India Automotive Market Size 2026-2030

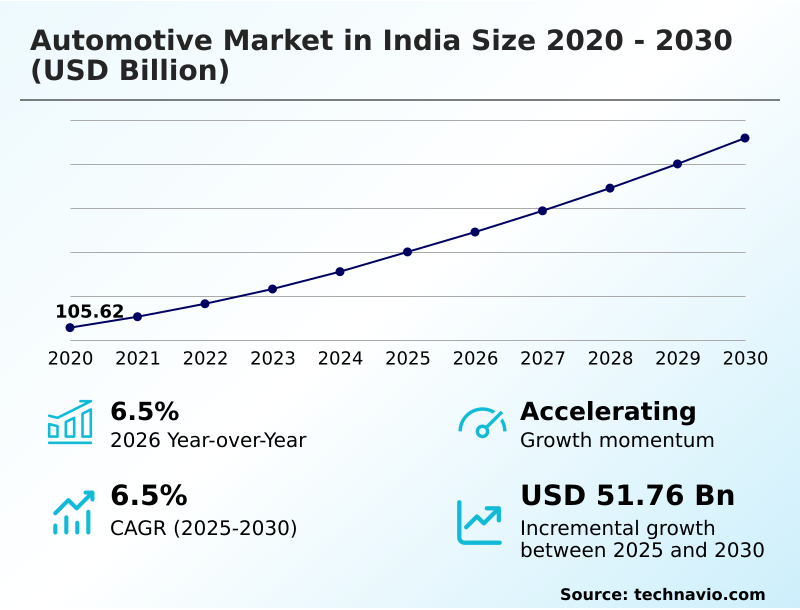

The india automotive market size is valued to increase by USD 51.76 billion, at a CAGR of 6.5% from 2025 to 2030. Integration of SUV and industrialization of premium lifestyle mobility solutions will drive the india automotive market.

Major Market Trends & Insights

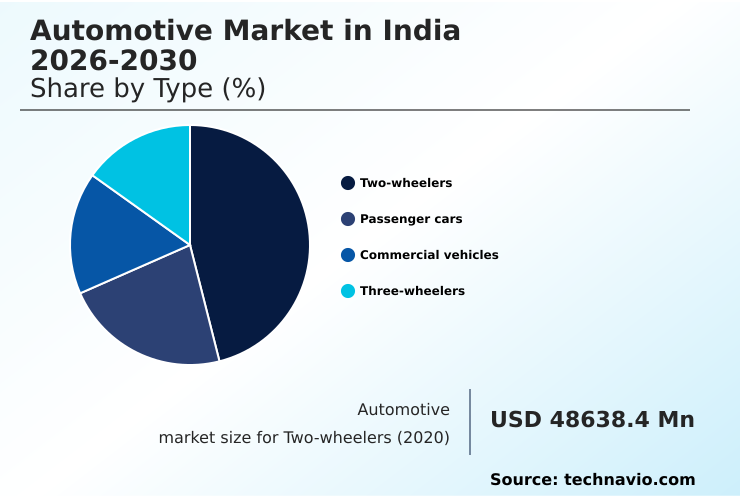

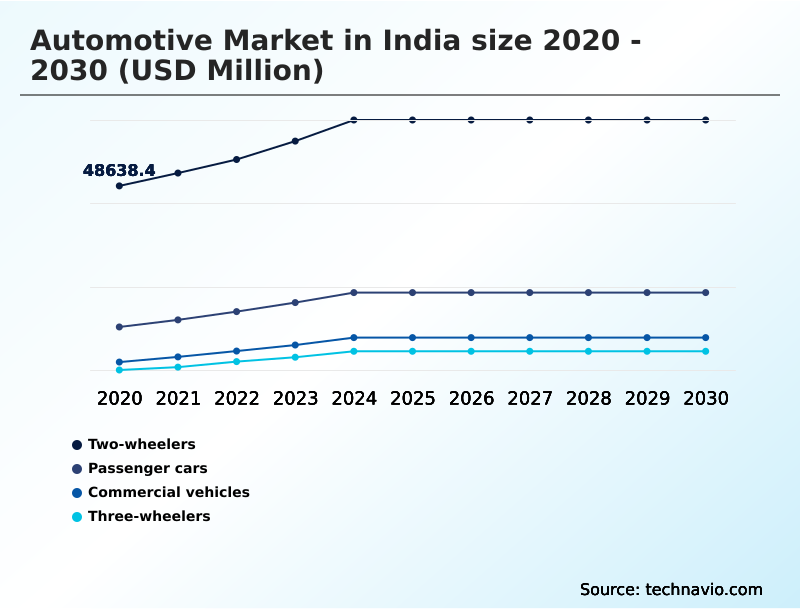

- By Type - Two-wheelers segment was valued at USD 60.33 billion in 2024

- By Fuel Type - Diesel segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 86.18 billion

- Market Future Opportunities: USD 51.76 billion

- CAGR from 2025 to 2030 : 6.5%

Market Summary

- The automotive market in India is navigating a period of profound structural and technological change, propelled by a definitive shift toward premiumization, green mobility, and regulatory modernization. This transformation is underpinned by expanding national infrastructure, rising disposable incomes, and governmental ambitions to establish the nation as a global electric vehicle (EV) manufacturing hub.

- A notable pivot in consumer preference from basic utility to feature-rich vehicles is evident, with strong demand for sport utility vehicles (SUVs), advanced driver-assistance systems (ADAS), and connected-car technologies. The maturation of the domestic component ecosystem, focusing on localizing high-value electronics and battery cells, is crucial for mitigating global supply chain risks.

- For instance, an OEM's ability to seamlessly integrate locally sourced powertrain components can significantly improve production timelines and cost structures. The convergence of robust domestic retail demand, diverse powertrain strategies including hybrid and CNG models, and a focus on manufacturing quality for export markets solidifies the automotive sector's role as a cornerstone of the nation's industrial economy.

What will be the Size of the India Automotive Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the India Automotive Market Segmented?

The india automotive industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Two-wheelers

- Passenger cars

- Commercial vehicles

- Three-wheelers

- Fuel type

- Diesel

- Petrol

- CNG and LPG

- Electric

- Distribution channel

- Offline

- Online

- Geography

- APAC

- India

- APAC

By Type Insights

The two-wheelers segment is estimated to witness significant growth during the forecast period.

The two-wheelers segment is the foundational pillar of personal mobility, particularly sensitive to rural income and credit availability.

This category is experiencing a significant rebound, with retail sales showing a substantial year-over-year increase, driven by normalized rural liquidity and favorable tax reforms enhancing affordability.

The adoption of electric mobility within this segment is notable, with electric variants now comprising 6.6% of the total category. Key evolution within the vehicle manufacturing process includes the integration of advanced safety features and connected-car technologies.

As digital platforms become more prevalent, maintaining high manufacturing quality and fuel efficiency remains critical for competitiveness, especially amid concerns over supply chain volatility and the push toward electric variants.

This ensures continued relevance in a dynamic transportation landscape, supported by robust vehicle-related financing options for three-wheelers as well.

The Two-wheelers segment was valued at USD 60.33 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

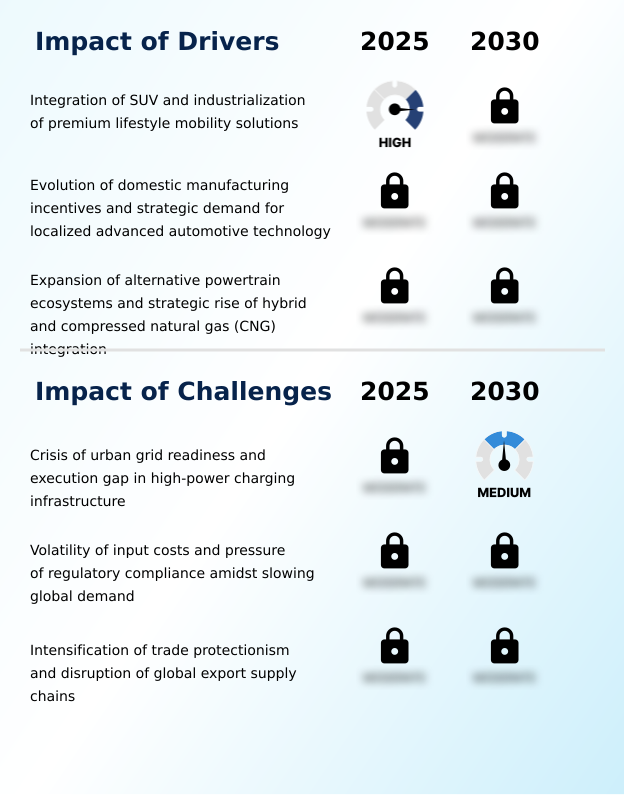

- The automotive market in India is witnessing a dynamic shift, heavily influenced by several interconnected factors. A key indicator is the robust growth in two-wheeler retail sales, which reflects strengthening rural economies and improved consumer liquidity. This is complemented by the pervasive trend of passenger vehicle premiumization, where consumers increasingly demand advanced features and connectivity.

- Concurrently, the sector is navigating the stringent compliance requirements for commercial vehicle emission norms, pushing manufacturers toward cleaner technologies. However, the ambitious push for electrification is tempered by the significant ev charging infrastructure execution gap, which remains a primary concern for potential buyers.

- To address this and reduce reliance on imports, the localization of battery chemistry cells has become a strategic priority for the industry. The recent impact of gst on vehicle affordability has been largely positive, streamlining the tax structure and boosting retail confidence.

- Finally, the sustained suv market dominance in passenger vehicles continues to shape production strategies and competitive dynamics, forcing all players to innovate within this high-volume segment. This has led to a market where retail performance has improved by over 25% year-on-year, underscoring the resilience and growth potential of the sector.

What are the key market drivers leading to the rise in the adoption of India Automotive Industry?

- The integration of SUVs and the industrialization of premium lifestyle mobility solutions are primary drivers of market growth.

- The expansion of alternative powertrain ecosystems is a primary market driver, fostering green powertrain diversity and promoting sustainable mobility.

- This is particularly evident in the development of electric drivetrain components and the rollout of high-power DC fast chargers to support them.

- While heavy-duty applications continue to rely on advanced diesel technology, the market for electric light commercial vehicles is expanding, driven by the automotive mission plan.

- The rise of premium lifestyle mobility is reshaping consumer expectations, while the growth of shared mobility solutions offers an alternative to personal vehicle ownership, influencing overall sales strategies.

- The adoption of these new mobility frameworks has led to a 15% increase in vehicle utilization rates in urban centers.

What are the market trends shaping the India Automotive Industry?

- A key trend is the institutionalization of affordable electrification. This marks a strategic shift toward mass-market adoption of electric vehicles.

- The market is undergoing a significant transition from traditional internal combustion engines (ICE) to advanced battery-electric vehicle (BEV) platforms and sophisticated hybrid powertrains. This shift is driven by a move toward the software-defined vehicle (SDV) architecture, enabling features like advanced driver-assistance systems (ADAS) to become mainstream.

- This evolution necessitates a global supply chain realignment, encouraging domestic value addition and local manufacturing. Consequently, indigenous battery pack assembly has seen a growth of over 40% in capacity, reducing dependency on external markets. The strategic emphasis on component localization is critical for improving production efficiency and cost structures across the board.

What challenges does the India Automotive Industry face during its growth?

- A critical challenge is the crisis of urban grid readiness, compounded by an execution gap in high-power charging infrastructure.

- Key challenges stem from the need to improve urban grid readiness to support the transition toward zero-emission vehicles. Original equipment manufacturers (OEMs) and component suppliers face pressure to innovate in autonomous vehicle technology while navigating complex regulatory compliance. The threat of trade protectionism adds another layer of complexity for global players.

- Furthermore, the push for mass-market EV adoption and premiumization across segments requires significant investment in technology and infrastructure. Organized retail dealerships must adapt their business models to handle these new product categories and consumer expectations. A failure to align with these shifts can increase operational risks by up to 25% for established players.

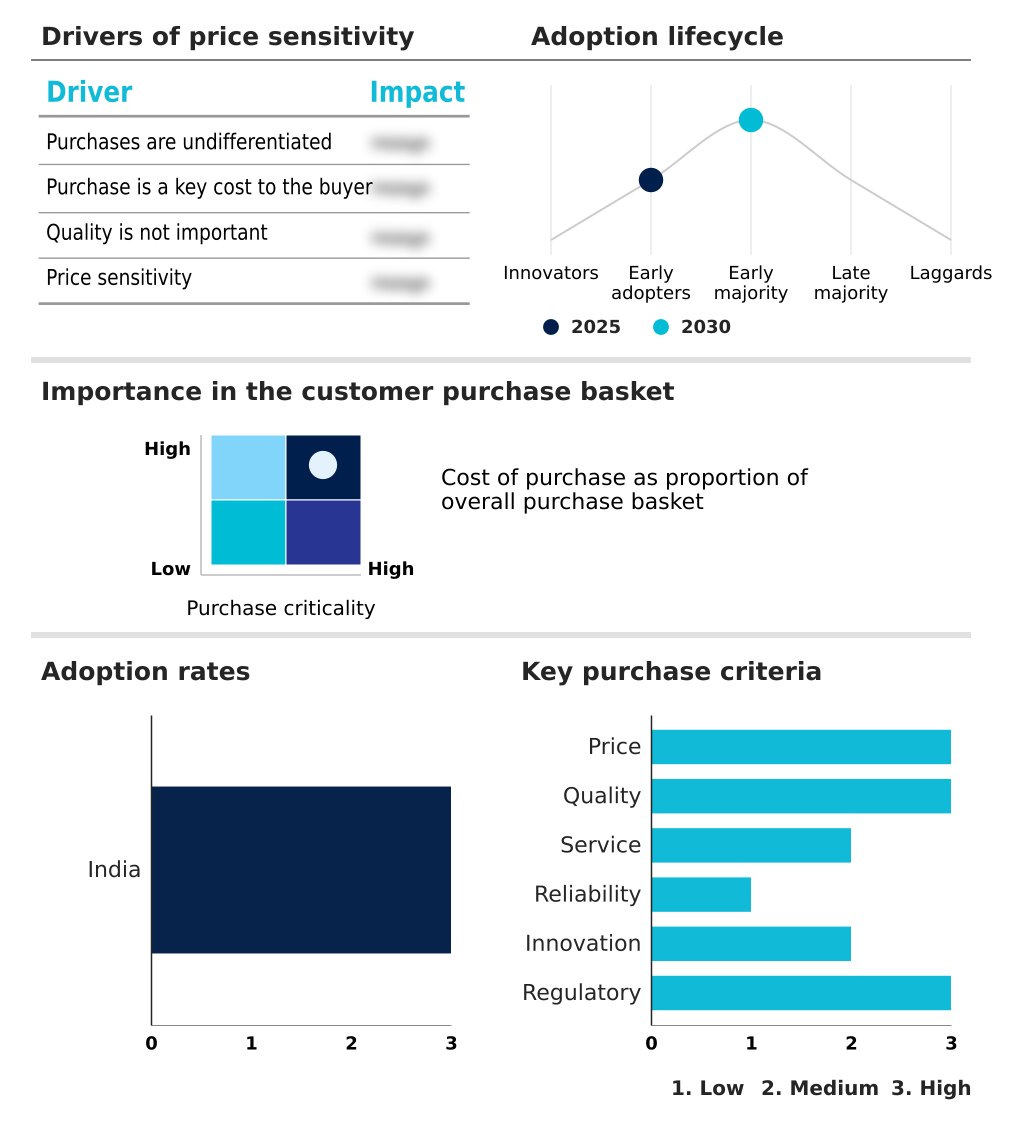

Exclusive Technavio Analysis on Customer Landscape

The india automotive market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the india automotive market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of India Automotive Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, india automotive market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ashok Leyland Ltd. - Key offerings include advanced engineering in commercial and passenger vehicles, focusing on global technology, durability, and innovative design for diverse market needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ashok Leyland Ltd.

- Bajaj Auto Ltd.

- Bayerische Motoren Werke AG

- Daimler Truck AG

- Eicher Motors Ltd.

- Force Motors Ltd.

- Ford Motor Co.

- General Motors Co.

- Hero Motors Ltd.

- Hinduja Group Ltd.

- Honda Motor Co. Ltd.

- Hyundai Motor Co.

- Mahindra and Mahindra Ltd.

- Mercedes Benz Group AG

- Nissan Motor Co. Ltd.

- Renault SAS

- Tata Motors Ltd.

- Toyota Motor Corp.

- TVS Motor Co.

- Volkswagen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in India automotive market

- In January, 2026, Maruti Suzuki made a significant move into the electric SUV segment with the full-scale commercial launch of the e Vitara, aiming to address consumer concerns with its extensive domestic service network.

- In February, 2026, Maruti Suzuki India Ltd. reported record monthly sales, a performance supported by its growing market share in the mid-sized SUV category and the commissioning of new manufacturing lines.

- In March, 2026, Ashok Leyland Ltd. initiated the construction of a new battery pack manufacturing facility with a substantial investment, aiming to localize critical EV components and reduce import dependency.

- In March, 2026, Tata Motors Ltd. saw overwhelming consumer response, with bookings for its new Sierra SUV surpassing the one hundred thousand unit mark, highlighting strong demand in the sport utility vehicle segment.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled India Automotive Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 189 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.5% |

| Market growth 2026-2030 | USD 51759.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.5% |

| Key countries | India |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive market in India is undergoing a significant transformation, characterized by the dual-focus on upgrading internal combustion engines (ICE) and accelerating the adoption of battery-electric vehicle (BEV) platforms. The rise of the software-defined vehicle (SDV) is compelling original equipment manufacturers (OEMs) to rethink their value chain, from component suppliers to organized retail dealerships.

- Integrating advanced driver-assistance systems (ADAS) and diverse hybrid powertrains has become standard practice to meet consumer demand and regulatory pressures. For boardroom consideration, the strategic decision to invest in proprietary powertrain engineering for green mobility solutions is critical, as it directly impacts long-term competitiveness and compliance.

- Success in this evolving landscape requires a holistic approach, encompassing not just vehicle manufacturing but also robust vehicle-related financing and strategies to mitigate supply chain volatility. Companies that have vertically integrated their electric mobility ecosystem have reported a reduction in time-to-market by over 20% for new electric models, showcasing a tangible business advantage.

What are the Key Data Covered in this India Automotive Market Research and Growth Report?

-

What is the expected growth of the India Automotive Market between 2026 and 2030?

-

USD 51.76 billion, at a CAGR of 6.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Two-wheelers, Passenger cars, Commercial vehicles, and Three-wheelers), Fuel Type (Diesel, Petrol, CNG and LPG, and Electric), Distribution Channel (Offline, and Online) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Integration of SUV and industrialization of premium lifestyle mobility solutions, Crisis of urban grid readiness and execution gap in high-power charging infrastructure

-

-

Who are the major players in the India Automotive Market?

-

Ashok Leyland Ltd., Bajaj Auto Ltd., Bayerische Motoren Werke AG, Daimler Truck AG, Eicher Motors Ltd., Force Motors Ltd., Ford Motor Co., General Motors Co., Hero Motors Ltd., Hinduja Group Ltd., Honda Motor Co. Ltd., Hyundai Motor Co., Mahindra and Mahindra Ltd., Mercedes Benz Group AG, Nissan Motor Co. Ltd., Renault SAS, Tata Motors Ltd., Toyota Motor Corp., TVS Motor Co. and Volkswagen AG

-

Market Research Insights

- Market dynamics are increasingly influenced by a structural realignment toward affordable electrification and the expansion of green powertrain diversity. This transition is catalyzed by domestic manufacturers launching dedicated electric platforms designed for local conditions, moving electric vehicles into the mainstream.

- The market's self-sustaining growth, driven by economies of scale and indigenous battery pack assembly, contrasts with regions reliant on government subsidies. A focus on improving real-world range addresses the needs of a growing middle class, while the proliferation of affordable electric SUVs makes sustainable mobility a central pillar of long-term industrial strategy.

- Retail sales have surged, with rural markets exhibiting a remarkable 34% year-on-year growth compared to 21% in urban areas, reflecting a fundamental shift in consumer demand and the success of localized strategies.

We can help! Our analysts can customize this india automotive market research report to meet your requirements.

RIA -

RIA -