Generative AI In Pharmaceutical Industry Market Size 2025-2029

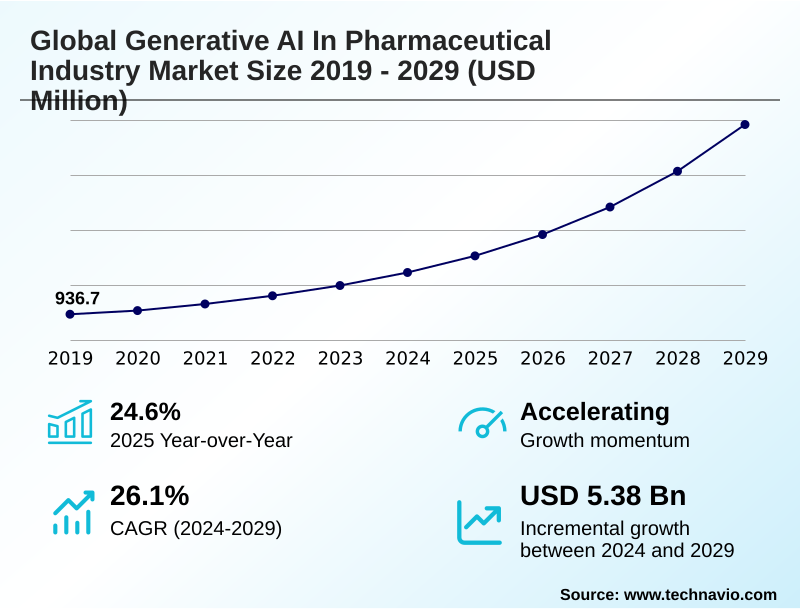

The generative ai in pharmaceutical industry market size is valued to increase by USD 5.38 billion, at a CAGR of 26.1% from 2024 to 2029. Accelerating drug discovery and development will drive the generative ai in pharmaceutical industry market.

Major Market Trends & Insights

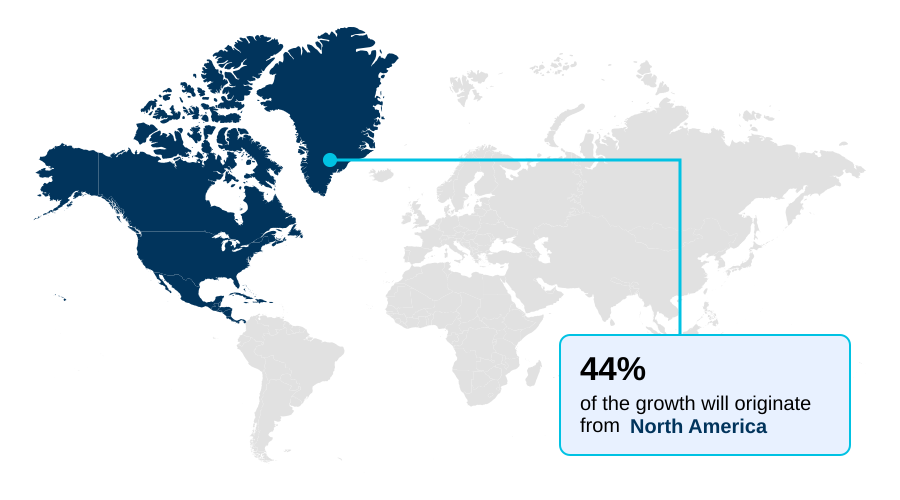

- North America dominated the market and accounted for a 44.1% growth during the forecast period.

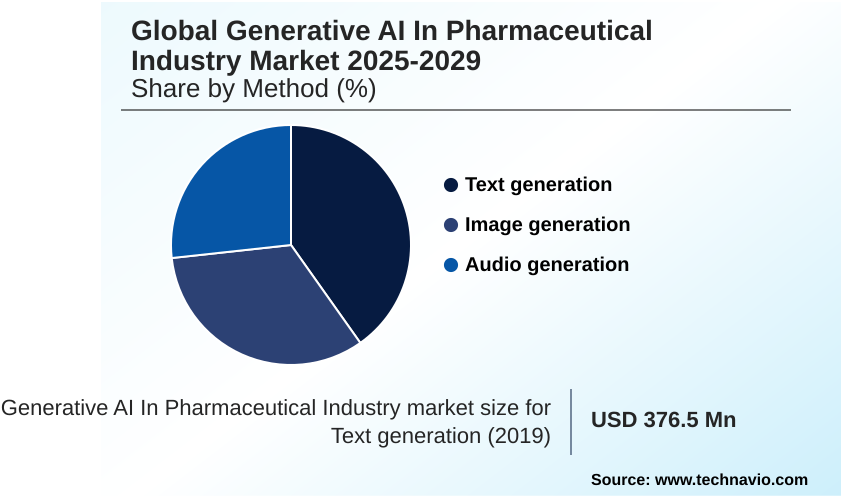

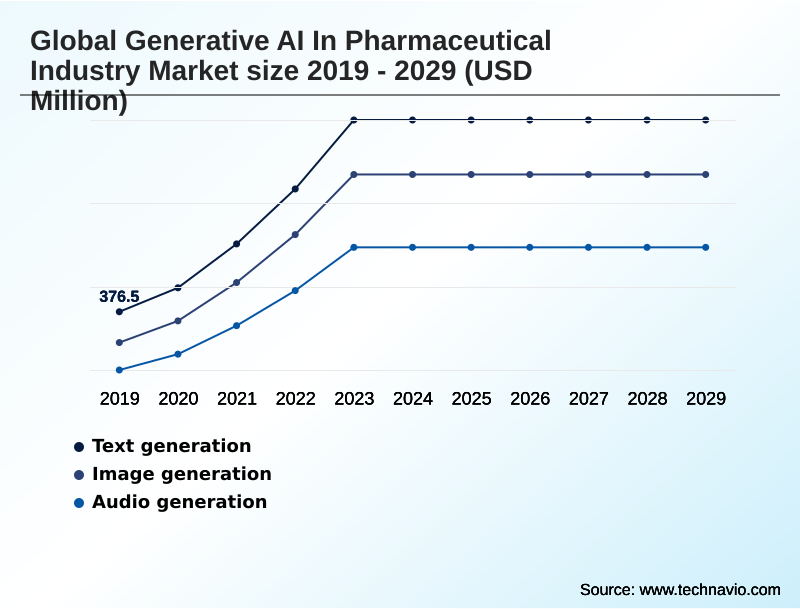

- By Method - Text generation segment was valued at USD 791.7 million in 2023

- By Application - Commercial segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 6.90 billion

- Market Future Opportunities: USD 5.38 billion

- CAGR from 2024 to 2029 : 26.1%

Market Summary

- The Generative AI in pharmaceutical industry market is fundamentally altering the R&D paradigm by enabling capabilities that were previously unfeasible. At its core, the technology leverages deep learning algorithms and predictive modeling to accelerate timelines, from initial target identification to late-stage clinical trials.

- A key application is de novo drug design, where models create novel molecular structures with desired therapeutic properties, moving beyond the limitations of traditional screening. This is complemented by the use of synthetic patient data, which helps train algorithms for rare diseases without compromising privacy.

- One common business scenario involves a company using natural language processing for clinical trial optimization, analyzing electronic health records to identify and recruit eligible patients with greater speed and precision than manual methods. While this accelerates enrollment, firms must concurrently implement robust frameworks like federated learning to manage data security and navigate the complex web of regulatory compliance.

- The effective use of these technologies, including vocal biomarkers and pharmacovigilance, is becoming a critical differentiator in the competitive Generative AI in pharmaceutical industry market.

What will be the Size of the Generative AI In Pharmaceutical Industry Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Generative AI In Pharmaceutical Industry Market Segmented?

The generative ai in pharmaceutical industry industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Method

- Text generation

- Image generation

- Audio generation

- Application

- Commercial

- Drug discovery

- Clinical development

- Research and development

- Operations

- Technology

- Deep learning models

- Natural language processing

- Generative adversarial networks

- Variational autoencoders

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- India

- Japan

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Method Insights

The text generation segment is estimated to witness significant growth during the forecast period.

The Generative AI in the pharmaceutical industry market is segmented by several methods, with text generation being a important component. This method leverages natural language processing and real-world evidence analysis to automate complex, language-based tasks.

Organizations utilize this for clinical study report automation and to generate regulatory submissions, achieving efficiency gains that can reduce submission timelines by as much as 40%.

The technology is also pivotal for precision medicine enablement, powering prognostic management programs and the automated molecule generation of descriptive outputs from complex datasets.

The application of AI in medical and regulatory writing, supported by NLP for clinical notes analysis and real-world data integration, is reshaping how scientific and clinical information is processed and communicated, enabling faster development cycles.

The Text generation segment was valued at USD 791.7 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Generative AI In Pharmaceutical Industry Market Demand is Rising in North America Request Free Sample

The geographic landscape of the generative AI in the pharmaceutical industry market is characterized by distinct regional strengths and growth trajectories.

North America is set to contribute over 44% of the market's incremental growth, driven by substantial venture capital, advanced high-performance computing infrastructure, and a high concentration of pharmaceutical leaders and AI startups.

This region excels in clinical trial optimization and AI-powered drug research. Concurrently, the APAC region is projected to exhibit the fastest adoption rate, fueled by government initiatives and a focus on digital health.

This growth is supported by expanding real-world evidence analysis and a burgeoning ecosystem for AI-powered target validation. Europe maintains a strong position with its focus on regulatory frameworks and collaborative research, particularly in areas like drug repurposing and protein engineering.

Across all regions, the focus is on leveraging AI for faster target identification and development.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The integration of advanced computational methods is reshaping the entire pharmaceutical value chain, from initial discovery to post-market surveillance. The use of generative adversarial networks for drug discovery and variational autoencoders in molecular design are becoming central to creating novel therapeutics.

- These technologies enable de novo drug design for small molecules and are increasingly applied to designing biologics with generative models. In early stages, AI-powered target identification and validation, combined with high-performance computing for molecular simulation, significantly shorten exploratory phases. As candidates progress, the focus shifts to optimizing clinical trials with predictive AI.

- This includes using NLP for clinical trial recruitment and generating synthetic control arms for trials, which is particularly valuable for rare diseases. Applying deep learning to pathology images helps in biomarker discovery and patient stratification. Throughout this process, enhancing pharmacovigilance with natural language processing and improving supply chain forecasting with AI ensure operational efficiency and safety.

- Cross-cutting concerns such as federated learning for pharmaceutical data privacy and mitigating algorithmic bias in AI drug models are critical for responsible deployment. This integrated approach has shown the potential to reduce preclinical timelines to under 18 months, a fraction of the traditional multi-year average, fundamentally accelerating drug development with synthetic data.

What are the key market drivers leading to the rise in the adoption of Generative AI In Pharmaceutical Industry Industry?

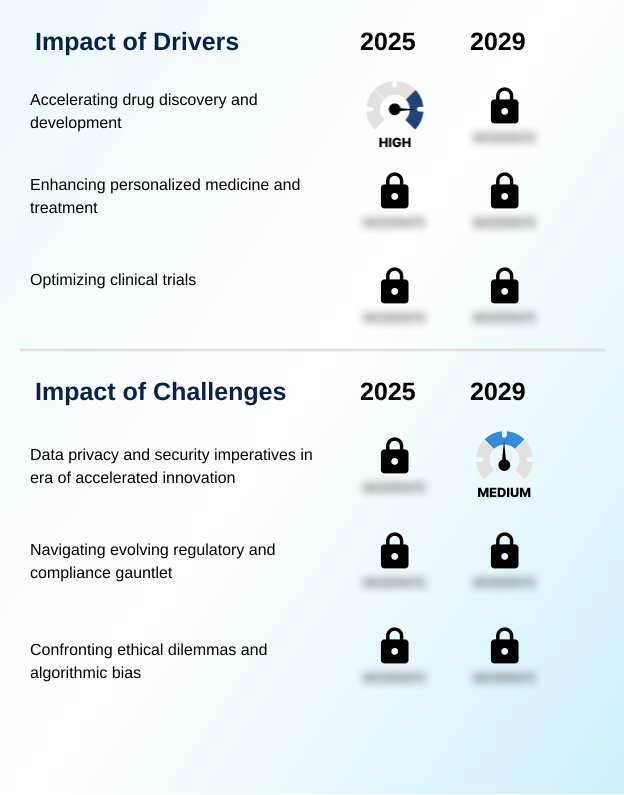

- The capability to significantly accelerate drug discovery and development timelines is a primary driver for the generative AI in the pharmaceutical industry market.

- The primary drivers of the generative AI in pharmaceutical industry market are its capabilities to accelerate discovery timelines and enable highly personalized therapies.

- The application of de novo drug design, including de novo antibody design, is a major factor, with demonstrated successes in bringing a novel drug candidate from discovery to preclinical stages in under eighteen months.

- This acceleration is creating a paradigm shift in how small molecule therapeutics are developed. Concurrently, the drive for precision medicine enablement is fueling adoption, as evidenced by the significantly higher number of novel personalized therapies approved in recent years.

- Generative AI allows for the creation of synthetic control arms, making patient-centered trial design more feasible, especially for rare diseases. The technology's capacity to generate new molecular structures and support machine learning for drug repurposing is fundamentally reshaping R&D productivity.

What are the market trends shaping the Generative AI In Pharmaceutical Industry Industry?

- A key trend is the revolutionizing of medical and regulatory writing through generative AI. This application significantly streamlines document creation, accelerating regulatory approvals and scientific communications.

- Key trends in the generative AI in pharmaceutical industry market are centered on operational automation and enhanced efficiency across the value chain. The adoption of AI-optimized supply chain management is proving transformative, with implementations demonstrating the ability to mitigate over 80% of low-inventory risks through improved predictive analytics.

- Another significant trend is the use of automated data analysis platforms for clinical study report automation, which can reduce the manual effort for medical writers by up to 30%. These advancements are powered by sophisticated deep learning algorithms and are enabling new approaches to AI-powered drug research.

- Generative chemistry platforms, which serve as high-throughput screening alternatives, are accelerating AI-accelerated drug development, particularly in creating treatments for rare diseases. This fusion of robotic lab automation and automated chemical synthesis is streamlining processes from discovery to delivery.

What challenges does the Generative AI In Pharmaceutical Industry Industry face during its growth?

- Ensuring data privacy and security for sensitive health information and intellectual property presents a key challenge amid accelerated innovation in the industry.

- Navigating data privacy, regulatory uncertainty, and ethical considerations are the primary challenges facing the generative AI in pharmaceutical industry market. The need to protect sensitive information while leveraging multi-omics data integration necessitates the use of advanced techniques like federated learning and the creation of digital twin simulations.

- A major hurdle is the risk of algorithmic bias, which can compromise the equity of patient stratification models if not actively addressed. Regulatory bodies are grappling with how to validate outputs from complex transformer architecture and predictive modeling, as highlighted by the more than 2 million adverse event reports they process annually.

- The development of clear frameworks, such as Europe's multi-annual AI workplan for 2023-2028, is crucial for establishing trust and ensuring AI compliance in pharmaceuticals, particularly for predictive toxicology models and other high-risk applications.

Exclusive Technavio Analysis on Customer Landscape

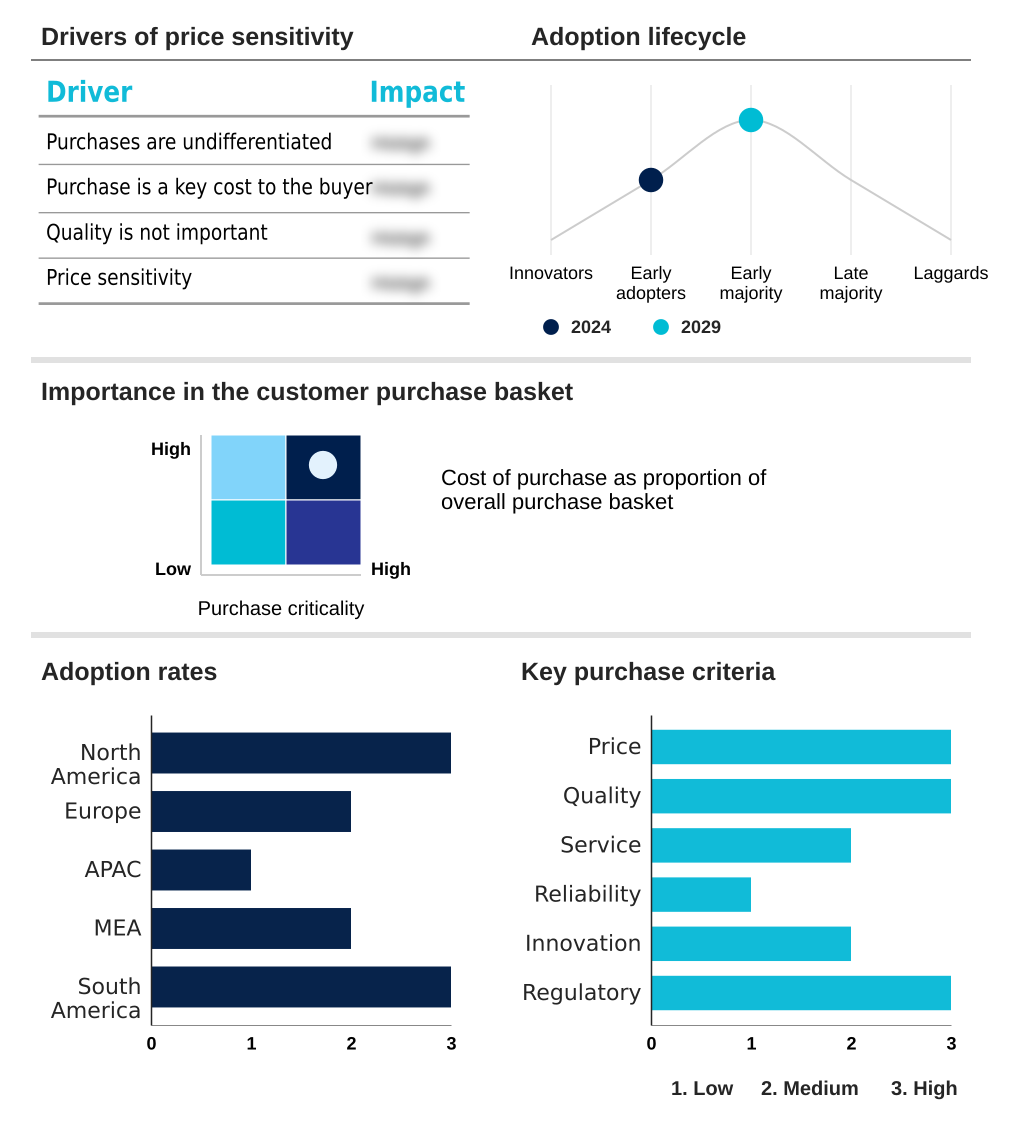

The generative ai in pharmaceutical industry market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the generative ai in pharmaceutical industry market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Generative AI In Pharmaceutical Industry Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, generative ai in pharmaceutical industry market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AstraZeneca Plc - Key offerings from vendors include platforms for de novo drug design, synthetic patient data generation, and clinical trial optimization, accelerating the entire pharmaceutical R&D pipeline.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AstraZeneca Plc

- Atomwise Inc.

- Bayer AG

- BenevolentAI

- BioXcel Therapeutics Inc.

- Deep Genomics Inc.

- Exscientia plc

- Insilico Medicine

- PathAI Inc.

- Recursion Pharmaceuticals Inc.

- Relay Therapeutics Inc.

- Sanofi SA

- Schrodinger Inc.

- Shenzhen Jingtai Technology Co.Ltd

- Valo Health

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Generative ai in pharmaceutical industry market

- In August 2024, Recursion Pharmaceuticals Inc. announced a definitive agreement to acquire Exscientia plc to enhance its early-stage drug discovery pipeline and precision chemistry capabilities.

- In October 2024, BioNTech SE's subsidiary, InstaDeep, announced the release of new foundational generative AI models for proteins and DNA through its DeepChain platform to accelerate biopharmaceutical research.

- In January 2025, the U.S. Food and Drug Administration (FDA) issued draft guidance on using artificial intelligence in drug development, providing a framework for sponsors to establish the credibility of AI models in clinical trials.

- In February 2025, Iktos secured a USD 2.93 million grant from the European Innovation Council Accelerator to further develop its AI drug discovery capabilities and launch a robotics platform for automated chemical synthesis.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Generative AI In Pharmaceutical Industry Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 26.1% |

| Market growth 2025-2029 | USD 5380.8 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 24.6% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, The Netherlands, Spain, China, India, Japan, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The generative AI in pharmaceutical industry market is characterized by the convergence of advanced computational science and deep biological understanding. The entire drug development lifecycle is being reimagined through technologies such as de novo drug design, generative adversarial networks, and variational autoencoders. From initial target identification and hit identification to complex lead optimization, these tools are compressing R&D timelines.

- The use of high-performance computing and robotic lab automation is enabling phenotypic screening and automated chemical synthesis at an unprecedented scale. In later stages, AI-driven clinical trial optimization and pharmacovigilance, supported by natural language processing and federated learning, are enhancing efficiency and safety.

- A pivotal trend influencing boardroom strategy is the automation of medical and regulatory writing; with AI-driven clinical study report automation projected to reduce writer effort by up to 30%, executives are re-evaluating R&D budgets and resource allocation.

- This shift, combined with innovations in vocal biomarkers, drug repurposing, and protein engineering, marks a fundamental move towards a more predictive and efficient pharmaceutical industry.

What are the Key Data Covered in this Generative AI In Pharmaceutical Industry Market Research and Growth Report?

-

What is the expected growth of the Generative AI In Pharmaceutical Industry Market between 2025 and 2029?

-

USD 5.38 billion, at a CAGR of 26.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Method (Text generation, Image generation, and Audio generation), Application (Commercial, Drug discovery, Clinical development, Research and development, and Operations), Technology (Deep learning models, Natural language processing, Generative adversarial networks, Variational autoencoders, Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Accelerating drug discovery and development, Data privacy and security imperatives in era of accelerated innovation

-

-

Who are the major players in the Generative AI In Pharmaceutical Industry Market?

-

AstraZeneca Plc, Atomwise Inc., Bayer AG, BenevolentAI, BioXcel Therapeutics Inc., Deep Genomics Inc., Exscientia plc, Insilico Medicine, PathAI Inc., Recursion Pharmaceuticals Inc., Relay Therapeutics Inc., Sanofi SA, Schrodinger Inc., Shenzhen Jingtai Technology Co.Ltd and Valo Health

-

Market Research Insights

- The generative AI in pharmaceutical industry market is defined by rapid innovation and a shift towards data-centric operations. AI for personalized medicine is enabling patient-centered trial design, while machine learning for drug repurposing uncovers new value in existing compounds.

- Organizations are achieving significant efficiencies, with some reducing medical writing efforts by up to 30% and others mitigating over 80% of low-inventory risks through AI-optimized supply chain management. The technology facilitates deep learning in pharmacovigilance and powers generative chemistry platforms, moving beyond high-throughput screening alternatives.

- As adoption grows, so does the focus on AI compliance in pharmaceuticals and mitigating algorithmic bias in healthcare to ensure equitable outcomes. From AI-driven biomarker discovery and automated clinical trial design to enhancing immuno-oncology research, the market's dynamism is reshaping the entire value chain.

We can help! Our analysts can customize this generative ai in pharmaceutical industry market research report to meet your requirements.