India Flexible Packaging Market Size 2025-2029

The India flexible packaging market size is forecast to increase by USD 17.49 billion at a CAGR of 12.7% between 2024 and 2029. The market is experiencing significant growth, driven by the rising logistics costs and the increasing preference for lightweight and convenient packaging solutions. This trend is particularly evident in the widespread adoption of stand-up pouches, which offer improved product protection, extended shelf life, and reduced transportation costs.

Major Market Trends & Insights

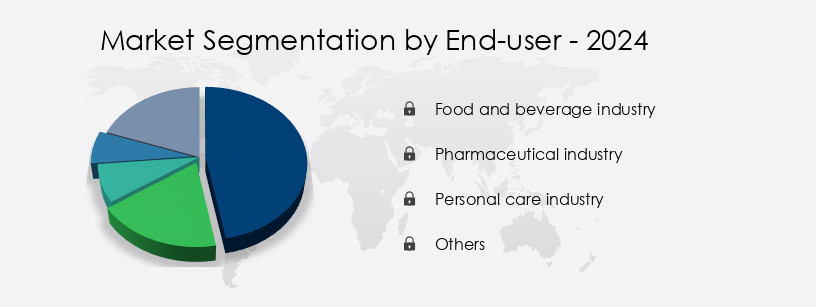

- Based on the End-user, the food and beverage industry segment led the market and was valued at USD 8.64 billion of the global revenue in 2022.

- Based on the Material, the plastic segment accounted for the largest market revenue share in 2022.

Market Size & Forecast

- Market Opportunities: USD 112.53 Billion

- Future Opportunities: USD 17.49 Billion

- CAGR (2024-2029): 12.7%

The market faces challenges as well, with the recent implementation of a new recycling policy increasing operational costs for companies. This policy, aimed at promoting sustainable packaging practices, requires manufacturers to bear the responsibility for post-consumer waste management. As a result, companies must invest in advanced recycling technologies or form strategic partnerships to remain competitive in the market.

To capitalize on these opportunities and navigate the challenges effectively, market participants should focus on innovation, sustainability, and collaboration. By investing in research and development, adopting eco-friendly materials, and forging alliances with waste management companies, businesses can differentiate themselves and meet the evolving demands of consumers and regulators.

What will be the size of the India Flexible Packaging Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The market continues to demonstrate dynamic growth, driven by the expanding applications across various sectors such as food and beverage, pharmaceuticals, and consumer goods. Packaging line automation and package integrity testing are key focus areas, ensuring cost effectiveness and enhancing product quality. Packaging equipment selection, material compatibility assessment, and printing press maintenance are essential elements of the production process. Flexible packaging design, with a focus on supply chain traceability and consumer packaging preferences, is increasingly important for brand differentiation. Packaging material recycling and waste management are crucial aspects of sustainability, with industry growth expected to reach 12% annually.

- Material certifications and packaging sustainability metrics are gaining significance, driving innovations in rollstock material handling and packaging production lines. Polymer film selection, durability testing, and ink adhesion testing are critical for product protection and tamper evidence. Flexible packaging inspection, process optimization strategy, and packaging line integration are essential for maintaining product quality and ensuring regulatory compliance. The flexible packaging industry is continually evolving, offering exciting opportunities for material suppliers and innovators.

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Food and beverage industry

- Pharmaceutical industry

- Personal care industry

- Others

- Material

- Plastic

- Paper

- Aluminum

- Product

- Pouches

- Bags

- Films and wraps

- Others

- Geography

- APAC

- India

- APAC

By End-user Insights

The food and beverage industry segment is estimated to witness significant growth during the forecast period. The segment was valued at USD 8.64 billion in 2022. It continued to the largest segment at a CAGR of 6.71%.

The Indian flexible packaging market is experiencing significant growth due to the increasing consumption of packaged food and beverages. Convenience is a key factor driving this trend, particularly in metropolitan cities where young working professionals prefer fast, processed food. According to the Indian Government, the worker population ratio has risen from 50.9% in 2019-2020 to 52.9% in 2021-2022. Rising disposable income also contributes to this growth. Flexible packaging converters are focusing on thermal sealing performance and modified atmosphere packaging to ensure product freshness and shelf life extension. Packaging design software is being utilized to optimize supply chain efficiency and reduce waste.

Multilayer film structures and seal strength measurement are essential for ensuring product protection during transportation and storage. E-commerce packaging design is a growing area of focus, with vacuum packaging techniques used to maintain product quality during transit. Lightweight packaging design is also a priority to reduce shipping costs and minimize environmental impact. Recyclable packaging materials are increasingly being adopted to address sustainability concerns. Automated packaging machinery is being used to increase production efficiency and improve product consistency. Quality control procedures, including barrier properties testing and material handling systems, are essential for maintaining product integrity. Flexographic printing quality is also crucial for brand recognition and consumer appeal.

The Indian flexible packaging market is expected to grow at a rate of 10% annually, with innovation in areas such as lamination process optimization, digital printing technology, and high-speed packaging lines driving this growth. For instance, a leading flexible packaging converter reported a 15% increase in sales due to the adoption of advanced packaging technologies.

The Food and beverage industry segment was valued at USD 8.06 billion in 2019 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is witnessing significant growth due to the increasing demand for lightweight, convenient, and cost-effective packaging solutions. Flexible packaging material properties, such as high barrier protection, printability, and versatility, make it an ideal choice for various industries, including food, beverages, pharmaceuticals, and consumer goods. Advanced flexible packaging technology is driving innovation in this sector, with sustainable flexible packaging options gaining popularity. High-barrier flexible packaging films are in high demand due to their ability to extend product shelf life and reduce waste. Automated flexible packaging machinery and flexible packaging design software solutions are improving production efficiency and reducing costs. Flexible packaging material sourcing strategies and waste management solutions are crucial considerations for businesses looking to optimize their supply chain. Sustainable sourcing of raw materials and implementing efficient waste management practices are essential to minimize environmental impact.

Quality control measures and best practices in flexible packaging design are essential to ensure product safety and consumer satisfaction. Innovative flexible packaging applications, such as stand-up pouches, laminated films, and flexible containers, are transforming the industry. New technologies in the flexible packaging industry, such as smart packaging and biodegradable films, are addressing sustainability concerns and enhancing consumer experience. The impact of flexible packaging on the environment is a critical issue, and safety regulations for flexible packaging ensure that the industry adheres to strict standards. Testing methods for flexible packaging materials are essential to ensure product quality and safety. Optimizing flexible packaging supply chain and production lines through automation and digitalization are key strategies for businesses to stay competitive. Flexible packaging material recyclability is a growing concern, and the industry is exploring new ways to make packaging more sustainable and eco-friendly.

What are the India Flexible Packaging Market drivers leading to the rise in adoption of the Industry?

- The increasing logistics costs in India have led companies to transition towards more flexible packaging solutions, serving as the primary market driver.

- The Indian flexible packaging market faces significant logistics challenges, with logistics costs accounting for approximately 16% of the country's GDP. This is significantly higher than the logistics costs in developed countries like the US and Germany, which range between 8%-10% of their GDP. Transportation costs, which make up 30-40% of the total logistics expense, are a major contributor to these high costs. Over 70% of freight in India is transported by road, leading to increased expenses due to fuel costs, poor road conditions, and traffic congestion.

- For instance, a study revealed that the transportation of goods from Delhi to Mumbai, a distance of approximately 1,500 kilometers, can take up to 10 days due to these factors. Despite these challenges, the flexible packaging industry in India is expected to grow at a robust rate, with estimates suggesting a 12% increase in sales by 2026.

What are the India Flexible Packaging Market trends shaping the Industry?

- The increasing use of stand-up pouches is becoming a notable trend in the market. This packaging solution is gaining popularity due to its convenience and sustainability benefits.

- The market is witnessing significant growth due to the increasing demand for lightweight, portable, and tamper-evident packaging solutions. Companies are innovating to meet this demand, offering aesthetically pleasing and functional packaging. One such innovation is the stand-up pouch, which has gained popularity in the food industry. Weighing an average of 5% of the total weight of a glass bottle, these pouches offer a substantial reduction in weight, making them highly portable. Moreover, they are replacing cans for storing processed food, further increasing their adoption.

- The market for flexible packaging in India is expected to grow robustly, with an estimated 15% increase in demand in the next year. This growth is driven by the convenience and cost-effectiveness of flexible packaging solutions compared to traditional alternatives.

How does India Flexible Packaging Market face challenges during its growth?

- The implementation of the new recycling policy in India poses a significant challenge for companies in the industry by increasing their operational costs, potentially hindering industry growth.

- Flexible packaging, primarily composed of non-degradable plastics, poses significant environmental challenges due to high labor and equipment costs associated with disposal and recycling. The multi-layered nature of packaging solutions like pouches makes separation of layers a labor-intensive process or necessitates expensive machinery investments. In response to increasing concerns over landfill issues and recyclability, governments and environmental organizations are imposing regulations. For instance, under the Plastic Waste Management Rules, companies introducing new plastic products are mandated to establish waste management systems.

- According to industry reports, the market is projected to grow at a robust 15% annually, driven by the increasing demand for convenience and on-the-go consumption. Despite this growth, the industry must address the environmental challenges associated with flexible plastic disposal and recycling to maintain sustainability and stakeholder confidence.

Exclusive India Flexible Packaging Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- Berry Global Inc.

- Bilcare Ltd.

- Constantia Flexibles Group GmbH

- Cosmo Films Ltd.

- Garware Hi Tech Films Ltd.

- Huhtamaki Oyj

- Jindal Poly Films Ltd.

- Multiflex Packaging India

- Nichrome Packaging Solutions

- Packone Solutions LLP

- Paharpur 3P

- Polyplex Corp. Ltd

- Pouch Makers Canada Inc.

- SOLOS POLYMERS PVT. LTD.

- Sonoco Products Co.

- Tetra Pak International SA

- TCPL Packaging Ltd

- UFlex Ltd.

- Uma Polymers Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Flexible Packaging Market In India

- In January 2024, Amcor, a global packaging company, announced the expansion of its flexible packaging facility in Tamil Nadu, India. This expansion aimed to increase the production capacity of the plant by 30%, catering to the growing demand for flexible packaging in the region (Amcor Press Release, 2024).

- In March 2024, Tetra Pak, a leading food processing and packaging solutions company, entered into a strategic partnership with Gujarat Cooperative Milk Marketing Federation Ltd (GCMMF), India's largest dairy cooperative, to develop and launch eco-friendly flexible packaging solutions for milk and dairy products (Tetra Pak Press Release, 2024).

- In May 2024, UFlex, a global flexible packaging solutions provider, secured a significant investment of INR 1,500 crore from Aditya Birla Group to expand its flexible packaging business in India and globally (Business Standard, 2024).

- In February 2025, the Indian government announced the 'Plastic Waste Management Rules, 2025', mandating a 75% extended producer responsibility (EPR) for plastic packaging waste, which is expected to drive the growth of the market due to the increasing focus on sustainable packaging solutions (Ministry of Environment, Forest and Climate Change, 2025).

Research Analyst Overview

The market continues to evolve, driven by the increasing demand for innovative and sustainable packaging solutions across various sectors. Flexible packaging converters are at the forefront of this transformation, leveraging advanced technologies to enhance thermal sealing performance and develop multilayer film structures for modified atmosphere packaging. Packaging design software plays a crucial role in this dynamic landscape, enabling companies to optimize supply chain operations and extend shelf life through vacuum packaging techniques and lightweight design. Seal strength measurement and barrier properties testing are essential components of quality control procedures, ensuring the integrity of packaging and maintaining product protection.

E-commerce packaging design is another area of growth, with automated packaging machinery streamlining processes and reducing waste. Recyclable packaging materials, such as biodegradable films, are gaining popularity, aligning with industry expectations of a 10% CAGR growth rate in the flexible packaging market. For instance, a leading flexible packaging converter successfully implemented a lamination process optimization project, resulting in a 15% increase in production efficiency and a 10% reduction in packaging costs. This success story underscores the potential for continuous improvement and innovation in the flexible packaging industry. Barrier film technology, digital printing, and high-speed packaging lines are other key trends shaping the market, with companies focusing on improving packaging material sourcing, flexographic printing quality, and material handling systems to meet evolving consumer demands.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Flexible Packaging Market in India insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 12.7% |

|

Market growth 2025-2029 |

USD 17.49 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

11.4 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across India

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch