Europe Fleet Management Market Size 2025-2029

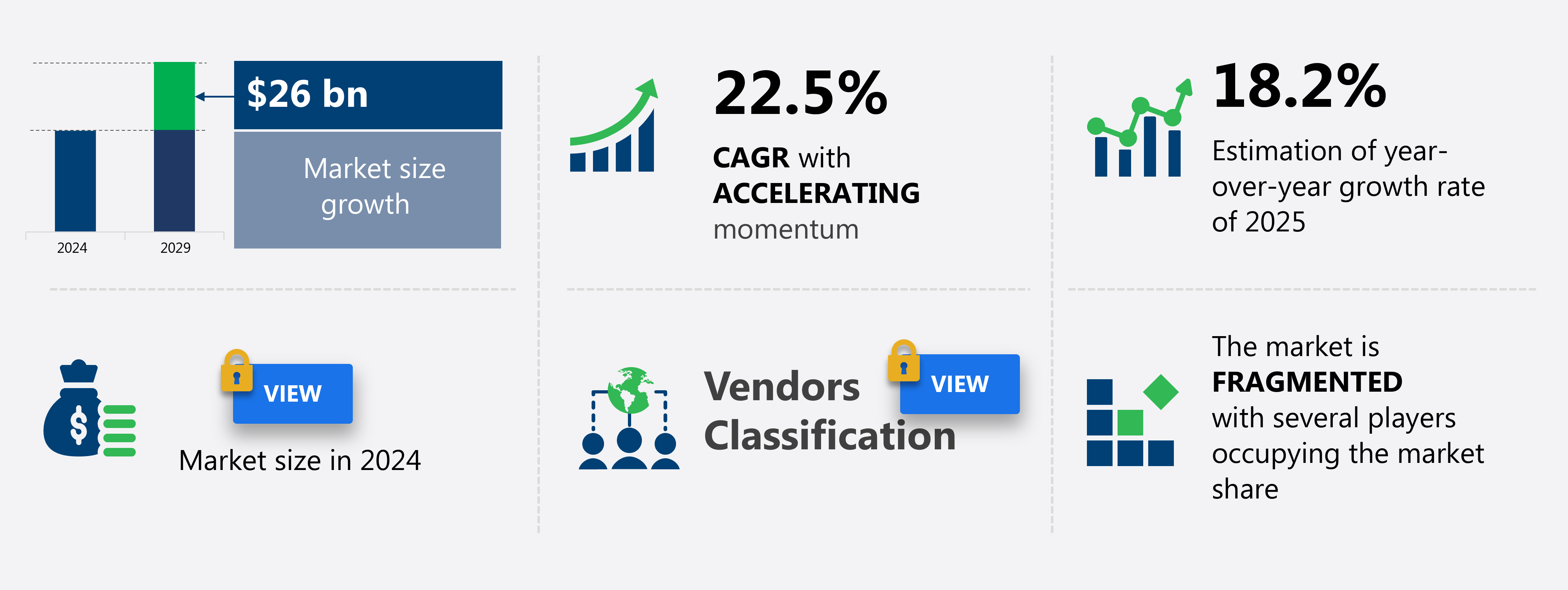

The fleet management market in Europe size is forecast to increase by USD 26 billion at a CAGR of 22.5% between 2024 and 2029.

-

The fleet management market is experiencing significant growth, driven by the increasing focus on data-driven efficiency and cost savings. Another key trend is the adoption of electric vehicles (EVs) as part of fleet strategies, in response to growing environmental concerns and regulatory pressures. However, the high cost of on-premises software solutions remains a challenge for many organizations, leading to a shift towards cloud-based solutions that offer greater flexibility and affordability.

-

As these trends continue to shape the market, fleet management companies must stay agile and innovative to meet the evolving needs of their clients. With the rise of connected vehicles and the Internet of Things (IoT), real-time data is increasingly being used to optimize fleet operations, reduce fuel consumption, and improve vehicle maintenance.

What will be the Size of the market During the Forecast Period?

In the dynamic fleet management market, IoT sensors and remote diagnostics play a pivotal role in optimizing vehicle performance and reducing maintenance costs. Machine learning algorithms analyze big data from these sensors to predict potential issues, enabling proactive repair management and improved service level agreements. Fleet renewal, driven by emission monitoring and carbon footprint reduction initiatives, is a significant trend. Insurance integration and ROI analysis are key considerations in the adoption of hybrid vehicles and alternative fuels. Sustainability initiatives, such as AI-powered analytics for driver training and electric vehicle integration, are shaping the industry's future.

Cost analysis, lifecycle cost analysis, incentive programs, and parts inventory management are essential elements of effective procurement and supplier management. Regulatory compliance, safety regulations, contract management, and predictive modeling are crucial aspects of fleet management, with blockchain technology offering potential solutions for transparency and security.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

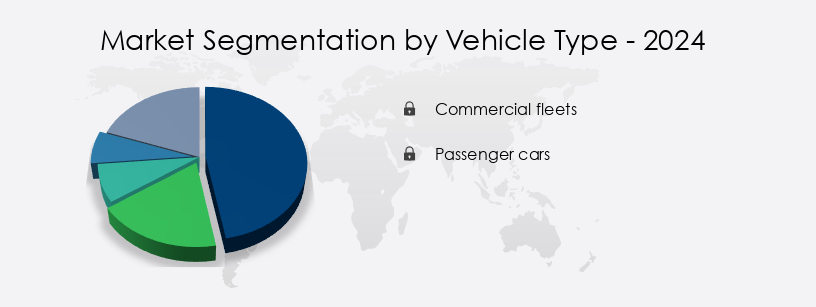

- Vehicle Type

- Commercial fleets

- Passenger cars

- Technology

- Commercial telematics hardware

- Software

- Connectivity technologies

- End-user

- Transportation and logistics

- Construction

- Energy and utilities

- Manufacturing

- Retail and e-commerce

- Geography

- Europe

- France

- Germany

- Italy

- UK

- Europe

By Vehicle Type Insights

The Commercial fleets segment is estimated to witness significant growth during the forecast period. The European fleet management market is experiencing significant growth, driven by the expansion of e-commerce and the increasing demand for efficient last-mile delivery. This market caters to a diverse range of commercial vehicles, including trucks, vans, and specialized models. Fleet management software is increasingly being adopted to optimize operations, enhance regulatory compliance, and improve route planning. Telematics, GPS tracking, and vehicle diagnostics technology are becoming more prevalent, leading to increased efficiency and cost savings. Moreover, there is a growing emphasis on sustainability and the integration of electric commercial vehicles into fleets, as corporations prioritize eco-friendly solutions to meet environmental objectives and regulations.

A cloud-based platform is essential for managing these complex operations, offering real-time location tracking, idle time monitoring, fuel management, asset tracking, accident reporting, maintenance scheduling, customer service, mobile applications, web portals, user-friendly interfaces, data analytics, better asset utilization, integration with ERP systems, speed monitoring, fuel efficiency, compliance monitoring, integration with CRM, performance reporting, security features, driver scorecards, reporting capabilities, vehicle diagnostics, customizable dashboards, and cost savings.

The market's evolution is further shaped by the integration of API, enabling seamless data exchange between systems, and real-time alerts for enhanced safety, driver safety, and performance monitoring. The use of GPS tracking and vehicle diagnostics technology also contributes to improved driver behavior and increased productivity.

Get a glance at the market report of share of various segments Request Free Sample

Market Dynamics

Our Europe Fleet Management Market researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Europe Fleet Management Market?

-

Growing focus on efficient use of data to enhance fleet management is the key driver of the market. The European fleet management market is experiencing growth due to the importance placed on data efficiency for optimizing fleet operations. Fleet operators gain access to substantial data on daily fleet activities, including fuel consumption, traveled routes, and work order execution. By integrating APIs and utilizing cloud-based platforms, operators can effectively manage this data in real-time, minimizing manual errors.

-

Fleet management systems offer essential features such as real-time location tracking, idle time monitoring, fuel management, asset tracking, accident reporting, and maintenance scheduling. These systems enable fleet operators to make informed decisions quickly and efficiently, improving overall fleet performance. Moreover, user-friendly interfaces, mobile applications, and web portals provide easy access to critical fleet information, enhancing customer service and streamlining communication between fleet managers and drivers. By automating fleet management processes, operators can focus on strategic decision-making and maintaining a well-maintained, productive fleet.

What are the market trends shaping the Europe Fleet Management Market?

-

Increase in EV adoption is the upcoming trend in the market. The market is experiencing significant growth due to the increasing adoption of electric vehicles (EVs) and government initiatives to reduce emissions and promote sustainable transport. Governments, including Germany and France, have offered substantial subsidies and tax incentives for EV adoption, compelling fleet operators to integrate electric vehicles into their operations. Consequently, there is a heightened demand for specialized EV fleet management solutions. These solutions offer real-time monitoring of EV battery status, charging station optimization, and route planning that considers EV range constraints.

-

Companies like Geotab and ChargePoint lead the EV fleet management systems sector, enabling businesses to effectively manage their electric vehicle assets while maximizing cost savings and environmental benefits. Key features of these solutions include reporting capabilities, vehicle diagnostics, customizable dashboards, mileage tracking, improved driver retention, improved compliance, data encryption, route optimization, real-time alerts, data visualization, and Eld integration. These solutions provide fleet operators with the tools necessary to optimize their operations and make data-driven decisions.

What challenges doesEurope Fleet Management Market face during the growth?

-

High cost of on-premises software is a key challenge affecting the market growth. The fleet management market faces the challenge of increasing costs associated with on-premises software solutions. These costs include licensing, installation, maintenance, hardware, customization, and training. On-premises fleet management software solutions offer enhanced security with a firewall and greater customization compared to cloud-based alternatives. However, they necessitate a skilled IT team for management and dedicated personnel for operation.

-

After implementation, regular upgrades are required to remain current with market trends and integrate with advanced technologies such as data analytics, AI, and blockchain. Furthermore, fleet management software solutions play a crucial role in ensuring driver safety, asset utilization, and compliance monitoring. Performance reporting, speed monitoring, fuel efficiency, and driver scorecards are essential features for optimizing fleet operations. Integration with ERP and CRM systems streamlines business processes and improves overall efficiency.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast , partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

AB Volvo - The company provides fleet management solutions through Volvo Connect software, enhancing operational efficiency and optimizing resources for businesses.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB Volvo

- ABAX UK Ltd.

- AddSecure Group AB

- Aeromark Communications Ltd.

- AREALCONTROL GmbH

- Astrata Europe BV

- Bridgestone Corp.

- Caterpillar Inc.

- Fleet Complete

- Frotcom International

- G4S Telematix

- Geotab Inc.

- Inseego Corp.

- Karooooo Ltd.

- Mercedes Benz Group AG

- MiX Telematics Ltd.

- Targa Telematics S.p.A.

- TraXall International

- Trimble Inc.

- Verizon Communications Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Fleet Management Market In Europe

- In January 2024, Volvo Group, a leading truck and bus manufacturer, launched its new connected services platform, Volvo Fleet Services, aimed at enhancing fleet management for commercial customers. This offering integrates real-time vehicle data, predictive maintenance, and fuel management tools (Volvo Group Press Release, 2024).

- In March 2024, Daimler Trucks and Mercedes-Benz announced a strategic partnership with Microsoft to develop and deploy a cloud-based fleet management solution. This collaboration leverages Microsoft's Azure platform and aims to improve fleet efficiency, reduce operating costs, and enhance safety (Daimler Trucks & Buses Press Release, 2024).

- In May 2024, Geotab, a global provider of IoT and connected transportation solutions, raised USD120 million in a funding round led by Siemens AG's Next47 venture capital arm. This investment will support Geotab's continued growth and expansion into new markets (Geotab Press Release, 2024).

- In April 2025, the European Union introduced new regulations on CO2 emissions from heavy-duty vehicles. These rules mandate a 15% reduction in CO2 emissions by 2025 and a 30% reduction by 2030. Fleet managers will need to adopt advanced technologies, such as electric and hybrid vehicles and fleet optimization software, to meet these targets (European Commission Press Release, 2025).

Research Analyst Overview

In the dynamic and ever-evolving fleet management market, technology continues to play a pivotal role in optimizing operations and enhancing productivity across various sectors. Real-time location tracking, idle time monitoring, fuel management, asset tracking, and accident reporting are just a few of the essential functions that have become indispensable for businesses seeking to streamline their fleet operations. Cloud-based platforms with user-friendly interfaces offer seamless integration with ERP and CRM systems, enabling better asset utilization and improved customer service. Mobile applications and web portals provide real-time access to performance reporting, vehicle diagnostics, and customizable dashboards. Enhanced safety features, such as driver safety, data analytics, and compliance monitoring, are integrated into these systems to ensure optimal performance and regulatory compliance.

Real-time alerts, data visualization, and ELD integration offer valuable insights into fleet operations, enabling proactive decision-making and increased productivity. Subscription models offer cost savings and flexibility, while data privacy and security features ensure the protection of sensitive information. Automated reporting, dispatch management, and work order management further streamline processes, reducing fuel consumption and improving efficiency. GPS tracking and vehicle diagnostics provide valuable data for optimizing routes, reducing idle time, and monitoring driver behavior. Integration with third-party applications, such as performance reporting and vehicle diagnostics, offers additional functionality and enhanced capabilities. In summary, the fleet management market is characterized by continuous innovation and the integration of advanced technologies to meet the evolving needs of businesses.

From real-time location tracking and fuel management to data analytics and compliance monitoring, these solutions offer significant benefits in terms of cost savings, improved efficiency, and enhanced safety. The Fleet Management Market in Europe is evolving swiftly, driven by a focus on safety, efficiency, and real-time control. Advanced driver behavior monitoring systems help reduce accidents and operational costs, while comprehensive vehicle tracking system provide actionable insights across diverse fleets. Seamless API integration ensures smooth connectivity between software platforms and hardware components, enhancing automation and analytics. With increasing demand for mobility, intuitive mobile application and centralized web portal are becoming the norm for fleet operations. A key differentiator in this market is a userfriendly interface that empowers fleet managers to make informed decisions quickly and effectively.

The Fleet Management Market in Europe is evolving with a sharp focus on sustainability and operational efficiency. Technologies like over-the-air updates streamline maintenance and keep vehicle software current without downtime. With rising climate awareness, minimizing the environmental impact of fleets is becoming a top priority. Companies are investing in hybrid vehicle integration to reduce emissions while maintaining performance. Strategic procurement management and smart vehicle selection play a critical role in aligning fleet capabilities with business needs. At the heart of these efforts lies the pursuit of optimal return on investment, balancing cost, compliance, and carbon footprints.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Fleet Management Market in Europe insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

197 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 22.5% |

|

Market growth 2025-2029 |

USD 26 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

18.2 |

|

Key countries |

Germany, UK, France, Italy, and Rest of Europe |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -