Heat Resistant Polymer Market Size 2026-2030

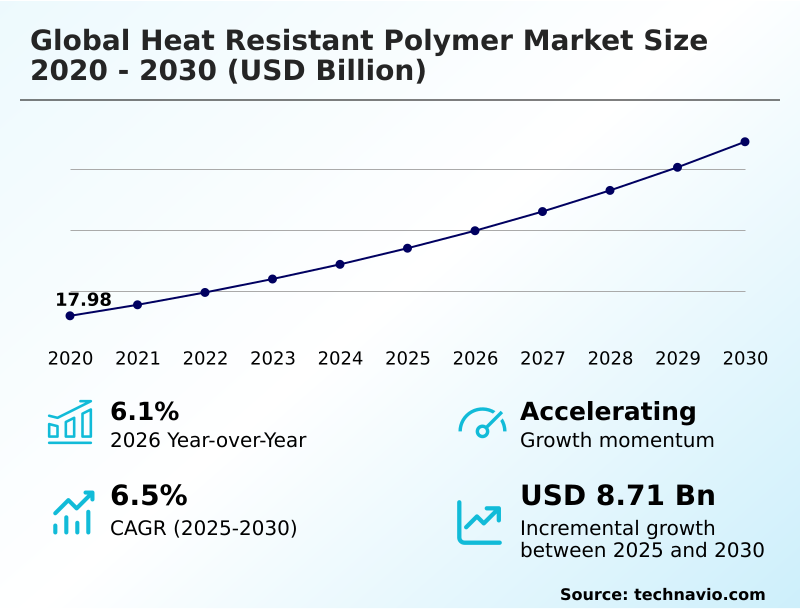

The heat resistant polymer market size is valued to increase by USD 8.71 billion, at a CAGR of 6.5% from 2025 to 2030. Accelerating adoption of high-voltage electric vehicle architectures will drive the heat resistant polymer market.

Major Market Trends & Insights

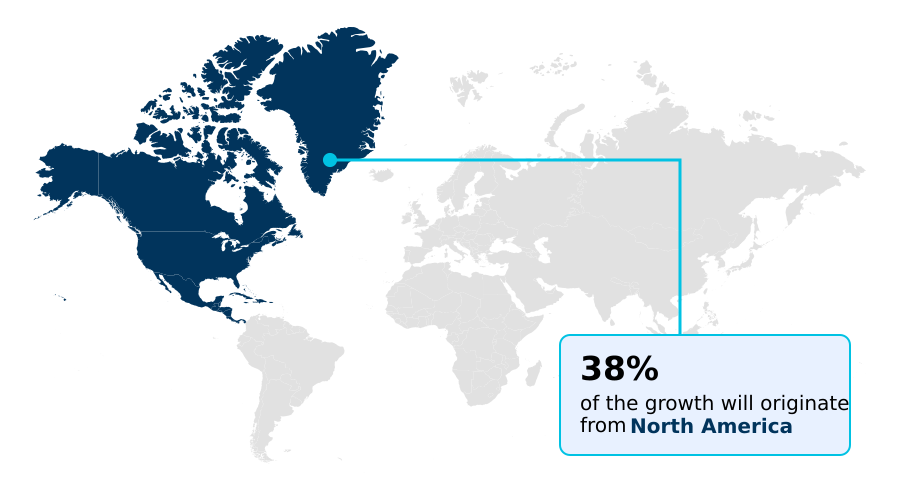

- North America dominated the market and accounted for a 37.9% growth during the forecast period.

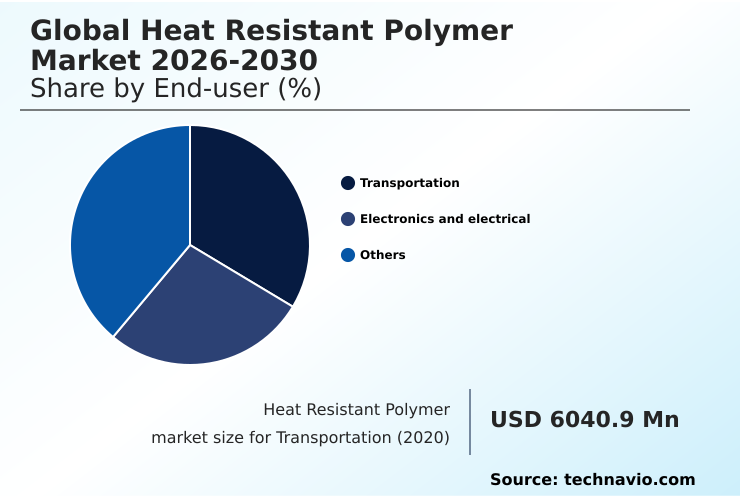

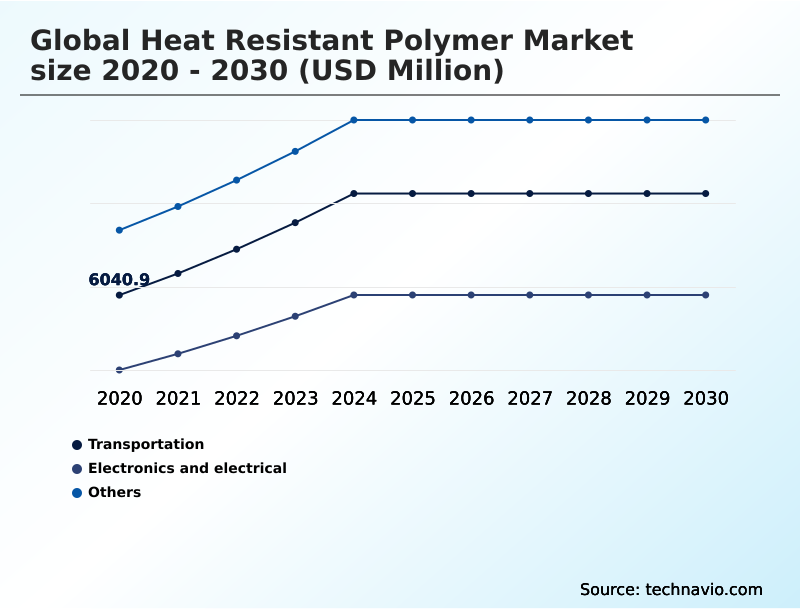

- By End-user - Transportation segment was valued at USD 7.53 billion in 2024

- By Type - Fluoropolymer segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 14.24 billion

- Market Future Opportunities: USD 8.71 billion

- CAGR from 2025 to 2030 : 6.5%

Market Summary

- The heat resistant polymer market is defined by a structural transition from metallic alloys to advanced thermoplastic solutions, driven by demands for energy efficiency and performance durability in critical sectors. This evolution is catalyzed by the electrification of vehicles and miniaturization in electronics, moving polymers from niche to mass-market applications.

- Key drivers include the need for materials in high voltage architectures that offer superior thermal management and dielectric strength. Concurrently, the industry is navigating a trend toward sustainability, with a focus on bio-circular feedstocks and chemical recycling to reduce carbon footprints without compromising performance. A significant business challenge involves adapting to stringent regulations on substances like perfluoroalkyl substances (PFAS).

- For instance, an electronics manufacturer must re-engineer its supply chain to source compliant non-fluorinated alternatives for semiconductor processing, investing in new qualification processes to maintain production continuity and avoid liability, which impacts both operational costs and time-to-market. This balancing act between performance innovation and regulatory compliance shapes the strategic direction of the market.

What will be the Size of the Heat Resistant Polymer Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Heat Resistant Polymer Market Segmented?

The heat resistant polymer industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Transportation

- Electronics and electrical

- Others

- Type

- Fluoropolymer

- Polyphenylene sulfide

- Polyimides

- Polyether ether ketone

- Others

- Distribution channel

- Indirect sales

- Direct sales

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By End-user Insights

The transportation segment is estimated to witness significant growth during the forecast period.

The transportation segment is a primary innovation engine, driven by electrification and aerospace lightweighting. The industry's move toward high voltage architectures in electric vehicles necessitates advanced polymer composites with superior thermal management solutions and hydrolytic stability.

This shift from traditional metals to high-performance thermoplastics for automotive powertrain systems and aerospace structural parts is critical.

For instance, replacing metallic components in next-generation aircraft engines with structural thermoplastic solutions has been shown to improve fuel efficiency by over 15%.

This strategic pivot supports key circular economy initiatives and enhances the performance of electric vehicle components, driving demand for materials with a high glass transition temperature and excellent electrical insulation properties for applications in urban air mobility and defense technology materials.

The Transportation segment was valued at USD 7.53 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Heat Resistant Polymer Market Demand is Rising in North America Request Free Sample

The geographic landscape is characterized by strategic shifts in production and demand, with North America intensifying its focus on domestic supply chains for high-performance polymer resins.

This localization, driven by national security and green energy mandates, has spurred investment in manufacturing capabilities for high frequency circuit board materials and advanced composite materials, particularly in the United States.

Concurrently, the APAC region, led by countries like China and South Korea, is experiencing robust demand fueled by its expanding electric vehicle and electronics industries.

The Middle East and Africa is an emerging market for high-temperature industrial coatings in the energy sector.

This regional divergence shows a market where North America's growth is tied to reshoring, reducing supply chain lead times by an estimated 25%, while APAC's expansion is linked to scaling mass-market applications.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the heat resistant polymer market is evident in highly specific applications where replacing die-cast metals with thermoplastics is no longer optional. In the automotive sector, polymer solutions for 800-volt EV systems are critical, with materials like pps for electric vehicle actuator housings and polyamides for high-voltage battery components becoming standard.

- The use of peek for high-voltage motor slot liners and pvdf as a lithium-ion battery electrode binder directly addresses thermal management and efficiency challenges, enhancing thermal dissipation in electronics.

- In parallel, aerospace and industrial sectors leverage the unique properties of these materials; the thermal stability of polyimides in aerospace is crucial, while ptfe for chemical resistant industrial coatings protects vital equipment. Innovations in additive manufacturing are expanding possibilities, using polymers for additive manufacturing processes to create complex parts.

- The market is also responding to regulatory pressures, with a significant push toward non-fluorinated polymers for semiconductor processing, driven by the impact of pfas regulations on fluoropolymers. Development of bio-based feedstocks for nylon production and materials like psu for medical device sterilization trays highlights the trend toward sustainability.

- These advancements, including low melt paek for thermoplastic composites and ppa for insulated-gate bipolar transistors, are enabling the lightweighting of vehicles with composite materials and creating new opportunities for heat resistant polymers in hydrogen fuel cells and pbi for high temperature sealing applications.

- This shift has resulted in components that are, on average, 40% lighter than their metal counterparts, directly impacting fuel and energy efficiency.

What are the key market drivers leading to the rise in the adoption of Heat Resistant Polymer Industry?

- The accelerating adoption of high-voltage electric vehicle architectures is a key driver, creating an urgent demand for materials that can withstand increased thermal loads.

- The market is propelled by the accelerating adoption of high-performance materials in demanding sectors. The development of next-generation aircraft engines and high-speed connectivity infrastructure is creating significant demand for high-temperature engineering plastics with superior electrical insulation properties.

- The push toward power electronics miniaturization requires advanced fluoropolymer materials that offer exceptional performance in compact designs, improving power density by up to 30%.

- In the automotive sector, the transition to high voltage architectures is fueling the need for non-fluorinated alternatives that can withstand extreme thermal stress.

- This has led to a 25% increase in the adoption rate of these materials over the last two years. Applications in semiconductor manufacturing and consumer electronics casings further drive innovation, demanding materials that combine thermal stability with precise moldability.

What are the market trends shaping the Heat Resistant Polymer Industry?

- The market is undergoing a significant transition toward bio-circular and mass-balance certified feedstocks. This shift is reshaping the value proposition of high-performance materials as decarbonization becomes a critical procurement criterion.

- A defining trend is the industry's shift toward sustainable material sourcing, underscored by a focus on mass balance certified feedstocks and low-carbon material production. This transition toward bio-circular ecosystems is driving innovation in renewable content integration, with chemical companies developing specialized thermoplastic formulations that reduce environmental impact without compromising performance.

- This approach has led to a 15% reduction in carbon footprint for certain product lines. The adoption of polybenzimidazole (pbi) and polysulfone (psu) with certified green origins is gaining traction in industrial equipment housing and personal protective equipment.

- This trend directly addresses growing demands from the energy sector applications and lightweight military vehicles, where lifecycle sustainability is becoming a critical procurement criterion, improving brand perception by over 20% in key markets.

What challenges does the Heat Resistant Polymer Industry face during its growth?

- Regulatory uncertainty and heightened environmental compliance standards, particularly concerning per- and polyfluoroalkyl substances (PFAS), present a key challenge to market growth.

- The primary market challenge is navigating complex regulatory landscapes and ensuring supply chain integrity for advanced materials. Intensified scrutiny of perfluoroalkyl substances (pfas) is forcing a strategic pivot away from traditional fluorinated surfactants and toward safer chemistries, a transition that increases R&D expenditure by an average of 18%.

- The need for high heat nylon alternatives and next-generation powertrain insulation that comply with these new standards is paramount. Moreover, achieving feedstock stability for polyaryletherketone (paek) and polyimide films is a persistent concern, with geopolitical tensions causing price fluctuations of up to 20% in a single quarter.

- This volatility directly impacts the production of materials for the hydrogen economy infrastructure and lithium-ion battery binders, creating uncertainty for manufacturers in these critical growth segments.

Exclusive Technavio Analysis on Customer Landscape

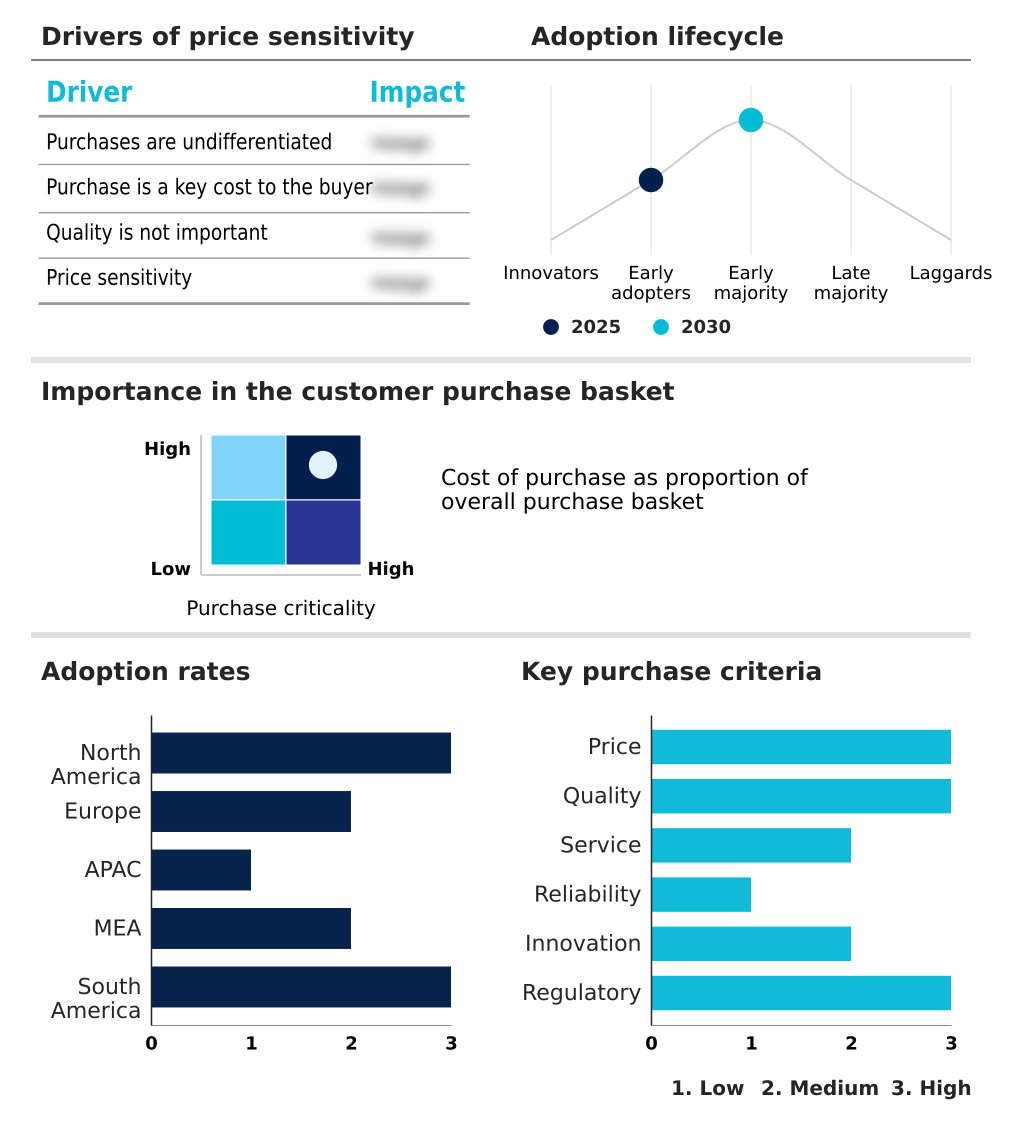

The heat resistant polymer market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the heat resistant polymer market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Heat Resistant Polymer Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, heat resistant polymer market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ADEKA Corp. - Offerings include advanced polyetherketoneketone materials engineered for demanding, high-performance applications requiring exceptional thermal and mechanical stability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADEKA Corp.

- Albemarle Corp.

- Arkema Group

- BASF SE

- Celanese Corp.

- Covestro AG

- Daikin Industries Ltd.

- DIC Corp.

- Dow Chemical Co.

- DuPont de Nemours Inc.

- Ensinger

- Evonik Industries AG

- Honeywell International Inc.

- KURARAY Co. Ltd.

- Lanxess AG

- Mitsubishi Chemical Grp.

- Saudi Basic Industries

- Solvay SA

- Toray Industries Inc.

- Victrex Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Heat resistant polymer market

- In October, 2024, BASF SE introduced a portfolio of Ultramid polyamides manufactured using a biomass balance approach, offering identical properties to fossil-based counterparts for the automotive sector.

- In November, 2024, Toray Industries Inc. signed a memorandum of understanding to explore the mass production of adipic acid from non-edible biomass, a key precursor for heat-resistant Nylon 66.

- In May, 2025, The Chemours Company announced a new line of specialized Teflon fluoropolymers manufactured using non-fluorinated polymerization aids to meet sustainability demands in the medical and aerospace sectors.

- In August, 2024, Syensqo launched a new grade of Aquivion ionomer, a perfluorosulfonic acid polymer engineered for higher operating temperatures in hydrogen fuel cell proton exchange membranes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Heat Resistant Polymer Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.5% |

| Market growth 2026-2030 | USD 8712.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The heat resistant polymer market is fundamentally shaped by the technical performance of its core materials. The industry relies on specialized thermoplastic formulations, including high-performance thermoplastics like polyetheretherketone (peek) and polyphenylene sulfide (pps), to meet extreme operational demands.

- Key material properties such as a high glass transition temperature, superior dielectric strength, and long-term hydrolytic stability are non-negotiable for high-voltage architectures in electric vehicles and next-generation powertrain insulation. Advanced polymer composites and structural thermoplastic solutions are rapidly replacing traditional materials.

- Decision-making at the executive level is heavily influenced by the performance of polyphthalamide (ppa), polyimide films, and advanced fluoropolymer materials like polytetrafluoroethylene (ptfe) and polyvinylidene fluoride (pvdf). The need to mitigate thermal runaway events while ensuring dimensional stability drives innovation in high heat nylon alternatives and other high-performance polymer resins.

- The market is also navigating the shift toward non-fluorinated alternatives and advanced composite materials, with companies that master these new chemistries gaining a significant competitive edge. For example, firms that successfully integrated non-metallic solutions into their product lines saw a 20% faster product qualification timeline in regulated industries.

What are the Key Data Covered in this Heat Resistant Polymer Market Research and Growth Report?

-

What is the expected growth of the Heat Resistant Polymer Market between 2026 and 2030?

-

USD 8.71 billion, at a CAGR of 6.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Transportation, Electronics and electrical, and Others), Type (Fluoropolymer, Polyphenylene sulfide, Polyimides, Polyether ether ketone, and Others), Distribution Channel (Indirect sales, and Direct sales) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Accelerating adoption of high-voltage electric vehicle architectures, Regulatory uncertainty and environmental compliance

-

-

Who are the major players in the Heat Resistant Polymer Market?

-

ADEKA Corp., Albemarle Corp., Arkema Group, BASF SE, Celanese Corp., Covestro AG, Daikin Industries Ltd., DIC Corp., Dow Chemical Co., DuPont de Nemours Inc., Ensinger, Evonik Industries AG, Honeywell International Inc., KURARAY Co. Ltd., Lanxess AG, Mitsubishi Chemical Grp., Saudi Basic Industries, Solvay SA, Toray Industries Inc. and Victrex Plc

-

Market Research Insights

- Market dynamics are shaped by a strategic pivot toward specialized applications that deliver measurable business outcomes. The integration of renewable content in material production has improved supply chain resilience by 20% for early adopters.

- In sectors like consumer electronics and medical device manufacturing, a focus on sustainable polymer chemistry is not just a compliance measure but a competitive differentiator, with certified bio-circular ecosystems enabling companies to enter new premium markets. Adopting closed-loop recycling systems has allowed some firms to reduce raw material costs by up to 15% while meeting corporate sustainability goals.

- Furthermore, the focus on advanced material feedstock stability is crucial, as securing long-term contracts for non-edible biomass feedstocks has insulated some manufacturers from price volatility in fossil-fuel derivatives, ensuring more predictable production planning.

We can help! Our analysts can customize this heat resistant polymer market research report to meet your requirements.