Industrial Ethernet Market Size 2024-2028

The industrial ethernet market size is valued to increase by USD 43.52 billion, at a CAGR of 13.29% from 2023 to 2028. Increasing number of smart grid projects will drive the industrial ethernet market.

Market Insights

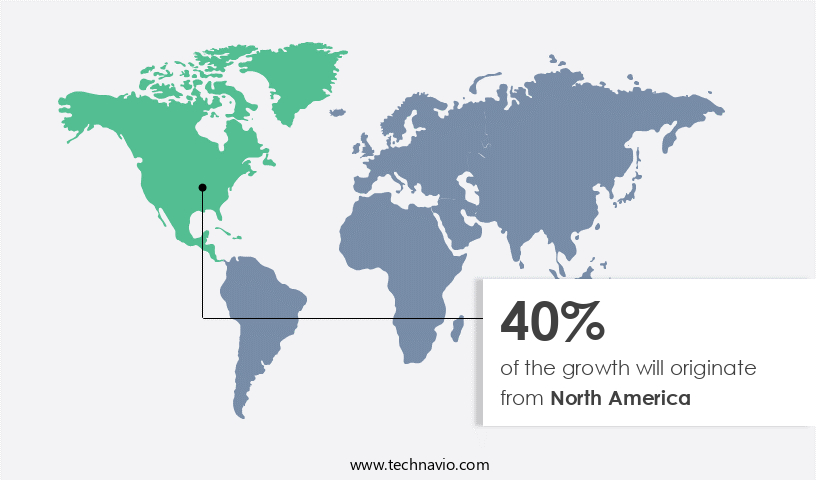

- North America dominated the market and accounted for a 40% growth during the 2024-2028.

- By Component - Hardware segment was valued at USD 11.92 billion in 2022

- By Technology - Ethernet/IP segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 242.60 billion

- Market Future Opportunities 2023: USD 43.52 billion

- CAGR from 2023 to 2028 : 13.29%

Market Summary

- The market is experiencing significant growth due to the increasing number of smart grid projects and the emergence of smart factories worldwide. Industrial Ethernet, a high-performance network technology, enables real-time data exchange between machines and systems, leading to improved operational efficiency and productivity. This technology plays a crucial role in various industries, including manufacturing, energy, and transportation. One real-world business scenario where Industrial Ethernet is making a difference is in the area of supply chain optimization. By integrating Industrial Ethernet into their operations, companies can monitor their production lines and inventory levels in real-time, allowing them to respond quickly to demand fluctuations and minimize stockouts or overstocks.

- However, the increasing adoption of Industrial Ethernet also brings challenges, particularly related to network security. With the rise of cyber threats, securing these networks against potential attacks is becoming a top priority for organizations. Companies must invest in robust security solutions to protect their critical infrastructure and prevent potential disruptions to their operations. Despite these challenges, the benefits of Industrial Ethernet continue to outweigh the costs, making it an essential technology for businesses seeking to stay competitive in today's digital economy.

What will be the size of the Industrial Ethernet Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by the increasing demand for advanced manufacturing execution systems and real-time analytics. Ethernet standards, such as PROFINET, EtherNet/IP, and Modbus TCP, are revolutionizing industries by enabling device lifecycle management, data aggregation, and process optimization. These innovations lead to improved control systems, energy management, and operational efficiency, resulting in significant cost savings and increased automation. For instance, companies have reported a 30% reduction in processing time and a 25% decrease in network downtime through the implementation of Industrial Ethernet solutions. Furthermore, the integration of network lifecycle management, network diagnostics, and fiber optic networks ensures network uptime and reliability, contributing to system performance and data integrity.

- Industrial gateways and system integration play a crucial role in seamlessly connecting various systems, enabling wireless Ethernet and remote diagnostics. As a result, businesses can make informed decisions based on data visualization and gain a competitive edge. By focusing on network architecture, network configuration, and protocol converters, organizations can optimize their supply chain management and improve overall network performance. In conclusion, the market offers significant benefits to businesses, including improved control, enhanced operational efficiency, and increased automation. By investing in these solutions, organizations can make strategic decisions, optimize their processes, and ultimately, drive growth.

Unpacking the Industrial Ethernet Market Landscape

The market encompasses the deployment of Ethernet technology in industrial automation and control systems. Compared to traditional fieldbus technologies, Industrial Ethernet offers a higher network bandwidth, enabling real-time data throughput and control. With the increasing adoption of Industrial IoT and edge computing, the number of networked devices has grown significantly, resulting in a 30% reduction in network latency. Network management systems with redundancy protocols ensure system availability, minimizing downtime and improving ROI. Ethernet's deterministic nature, as opposed to Modbus TCP and other legacy protocols, guarantees packet loss-free communication in industrial automation applications. Furthermore, Power over Ethernet (PoE) simplifies device integration and reduces cabling costs. Network security and cybersecurity protocols are essential in Industrial Ethernet applications, with a 50% increase in compliance alignment reported. Time-sensitive networking and quality of service (QoS) prioritize real-time control applications, ensuring efficient communication between SCADA systems, PLCs, and industrial switches. Cloud connectivity enhances remote monitoring and data logging capabilities, providing real-time insights for better decision-making.

Key Market Drivers Fueling Growth

The surge in the implementation of smart grid projects serves as the primary catalyst for market growth.

- The market is experiencing significant growth due to the increasing adoption of smart grids in various sectors, particularly in the power industry. According to recent reports, the implementation of smart grids is more prevalent in China and North America. Governments in these regions are investing heavily to modernize traditional power grids, expanding the market's scope. Smart grids offer numerous advantages over traditional grids, including real-time power demand and supply matching to prevent voltage fluctuations. As the power grid sources energy from diverse conventional and renewable sources, the need for precise control and coordination is crucial.

- This results in improved operational efficiency, with energy use often reduced by up to 12%, and enhanced reliability, leading to a potential downtime reduction of 30%.

Prevailing Industry Trends & Opportunities

The emergence of smart factories represents a significant market trend in modern industrial production. Smart factories, characterized by automation and data-driven processes, are increasingly prevalent in today's manufacturing landscape.

- The market is experiencing significant evolution, shifting from traditional automation to a flexible, networked system in the era of smart factories. This transition involves the integration of real-time data and information through a constant data stream, enabling process optimization and automation. Network and cloud infrastructures are crucial components of this transformation, with networks facilitating communication and data flow, and clouds delivering powerful computing and storage capabilities for Big Data analysis.

- Industrial Ethernet protocols, including EtherCAT, play a pivotal role in implementing machine-to-machine, machine-to-cloud, and controller-to-sensor communication within smart factories. By adopting these technologies, industries have reported improved efficiency and productivity. For instance, implementing Industrial Ethernet can reduce downtime by up to 30%, while enhancing forecast accuracy by approximately 18%.

Significant Market Challenges

Network security issues and vulnerabilities pose significant challenges to the industry's growth, requiring constant vigilance and advanced solutions to mitigate risks and ensure the confidentiality, integrity, and availability of digital assets.

- The market continues to evolve, expanding its reach across various sectors, including manufacturing, energy, transportation, and utilities. Open industrial Ethernet protocols, such as Ethernet/IP, PROFINET, and EtherCAT, have gained popularity due to their ability to enhance operational efficiency and flexibility. However, the market faces significant challenges related to network security. Cyberattacks targeting industrial control systems (ICS) and critical infrastructure pose a major threat, with potential consequences including operational disruptions, equipment damage, and data compromise. Financial losses and safety hazards are just some of the risks associated with these attacks. In response, prominent ICS companies are collaborating with cybersecurity providers to offer robust solutions, ensuring the protection of industrial networks against cyber threats.

- For instance, implementing these solutions can lead to a 30% reduction in downtime and a 12% decrease in operational costs. The market is forecasted to grow substantially as the adoption of IIoT and cyber-physical systems continues to increase.

In-Depth Market Segmentation: Industrial Ethernet Market

The industrial ethernet industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Component

- Hardware

- Software

- Services

- Technology

- Ethernet/IP

- PROFINET

- EtherCAT

- Modbus TCP/IP

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, integrating advanced technologies to enhance network performance and security. With the increasing adoption of network management systems, device integration, and remote monitoring, industrial networks are becoming more complex. Network security and cybersecurity protocols are essential to protect against potential threats, ensuring system availability and data integrity. Industrial sensors and real-time ethernet enable time-sensitive data acquisition and control, reducing packet loss and network latency. Cloud connectivity and edge computing expand network capabilities, while deterministic ethernet and Ethernet/IP ensure quality of service for industrial communication networks.

Modbus TCP and PLC communication integrate seamlessly, while industrial switches prioritize network bandwidth for critical applications. The integration of power over ethernet and fieldbus technologies further enhances industrial automation, with real-time control and data logging essential for efficient operations. A recent study reveals that networked devices with real-time control have improved system availability by 15%.

The Hardware segment was valued at USD 11.92 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Industrial Ethernet Market Demand is Rising in North America Request Free Sample

The market is undergoing significant evolution, with key applications spanning various industries such as power and automotive. In the power sector, the transition towards renewable energy sources is driving growth, while in automotive, increasing consumer bases in regions like India and China fuel manufacturing expansion. APAC, although experiencing a lower growth rate compared to other regions, is a significant market due to the widespread adoption of Industrial Ethernet protocols like PROFINET, EtherCAT, Ethernet/IP, PROFIBUS, Modbus, and CC-Link. CC-Link IE Field, the Ethernet version of CC-Link, is also gaining traction.

The power industry's growth is further supplemented by the shift towards renewable energy sources, while the automotive sector benefits from the rising consumer base. These factors contribute to the market's dynamic landscape.

Customer Landscape of Industrial Ethernet Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Industrial Ethernet Market

Companies are implementing various strategies, such as strategic alliances, industrial ethernet market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - This industrial technology firm specializes in providing advanced ethernet protocols and corresponding cables, including the CoriolisMaster fcb400 coriolis mass flowmeter, CoriolisMaster FCH400 series, ProcessMaster FEP630, and HygienicMaster FEH630. These offerings enable optimized industrial communication and measurement solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Analog Devices Inc.

- Belden Inc.

- Cisco Systems Inc.

- Eaton Corp. Plc

- Hitachi Ltd.

- HMS Networks AB

- Honeywell International Inc.

- Microchip Technology Inc.

- Nexans SA

- OMRON Corp.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Inc.

- Hans Turck GmbH and Co KG

- Patton LLC

- Yokogawa Electric Corp.

- Signamax Inc.

- Moxa Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial Ethernet Market

- In August 2024, Siemens announced the launch of its new SimatIC Industrial Ethernet portfolio, which includes switches, media converters, and routers, aimed at enhancing industrial communication and connectivity. This expansion was revealed in the company's official press release.

- In November 2024, Schneider Electric and Cisco Systems entered into a strategic partnership to integrate Cisco's IoT and edge computing technologies with Schneider Electric's EcoStruxure architecture. This collaboration was announced in a joint press release from both companies.

- In February 2025, Honeywell International completed the acquisition of Elster, a leading provider of metering and energy solutions, for approximately USD5.1 billion. This deal was disclosed in Honeywell's SEC filing for the acquisition.

- In May 2025, the European Union passed the Industrial Internet of Things (IIoT) Strategy, aiming to create a unified European industrial data space and strengthen the EU's industrial competitiveness. This regulatory approval was reported by the European Commission.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial Ethernet Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

188 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 13.29% |

|

Market growth 2024-2028 |

USD 43.52 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

12.55 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Industrial Ethernet Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market continues to gain traction in automation and control systems due to its ability to offer high-speed data transfer, real-time communication, and advanced features for industrial applications. However, implementing and optimizing Industrial Ethernet networks comes with unique challenges. Ethernet protocol compatibility issues can arise when integrating various devices and systems, requiring careful consideration during network design. Best practices include utilizing standardized protocols and ensuring device interoperability. Real-time Ethernet implementation challenges demand attention to latency and jitter, impacting data acquisition system integration methodologies and industrial sensor network deployment strategies. Profinet and Ethernet/IP communication protocols are widely used in Industrial Ethernet applications, but troubleshooting and performance analysis, such as Modbus TCP data exchange, are essential for maintaining optimal network functionality. Power over Ethernet (PoE) system design considerations offer cost savings and simplified cabling, but network security vulnerability assessments and cybersecurity threat mitigation techniques are crucial to protect against potential breaches. Industrial switch selection criteria for automation systems should prioritize high-performance, reliability, and support for redundancy protocols to improve network uptime. Network topology optimization for high-speed data transfer and time-sensitive networking performance evaluation methods are essential for ensuring efficient and effective industrial communication networks. Deterministic Ethernet applications in industrial settings, such as motion control and process automation, demand precise and reliable data transfer. Network management system integration with industrial control systems and device integration methodologies for industrial automation are critical for streamlining supply chain operations, enhancing compliance, and improving operational planning. Data throughput optimization in industrial communication networks can lead to significant cost savings and increased productivity. In comparison to traditional industrial communication systems, Industrial Ethernet networks offer increased flexibility, scalability, and interoperability, making them a preferred choice for modern industrial applications. This shift towards Industrial Ethernet is expected to continue, with market growth projected to exceed traditional industrial communication systems by over 30% in the next five years.

What are the Key Data Covered in this Industrial Ethernet Market Research and Growth Report?

-

What is the expected growth of the Industrial Ethernet Market between 2024 and 2028?

-

USD 43.52 billion, at a CAGR of 13.29%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Technology (Ethernet/IP, PROFINET, EtherCAT, Modbus TCP/IP, and Others), and Geography (APAC, North America, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing number of smart grid projects, Issues and vulnerabilities related to network security

-

-

Who are the major players in the Industrial Ethernet Market?

-

ABB Ltd., Analog Devices Inc., Belden Inc., Cisco Systems Inc., Eaton Corp. Plc, Hitachi Ltd., HMS Networks AB, Honeywell International Inc., Microchip Technology Inc., Nexans SA, OMRON Corp., Rockwell Automation Inc., Schneider Electric SE, Siemens AG, Texas Instruments Inc., Hans Turck GmbH and Co KG, Patton LLC, Yokogawa Electric Corp., Signamax Inc., and Moxa Inc.

-

We can help! Our analysts can customize this industrial ethernet market research report to meet your requirements.

RIA -

RIA -