North America Folding Carton Market Size 2025-2029

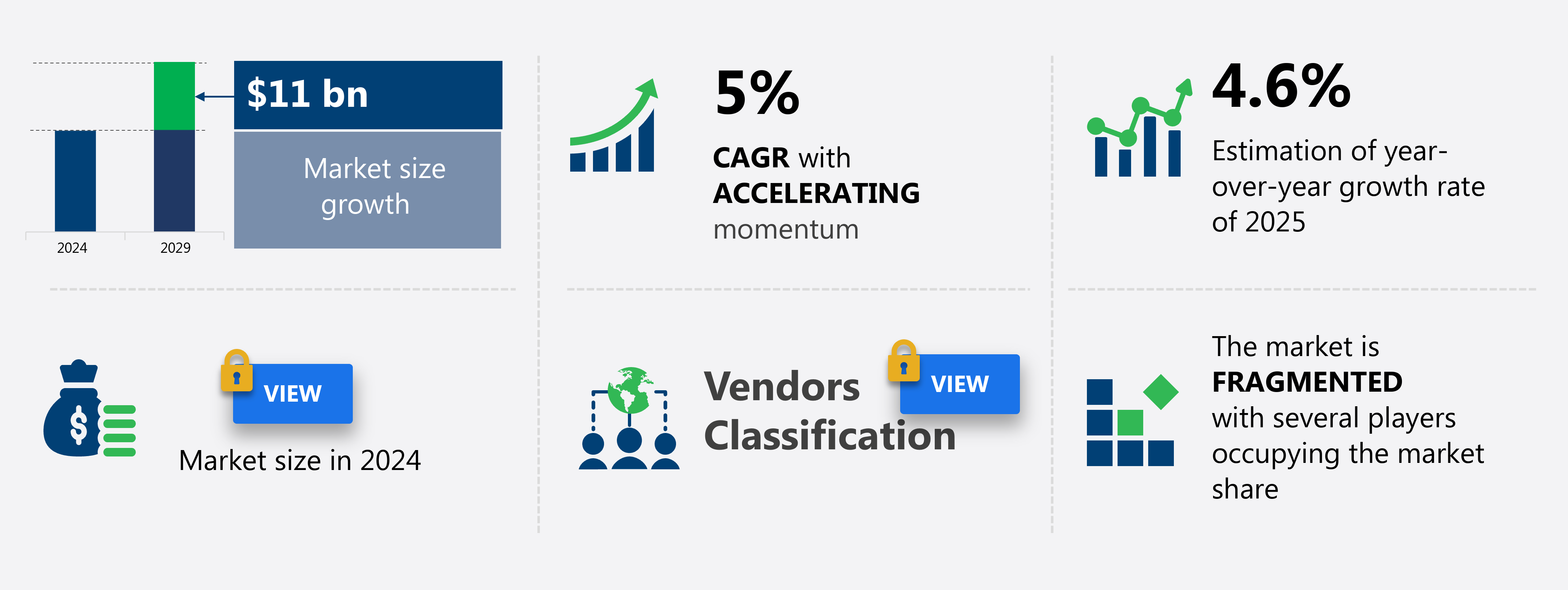

The folding carton market size in North America is forecast to increase by USD 11 billion at a CAGR of 5% between 2024 and 2029.

-

The folding carton market in North America is experiencing significant growth, driven by the increasing use of eco-friendly materials in packaging. Sustainability is a top priority for businesses, leading to a rise in demand for folding cartons made from renewable resources. Another market growth factor is the ongoing trend of mergers and acquisitions, as companies seek to expand their reach and capabilities in this competitive industry. However, the market faces challenges, including the volatility in prices of raw materials used in manufacturing folding cartons, such as paper and chemicals.

These price fluctuations can impact profitability and put pressure on manufacturers to find cost-effective solutions. The folding carton market in North America is experiencing steady growth, driven by increasing demand for packaging and advancements in digital printing. As the market continues to evolve, it's essential for businesses to stay informed about these trends and challenges to remain competitive and succeed in the folding carton industry.

What will be the Size of the market During the Forecast Period?

-

The folding carton market in North America is experiencing significant shifts as brands prioritize innovative packaging solutions to differentiate themselves in a crowded marketplace. Three-dimensional (3D) packaging design, enabled by digital printing technology, is gaining traction, offering consumers an unboxing experience. Brand protection and supply chain optimization are key concerns for folding carton manufacturers, leading to advancements in packaging security and cost optimization through automated packaging systems. Market research indicates that consumer insights drive packaging trends, with a focus on sustainability concerns and environmental regulations. Packaging suppliers are responding by investing in e-commerce growth and offering flexible packaging solutions such as stand-up pouches and flow wrapping. The market encompasses the production and distribution of containers made from paperboard. Folding cartons, available in diverse colors, sizes, and designs, cater to the needs of food, beverage, institutional, healthcare, household, electrical and electronic, e-commerce, tobacco, and other sectors.

Counterfeit prevention is a critical priority, with packaging design software and virtual reality technology playing a role in preventing counterfeit products. Packaging consultants and converters are leveraging packaging data and analytics to improve packaging efficiency and product protection. Augmented reality and artificial intelligence are also transforming the industry, offering new opportunities for product customization and personalization. Shrink wrapping and other traditional packaging methods continue to evolve, with innovations in materials and processes enhancing their value proposition. Overall, the folding carton market is a dynamic and innovative space, driven by consumer preferences, technological advancements, and regulatory requirements.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

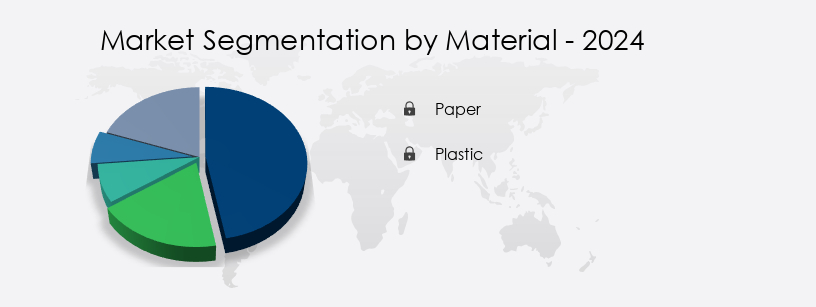

- Material

- Paper

- Plastic

- End-user

- Food and beverage products

- Homecare and personal products

- Healthcare products

- Tobacco products

- Others

- Type

- Standard

- Customized

- Geography

- North America

- US

- Canada

- Mexico

- North America

By Material Insights

- The paper segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth, particularly in the paper segment. This segment encompasses various types of paper, including kraft, recycled, virgin, and others. The eco-friendly and sustainable nature of paper is driving its demand, as there is increasing awareness and concern regarding the environmental impact of plastic packaging. The global annual plastic waste production has nearly doubled from 180 million tons in the early 2000s to around 400 million tons in 2024. Folding cartons made of paper are extensively used for packaging various products such as food and beverages, pharmaceuticals, cosmetics, and more. Print finishing plays a crucial role in enhancing the visual appeal of folding cartons. Millennials' stress levels and changing lifestyles have led to an increase in the consumption of ready-to-eat and frozen food, further boosting the market.

Technologies like digital printing and offset printing enable customization and personalization, while flexographic printing offers cost-effectiveness and high-speed production. Gift packaging and luxury packaging segments are also gaining popularity due to their ability to create brand experience. Retail packaging and shelf-ready packaging are essential for inventory management and supply chain efficiency. Durability testing and packaging compliance ensure the safety and integrity of the products during transportation and storage. Sustainable packaging, such as biodegradable materials and recycled content, is a growing trend as consumers demand eco-friendly solutions. Pharmaceutical packaging requires stringent regulations and high-security features, while food packaging must adhere to specific regulations and comply with food safety standards.

Beverage packaging, display packaging, and blister packaging cater to various industries and product types. Packaging design and graphics play a pivotal role in product branding and consumer appeal. High-speed packaging lines and automation improve production efficiency and reduce costs. Corrugated cardboard and stacking strength ensure the protection and transportation of fragile products. E-commerce packaging and tray packaging cater to the growing online shopping trend, while packaging software streamlines the entire process from design to production and distribution. Compression testing and drop testing ensure the durability and functionality of the packaging. Overall, the folding carton market is dynamic and evolving, driven by various factors such as consumer preferences, regulatory requirements, and technological advancements.

Get a glance at the market report of share of various segments Request Free Sample

Market Dynamics

The North America folding carton market is thriving, driven by demand for sustainable folding carton solutions and eco-friendly folding cartons. Custom folding cartons are gaining traction in the food and beverage folding carton market, pharmaceutical folding carton packaging, and e-commerce folding carton market, fueled by innovations like digital printing for folding cartons and personalized folding carton packaging. Biodegradable folding cartons North America and recyclable folding cartons align with sustainability goals, while anti-counterfeiting folding cartons and tamper-evident folding cartons ensure safety in pharmaceuticals. Retail-ready folding cartons and lightweight folding cartons cater to e-commerce needs. High-speed folder-gluers and automated folding carton production enhance efficiency, while smart folding cartons with QR codes elevate consumer engagement, shaping North America folding carton market trends.

Our North America Folding Carton Market researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of North America Folding Carton Market?

- Increasing use of eco-friendly materials in packaging is the key driver of the market. Eco-friendly folding carton packaging is gaining traction in various industries due to increasing consumer awareness and regulatory pressures. The use of recyclable, biodegradable, and reusable materials in packaging is essential for reducing environmental impact. Major brands, including Aldi, Coca-Cola, Nestle, Unilever, Tesco, and Procter & Gamble, are leading the way by reducing plastic packaging and setting sustainability goals. For instance, Coca-Cola aims to use 35% to 40% recycled material in primary packaging by 2035. Print finishing techniques, such as flexographic printing and packaging labels, are crucial for enhancing product branding and ensuring durability. Retail packaging, including gift packaging, requires high stacking strength to prevent damage during transportation and storage.

-

Pharmaceutical packaging, in particular, must meet stringent regulations for safety and sterility. High-speed packaging lines are essential for meeting the demand for eco-friendly folding cartons while maintaining efficiency. Folding carton manufacturers invest in advanced technologies to improve production speed and reduce waste. Durability testing is a critical aspect of the manufacturing process to ensure the cartons can withstand various conditions, such as temperature and humidity, during transportation and storage. The demand for eco-friendly folding cartons is driven by consumer preferences, regulatory requirements, and brand initiatives. Print finishing, durability testing, and high-speed packaging lines are essential for producing high-quality, sustainable folding cartons that meet the needs of various industries.

What are the market trends shaping the North America Folding Carton Market?

- Rise in mergers and acquisitions in folding carton market is the upcoming trend in the market. The market experiences moderate competition, which has led to an increase in strategic mergers and acquisitions among market participants. This competition arises from the evolving technologies and the growing demand for folding cartons from various industries, including healthcare and food and beverage. Companies are utilizing mergers and acquisitions to expand their market reach and customer base in response to the increasing demand. Additionally, established firms are expected to strengthen their market presence through similar strategies due to the moderate competition in the market.

-

Folding carton boxes, produced through folding and gluing processes, are essential for e-commerce packaging and tray packaging applications. Packaging software and packaging machinery are crucial for the production and design of folding carton boxes, which must adhere to packaging compliance regulations and be suitable for shelf-ready packaging.

What challenges does North America Folding Carton Market face during the growth?

- Volatility in prices of raw materials used in manufacturing folding cartons is a key challenge affecting the market growth. Folding cartons, a form of packaging widely used for consumer goods and food products, are primarily manufactured using paper pulp as the primary raw material. Paperboard, a thicker and more durable variant of paper, is the typical material used in their production. The cost of manufacturing folding cartons is influenced by the price fluctuations of paperboard, which can increase due to the imbalance between its demand and supply. Digital printing technology has revolutionized the packaging industry, enabling customized graphics and designs on folding cartons. Sustainability is a key trend in the market, with biodegradable materials gaining popularity for their eco-friendly attributes.

-

Packaging inserts, such as leaflets and promotional materials, can be integrated into folding cartons to enhance the consumer experience. Luxury packaging applications, which require high-quality finishes and custom printing, represent a significant market segment. Inventory management is crucial for businesses to maintain optimal stock levels and reduce wastage. Packaging testing is essential to ensure product safety and compliance with regulations. The shift towards sustainable packaging solutions, including those made from renewable resources and biodegradable materials, is a significant market driver. As consumer preferences evolve, companies are focusing on innovative and eco-friendly packaging solutions to meet their demands.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast , partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Amcor Plc - This company specializes in producing a range of folding cartons for various industries, including pharmaceuticals, healthcare, food, spirits, and personal care.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- American Carton Co.

- Arkay

- Astro Box Corp.

- BC Box Manufacturing Ltd.

- Bell Packaging Ltd.

- Cross Country Box Co. Inc.

- Diamond Packaging

- Edelmann Group

- Graphic Packaging Holding Co.

- Great Little Box Co. Ltd.

- Imperial Printing and Paper Box Mfg. Co.

- Industrial Development Co. sal

- International Paper Co.

- JohnsByrne

- Koch Industries Inc.

- Oliver Inc.

- Rinaldi Printing Co.

- Service Die Cutting and Packaging Corp.

- Smurfit Westrock plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Folding Carton Market In North America

- In January 2024, international packaging giant, Smurfit Kappa, announced the launch of its innovative, sustainable folding carton solution, "Greenbox," made entirely from renewable resources (Smurfit Kappa Press Release, 2024). This new product development underscores the growing market demand for eco-friendly packaging solutions.

- In March 2025, Ball Corporation and WestRock Company entered into a strategic partnership to expand their folding carton businesses, combining their resources and expertise to cater to a broader customer base and enhance their product offerings (Ball Corporation Press Release, 2025). This collaboration represents a significant shift in the competitive landscape of the folding carton market.

- In August 2024, DS Smith Plc, a leading provider of sustainable packaging solutions, completed the acquisition of Fibre Box Corporation, a major North American folding carton manufacturer, significantly expanding its presence in the region (DS Smith Plc Press Release, 2024). The acquisition strengthened DS Smith's position as a global player in the folding carton market.

Research Analyst Overview

The folding carton market continues to evolve, shaped by dynamic market conditions and diverse applications across various sectors. Supply chain management plays a crucial role in ensuring the seamless delivery of high-quality cartons. Compression testing is essential to assess the durability of these packages, while recycled materials offer sustainability benefits. Packaging automation and offset printing streamline production processes, enabling high-speed packaging lines to meet increasing demand. Beverage packaging and display packaging showcase the creativity of folding carton designs, enhancing brand identity. Eco-friendly packaging, including biodegradable materials and sustainable practices, responds to consumer preferences. Folded cartons undergo rigorous testing, including drop testing and packaging regulations compliance, to ensure product safety and integrity. The market's future holds opportunities for innovation in smart folding cartons, smart packaging, clinical monitoring, printed electronics, and QR codes. Consumer packagings, anti-grease barriers, aluminum, plastic inner packaging, food-safe colors, varnishes, and stockpiling are essential considerations for companies in the market.

Brand identity is a significant consideration, with custom printing and luxury packaging options catering to diverse market needs. Box sizes and styles adapt to the unique requirements of consumer goods, food packaging, and pharmaceutical industries. Inventory management software and packaging design tools facilitate efficient production and design processes. Shelf-ready packaging and e-commerce packaging cater to the growing importance of retail and online sales channels. Packaging machinery and folding and gluing techniques ensure the production of high-quality cartons. The folding carton market's continuous evolution reflects the industry's commitment to innovation and adaptation. From product branding and box styles to packaging automation and eco-friendly solutions, the market remains an exciting and dynamic space.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

191 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5% |

|

Market growth 2025-2029 |

USD 11 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.6 |

|

Key countries |

US, Canada, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -