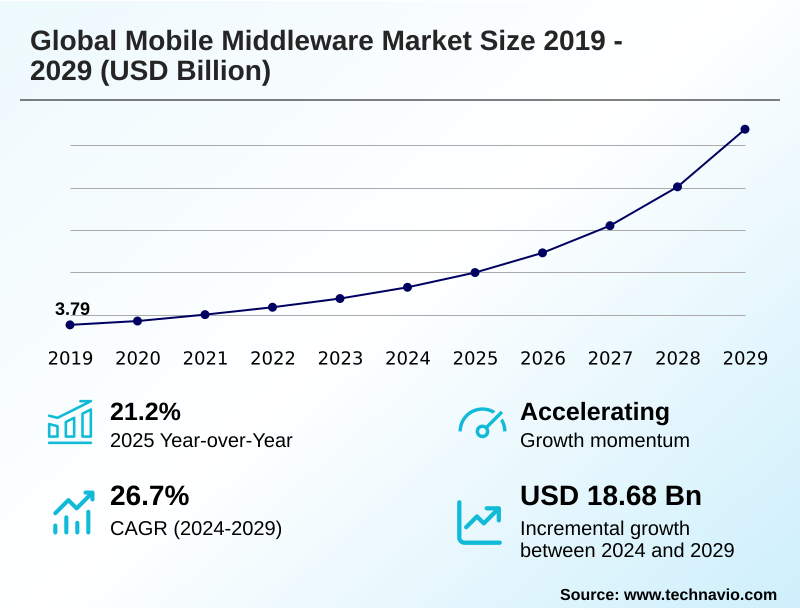

The mobile middleware market size is valued to increase by USD 25.88 billion, at a CAGR of 29.2% from 2025 to 2030. Increasing adoption of enterprise mobility and BYOD policies will drive the mobile middleware market.

Major Market Trends & Insights

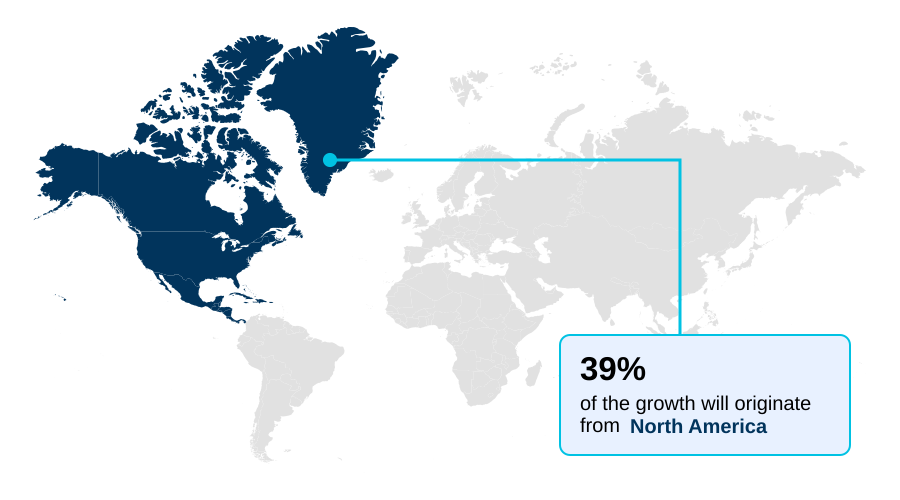

- North America dominated the market and accounted for a 38.8% growth during the forecast period.

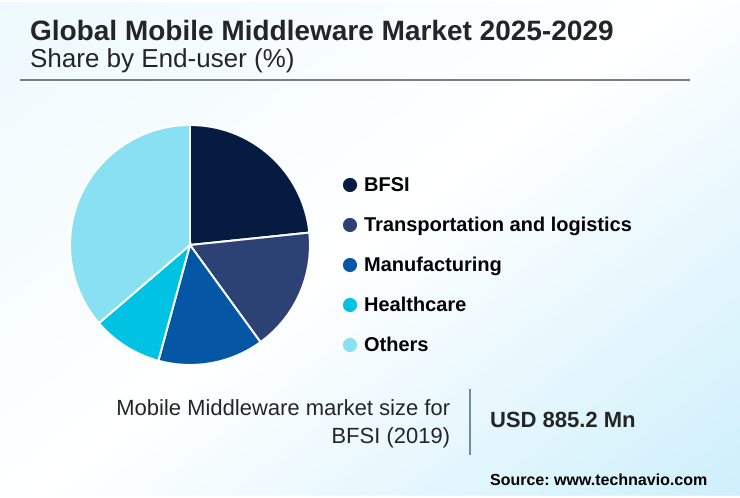

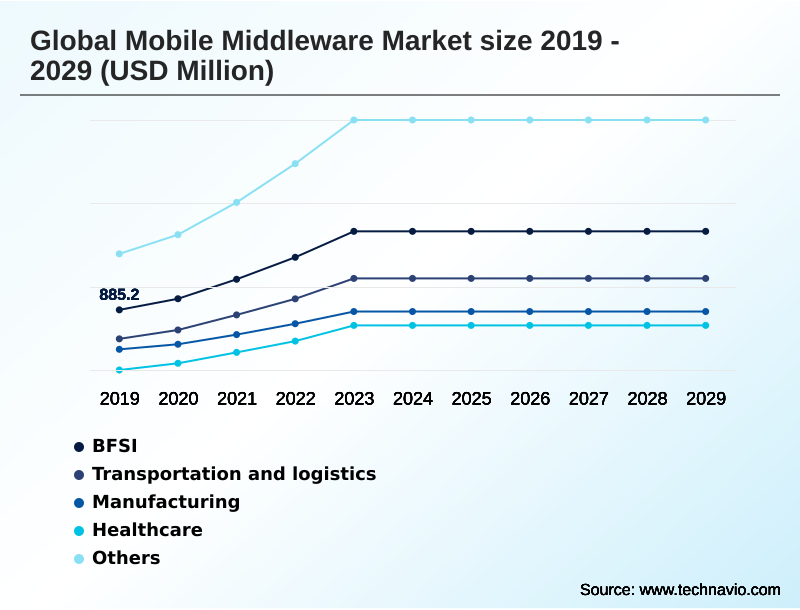

- By End-user - BFSI segment was valued at USD 1.86 billion in 2024

- By Deployment - On-premises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 31.61 billion

- Market Future Opportunities: USD 25.88 billion

- CAGR from 2025 to 2030 : 29.2%

Market Summary

- The mobile middleware market is foundational to modern enterprise mobility, enabling seamless communication between diverse mobile applications and complex backend systems. It addresses critical challenges in enterprise application integration by providing a structured layer for data synchronization, security, and API management. The market's evolution is driven by the need for real-time data processing and support for hybrid cloud deployments.

- Platforms increasingly incorporate low-code development capabilities, AI integration, and edge computing support to meet demands for agility and intelligence. A key business scenario involves a global logistics company using middleware to connect its mobile apps for drivers with legacy inventory systems and cloud-based route optimization services.

- This integration platform as a service ensures data consistency across all endpoints, enables offline data synchronization in areas with poor connectivity, and enforces a zero-trust security model to protect sensitive shipment data. This use of API-led connectivity and mobile backend services achieves significant latency reduction, improving delivery times and operational efficiency.

- The market is also shaped by the need for cross-platform mobile frameworks to manage device fragmentation and the push for containerization support to enhance scalability and portability of mobile workflow orchestration tasks.

What will be the Size of the Mobile Middleware Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Mobile Middleware Market Segmented?

The mobile middleware industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- BFSI

- Transportation and logistics

- Healthcare

- Manufacturing

- Others

- Deployment

- On-premises

- Cloud

- Type

- Software

- Services

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By End-user Insights

The bfsi segment is estimated to witness significant growth during the forecast period.

The BFSI sector demonstrates significant adoption, driven by the need for secure and compliant mobile solutions. This industry leverages middleware for robust enterprise application integration, connecting core banking systems with modern mobile frontends.

Key functionalities include real-time data processing for instant transactions and secure data transport to protect sensitive financial information. Platforms incorporate strong data encryption standards and advanced user authentication methods for enhanced mobile identity management.

Solutions also provide comprehensive audit trail logging and facilitate GDPR compliance support, which are critical for data sovereignty management. The use of message-oriented middleware ensures reliable communication, while data format translation bridges legacy and new systems.

This comprehensive approach to enterprise data connectivity and secure access control has led to a 25% reduction in transaction processing errors.

The BFSI segment was valued at USD 1.86 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Mobile Middleware Market Demand is Rising in North America Request Free Sample

North America is poised to contribute nearly 39% of the market's incremental opportunity, driven by advanced cloud adoption and a mature enterprise ecosystem focused on digital transformation.

The region's demand for sophisticated API lifecycle management and comprehensive backend as a service (BaaS) platforms is high. European markets prioritize compliance and security, while APAC emerges as the fastest-growing region due to rapid mobile proliferation.

Across regions, enterprises are adopting integration platform as a service (iPaaS) solutions to achieve latency reduction and data throughput optimization.

Key features in demand include robust API gateway functionality for managing API traffic management, effective offline data synchronization, and reliable backend data synchronization.

Building a scalable backend architecture with mobile data caching and seamless enterprise systems connection is critical for providing superior cross-platform development support.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global mobile middleware market 2026-2030 is evolving beyond simple connectivity, becoming a strategic enabler for digital business. A key application is its use in the global mobile middleware market 2026-2030 for enterprise mobility, where it supports diverse device ecosystems.

- The global mobile middleware market 2026-2030 in hybrid cloud environments is particularly significant, providing the flexibility to manage workloads across on-premises and public cloud infrastructures. Strong global mobile middleware market 2026-2030 security features are non-negotiable, especially when dealing with the global mobile middleware market 2026-2030 and legacy systems, where bridging old and new technologies creates vulnerabilities.

- For organizations with the global mobile middleware market 2026-2030 for BYOD policies, it ensures secure access without compromising corporate data. The rise of the global mobile middleware market 2026-2030 using low-code platforms is democratizing app development. Furthermore, the global mobile middleware market 2026-2030 in 5G networks is unlocking new use cases by reducing application latency.

- The global mobile middleware market 2026-2030 with AI integration is adding a layer of intelligence for predictive analytics. This is crucial for the global mobile middleware market 2026-2030 for IoT devices, where managing massive data streams is essential.

- Sectors like the global mobile middleware market 2026-2030 in financial services and the global mobile middleware market 2026-2030 for supply chain depend on its reliability. The focus on global mobile middleware market 2026-2030 platform scalability ensures that solutions can grow with the business. Global mobile middleware market 2026-2030 deployment best practices emphasize a phased approach.

- A key debate is the value of the global mobile middleware market 2026-2030 vs direct API integration, with middleware offering superior governance and lifecycle management. Addressing global mobile middleware market 2026-2030 managing device fragmentation and understanding global mobile middleware market 2026-2030 implementation cost factors are critical for success.

- Its role in global mobile middleware market 2026-2030 ensuring data sovereignty, especially for the global mobile middleware market 2026-2030 for healthcare data, and its fit with the global mobile middleware market 2026-2030 with microservices solidify its importance. Businesses using comprehensive middleware platforms report twice the success rate in their digital transformation initiatives compared to those relying on custom point-to-point integrations.

What are the key market drivers leading to the rise in the adoption of Mobile Middleware Industry?

- The increasing adoption of enterprise mobility strategies and bring-your-own-device policies is a key driver for market growth.

- Market growth is significantly driven by enterprise mobility initiatives and the need for flexible infrastructure.

- Widespread adoption of enterprise mobility management strategies and formal BYOD policy enforcement necessitates robust platforms that can handle diverse endpoints securely, often leading to a 20% improvement in workforce productivity.

- The shift towards hybrid cloud deployment and multi-cloud interoperability demands middleware that serves as a hybrid integration platform, ensuring seamless cloud service integration. This is supported by cloud-native integration and extensive containerization support, managed through application container orchestration.

- Implementing a zero-trust security model is becoming standard for securing data flows. These drivers promote application deployment automation and sophisticated mobile workflow orchestration, streamlining operations and enhancing security through effective mobile device management.

What are the market trends shaping the Mobile Middleware Industry?

- The integration of artificial intelligence into middleware platforms is an emerging market trend, enhancing automation and decision-making capabilities within mobile ecosystems.

- Emerging trends are reshaping the market, with an emphasis on agility and intelligence. The adoption of a low-code development platform and tools for no-code application integration accelerates deployment cycles by up to 60%. This shift democratizes development, enabling business users to create solutions within a controlled integration development environment.

- Concurrently, edge computing middleware is gaining traction, facilitating processing closer to data sources and reducing latency. This is complemented by the move toward event-driven architecture and serverless computing models, which optimize resource use and enhance scalability. These trends leverage API-led connectivity and advanced real-time messaging protocols for seamless data flow.

- The integration with a real-time analytics engine provides immediate insights, while mobile network optimization and event stream processing ensure high performance for modern applications.

What challenges does the Mobile Middleware Industry face during its growth?

- The complexity of integrating with legacy systems presents a significant challenge to market growth, requiring specialized solutions to bridge technological gaps.

- Despite market momentum, significant challenges persist, primarily concerning integration and cost. The complexity of legacy system integration remains a primary hurdle, as connecting modern mobile backend services with outdated systems often requires extensive custom data mapping services and can increase project costs by over 30%. Ensuring data consistency management across a distributed system integration is also difficult.

- Device fragmentation complicates development, requiring a robust cross-platform mobile framework but increasing testing overhead. High implementation and maintenance costs, especially for mobile application security, deter smaller enterprises. Continuous application performance monitoring and the use of mobile app performance analytics are essential but add to operational expenses, even when moving from a service-oriented architecture to modern workflow automation tools.

Exclusive Technavio Analysis on Customer Landscape

The mobile middleware market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the mobile middleware market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Mobile Middleware Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, mobile middleware market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - Delivers cloud-native backend services and API management, enabling scalable mobile backends with data synchronization and enterprise systems integration.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Appian Corp.

- Axway Software SA

- Broadcom Inc.

- Google LLC

- IBM Corp.

- Magic Software Enterprises Ltd.

- Mendix Technology BV

- Microsoft Corp.

- Open Text Corp.

- Oracle Corp.

- OutSystems Software Rede SA

- Pegasystems Inc.

- Progress Software Corp.

- Salesforce Inc.

- SAP SE

- ServiceNow Inc.

- Temenos AG

- TIBCO Software Inc.

- WSO2 Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Mobile middleware market

- In January 2025, IBM Corporation announced a new middleware platform focused on virtualized deployments to support seamless integration in hybrid work settings.

- In February 2025, Oracle Corporation enhanced its cloud-based Oracle Integration solution with AI capabilities to improve automation for mobile-edge interactions.

- In April 2025, IBM Corp. and SAP SE expanded their collaboration to offer a unified approach for mobile access to enterprise resource planning systems, improving supply chain visibility.

- In May 2025, Microsoft Corp. released an updated Azure API Management platform featuring AI-enhanced security measures and automated policy enforcement for enterprise mobile applications.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Mobile Middleware Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 29.2% |

| Market growth 2026-2030 | USD 25879.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 23.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The mobile middleware market is instrumental in enterprise digital transformation, bridging the gap between mobile frontends and backend infrastructure. Core offerings revolve around providing robust mobile backend services, comprehensive API lifecycle management, and effective cross-platform development support. Platforms are evolving to deliver sophisticated workflow automation tools and data mapping services that simplify legacy system integration.

- A key boardroom consideration is aligning middleware strategy with BYOD policy enforcement and implementing a zero-trust security model to mitigate risks in hybrid cloud deployment scenarios. Adopting message-oriented middleware alongside an event-driven architecture ensures reliable real-time data processing and data throughput optimization. The integration of AI-powered solutions is a pivotal trend.

- Functionalities like offline data synchronization, push notification services, and API gateway functionality have become standard. Moreover, the shift toward a low-code development platform and no-code application integration significantly boosts developer productivity increase. Advanced application performance monitoring tools help achieve crucial latency reduction. The adoption of cloud-native integration, containerization support, and serverless computing models enhances multi-cloud interoperability.

- Managing compliance through GDPR compliance support, audit trail logging, and data sovereignty management is critical, with firms reporting a 20% improvement in compliance-related workflows. This is all enabled by secure data transport and precise data format translation.

What are the Key Data Covered in this Mobile Middleware Market Research and Growth Report?

-

What is the expected growth of the Mobile Middleware Market between 2026 and 2030?

-

USD 25.88 billion, at a CAGR of 29.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (BFSI, Transportation and logistics, Healthcare, Manufacturing, and Others), Deployment (On-premises, and Cloud), Type (Software, and Services) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing adoption of enterprise mobility and BYOD policies, Complexities in integrating with legacy systems

-

-

Who are the major players in the Mobile Middleware Market?

-

Amazon.com Inc., Appian Corp., Axway Software SA, Broadcom Inc., Google LLC, IBM Corp., Magic Software Enterprises Ltd., Mendix Technology BV, Microsoft Corp., Open Text Corp., Oracle Corp., OutSystems Software Rede SA, Pegasystems Inc., Progress Software Corp., Salesforce Inc., SAP SE, ServiceNow Inc., Temenos AG, TIBCO Software Inc. and WSO2 Inc.

-

Market Research Insights

- The market is characterized by a strategic shift toward API-led connectivity and hybrid integration platform models to unify distributed system integration. Enterprises leveraging a scalable backend architecture report a 30% improvement in application responsiveness. The adoption of integration platform as a service (iPaaS) is accelerating, with firms achieving a 25% reduction in integration project timelines.

- Advanced real-time messaging protocols are critical for event stream processing, while mobile network optimization and mobile data caching address performance challenges. Effective API traffic management and user authentication methods are central to mobile application security. Mobile device management and application container orchestration are key for managing hybrid cloud deployment.

- This focus on enterprise data connectivity and backend data synchronization provides a clear competitive advantage.

We can help! Our analysts can customize this mobile middleware market research report to meet your requirements.

RIA -

RIA -