Hot Swap Controllers Market Size 2025-2029

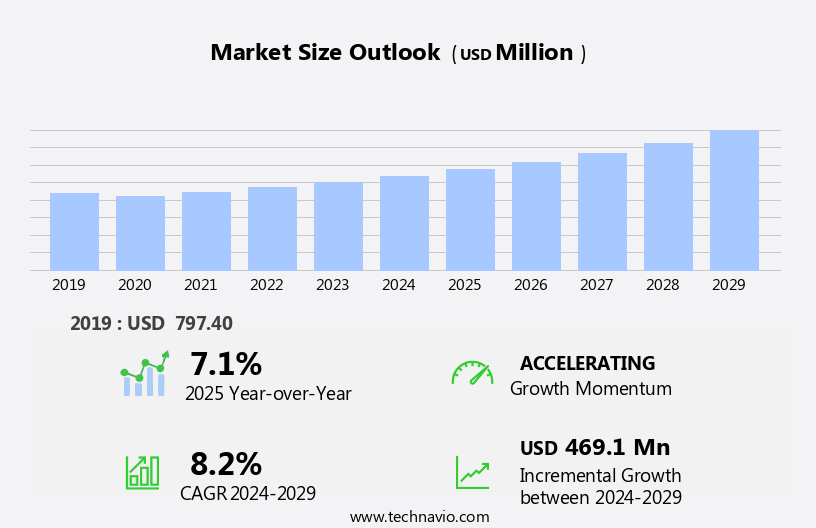

The hot swap controllers market size is forecast to increase by USD 469.1 million at a CAGR of 8.2% between 2024 and 2029.

- The market is witnessing significant growth, driven by the increasing expansion of hyperscale data center and the subsequent demand for reliable and efficient power management solutions. This trend is further fueled by the continuous launch of new products, which cater to the evolving needs of data-intensive industries. However, thermal management remains a persistent challenge for market participants. The intricacy of hot-swap controllers, which enable seamless power distribution and data transfer between components without disrupting the system, necessitates effective thermal management to prevent overheating and ensure optimal performance.

- As data centers continue to expand and the demand for uninterrupted power and data transfer increases, market players must address this challenge through innovative thermal management solutions. Companies that successfully navigate these dynamics will be well-positioned to capitalize on the market's potential and maintain a competitive edge. Physical security measures, such as patch management and emergency response procedures, are enhanced through the controllers' remote management tools.

What will be the Size of the Hot Swap Controllers Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The market is experiencing significant growth, driven by the increasing adoption of energy management process safety systems and the integration of hypervisor technology in data centers. This trend is evident in the proliferation of modular and containerized data centers, which require high levels of application load balancing, log management, and data center automation for optimal performance. Redundancy architectures, capacity management, and cloud-native applications are also key factors fueling market expansion.

- Performance monitoring and serverless functions are further enhancing the agility and efficiency of data center environments. In summary, the market is witnessing dynamic growth, fueled by the adoption of advanced energy management systems, hypervisor technology, and the increasing importance of data security policies in the context of modular and containerized data centers, cloud-native applications, and network virtualization. Market players must stay abreast of these trends to remain competitive and meet the evolving needs of US businesses. Data security policies are becoming increasingly important in the context of network virtualization and fault tolerance, as infrastructure monitoring, incident response, multi-factor authentication, data governance, and event management become essential components of robust data center operations.

How is this Hot Swap Controllers Industry segmented?

The hot swap controllers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Advanced

- High voltage

- Low voltage

- PCI

- Application

- Servers and storage systems

- Industrial control systems

- Network switches and routers

- Telecom base stations

- PDUs

- Industry Application

- Data centers

- Telecommunications

- Industrial automation

- Consumer electronics

- Healthcare equipment

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

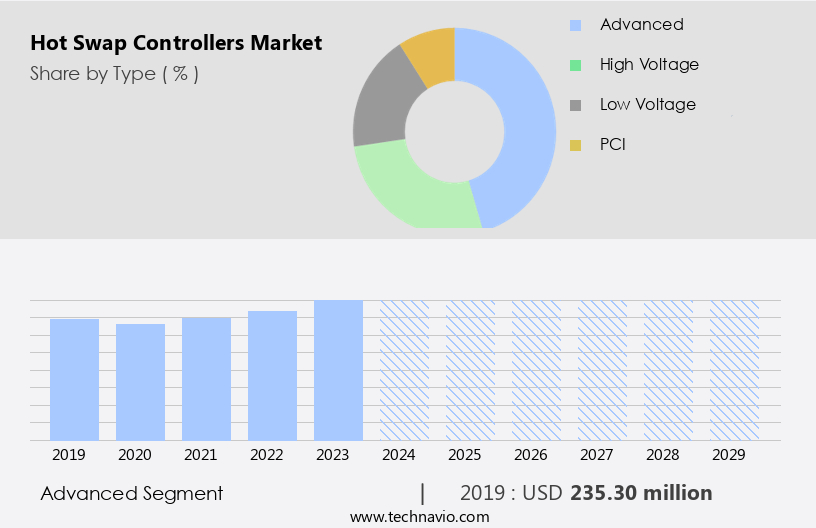

By Type Insights

The advanced segment is estimated to witness significant growth during the forecast period. Advanced hot swap controllers, characterized by digital telemetry and communication interfaces, are gaining traction in various industries due to their ability to enhance monitoring, control, and predictive maintenance capabilities. These controllers, which operate across a broad voltage range from 1 volt to 80 volts, are integral to mission-critical systems, reflecting the increasing importance of intelligent power management solutions. In the context of smart data centers, advanced hot swap controllers facilitate remote monitoring and control through interfaces like PMBus and SMBus. These features are crucial for managing power distribution in high-density server environments and promoting energy efficiency initiatives. Furthermore, these controllers are compatible with open standards, ensuring seamless integration with existing infrastructure.

Microservices architecture, network redundancy, operational efficiency, automated provisioning, and network segmentation are all optimized through the use of advanced hot swap controllers. Containerization technologies, data center certifications, and cloud computing services also benefit from their capabilities. Additionally, they support high availability clusters, disaster recovery solutions, and scalability and elasticity. Compliance and auditing, data encryption, and software compatibility are maintained through rigorous testing and system failover procedures. Raid configurations, redundant power supplies, and capacity planning are optimized for improved performance and power consumption.

Overall, the advanced market reflects the evolving trends towards intelligent power management, energy efficiency, and real-time system optimization.

The Advanced segment was valued at USD 235.30 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

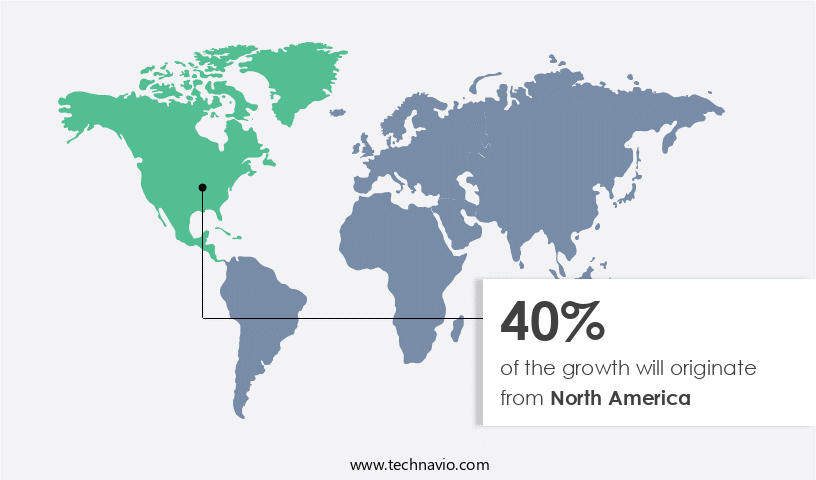

North America is estimated to contribute 40% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the rapidly evolving digital landscape, North America is experiencing significant growth in sectors such as digital infrastructure, advanced manufacturing, and clean mobility. This transformation is driving the demand for hot swap controllers, which play a crucial role in ensuring continuous power delivery and safe system maintenance in high-availability environments, including data centers, telecom networks, electric vehicles, and industrial automation. The region's investments in 5G, AI infrastructure, EV production, and electronics manufacturing are fostering a thriving ecosystem where hot swap technology is increasingly becoming indispensable. In the telecom sector, major service providers like Verizon, AT&T, and T-Mobile are leading the charge in 5G base station deployment, with leading equipment companies such as Ericsson, Nokia, Samsung, and Huawei vying for infrastructure contracts.

Hot swap controllers are also gaining traction in data centers, where they enable operational efficiency, network redundancy, and automated provisioning. Microservices architecture, containerization technologies, and virtualization platforms are further enhancing the flexibility and scalability of these data centers. Environmental control units, network segmentation, and compliance and auditing are essential considerations for businesses seeking to ensure data security and regulatory compliance. Meanwhile, cloud computing services, business continuity planning, and disaster recovery solutions are becoming increasingly important as companies prioritize operational resilience and business continuity. As businesses strive for operational efficiency and sustainability, green data centers and edge computing are gaining popularity.

These approaches help reduce energy consumption, improve performance optimization, and enhance disaster recovery capabilities. Physical security measures, patch management, and emergency response procedures are also critical components of a robust IT infrastructure. Hardware interoperability, remote management tools, and capacity planning are essential for ensuring seamless integration and efficient utilization of resources. In the context of evolving technology trends, hot swap controllers offer numerous benefits, including improved system reliability, reduced downtime, and enhanced system flexibility. As businesses continue to prioritize operational efficiency, sustainability, and regulatory compliance, the demand for hot swap controllers is expected to remain strong.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Hot Swap Controllers market drivers leading to the rise in the adoption of Industry?

- Data center expansion serves as the primary catalyst for market growth, as organizations continue to invest in infrastructure to support increasing digital transformation initiatives and accommodate rising data demands. The market is experiencing significant growth due to the increasing demand for edge computing and high-density data center infrastructure. These facilities require advanced power management solutions that enable live maintenance of power modules, storage devices, and compute accelerators without system downtime. Hot swap controllers play a vital role in ensuring uninterrupted operation in mission-critical environments, such as those supporting high-density GPU clusters and advanced networking infrastructure. Amazon Web Services' recent USD10 billion investment in AI-focused data centers in North Carolina is a testament to this trend. These data centers will support advanced networking infrastructure and high-density GPU clusters, making hot swap controllers essential for managing power delivery and protecting sensitive components during upgrades or replacements.

- Moreover, virtualization platforms, performance optimization, vulnerability assessment, high availability clusters, compliance and auditing, system failover testing, software upgrade cycles, and sustainable practices are other factors driving the market's growth. Hot swap controllers enable businesses to optimize their power usage, reduce downtime, and maintain compliance with industry regulations. The market is expected to continue its growth trajectory, driven by the expanding data center infrastructure and the need for robust, modular, and serviceable power management solutions. Hot swap controllers' ability to enable live maintenance and protect sensitive components during upgrades or replacements makes them an indispensable component of modern data centers.

What are the Hot Swap Controllers market trends shaping the Industry?

- The focus on new product launches is currently a significant trend in the market. It is essential for businesses to stay informed and prepared for introducing innovative offerings to remain competitive. The market is experiencing significant growth due to the increasing demand for hardware interoperability and remote management tools in data center infrastructure, cloud computing services, and business continuity planning. Semiconductor manufacturers are responding by introducing advanced products that cater to high-performance computing and networking environments. For instance, Infineon Technologies recently launched the XDP711-001, a 48-volt hot swap controller, as part of its XDP digital protection family.

- Moreover, the trend toward serverless computing and software compatibility necessitates the adoption of energy-efficient hot swap controllers with high data recovery test and measurement capabilities. Physical security measures, patch management, and software compatibility are other essential factors driving market growth. As companies prioritize energy efficiency and business continuity planning, the market is expected to continue its expansion. Designed for high-power AI servers, this controller supports power delivery boards up to 8 kilowatts and offers precise voltage and current monitoring, digital safe operating area (SOA) control, and the ability to drive multiple MOSFETs in parallel.

How does Hot Swap Controllers market face challenges during its growth?

- The growth of the industry is significantly impacted by thermal management issues, which pose a significant challenge that necessitates innovative solutions. Hot swap controllers play a crucial role in managing the safe insertion and removal of components under live conditions, particularly in high-density environments such as data centers, telecommunications racks, and industrial automation systems. These controllers are essential for DevOps integration and disaster recovery solutions, enabling emergency response procedures and ensuring business continuity. However, thermal management remains a significant challenge due to the compact and power-dense nature of modern electronic systems. The generation of heat during hot swap operations can degrade performance, reduce reliability, and lead to premature component failure. In close-proximity installations, thermal hotspots can complicate heat dissipation, limiting airflow and increasing power consumption.

- To address these challenges, hot swap controllers are being designed with advanced features such as data encryption, RAID configurations, redundant power supplies, scalability and elasticity, power consumption optimization, and disaster recovery drills. These features ensure efficient heat dissipation, enhanced system reliability, and improved overall performance. Additionally, capacity planning and disaster recovery solutions are being integrated into hot swap controller systems to minimize downtime and ensure business continuity in the event of power outages or other emergencies.

Exclusive Customer Landscape

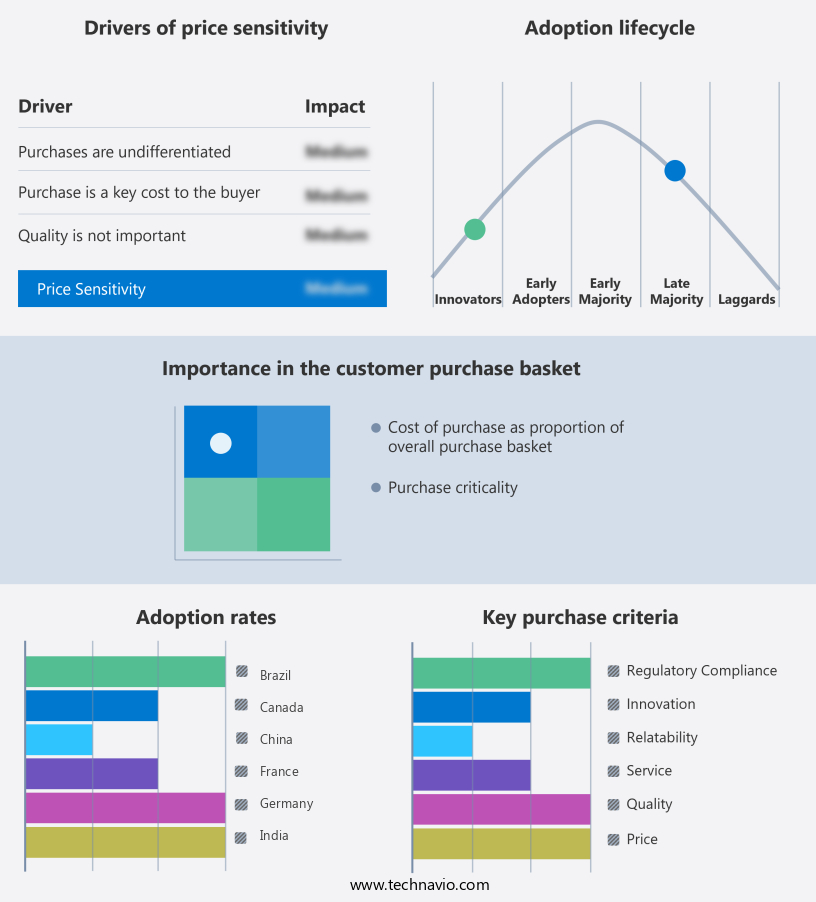

The hot swap controllers market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hot swap controllers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, hot swap controllers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Allegro MicroSystems Inc. - The company specializes in hot swap controllers, including the ACS761ELFTR-20B-T model.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Allegro MicroSystems Inc.

- Alpha and Omega Semiconductor Ltd.

- Analog Devices Inc.

- Diodes Inc.

- Infineon Technologies AG

- Microchip Technology Inc.

- Monolithic Power Systems Inc.

- ON Semiconductor Corp.

- Renesas Electronics Corp.

- Richtek Technology Corp.

- ROHM Co. Ltd.

- Semtech Corp.

- STMicroelectronics NV

- Texas Instruments Inc.

- Vicor Corp.

- Vishay Intertechnology Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Hot Swap Controllers Market

- In February 2023, Schneider Electric, a global energy management and automation company, announced the launch of its new Masterpact MTZ Hot Swap UPS System. This innovative solution allows for the hot swap of power modules without the need for maintenance bypass switches, reducing downtime and improving data center efficiency (Schneider Electric Press Release, 2023).

- In March 2024, ABB, a leading technology provider, entered into a strategic partnership with Microsoft to integrate ABB's Ability⢠Electrical Distribution Control System with Microsoft Azure. This collaboration enables real-time monitoring and predictive maintenance of electrical distribution networks, enhancing grid resilience and efficiency (ABB Press Release, 2024).

- In May 2024, Delta Electronics, a global power and thermal management solutions provider, acquired Power Control Corporation, a US-based manufacturer of power protection equipment. This acquisition strengthened Delta's position in the North American market and expanded its product offerings, particularly in the hot swap controller segment (Delta Electronics Press Release, 2024).

- In January 2025, the European Union passed the new Ecodesign Regulation for external power supplies. This regulation sets minimum energy efficiency requirements for hot swap controllers and other power supplies, driving innovation and market growth in energy-efficient solutions (European Commission Press Release, 2025).

Research Analyst Overview

The market continues to evolve, driven by the dynamic needs of various sectors. These controllers play a crucial role in ensuring hardware interoperability and operational efficiency in data centers, cloud computing environments, and business continuity planning. Remote management tools and network redundancy are essential features, enabling seamless integration of containerization technologies, microservices architecture, and virtualization platforms. Data center certifications, green data centers, and edge computing are gaining traction, as businesses prioritize operational efficiency and sustainability. Failover mechanisms and virtualization platforms ensure high availability clusters, while compliance and auditing, system failover testing, and software upgrade cycles are integral to maintaining security and reliability.

Energy efficiency ratings and software compatibility are critical considerations in the age of serverless computing and server blade systems. Physical security measures, patch management, and data recovery testing are essential components of disaster recovery solutions, ensuring business continuity in the face of unexpected events. DevOps integration, data encryption, and emergency response procedures further enhance the resilience of IT infrastructure. The market's continuous unfolding is marked by the integration of open standards compliance, network segmentation, performance optimization, and vulnerability assessment. Redundant power supplies, scalability and elasticity, and disaster recovery drills are also key elements shaping the market's evolution.

Power consumption optimization and capacity planning are increasingly important as businesses strive for optimal resource utilization.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hot Swap Controllers Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

250 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.2% |

|

Market growth 2025-2029 |

USD 469.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.1 |

|

Key countries |

US, China, Japan, South Korea, Germany, India, UK, Brazil, France, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Hot Swap Controllers Market Research and Growth Report?

- CAGR of the Hot Swap Controllers industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the hot swap controllers market growth of industry companies

We can help! Our analysts can customize this hot swap controllers market research report to meet your requirements.

RIA -

RIA -