Footwear Market Size 2026-2030

The footwear market size is valued to increase by USD 109.7 billion, at a CAGR of 4.3% from 2025 to 2030. Pervasive influence of athleisure and fusion of performance with style will drive the footwear market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 48% growth during the forecast period.

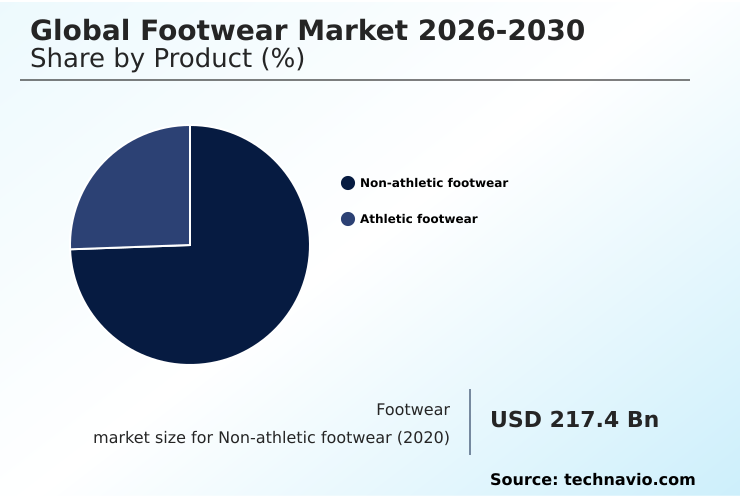

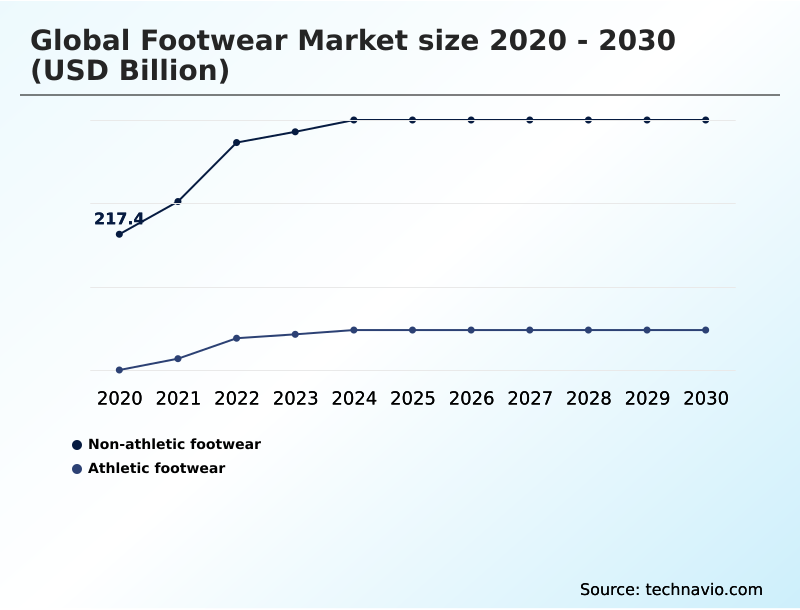

- By Product - Non-athletic footwear segment was valued at USD 337.5 billion in 2024

- By End-user - Men segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 289.8 billion

- Market Future Opportunities: USD 109.7 billion

- CAGR from 2025 to 2030 : 4.3%

Market Summary

- The footwear market is undergoing a significant transformation, driven by the convergence of fashion, technology, and sustainability. The deep influence of the athleisure movement continues to blur the lines between performance athletic footwear and casual lifestyle sneakers, creating strong demand for hybrid, multi-functional products.

- This shift is mirrored by a growing consumer insistence on ethical production standards and sustainable raw materials, pushing brands toward circular economy models and greater supply chain transparency. For example, a brand leveraging a direct-to-consumer model can utilize sales data to inform on-demand manufacturing at regional micro-factories, effectively reducing waste and mitigating the risks of logistical bottlenecks.

- This agile approach, powered by AI-driven recommendations and virtual try-on tools, allows for hyper-personalization at scale. However, the industry simultaneously grapples with challenges like production cost escalation and the need for robust intellectual property protection against sophisticated counterfeiting. Success hinges on balancing innovation with operational resilience and a genuine commitment to sustainability.

What will be the Size of the Footwear Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Footwear Market Segmented?

The footwear industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Non-athletic footwear

- Athletic footwear

- End-user

- Men

- Women

- Children

- Distribution channel

- Offline

- Online

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Product Insights

The non-athletic footwear segment is estimated to witness significant growth during the forecast period.

The non-athletic footwear segment is evolving beyond traditional categories, heavily influenced by the athleisure movement.

A significant shift in consumer purchasing behavior is compelling brands to create hybrid multi-functional footwear that merges classic aesthetics with the ergonomic footwear design principles of casual lifestyle sneakers.

This has spurred sustainable material innovation, with a focus on plant-based leather alternatives and other sustainable raw materials. To meet this demand, companies are increasingly adopting a direct-to-consumer model, which improves supply chain transparency.

Surveys indicate over 60% of consumers now prioritize comfort-centric features in formal wear, reinforcing the move toward performance technology integration. This evolution demands agile responses to both style and substance.

The Non-athletic footwear segment was valued at USD 337.5 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 48% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Footwear Market Demand is Rising in APAC Request Free Sample

The global landscape is led by APAC, which accounts for 48% of incremental growth, driven by rising disposable incomes and a mobile-first e-commerce ecosystem.

In North America, which represents 25% of the growth opportunity, the market is characterized by strong brand loyalty and a dominant sneaker culture influence, with a high demand for the luxury footwear segment.

Europe focuses on quality and ethical production standards, heavily influenced by regulations. Across these regions, a key challenge remains geopolitical instability risks, which can disrupt supply chains.

To counter this, some firms are exploring a nearshoring production strategy, with adoption of regional micro-factories in certain areas reducing logistical bottlenecks by up to 20%, showcasing a move towards more resilient operational models.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The modern footwear market is defined by the profound impact of athleisure on footwear design, which necessitates advanced technology integration in lifestyle footwear and even influences ergonomic design for formal shoes.

- This convergence is coupled with a strong consumer demand for ethical footwear, pushing the industry toward a circular economy in athletic footwear and the use of sustainable materials for non-athletic shoes. This shift is reinforced by strengthening sustainability regulations for footwear industry, including the rollout of digital product passports in fashion.

- To meet these evolving expectations, brands are adopting hyper-personalization with 3d printing and exploring the role of ai in footwear retail. A successful dtc strategy for footwear brands is crucial, often supported by regional micro-factories for customization that cater to trends amplified by the impact of social media on sneaker culture.

- Brands that have effectively implemented such localized production have reported a reduction in excess inventory by over 25% compared to traditional wholesale models. However, these opportunities are tempered by significant challenges of global footwear supply chains, including supply chain risks from geopolitical instability and the difficulty of managing rising production costs.

- Furthermore, the industry is constantly engaged in combating counterfeit luxury sneakers and protecting ip in online marketplaces to preserve brand value.

What are the key market drivers leading to the rise in the adoption of Footwear Industry?

- A key market driver is the pervasive influence of athleisure, which creates sustained demand for footwear that fuses high-performance functionality with sophisticated style.

- Market growth is primarily propelled by the enduring athleisure movement and the widespread adoption of digital technologies.

- The direct-to-consumer model has become a critical channel, enabling brands to control their narrative and margins, with some achieving profit improvements of up to 20%.

- This digital shift is enhanced by tools that improve the online shopping experience; for instance, the use of AI-powered virtual try-on tools has reduced online return rates by a reported 35% in pilot programs.

- These technologies not only boost consumer confidence but also provide valuable data that informs product development, from performance athletic footwear to casual lifestyle sneakers, making the digital ecosystem a core driver of innovation and sales.

What are the market trends shaping the Footwear Industry?

- A key market trend is the imperative for a circular economy, which is driving significant advancements in material innovation. This includes the development and adoption of sustainable inputs and end-of-life solutions.

- Key trends are reshaping the market, moving it toward a more sustainable and personalized future. The push for a circular economy is driving significant sustainable material innovation, with brands exploring advanced materials like bio-fabricated leathers. This shift is supported by on-demand manufacturing, which allows for greater customization and waste reduction.

- Brands using hyper-personalization manufacturing report a 25% increase in customer loyalty. Furthermore, the integration of advanced material science into both athletic and casual footwear has led to products with 15% greater durability, meeting consumer demand for both style and longevity. These trends indicate a move away from mass production toward more agile, responsible, and consumer-centric models.

What challenges does the Footwear Industry face during its growth?

- A primary challenge affecting industry growth is the need to navigate significant supply chain volatility and escalating production costs.

- The industry faces significant operational and reputational challenges. Supply chain volatility remains a primary concern, with unpredictable logistical bottlenecks and rising production cost escalation straining margins. Transportation costs in key trade lanes have increased by over 40%, directly impacting profitability. Concurrently, the threat from sophisticated counterfeiting and the prevalence of high-quality replicas requires constant investment in intellectual property rights protection.

- The fight against fakes costs the industry an estimated 10% of its annual revenue. Navigating these complexities, alongside rising consumer expectations for sustainability and transparency, defines the current competitive landscape and demands strategic resilience from all market participants.

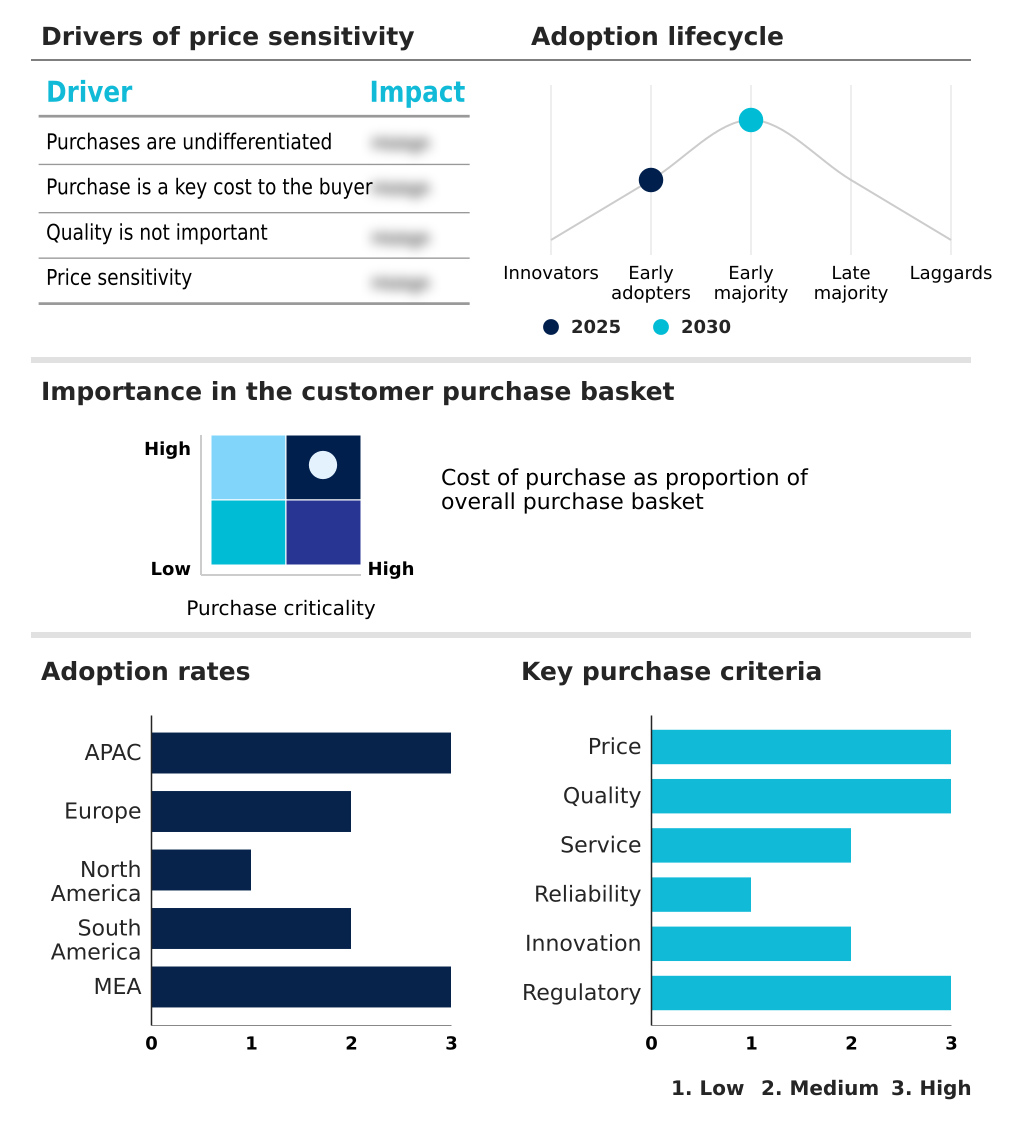

Exclusive Technavio Analysis on Customer Landscape

The footwear market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the footwear market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Footwear Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, footwear market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adidas AG - The vendor portfolio is centered on performance sports shoes and lifestyle sneakers, driven by innovation and global brand appeal to capture diverse consumer preferences.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adidas AG

- ASICS Corp.

- Brooks Sports Inc.

- Burberry Group Plc

- Dolce and Gabbana Srl

- FILA Holdings Corp.

- Geox S.p.A

- Hermes International SA

- Kering SA

- LVMH Moet Hennessy

- New Balance Athletics Inc.

- Nike Inc.

- PUMA SE

- Skechers USA Inc.

- Under Armour Inc.

- VALENTINO Spa

- VF Corp.

- Wolverine World Wide Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Footwear market

- In May, 2025, VF Corp. announced the rollout of a new unified e-commerce platform designed to create a seamless cross-brand shopping experience and leverage shared data analytics for improved personalization.

- In May, 2025, New Balance launched its NB Custom Fit program in flagship stores, featuring in-store 3D foot scanners to create biomechanical profiles for 3D-printing custom midsoles.

- In April, 2025, Kering announced a long-term partnership with a German biomechanics research institute to co-develop a new line of haute couture footwear engineered for optimal ergonomic support.

- In March, 2025, Adidas launched its Nomad Pro collection, featuring a modular design with independently replaceable soles and uppers, crafted from advanced lab-grown leather and recycled ocean plastics.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Footwear Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 288 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.3% |

| Market growth 2026-2030 | USD 109.7 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.1% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The footwear market is characterized by rapid innovation, driven by the persistent athleisure movement and the corresponding need for performance technology integration. A critical boardroom-level concern is aligning with emerging regulations, such as the digital product passport, which compels a strategic shift toward circular economy models and sustainable material innovation, including bio-fabricated leathers and algae-based foams.

- This is reshaping supply chains, where volatility and production cost escalation remain significant risks. In response, companies are leveraging a direct-to-consumer model, enhanced by virtual try-on tools and ai-powered recommendations, to enable hyper-personalization manufacturing. Adoption of additive manufacturing in regional micro-factories has enabled some firms to reduce lead times by over 40% for customized orders.

- This move toward on-demand production also addresses geopolitical instability risks and logistical bottlenecks. Simultaneously, the industry continues to invest in advanced material science and counterfeiting protection to safeguard intellectual property rights against high-quality replicas and mitigate e-commerce marketplace liability.

What are the Key Data Covered in this Footwear Market Research and Growth Report?

-

What is the expected growth of the Footwear Market between 2026 and 2030?

-

USD 109.7 billion, at a CAGR of 4.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Non-athletic footwear, and Athletic footwear), End-user (Men, Women, and Children), Distribution Channel (Offline, and Online) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Pervasive influence of athleisure and fusion of performance with style, Navigating supply chain volatility and escalating production costs

-

-

Who are the major players in the Footwear Market?

-

Adidas AG, ASICS Corp., Brooks Sports Inc., Burberry Group Plc, Dolce and Gabbana Srl, FILA Holdings Corp., Geox S.p.A, Hermes International SA, Kering SA, LVMH Moet Hennessy, New Balance Athletics Inc., Nike Inc., PUMA SE, Skechers USA Inc., Under Armour Inc., VALENTINO Spa, VF Corp. and Wolverine World Wide Inc.

-

Market Research Insights

- The market's dynamics are shaped by the powerful sneaker culture influence and the resulting demand for hybrid multi-functional footwear. This has pushed brands toward an omnichannel retail strategy that combines experiential retail concepts with seamless online experiences. Firms leveraging data-driven footwear customization have seen return rates drop by up to 30%, a significant improvement in operational efficiency.

- This personalization is increasingly achieved through bespoke shoe manufacturing and advancements like smart running shoes with integrated biometric sensors. Furthermore, implementing eco-friendly product lifecycle management and supply chain transparency has been linked to a 15% improvement in brand trust metrics, highlighting the growing importance of ethical production standards in consumer decisions.

We can help! Our analysts can customize this footwear market research report to meet your requirements.

RIA -

RIA -