Hair Loss Treatment Products Market Size 2026-2030

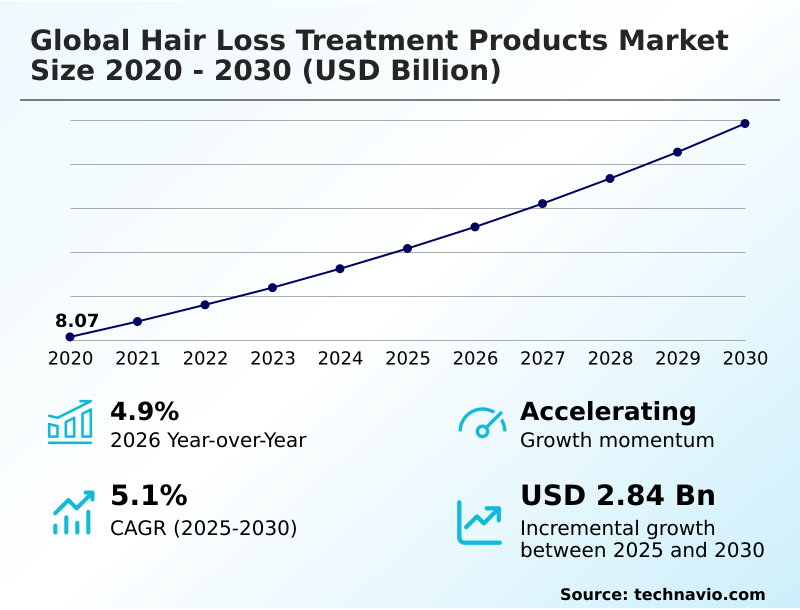

The hair loss treatment products market size is valued to increase by USD 2.84 billion, at a CAGR of 5.1% from 2025 to 2030. Increasing prevalence of alopecia and other hair loss conditions will drive the hair loss treatment products market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 41.4% growth during the forecast period.

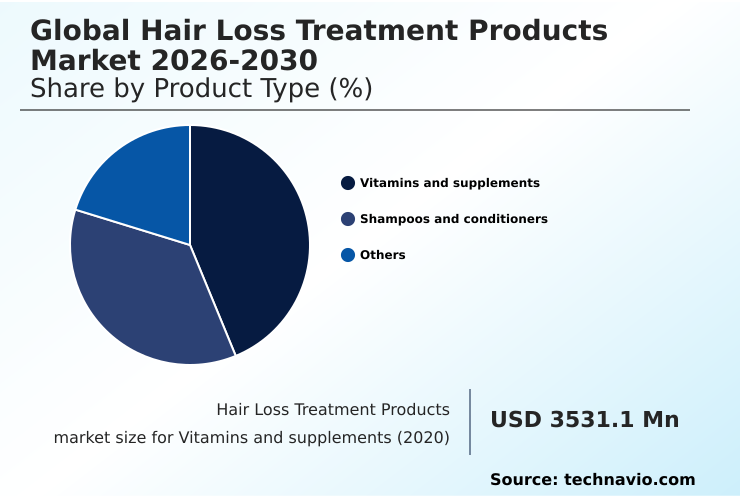

- By Product Type - Vitamins and supplements segment was valued at USD 4.16 billion in 2024

- By Gender - Men segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.85 billion

- Market Future Opportunities: USD 2.84 billion

- CAGR from 2025 to 2030 : 5.1%

Market Summary

- The hair loss treatment products market is expanding, driven by a growing consumer focus on aesthetic and wellness solutions. Conditions such as androgenetic alopecia and telogen effluvium are increasingly addressed through scientifically advanced products that go beyond simple cosmetic fixes.

- The market is characterized by a strong emphasis on research and development, leading to innovations like dihydrotestosterone (dht) blocker formulations and enhanced low-level laser therapy (lllt) devices. A key trend is the integration of diagnostic data into product offerings.

- For instance, a direct-to-consumer brand leverages trichological assessment data to formulate a custom hair regrowth serum, optimizing its supply chain by predicting demand for specific scientifically proven ingredients and reducing waste by 25%. This data-driven approach enhances efficacy and consumer trust.

- As a result, offerings are shifting from one-size-fits-all to personalized regimens that target specific issues like follicular miniaturization and poor scalp microbiome health, signaling a more sophisticated and effective future for hair care.

What will be the Size of the Hair Loss Treatment Products Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Hair Loss Treatment Products Market Segmented?

The hair loss treatment products industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

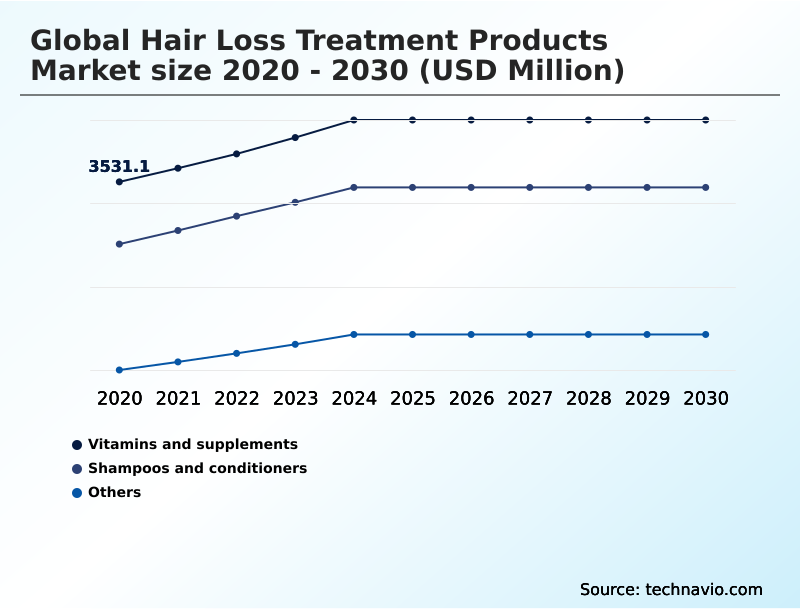

- Product type

- Vitamins and supplements

- Shampoos and conditioners

- Others

- Gender

- Men

- Women

- Children

- Category

- Topical

- Oral

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of World (ROW)

- APAC

By Product Type Insights

The vitamins and supplements segment is estimated to witness significant growth during the forecast period.

The hair wellness supplement segment represents a significant and growing category, driven by a consumer shift toward a holistic hair health approach.

These products, addressing early-stage hair loss intervention, account for over 43% of the market by focusing on scientifically proven ingredients. Formulations emphasize an advanced nutrient delivery system to support the body's natural processes.

Innovations in advanced hair science include products designed for scalp detoxification and hair fiber repair. Advanced peptide complex ingredients and support for follicular stem cells are becoming standard.

These supplements are designed to influence gene expression modulation related to hair health, offering a non-pharmaceutical option for consumers seeking a scalp soothing formula to manage hair fall control.

The Vitamins and supplements segment was valued at USD 4.16 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 41.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Hair Loss Treatment Products Market Demand is Rising in APAC Request Free Sample

Regional dynamics show significant variation, with the APAC region driving over 41% of the market’s incremental growth. This is fueled by high consumer awareness and a rising demand for solutions addressing stress-induced hair shedding and scalp aging defense.

Key markets in the region exhibit an adoption rate for over-the-counter hair treatment and prescription hair medication that is 15% higher than the global average. Innovations focus on hair shaft strengthening and improving hair strand resilience.

Localized strategies often incorporate ingredients that aid in sebaceous gland regulation and support hair matrix cells.

This proactive approach to hair vitality booster products, including those featuring a hair anchoring complex for vellus hair conversion, underscores the region's importance as both a high-growth area and a center for product innovation.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the market are increasingly influenced by comparative efficacy and targeted applications. The debate over dht blocker vs minoxidil efficacy continues to drive consumer choice and clinical research, while understanding the impact of scalp microbiome on hair loss opens new avenues for product development.

- Innovations such as topical finasteride with reduced side effects are addressing key consumer concerns, making prescription medication for advanced hair loss more accessible. The effectiveness of hair density improvement serums is now a key performance indicator for many brands. In parallel, the demand for non-invasive treatments for follicular miniaturization is growing, with low-level laser therapy for androgenetic alopecia gaining traction.

- Companies are focusing on the best peptide technology for hair regrowth and optimizing nutrient delivery systems for hair follicles. Formulations that include keratin synthesis support for stronger hair and botanical extracts for telogen effluvium are popular. Discussions on how to improve scalp circulation for hair growth and the role of gene expression in hair thinning are central to R&D.

- Furthermore, understanding the relationship between sebaceous gland and hair loss informs the development of targeted solutions. The use of trichological assessment for hair loss diagnosis is becoming standard, guiding the creation of personalized hair supplements for women and advanced anti-inflammatory scalp care for alopecia areata.

- The development of a hair anchoring complex for reducing shedding shows a market shift toward preventative measures, with clinical trials for new hair loss treatments validating these new approaches.

What are the key market drivers leading to the rise in the adoption of Hair Loss Treatment Products Industry?

- The increasing global prevalence of alopecia and various other hair loss conditions is a primary driver for market expansion.

- Key market drivers are rooted in heightened consumer awareness and significant product innovation. The demand for solutions addressing male pattern baldness solution and hormonal hair loss treatment has led to a market expansion of nearly 5% year-over-year.

- This growth is sustained by advancements in understanding scalp microbiome health and keratin synthesis support, which are crucial for hair density improvement.

- An effective hair care regimen now often includes a topical hair growth formula designed for anagen phase extension and scalp circulation enhancement.

- This focus on treating conditions like non-scarring alopecia and follicular miniaturization has broadened the scope of cosmetic hair restoration. As the population faces more age-related hair thinning, R&D pipelines have expanded by over 15% to develop more effective treatments.

What are the market trends shaping the Hair Loss Treatment Products Industry?

- The trend toward personalization and customized solutions is reshaping the market. This shift reflects a move from generic products to treatments tailored for individual needs.

- Market trends are converging around hyper-personalization, driven by advanced hair science and consumer demand for targeted results. This shift toward customized hair treatment and personalized hair wellness is supported by digital platforms, which have improved the accessibility of tailored hair regrowth serum formulations by over 40%.

- Rather than generic approaches, consumers now seek a scalp health solution for specific concerns like androgenetic alopecia or telogen effluvium. As a result, products combining a dihydrotestosterone (dht) blocker with a nutritional hair supplement are gaining traction.

- This trend has pushed R&D investments in low-level laser therapy (lllt) and other forms of hair follicle stimulation up by 25%, as brands aim to offer a comprehensive hair thinning prevention strategy that includes minoxidil topical solution and finasteride oral medication.

What challenges does the Hair Loss Treatment Products Industry face during its growth?

- Stringent regulatory approval processes for new treatments present a significant challenge to industry growth and product innovation.

- Navigating the complex regulatory landscape remains a primary challenge, with compliance costs increasing by over 20% in recent years. The stringent criteria for a clinical hair trial and approval of any dermatological formulation slow down market entry. This is particularly true for products targeting female pattern hair loss and post-partum hair loss, which require extensive safety data.

- The prevalence of counterfeit products, capturing an estimated 10% of online sales, further complicates the market, eroding trust in legitimate therapeutic hair care. Companies invest heavily in advanced scalp care and preventative hair care solutions using peptide technology for hair and botanical hair extracts.

- However, bringing these innovations, including those for hair structure improvement and hair growth cycle regulation, to market requires navigating a complex web of approvals after a thorough trichological assessment.

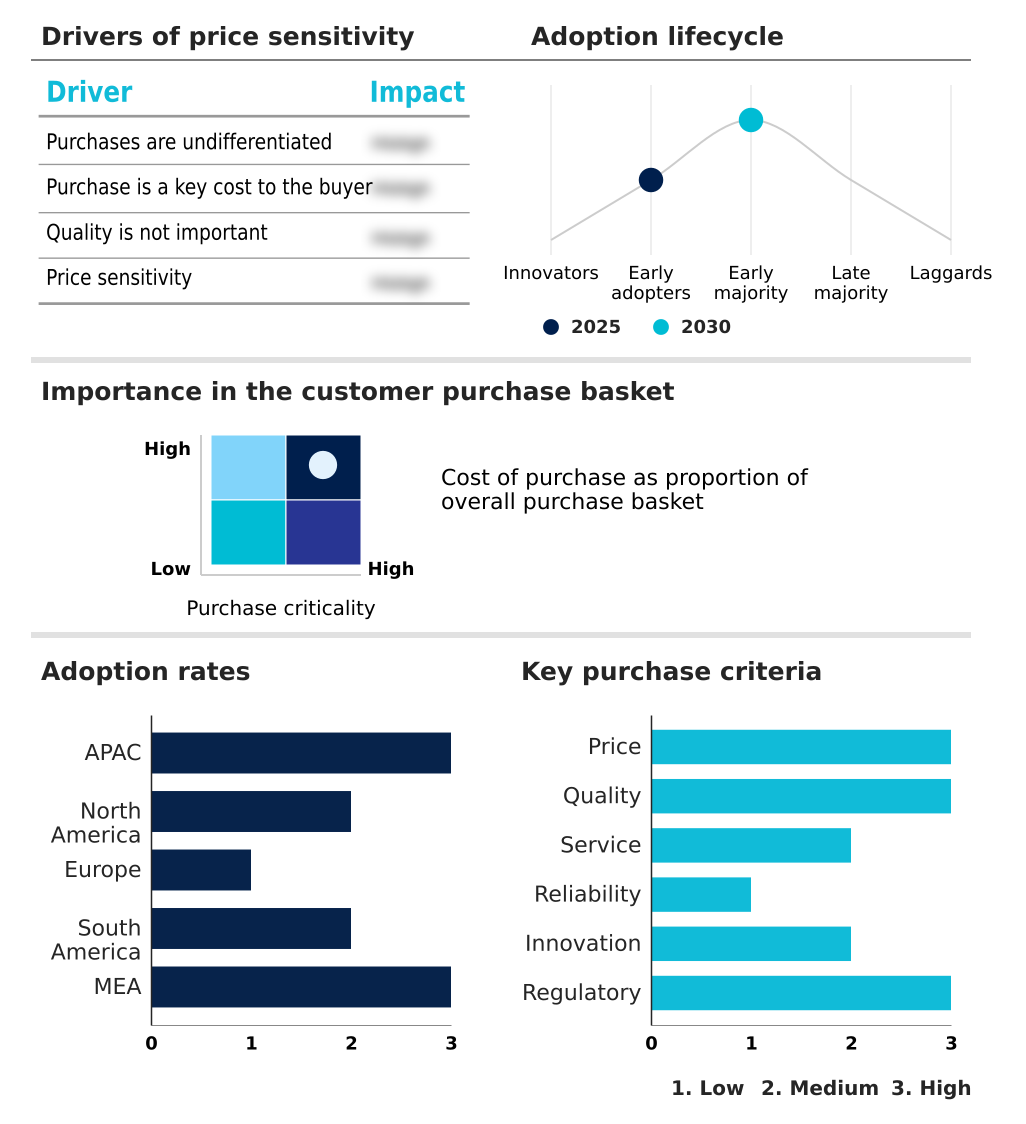

Exclusive Technavio Analysis on Customer Landscape

The hair loss treatment products market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hair loss treatment products market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Hair Loss Treatment Products Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, hair loss treatment products market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Cipla Inc. - Offers therapeutic hair care solutions and targeted treatments for hair thinning, emphasizing scientifically proven ingredients to restore scalp health and improve overall hair density.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Cipla Inc.

- Dr Reddys Laboratories Ltd.

- Glenmark Pharmaceuticals Ltd.

- Henkel AG and Co. KGaA

- Johnson and Johnson Services

- Kao Corp.

- Hairmax International, LLC.

- LOreal SA

- Mankind Pharma Ltd.

- Merck and Co. Inc.

- Pierre Fabre SA

- Procter and Gamble Co.

- Pure Source LLC

- Revlon Inc.

- Shiseido Co. Ltd.

- Sun Pharmaceutical Industries Ltd.

- Taisho Pharmaceutical Co. Ltd.

- The Estee Lauder Co. Inc.

- The Himalaya Drug Co.

- Unilever PLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Hair loss treatment products market

- In September, 2024, L'Oreal SA announced a strategic partnership with a leading biotechnology firm to accelerate research into novel biological pathways for hair growth, focusing on follicular stem cells.

- In November, 2024, DS Healthcare Group Inc. launched a new line of topical serums incorporating advanced peptide complex technology to combat follicular miniaturization and promote hair density.

- In January, 2025, a major pharmaceutical company confirmed a delay in the European market launch of its new topical finasteride treatment, citing requests for additional long-term safety data from the European Medicines Agency (EMA).

- In April, 2025, Shiseido Co. Ltd. expanded its presence in the APAC market with the release of a new scalp care system designed with botanical hair extracts to address early-stage hair loss.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hair Loss Treatment Products Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.1% |

| Market growth 2026-2030 | USD 2836.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.9% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, South Africa, UAE, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is defined by a shift toward science-backed, targeted interventions. At the core, managing androgenetic alopecia and telogen effluvium remains paramount, with a multi-faceted approach involving a dihydrotestosterone (dht) blocker, minoxidil topical solution, and finasteride oral medication. Technological advancements like low-level laser therapy (lllt) complement these treatments through direct hair follicle stimulation.

- A boardroom-level focus on R&D has led to breakthroughs in scalp microbiome health and keratin synthesis support, enabling an extension of the anagen phase for hair density improvement. This focus on the hair growth cycle regulation addresses follicular miniaturization and non-scarring alopecia by improving scalp circulation enhancement.

- Recent innovations in peptide technology for hair and botanical hair extracts have resulted in superior dermatological formulation, evident in new anti-inflammatory scalp treatment products. Boardroom strategy is now influenced by the outcomes of a clinical hair trial, with decisions on over-the-counter hair treatment versus prescription hair medication hinging on trichological assessment data.

- Formulations now target hair shaft strengthening, vellus hair conversion, sebaceous gland regulation, and hair matrix cells via advanced nutrient delivery systems and hair anchoring complex technology. This is driven by a deeper understanding of gene expression modulation, scalp detoxification, and follicular stem cells, leading to sophisticated hair wellness supplement products with advanced peptide complex ingredients for hair fiber repair.

What are the Key Data Covered in this Hair Loss Treatment Products Market Research and Growth Report?

-

What is the expected growth of the Hair Loss Treatment Products Market between 2026 and 2030?

-

USD 2.84 billion, at a CAGR of 5.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Vitamins and supplements, Shampoos and conditioners, and Others), Gender (Men, Women, and Children), Category (Topical, and Oral) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of alopecia and other hair loss conditions, Stringent regulatory approval processes

-

-

Who are the major players in the Hair Loss Treatment Products Market?

-

Cipla Inc., Dr Reddys Laboratories Ltd., Glenmark Pharmaceuticals Ltd., Henkel AG and Co. KGaA, Johnson and Johnson Services, Kao Corp., Hairmax International, LLC., LOreal SA, Mankind Pharma Ltd., Merck and Co. Inc., Pierre Fabre SA, Procter and Gamble Co., Pure Source LLC, Revlon Inc., Shiseido Co. Ltd., Sun Pharmaceutical Industries Ltd., Taisho Pharmaceutical Co. Ltd., The Estee Lauder Co. Inc., The Himalaya Drug Co. and Unilever PLC

-

Market Research Insights

- The market is increasingly shaped by a focus on tailored solutions, where adoption of personalized hair wellness plans has surged by over 30%. This move toward customized hair treatment is proving effective, with consumer retention for brands offering a unique follicle revival program being 20% higher than for those with standard product lines.

- The demand for advanced scalp care and preventative hair care is compelling businesses to innovate. As a result, product development is centered on hair strand resilience and cosmetic hair restoration.

- This dynamic environment rewards companies that can effectively implement a holistic hair health strategy, integrating a scalp soothing formula and root strengthening treatment to deliver measurable improvements in hair structure and vitality.

We can help! Our analysts can customize this hair loss treatment products market research report to meet your requirements.