Heavy Construction Equipment Market Size 2025-2029

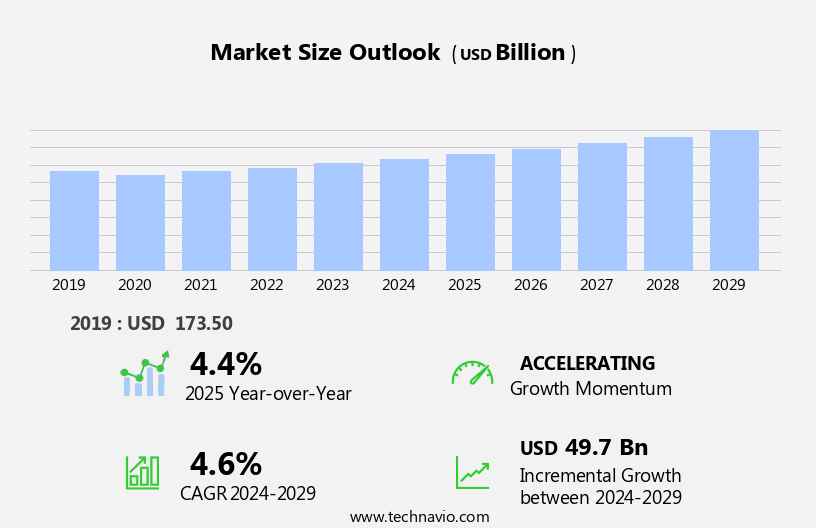

The heavy construction equipment market size is forecast to increase by USD 49.7 billion at a CAGR of 4.6% between 2024 and 2029.

- The market is experiencing significant growth, driven by increased investment in infrastructure projects worldwide. This trend is expected to continue, creating lucrative opportunities for market participants. Fuel alternatives, including diesel engines and hydraulic systems, are essential components of heavy construction machinery. The secondhand machine market is also expanding, providing an affordable alternative for companies seeking to acquire equipment without the high upfront costs of new machinery.

- Strategic partnerships, innovation, and operational efficiency are essential for success in the market. However, challenges persist in the form of intense competition, increasing raw material prices, and regulatory compliance, which may impact profitability. Companies must navigate these challenges effectively to capitalize on the market's potential and maintain a competitive edge. Manufacturing processes incorporate advanced engineering and quality control measures, while supply chain efficiency is enhanced through fleet management and raw materials sourcing strategies. Technological advances, including the adoption of battery technology, telematics, and automation, are driving innovation and improving efficiency, safety, and sustainability in the industry.

What will be the Size of the Heavy Construction Equipment Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- In the market, product lifecycle management plays a crucial role in ensuring optimal performance and longevity of machinery. Dealers maintain a robust network to provide site preparation services, monitoring systems, parts distribution, and project management solutions. Equipment financing options facilitate the acquisition of new machinery, while used equipment market participation offers cost-effective alternatives. Control valves, hydraulic pumps, and braking system components are essential components undergoing rigorous compliance testing to meet industry standards. Safety systems and operator interface design are increasingly prioritized for worksite logistics and demolition techniques.

- Customer service, spare parts supply, and technical support are integral to maintaining a competitive edge. Certification bodies and training programs ensure adherence to safety and standards compliance, while field testing and compliance testing are critical aspects of the product development cycle. The integration of monitoring systems and technical support enhances overall equipment performance and reliability. Another key driver is the growing trend of construction equipment rentals, which offers flexibility and cost savings for businesses.

How is this Heavy Construction Equipment Industry segmented?

The heavy construction equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

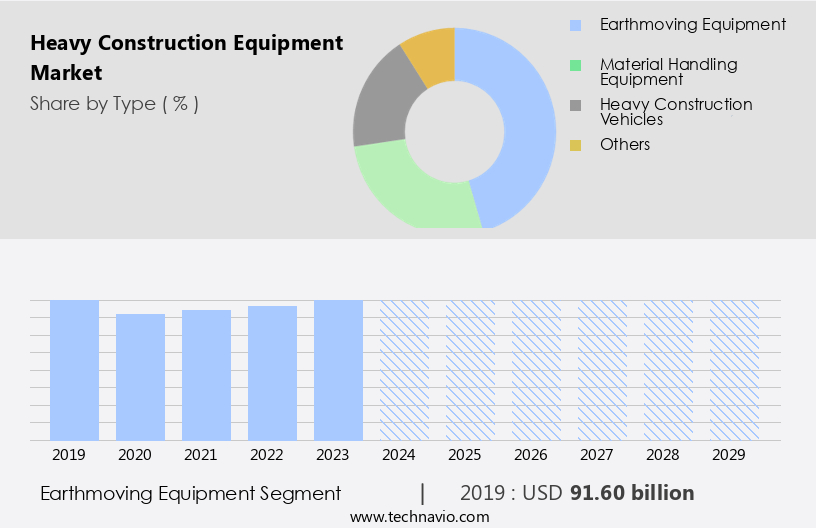

- Earthmoving equipment

- Material handling equipment

- Heavy construction vehicles

- Others

- Application

- Excavation and demolition

- Heavy lifting

- Material handling

- Tunneling

- Others

- Propulsion

- ICE

- Electric

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The earthmoving equipment segment is estimated to witness significant growth during the forecast period. The market encompasses machinery utilized for carrying, digging, spreading, or moving earth and materials. Key equipment in this sector includes excavators, loaders, dozers, and motor graders. Operating costs are a significant consideration for businesses in this industry, making aftermarket parts essential for maintaining equipment and maximizing return on investment. Software solutions and IoT sensors enhance machine performance and efficiency, while electric motors and remote control capabilities offer environmental benefits and increased safety. Infrastructure projects, driven by both public and private investment, provide opportunities for growth. Rapid urbanization, particularly in developing countries like China and India, is increasing the demand for heavy construction equipment due to the emergence of megacities.

Safety regulations and rental services ensure accessibility to various businesses. Transmission systems, lifting capacity, GPS guidance, and emission standards are crucial performance metrics. Specialized tools, such as dump trucks, are integral to material handling and land clearing. Maintenance contracts and fuel efficiency are essential for minimizing downtime and reducing operational costs. Cab comfort and emission reduction technologies are prioritized for operator training and environmental impact considerations. Braking systems and waste management systems are essential safety features. Construction sites rely on these machines to optimize productivity and efficiency.

The Earthmoving equipment segment was valued at USD 91.60 billion in 2019 and showed a gradual increase during the forecast period.

The Heavy Construction Equipment Market is expanding steadily, driven by rising infrastructure demands and technological advancements. Dump truck remain essential for material transportation, valued for their durability and adaptability across terrains. Contractors increasingly focus on minimizing operating cost by selecting machines with optimized fuel efficiency and longer service intervals. Payload capacity plays a crucial role in productivity, influencing the speed and scale of operations. High engine power is another critical factor, ensuring equipment can handle demanding tasks with ease. Additionally, operating weight affects machine stability and ground pressure, both of which are vital in varied site conditions. The growing use of auxiliary attachments further enhances equipment versatility, allowing one machine to perform multiple tasks and improving return on investment.

The Heavy Construction Equipment Market is evolving with cutting-edge innovations aimed at improving efficiency, safety, and sustainability. Advancements in engine technology are enhancing fuel economy and reducing emissions, aligning with global environmental standards. Sophisticated steering system now offer better maneuverability, especially in tight or rugged job sites. Modern display panels provide operators with real-time diagnostics and intuitive controls, boosting productivity and reducing downtime. A strong dealer network plays a pivotal role in after-sales service, spare parts availability, and technical support, influencing purchase decisions. Additionally, the focus on waste disposal solutions is growing, with equipment increasingly tailored to handle debris responsibly and sustainably.

Regional Analysis

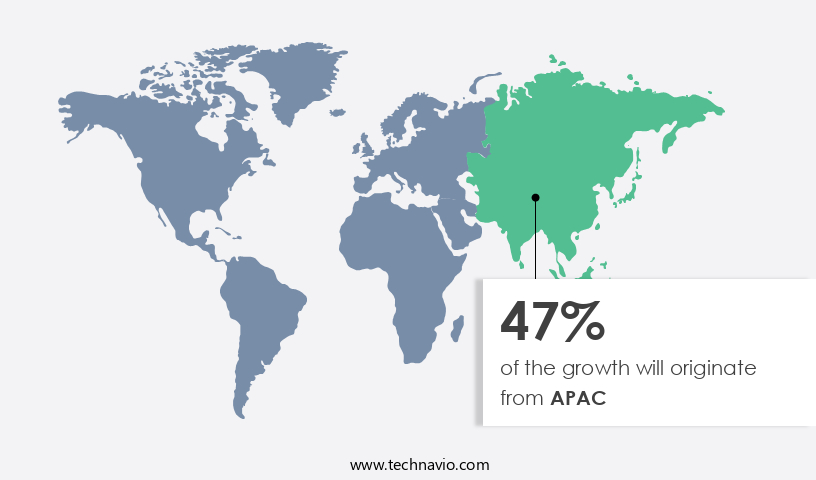

APAC is estimated to contribute 47% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in the APAC region is witnessing significant growth, driven by an increase in infrastructure projects such as roads, dams, and airports. China, India, and Japan are key contributors to this expansion, with global manufacturers setting up operations in response to the promising business opportunities. The construction sector's growth is further fueled by rising demand in emerging nations, particularly in the residential and commercial sectors. With steady growth projected, the region's construction market is expected to drive new infrastructure development, catering to the needs of a growing urban population. Moreover, the integration of IoT sensors, software solutions, and data analytics in heavy construction equipment is revolutionizing the industry.

Electric motors, remote control, and emission reduction technologies are becoming increasingly popular, with a focus on fuel efficiency and environmental impact. Operating costs are being optimized through lease agreements, maintenance contracts, and component parts. Operator training, safety regulations, and specialized tools ensure optimal performance and safety. Lifting capacity, transmission systems, and braking systems are essential features, while cab comfort and emission standards are key considerations for manufacturers. The market in APAC is experiencing robust growth, driven by infrastructure projects, rising construction activity, and technological advancements. The integration of IoT sensors, software solutions, and data analytics is transforming the industry, with a focus on reducing operating costs, improving performance metrics, and minimizing environmental impact.

The market's evolving trends include the adoption of electric motors, remote control, and emission reduction technologies, as well as the growing popularity of fuel alternatives and specialized tools.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Heavy Construction Equipment market drivers leading to the rise in the adoption of Industry?

- A significant increase in infrastructure investment serves as the primary catalyst for market growth. The market is experiencing significant growth due to increased investment in infrastructure projects worldwide. Governments and private entities are allocating substantial resources to modernize outdated systems, stimulate economic growth, and enhance competitiveness. In the US, the proposed infrastructure plan aims to invest over USD 2 trillion in rebuilding roads, bridges, airports, and public transit, as well as upgrading water systems and expanding broadband access. Meanwhile, China's Belt and Road Initiative and Made in China 2025 strategy are driving demand for heavy equipment in Asia, Africa, and Europe, with a focus on improving connectivity and advancing manufacturing infrastructure. Safety regulations are a crucial factor in the market, ensuring the protection of operators and workers.

- Rental services provide flexibility for businesses, allowing them to lease equipment with varying engine powers and lifting capacities as needed. Component parts and transmission systems require regular maintenance and replacement, creating opportunities for suppliers. Data analytics and operator training are essential for optimizing equipment performance and reducing downtime. The market is thriving due to the increasing demand for infrastructure development and modernization projects. Safety regulations, rental services, component parts, data analytics, operator training, and transmission systems are key market dynamics shaping the industry's growth.

What are the Heavy Construction Equipment market trends shaping the Industry?

- The increasing popularity of construction equipment rentals represents a significant market trend. This trend is driven by the numerous benefits it offers, including cost savings, flexibility, and access to the latest technology. The market experiences continuous growth due to the increasing trend of equipment rental services. Renting heavy construction equipment offers numerous advantages to businesses, such as flexibility, cost savings, and access to advanced technology without substantial upfront investments. With rental services, companies can adapt to their equipment requirements according to specific projects and scale operations efficiently.

- Additionally, the exploration of fuel alternatives, such as hybrid and electric engines, and the development of advanced hydraulic, braking, and waste management systems contribute to the market's expansion. Overall, the market's growth is driven by the evolving needs of construction companies and contractors, as well as the ongoing advancements in equipment technology. Moreover, rental firms compete fiercely to offer expanded rental fleets, enhanced service offerings, and competitive pricing strategies, enabling businesses to utilize the latest machinery and technology without ownership responsibilities. Technological advancements in heavy construction equipment are significant market growth factors. For instance, GPS guidance systems, emission reduction technologies, and improved cab comfort enhance machine productivity and operator experience.

How does Heavy Construction Equipment market face challenges during its growth?

- The expanding secondhand machine market poses a significant challenge to the industry's growth trajectory. The market is experiencing a shift in trends due to the increasing availability and demand for secondhand machines. This dynamic is particularly noticeable in industries based in the United States and Europe, where high labor expenses and stringent pollution regulations have led to the closure of several manufacturing and mining operations. As a result, there is an oversupply of secondhand heavy construction equipment, such as dump trucks, excavators, and bulldozers, which are being exported to developing economies in Asia. In response to this trend, Asian contractors and mining firms are actively seeking to purchase secondhand European equipment at reduced prices.

- This trend is driven by the cost-effective production facilities in APAC, which have attracted many manufacturing industries to relocate from developed economies. Performance metrics, such as fuel efficiency and safety features, remain key considerations for both new and secondhand equipment purchases. Additionally, maintenance contracts and specialized tools are essential for ensuring the longevity and productivity of heavy construction equipment. Overall, the market is characterized by a focus on maintaining equipment performance and reducing operational costs through the use of secondhand machinery.

Exclusive Customer Landscape

The heavy construction equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the heavy construction equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, heavy construction equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AB Volvo - This company specializes in providing heavy construction equipment solutions, including excavators and wheel loaders, to clients worldwide.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB Volvo

- Caterpillar Inc.

- CNH Industrial NV

- Deere and Co.

- Dieci Srl

- Doosan Corp.

- Eazi Access Investments Pty Ltd

- Hitachi Ltd.

- Hyundai Heavy Industries Group

- J C Bamford Excavators Ltd.

- Kobe Steel Ltd.

- Komatsu Ltd.

- Liebherr International AG

- Manitou BF SA

- Oshkosh Corp.

- Sany Group

- Terex Corp.

- Wacker Neuson SE

- Xuzhou Construction Machinery Group Co. Ltd.

- Zoomlion Heavy Industry Science and Technology Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Heavy Construction Equipment Market

- In January 2024, Caterpillar Inc., a leading heavy construction equipment manufacturer, launched its new electric mining truck prototype, the 793F AC Electric Drive, marking a significant step towards sustainable mining operations (Caterpillar Press Release, 2024).

- In March 2024, Volvo Construction Equipment and Gehl Company announced their strategic partnership, combining Volvo's global presence and Gehl's compact construction equipment expertise to expand their product offerings (Volvo Construction Equipment Press Release, 2024).

- In April 2025, Komatsu Limited, a major player in the heavy construction equipment industry, acquired Mobiles de Manutention SAS, a French forklift manufacturer, to strengthen its presence in the European market and expand its product portfolio (Komatsu Limited Press Release, 2025).

- In May 2025, the European Union approved the new emission standards for heavy construction equipment, which will come into effect from 2027, driving the market towards greener and more efficient machinery (European Commission Press Release, 2025).

Research Analyst Overview

The market continues to evolve, driven by advancements in technology and shifting market dynamics. Operating costs remain a key consideration, with aftermarket parts and software solutions playing essential roles in optimizing efficiency and reducing expenses. IoT sensors and GPS guidance enhance productivity and safety, while emission standards and cab comfort are increasingly prioritized for environmental impact and operator satisfaction. Emission reduction and fuel alternatives are at the forefront of industry innovation, with electric motors and diesel engines undergoing continuous improvements. Hydraulic systems and braking systems are being optimized for greater performance and reduced environmental footprint.

Waste management solutions are also gaining traction, as the industry focuses on sustainability and compliance with regulatory requirements. Infrastructure projects, material handling, and land clearing applications are among the sectors benefiting from these advancements. Lease agreements, maintenance contracts, and operator training are crucial components of the market's evolving business models. Transmission systems, lifting capacity, and safety features are also subject to ongoing research and development, ensuring that heavy construction equipment remains a vital and dynamic force in the industry. Specialized tools and remote control capabilities are increasingly important, enabling greater precision and flexibility on construction sites.

Performance metrics, safety regulations, and rental services are also shaping the market, as the industry continues to adapt and innovate. The market is characterized by continuous change and growth. From emission reduction and cab comfort to hydraulic systems and braking technology, the industry is constantly pushing the boundaries of what is possible. Whether it's through the integration of IoT sensors or the development of new fuel alternatives, the future of heavy construction equipment is bright and full of possibilities.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Heavy Construction Equipment Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

215 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.6% |

|

Market growth 2025-2029 |

USD 49.7 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.4 |

|

Key countries |

US, China, India, Brazil, Germany, Japan, UK, France, Canada, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Heavy Construction Equipment Market Research and Growth Report?

- CAGR of the Heavy Construction Equipment industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the heavy construction equipment market growth of industry companies

We can help! Our analysts can customize this heavy construction equipment market research report to meet your requirements.

RIA -

RIA -