Hypervisor Market Size 2026-2030

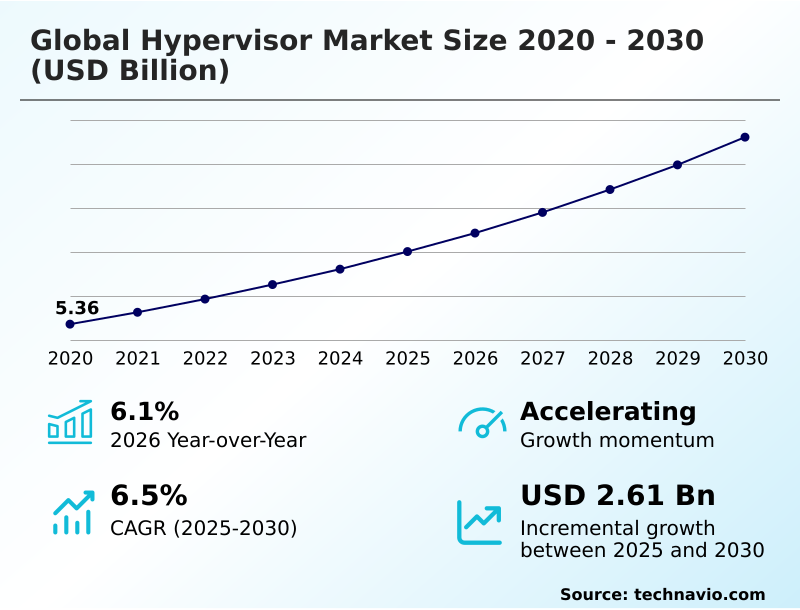

The hypervisor market size is valued to increase by USD 2.61 billion, at a CAGR of 6.5% from 2025 to 2030. Pervasive proliferation of cloud computing and server virtualization will drive the hypervisor market.

Major Market Trends & Insights

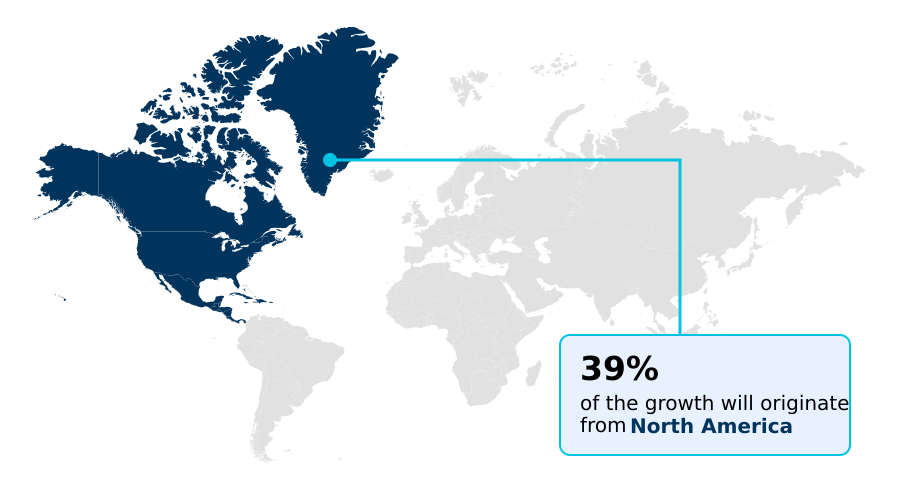

- North America dominated the market and accounted for a 38.9% growth during the forecast period.

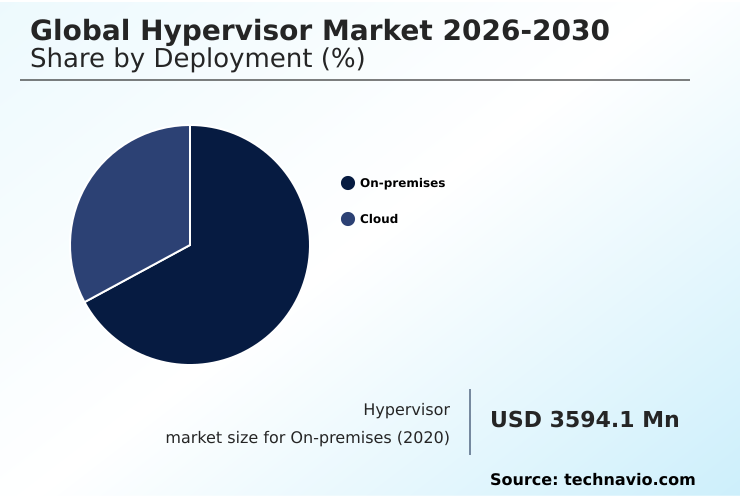

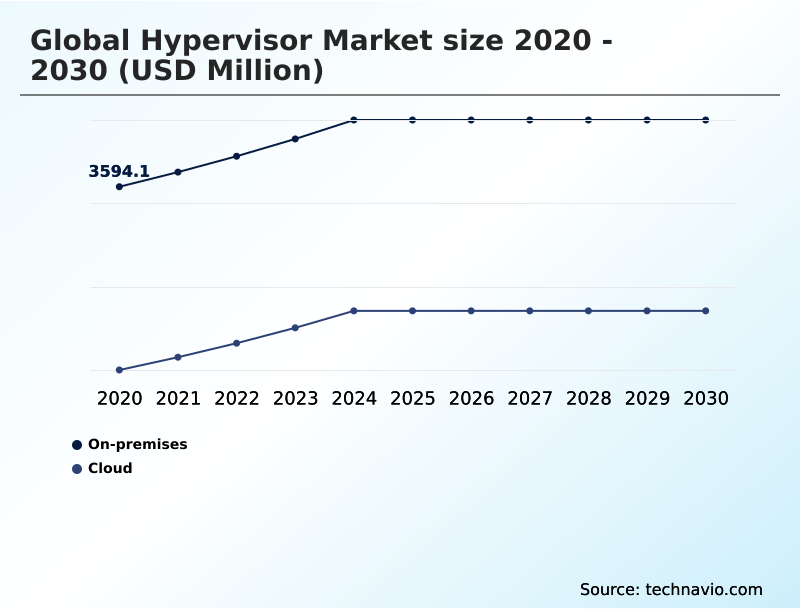

- By Deployment - On-premises segment was valued at USD 4.26 billion in 2024

- By Product - Large enterprises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.26 billion

- Market Future Opportunities: USD 2.61 billion

- CAGR from 2025 to 2030 : 6.5%

Market Summary

- The hypervisor market remains a cornerstone of modern IT infrastructure, enabling the efficiency and agility required for digital transformation. As the foundational technology for server consolidation, it allows organizations to maximize hardware utilization, leading to significant reductions in capital and operational expenditures.

- The evolution of this market is shaped by the relentless drive toward hybrid and multi-cloud environments, demanding solutions that offer seamless workload portability and consistent management across disparate platforms. Key trends include the integration of AI-driven analytics for dynamic resource allocation and the rise of lightweight hypervisors optimized for edge computing deployments.

- A typical business scenario involves a financial services firm leveraging a bare-metal hypervisor to run high-frequency trading applications alongside legacy systems on the same hardware, ensuring workload isolation and compliance with strict regulatory standards through features like microsegmentation.

- However, the market also faces challenges from the growing adoption of containerization as a substitute for some workloads and navigating complex virtualization licensing models, which pushes enterprises to evaluate their total cost of ownership and explore multi-hypervisor strategies.

What will be the Size of the Hypervisor Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Hypervisor Market Segmented?

The hypervisor industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- On-premises

- Cloud

- Product

- Large enterprises

- SMEs

- Component

- Hardware

- Software

- Service

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

The on-premises deployment model remains central, affording enterprises complete on-premises virtualization control over their private cloud infrastructure. This approach is critical for virtualization for mission-critical apps in regulated industries where data sovereignty and strict workload isolation are non-negotiable.

By deploying a type-1 hypervisor directly on owned hardware, organizations achieve unparalleled security through features like secure boot capabilities and superior performance for demanding applications.

This model facilitates deep hardware customization, enabling optimized configurations for guest operating systems and achieving predictable performance, which can reduce application latency by over 20%.

The foundation of resource abstraction through network virtualization and storage virtualization allows for efficient server consolidation and robust virtualization policy enforcement within the corporate firewall.

The On-premises segment was valued at USD 4.26 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Hypervisor Market Demand is Rising in North America Request Free Sample

North America currently accounts for 38.92% of the market's incremental growth, driven by advanced adoption of the hybrid cloud operating model and investments in hyperconverged infrastructure. Enterprises in the region heavily leverage live migration and high-availability clustering for resilience.

Europe, with a regional growth rate of 6.1%, emphasizes data sovereignty, reinforcing demand for strong on-premises virtualization control.

APAC is a close second in growth, fueled by digitalization and demand for a hypervisor for big data analytics, pushing virtual machine density to new limits. The region sees increased use of multi-tenancy in its cloud services.

This dynamic landscape shows a global push for efficient disaster recovery orchestration and experimentation with technologies like nested virtualization.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The Global Hypervisor Market 2026-2030 for enterprise data centers is mature, focusing on performance and evaluating hypervisor total cost of ownership. In contrast, the Global Hypervisor Market 2026-2030 for edge computing demands lightweight, resilient solutions. A key debate is the Global Hypervisor Market 2026-2030 vs container orchestration, though many use both in hybrid models.

- Navigating the Global Hypervisor Market 2026-2030 licensing and TCO is a major challenge, spurring a cost-benefit analysis of open-source hypervisors. The future lies with the Global Hypervisor Market 2026-2030 with hardware acceleration, as DPUs and SmartNICs offload tasks. Organizations are also scrutinizing the Global Hypervisor Market 2026-2030 security and isolation capabilities.

- This makes choosing a hypervisor for private cloud a critical decision. Many are now managing multi-hypervisor environments effectively to avoid lock-in. The hypervisor role in AI and ML workloads is growing, requiring advanced scheduling. Security teams are focused on securing virtual machines from lateral movement. Development teams are automating vm deployment with iac tools.

- For end-user computing, hypervisor considerations for vdi deployments are paramount. For industrial use, hypervisor requirements for real-time systems are strict. Performance is also key, leading to hypervisor performance benchmarking for databases and work on optimizing network performance in virtual environments. Finally, achieving compliance with hypervisor security controls is essential, driving the need for better hypervisor integration with cloud management platforms.

- In fact, firms that fully automate compliance checks within their platforms report audit preparation times that are over 50% faster than those using manual processes.

What are the key market drivers leading to the rise in the adoption of Hypervisor Industry?

- The pervasive proliferation of cloud computing and server virtualization technologies is the single most influential driver propelling the market's expansion.

- The primary market driver is the economic imperative for server consolidation and virtualization cost optimization, which can reduce data center hardware footprints by up to 60%. This is enabled by the fundamental resource abstraction that hypervisors provide.

- The adoption of hyperconverged infrastructure further accelerates this by simplifying the deployment of private cloud infrastructure. For enterprises running virtualization for mission-critical apps, the need for robust business continuity frameworks is a major catalyst.

- Features like high-availability failover within high-availability clustering and streamlined disaster recovery orchestration are indispensable. The demand for disaster recovery virtualization solutions has been shown to lower business downtime by over 75% during outages.

- Furthermore, workload portability is essential for enabling flexible hybrid cloud strategies and efficient multi-tenancy.

What are the market trends shaping the Hypervisor Industry?

- The strategic shift toward distributed edge architectures is a defining market trend, creating a significant demand for seamless workload portability across heterogeneous computing environments.

- Market trends are driven by the shift towards edge virtualization and IT/OT convergence, demanding lightweight hypervisors with small footprints. These platforms support a hypervisor for IoT workloads and real-time hypervisor use cases where low latency is critical.

- The integration of AI is enabling more sophisticated dynamic resource allocation and predictive CPU scheduling, with some platforms improving virtual machine density by over 15% without performance degradation. This intelligent hypervisor resource scheduling is crucial for cloud-native virtualization environments.

- Enhanced hypervisor security features are also a major trend, providing deep workload isolation needed to run mixed-criticality applications and emerging unikernel artifacts securely.

What challenges does the Hypervisor Industry face during its growth?

- Complex licensing models, challenges in cost governance, and difficulties in demonstrating a clear return on investment represent a primary challenge affecting market velocity.

- A significant challenge is navigating complex virtualization licensing models, which can obscure total cost of ownership and increase operational expenses by 20% or more if not managed properly. This complexity drives interest in a multi-hypervisor strategy, but this approach introduces its own issues, such as ensuring virtual machine image compatibility.

- Another challenge is managing hypervisor performance overhead, particularly in dense multi-tenant environments. The rise of container orchestration on VMs creates a new management layer, requiring strong hypervisor api integration and advanced tools.

- While infrastructure as code helps automate deployment, the technical debt of legacy systems and the difficulty of implementing advanced features like microsegmentation or nested virtualization across different platforms remains a hurdle for many IT teams.

Exclusive Technavio Analysis on Customer Landscape

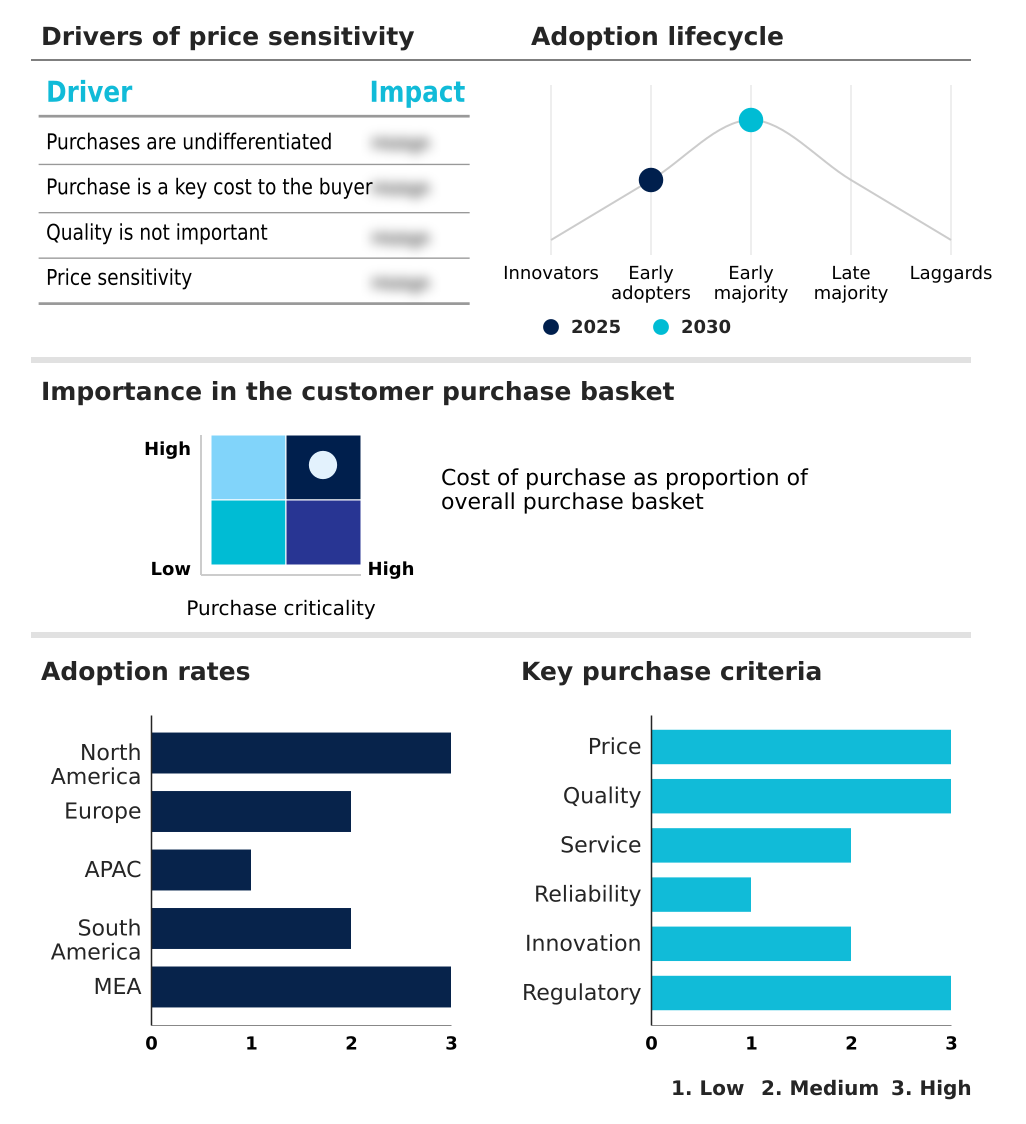

The hypervisor market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hypervisor market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Hypervisor Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, hypervisor market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

acontis technologies GmbH - Delivers a diverse portfolio of hypervisor solutions, including enterprise-grade virtualization, specialized real-time hypervisors, and embedded platforms for mixed-criticality systems, meeting diverse workload demands.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- acontis technologies GmbH

- Aptiv Plc

- BlackBerry Ltd.

- Broadcom Inc.

- Citrix Systems Inc.

- General Dynamics Corp.

- Green Hills Software LLC

- Hewlett Packard Entp Co.

- IBM Corp.

- Kernkonzept GmbH

- Lynx Software Technologies

- Microsoft Corp.

- NXP Semiconductors NV

- Oracle Corp.

- Parallels International GmbH

- Proxmox Server Solutions GmbH

- Scale Computing

- Siemens AG

- Thales Group

- Vates

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Hypervisor market

- In November, 2024, Broadcom Inc. completed its acquisition of VMware, subsequently announcing a strategic shift from perpetual licenses to a subscription-based model for its entire product portfolio.

- In February, 2025, Microsoft Corp. and Siemens AG announced an expanded partnership to integrate Azure Stack HCI's lightweight hypervisor capabilities with Siemens' industrial edge platform, aiming to accelerate IT/OT convergence.

- In March, 2025, the community behind the Xen Project released a new version of its hypervisor with significant security enhancements, including live patching capabilities and improved performance for ARM-based architectures.

- In April, 2025, the United States Department of Defense announced a landmark initiative to diversify its private cloud infrastructure by adopting a multi-hypervisor strategy to enhance operational resilience and mitigate vendor lock-in.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hypervisor Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.5% |

| Market growth 2026-2030 | USD 2607.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Spain, Italy, The Netherlands, China, Japan, India, South Korea, Australia, Singapore, Brazil, Argentina, Colombia, South Africa, Saudi Arabia, UAE, Turkey and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The hypervisor market's evolution is defined by a shift from basic server consolidation to enabling complex, automated IT ecosystems. The core technology, the virtual machine monitor, now supports everything from enterprise guest operating systems to emerging unikernel artifacts.

- Boardroom decisions increasingly weigh the benefits of a type-1 hypervisor or bare-metal hypervisor for performance against the flexibility of a hosted hypervisor (type-2 hypervisor). Advanced hardware-assisted virtualization is standard, with data processing units and smart network interface cards enabling superior network virtualization and storage virtualization. This resource abstraction is fundamental.

- Key trends include deploying lightweight hypervisors for edge virtualization and using a separation kernel for real-time hypervisor applications. Security is paramount, with virtual trusted platform modules and secure boot capabilities becoming standard for microsegmentation to prevent threats. For operations, live migration, dynamic resource allocation using techniques like memory overcommitment and cpu scheduling, and high-availability failover are critical.

- Modern management relies on infrastructure as code for zero-touch provisioning based on stable virtual device models. Hyperconverged infrastructure simplifies deployment, while nested virtualization supports complex lab environments. The focus is on increasing virtual machine density while ensuring robust disaster recovery orchestration and seamless workload portability. Organizations implementing zero-touch provisioning have reported a reduction in infrastructure deployment errors by over 90%.

What are the Key Data Covered in this Hypervisor Market Research and Growth Report?

-

What is the expected growth of the Hypervisor Market between 2026 and 2030?

-

USD 2.61 billion, at a CAGR of 6.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On-premises, and Cloud), Product (Large enterprises, and SMEs), Component (Hardware, Software, and Service) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Pervasive proliferation of cloud computing and server virtualization, Cost governance, licensing complexity, and lack of ROI proof

-

-

Who are the major players in the Hypervisor Market?

-

acontis technologies GmbH, Aptiv Plc, BlackBerry Ltd., Broadcom Inc., Citrix Systems Inc., General Dynamics Corp., Green Hills Software LLC, Hewlett Packard Entp Co., IBM Corp., Kernkonzept GmbH, Lynx Software Technologies, Microsoft Corp., NXP Semiconductors NV, Oracle Corp., Parallels International GmbH, Proxmox Server Solutions GmbH, Scale Computing, Siemens AG, Thales Group and Vates

-

Market Research Insights

- The modern hybrid cloud operating model requires a flexible multi-hypervisor strategy to achieve virtualization cost optimization while navigating complex virtualization licensing models. Effective virtualization management platforms are key for the automated infrastructure provisioning of private cloud infrastructure, supporting both virtualization for legacy applications and cloud-native virtualization.

- Prioritizing hypervisor security features ensures a secure multi-tenant architecture with proper workload isolation and virtualization policy enforcement. For virtualization for mission-critical apps, high-availability clustering and disaster recovery virtualization are essential. VDI hypervisor selection must account for hypervisor performance overhead, while a hypervisor for IoT workloads and a hypervisor for big data analytics need specialized hypervisor resource scheduling.

- Container orchestration on VMs on a bare-metal container platform shows the need for hypervisor ecosystem compatibility and virtual machine image compatibility. This is critical for IT/OT convergence, supporting virtual network functions and software-defined storage through robust hypervisor API integration. Some firms improve disaster recovery TCO by 45% using this model.

We can help! Our analysts can customize this hypervisor market research report to meet your requirements.

RIA -

RIA -