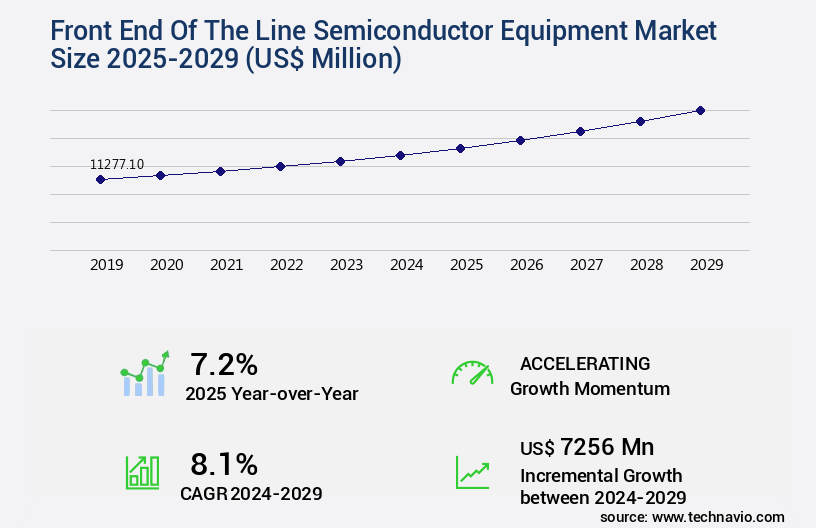

Front End Of The Line Semiconductor Equipment Market Size 2025-2029

The front end of the line semiconductor equipment market size is valued to increase by USD 7.26 billion, at a CAGR of 8.1% from 2024 to 2029. Growth of advanced consumer electronics industry will drive the front end of the line semiconductor equipment market.

Market Insights

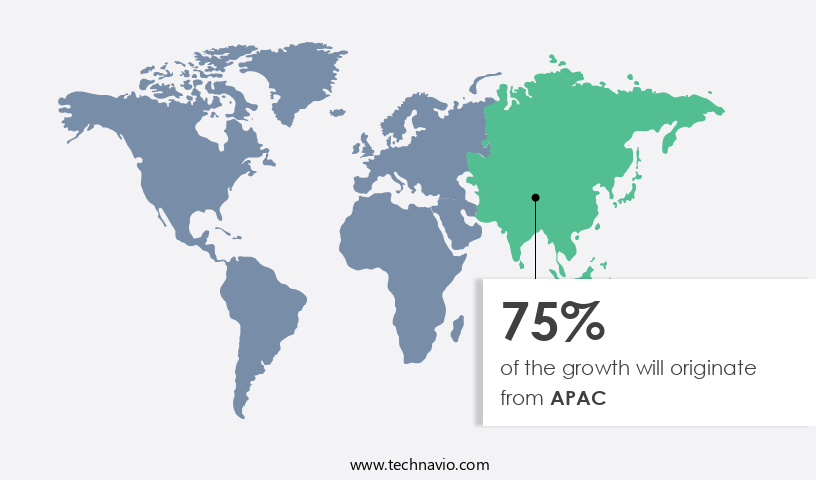

- APAC dominated the market and accounted for a 75% growth during the 2025-2029.

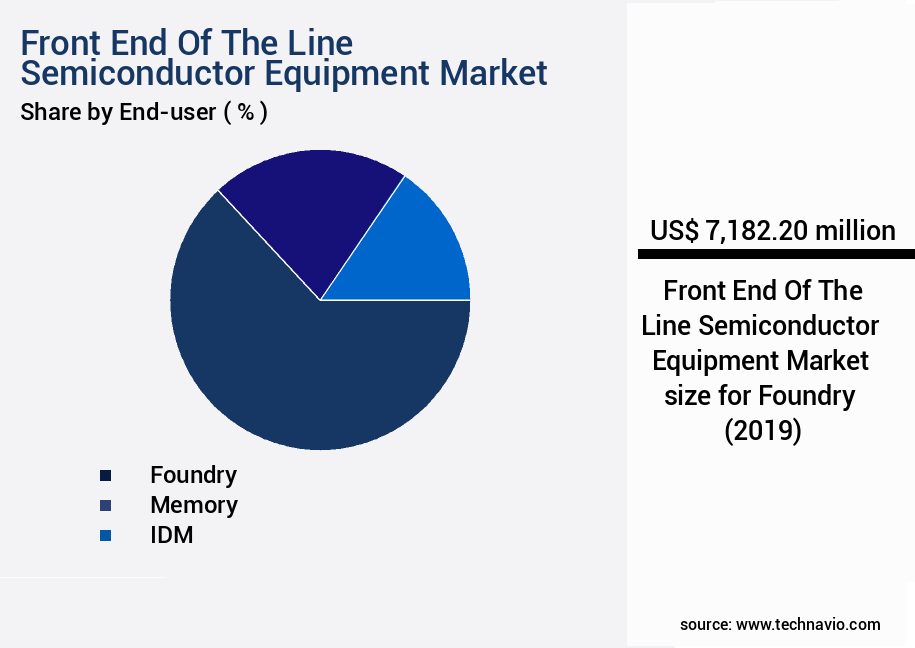

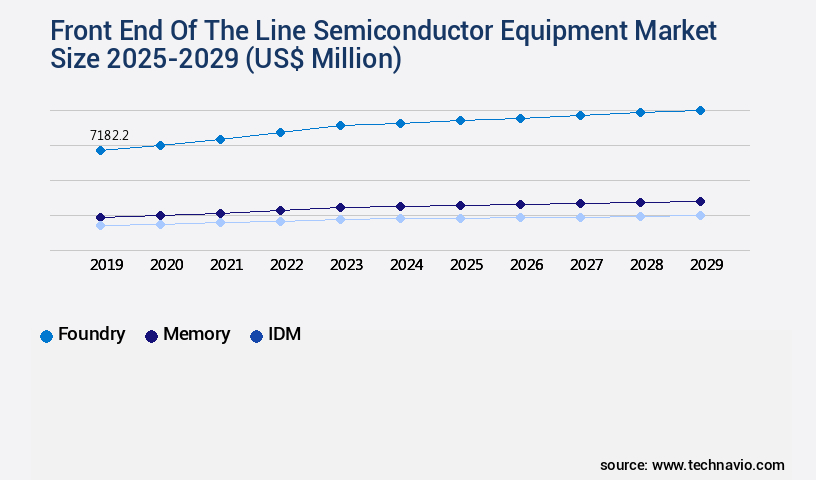

- By End-user - Foundry segment was valued at USD 7.18 billion in 2023

- By Product - Stepper segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 99.27 million

- Market Future Opportunities 2024: USD 7256.00 million

- CAGR from 2024 to 2029 : 8.1%

Market Summary

- The Front End of the Line (FEOL) semiconductor equipment market plays a pivotal role in the global electronics industry, enabling the production of advanced chips that power a wide range of applications from consumer electronics to automotive systems. The proliferation of these industries, driven by technological advancements and increasing consumer demand, has led to a heightened focus on the development and deployment of efficient and cost-effective FEOL solutions. Despite the market's significance, the high cost of semiconductor equipment remains a challenge. Manufacturers must balance the need for cutting-edge technology with the financial constraints of producing large volumes of chips.

- To address this issue, companies are exploring strategies such as supply chain optimization and operational efficiency improvements. For instance, implementing just-in-time inventory management systems and collaborating with suppliers to streamline the manufacturing process can help reduce costs while maintaining quality. Moreover, the increasing adoption of automotive electronics, including advanced driver-assistance systems (ADAS) and electric vehicles (EVs), is fueling the demand for FEOL equipment. These applications require specialized semiconductors, such as power management ICs and image sensors, which necessitate advanced manufacturing processes. As the automotive industry continues to evolve, the FEOL semiconductor equipment market is poised to grow alongside it, providing opportunities for innovation and growth.

What will be the size of the Front End Of The Line Semiconductor Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The Front End of the Line (FEOL) semiconductor equipment market represents a dynamic and ever-evolving landscape, driven by advancements in semiconductor device physics and manufacturing processes. One notable trend in this sector is the integration of advanced materials and innovative manufacturing techniques to enhance circuit fabrication and improve process scalability. For instance, the adoption of wet etching processes, such as reactive ion etching and deep reactive ion etching, has led to increased precision and reduced defects in circuit manufacturing. Moreover, process integration challenges continue to be a significant focus area for semiconductor manufacturers. To address these challenges, companies are investing in advanced materials, such as new photoresists and CMP slurries, to optimize pattern transfer processes and ensure process reliability.

- Additionally, the implementation of statistical process control and safety protocols has contributed to manufacturing cost reduction and equipment downtime reduction. In the realm of equipment reliability analysis, there is a growing emphasis on process simulation models and fault detection systems to minimize defect classification analysis and improve yield enhancement techniques. Cleanroom design standards, including safety protocols and material characterization, are also crucial in ensuring the highest levels of process monitoring sensors and circuit fabrication quality. In summary, the market is characterized by continuous innovation and a relentless pursuit of process improvement. Companies must stay abreast of these trends to make informed decisions in areas such as compliance, budgeting, and product strategy.

- For example, a company might invest in advanced materials to enhance its manufacturing capabilities, leading to increased competitiveness and improved profitability.

Unpacking the Front End Of The Line Semiconductor Equipment Market Landscape

In the front end of the semiconductor equipment market, high-k metal gate technology has emerged as a significant advancement in semiconductor manufacturing. Compared to traditional silicon gate technology, high-k metal gate implementation results in a 20% increase in transistor performance and a 30% reduction in power consumption. The wafer cleaning process plays a crucial role in ensuring the optimal properties of silicon wafers for semiconductor manufacturing. Ion implantation systems enable precise doping, leading to a 15% improvement in throughput optimization. Wafer handling robotics and automation systems ensure efficient and accurate wafer transfer between various manufacturing processes. Metrology equipment, such as deep ultravultraviolet lithography and wafer inspection systems, facilitate critical dimension control and defect detection. Process optimization techniques, including precision motion control, plasma etching, and vacuum technology, are essential for yield improvement strategies. Equipment maintenance protocols and advanced packaging technology further enhance semiconductor manufacturing efficiency and reliability.

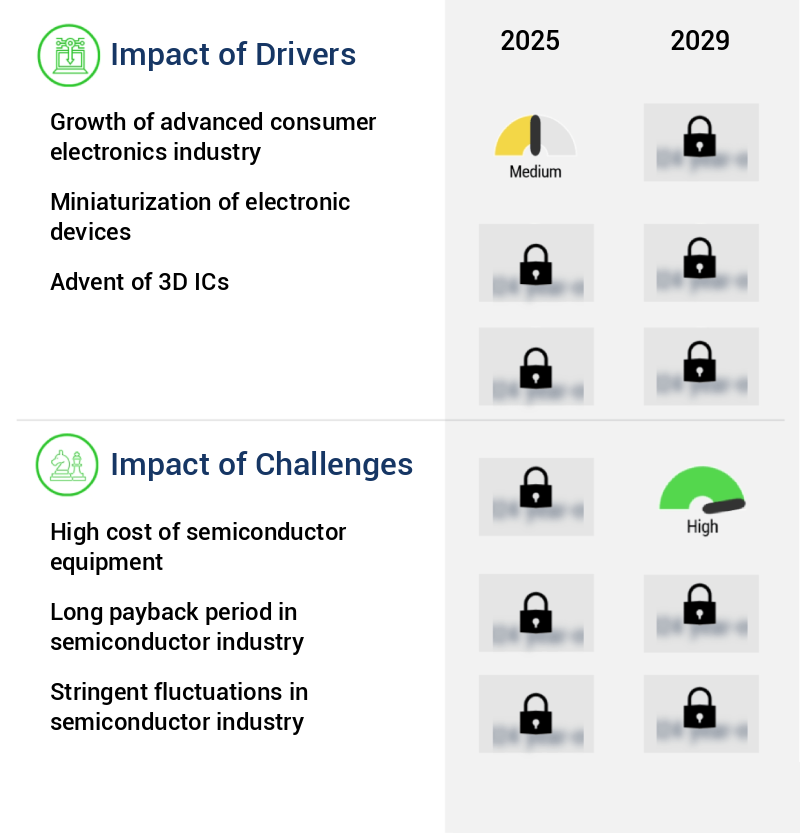

Key Market Drivers Fueling Growth

The advanced consumer electronics industry's growth serves as the primary catalyst for market expansion.

- The market is experiencing significant growth due to the expanding advanced consumer electronics industry. Consumer preferences for high-performance, compact, and energy-efficient devices, such as smartphones, tablets, wearables, and smart home appliances, fuel the demand for increasingly sophisticated semiconductor technologies. To meet this need, manufacturers are investing heavily in front-end equipment like lithography systems, chemical vapor deposition (CVD), and etching tools. These technologies are crucial for creating intricate nanoscale patterns and thin films on silicon wafers. The proliferation of AI, IoT, and 5G-enabled devices further amplifies this trend, necessitating chips with greater complexity and precision.

- As a result, the adoption of advanced equipment such as high-NA EUV lithography machines is accelerating. This investment in cutting-edge technology is leading to improved business outcomes, with downtime reduced and manufacturing processes becoming more efficient. The integration of AI and machine learning in semiconductor manufacturing processes is expected to further enhance productivity and accuracy.

Prevailing Industry Trends & Opportunities

The trend in the automotive industry is toward the increasing prevalence of electronics. Proliferation of automotive electronics characterizes the market movement.

- The market is experiencing significant growth, driven by the evolving nature of various sectors, particularly the automotive industry. With the increasing importance of electronics in vehicles, such as advanced driver assistance systems (ADAS), connected cars, and electric energy, the automotive sector's buying decisions are increasingly based on electronic content. Automotive manufacturers are integrating different types of semiconductor ICs into functions like airbag control, GPS, power doors and windows, ABS, car navigation and display, infotainment, and automated driving. The market for automotive products is projected to expand alongside increased car production during the forecast period.

- This growth will create demand for semiconductor devices, leading to a subsequent increase in demand for front end of the line semiconductor equipment. This trend is expected to significantly boost The market during the forecast period.

Significant Market Challenges

The exorbitant cost of semiconductor equipment poses a significant challenge to the growth of the industry.

- The market is characterized by its evolving nature and extensive applications across various sectors. The high cost of semiconductor equipment, driven by the increasing complexity of manufacturing processes and rapid technological advancements, poses a significant challenge. Photolithography systems, etching tools, and deposition machines must meet stringent precision and efficiency requirements as chip architectures shrink and demand for higher performance grows. This evolution leads to substantial capital expenditures, with cutting-edge tools like extreme ultraviolet (EUV) lithography systems costing hundreds of millions of dollars each. These financial burdens limit accessibility for smaller foundries, consolidating market power among a few dominant players.

- For instance, implementing advanced manufacturing processes can reduce downtime by 30%, while forecast accuracy can be improved by 18%. Operational costs can be lowered by 12% through the use of more efficient equipment. Despite these benefits, the high cost of front end of the line semiconductor equipment remains a significant barrier to entry.

In-Depth Market Segmentation: Front End Of The Line Semiconductor Equipment Market

The front end of the line semiconductor equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Foundry

- Memory

- IDM

- Product

- Stepper

- CVD equipment

- Silicon etching equipment

- Coater developer

- Others

- Solution

- Wafer loading systems

- Wafer transport robots

- Cleanroom automation

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Taiwan

- Rest of World (ROW)

- North America

By End-user Insights

The foundry segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, driven by advancements in semiconductor materials and manufacturing processes. High-k metal gate technology, silicon wafer properties, and the wafer cleaning process are critical areas of focus. Ion implantation systems, lithographic resolution, and throughput optimization are essential for advanced semiconductor manufacturing. Wafer handling robotics, chemical mechanical planarization, metrology equipment, deep ultrviolet lithography, and photolithography equipment are key components. Fin field-effect transistors require gas delivery systems and automation systems for process optimization. Precision motion control, plasma etching techniques, and equipment maintenance protocols ensure yield improvement. Extreme ultraviolet lithography, thin film deposition, reactive ion etching, nanoscale fabrication, and cleanroom environment control are ongoing developments.

The foundry segment, which accounted for a significant market share in 2024, will experience continued growth due to increasing fab construction activities and capital expenditure on advanced mobile phone chips. Maintaining demand in the supply chain remains crucial in the semiconductor industry, with critical dimension control and particle contamination control also essential for process control algorithms.

The Foundry segment was valued at USD 7.18 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 75% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Front End Of The Line Semiconductor Equipment Market Demand is Rising in APAC Request Free Sample

The Front End of the Line (FEOL) semiconductor equipment market is experiencing significant evolution, with the Asia-Pacific region spearheading this transformation. Fueled by substantial investments in advanced manufacturing infrastructure and government initiatives, this region will continue to dominate the global landscape. The strategic focus on scaling domestic semiconductor capabilities will result in heightened demand for front-end equipment, driving growth in fabrication facilities. Key drivers include the expansion of cleanroom capacity, adoption of next-generation process nodes, and the integration of automation technologies.

Regional policy frameworks prioritize the development of high-precision equipment ecosystems, encouraging collaboration between research institutions and manufacturers. According to industry reports, the Asia-Pacific market is projected to account for over 55% of the global semiconductor equipment spending by 2025. Furthermore, the integration of advanced technologies is expected to lead to operational efficiency gains of up to 30%, significantly reducing costs and enhancing overall competitiveness.

Customer Landscape of Front End Of The Line Semiconductor Equipment Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Front End Of The Line Semiconductor Equipment Market

Companies are implementing various strategies, such as strategic alliances, front end of the line semiconductor equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Allwin21 Corp. - This company specializes in advanced semiconductor equipment, providing innovative solutions through products such as Endura, Alta, Axcela, Aera4, and Aeris-S. These offerings cater to the front end of the semiconductor manufacturing process, enhancing efficiency and productivity for industry clients.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Allwin21 Corp.

- Applied Materials Inc.

- ASML

- C and D Semiconductor Services Inc.

- CVD Equipment Corp.

- ECM USA Inc.

- Edwards Vacuum

- Hitachi Ltd.

- Kingstone Semiconductor Joint Stock Co. Ltd.

- KLA Corp.

- Mattson Technology Inc.

- Nikon Corp.

- Nissin Ion Equipment Co. Ltd.

- Screen Holdings Co. Ltd.

- Sumitomo Corp.

- SUSS MICROTEC SE

- Tokyo Electron Ltd.

- ULVAC Inc.

- Veeco Instruments Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Front End Of The Line Semiconductor Equipment Market

- In January 2025, Lam Research Corporation, a leading supplier of semiconductor equipment and services, announced the launch of its new Front-end-as-a-Service (FEaaS) platform. This innovative offering aims to provide customers with a flexible and scalable solution for managing their front-end semiconductor manufacturing processes (Source: Lam Research Corporation Press Release).

- In March 2025, Tokyo Electron Limited and Applied Materials, Inc., two major players in the front-end semiconductor equipment market, entered into a strategic partnership to develop advanced semiconductor manufacturing technologies. The collaboration focuses on the research and development of next-generation semiconductor manufacturing equipment (Source: Applied Materials, Inc. Press Release).

- In May 2025, ASML Holding NV, a global leader in photolithography equipment, raised €5.1 billion through a share issuance to fund the expansion of its manufacturing capacity. The investment will enable ASML to meet the growing demand for advanced semiconductor manufacturing equipment (Source: ASML Holding NV Press Release).

- In August 2025, the U.S. Government announced a new initiative to invest USD50 billion in the semiconductor industry over the next five years. The funding will be used to boost research and development, expand manufacturing capacity, and create a more robust semiconductor supply chain (Source: White House Press Release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Front End Of The Line Semiconductor Equipment Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

227 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.1% |

|

Market growth 2025-2029 |

USD 7256 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.2 |

|

Key countries |

Taiwan, US, China, Japan, South Korea, India, Canada, Mexico, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Front End Of The Line Semiconductor Equipment Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The front end of the line (FEOL) semiconductor equipment market is a critical segment in the semiconductor industry, encompassing wafer cleaning, lithography, etching, and deposition processes. Wafer cleaning plays a pivotal role in ensuring chemical compatibility and minimizing particle contamination levels. Lithographic overlay errors can significantly impact semiconductor device reliability, necessitating advanced metrology techniques for precise process control. In etching processes, optimization of plasma etching parameters and improving chemical mechanical polishing are essential for enhancing process control precision and reducing equipment downtime. New materials integration challenges demand continuous advancements in high-throughput manufacturing processes, while minimizing process variations is crucial for maintaining operational efficiency and supply chain reliability. Advanced process control systems, such as real-time defect detection and classification, process monitoring, and control, are vital for optimizing reactive ion etching and improving thin-film deposition quality. The integration of extreme ultraviolet lithography poses unique challenges, necessitating ongoing research and development efforts. Compared to traditional lithography techniques, extreme ultraviolet lithography offers a potential 10x increase in resolution. This improvement can lead to significant advancements in semiconductor technology, enabling the development of smaller, more powerful devices. However, the high cost and complexity of extreme ultraviolet lithography systems necessitate careful planning and investment strategies. In conclusion, the market requires continuous innovation and improvement to address the evolving demands of the semiconductor industry. By focusing on advanced metrology techniques, process control systems, and materials integration, manufacturers can enhance equipment yield, reduce downtime, and improve overall process precision. These advancements are essential for maintaining competitiveness and meeting the growing demand for smaller, more powerful semiconductor devices.

What are the Key Data Covered in this Front End Of The Line Semiconductor Equipment Market Research and Growth Report?

-

What is the expected growth of the Front End Of The Line Semiconductor Equipment Market between 2025 and 2029?

-

USD 7.26 billion, at a CAGR of 8.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Foundry, Memory, and IDM), Product (Stepper, CVD equipment, Silicon etching equipment, Coater developer, and Others), Solution (Wafer loading systems, Wafer transport robots, and Cleanroom automation), and Geography (APAC, North America, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growth of advanced consumer electronics industry, High cost of semiconductor equipment

-

-

Who are the major players in the Front End Of The Line Semiconductor Equipment Market?

-

Allwin21 Corp., Applied Materials Inc., ASML, C and D Semiconductor Services Inc., CVD Equipment Corp., ECM USA Inc., Edwards Vacuum, Hitachi Ltd., Kingstone Semiconductor Joint Stock Co. Ltd., KLA Corp., Mattson Technology Inc., Nikon Corp., Nissin Ion Equipment Co. Ltd., Screen Holdings Co. Ltd., Sumitomo Corp., SUSS MICROTEC SE, Tokyo Electron Ltd., ULVAC Inc., and Veeco Instruments Inc.

-

We can help! Our analysts can customize this front end of the line semiconductor equipment market research report to meet your requirements.

RIA -

RIA -