Dump Truck and Mining Truck Market Size 2024-2028

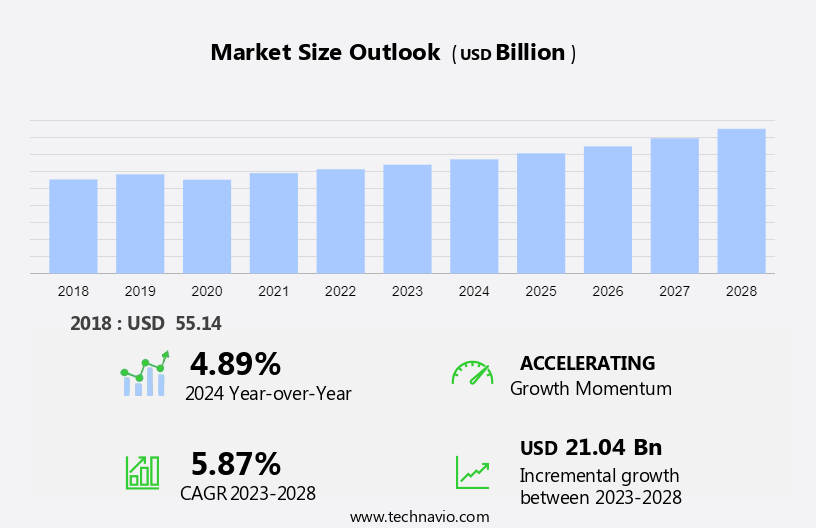

The dump truck and mining truck market size is forecast to increase by USD 21.04 billion at a CAGR of 5.87% between 2023 and 2028. The market is experiencing significant growth, driven by the increasing adoption of autonomous and semi-autonomous technologies. These advanced systems enable improved efficiency, productivity, and safety in mining and construction operations. Additionally, the integration of advanced safety features, such as collision avoidance systems and load sensing technologies, further enhances the safety and reliability of these vehicles.

However, challenges persist in optimizing powertrain systems to address stringent fuel efficiency and emissions standards. This market analysis report delves into these trends and challenges, providing valuable insights into the future of the dump truck and mining truck industry.

Market Analysis

The global mining industry relies heavily on heavy-duty vehicles, particularly mining trucks, for the transportation of minerals and ores from mines to processing plants. Dump trucks are a crucial part of this transportation infrastructure. These trucks come in various types, including Rigid Dump Trucks, Articulated Dump Trucks, Rear Dump Trucks, Side Dump Trucks, and Roll-off Dump Trucks. Mining companies use these trucks to transport gravel, sand, iron ore, and other minerals. Mining trucks are transitioning from Internal Combustion Engine to electric power trains to reduce sulfur emissions and meet emission regulations. Telematics is also being integrated into mining trucks to improve operational efficiency and productivity. The global mining truck market is expected to grow significantly due to the increasing demand for mining activities and infrastructure development. Electric mining trucks are gaining popularity due to their energy-efficient nature and minimal environmental impact. The market is expected to witness significant growth in the coming years as mining companies continue to invest in automation and energy-efficient vehicles.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

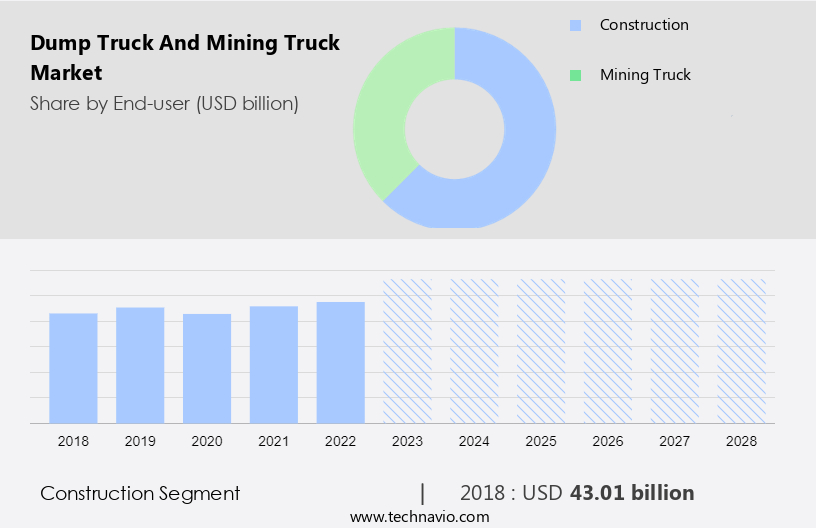

- Construction

- Mining truck

- Vehicle Type

- Internal combustion

- Electric

- Geography

- APAC

- China

- India

- North America

- US

- Europe

- Germany

- South America

- Middle East and Africa

- APAC

By End-user Insights

The construction segment is estimated to witness significant growth during the forecast period. In the global mining industry, Mining Trucks play a pivotal role in transporting minerals and ores from mining sites to processing facilities and construction infrastructure projects. Mining companies rely heavily on these powerful vehicles for efficient material handling and transportation. With the increasing emphasis on emission regulations, there is a growing trend towards the adoption of electric power trains, telematics, and energy-efficient vehicles in the mining sector. For instance, Phillips & Temro Industries offer electric mining trucks that reduce carbon impact and sulfur emissions. Dump trucks, including rigid dump trucks, articulated dump trucks, rear dump trucks, side dump trucks, and roll-off dump trucks, are integral to the mining and construction industries. Rigid dump trucks, such as the Hitachi EH 3500AC-3 with a nominal payload of 181 tons and engine power of 1,491-1,510 KW, are commonly used in the construction industry.

Mining trucks are also utilized for transporting gravel, sand, iron ore, and other materials to construction sites. Infrastructural developments and automation are driving the demand for advanced mining trucks. Digitalization of vehicles and the integration of robotic technology are expected to further enhance their efficiency and productivity. Off-road dump trucks and on-road dump trucks cater to different applications, with the former being used in mining and quarrying operations and the latter for transportation on public roads. Engine capacity and maintenance are crucial factors in the selection of mining trucks, with regulations playing a significant role in shaping the market landscape.

Get a glance at the market share of various segments Request Free Sample

The construction segment accounted for USD 43.01 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

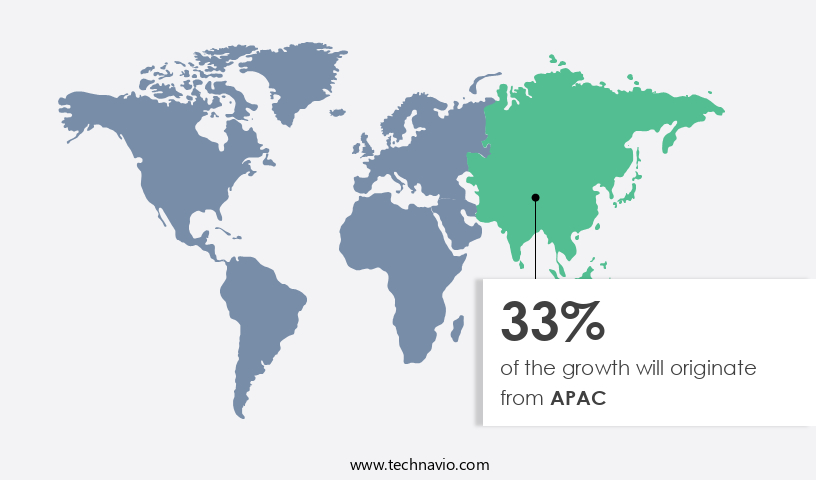

APAC is estimated to contribute 33% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The global mining industry's expansion, driven by infrastructure development and the extraction of minerals and ores in the APAC region, fuels the demand for Mining Trucks. Mining companies rely on these vehicles to transport gravel, sand, iron ore, and other resources from mining sites to construction projects. The APAC region, particularly China, India, and Southeast Asian countries, are rich in natural resources, making the demand for Mining Trucks concentrated. Emission regulations have led to the adoption of electric power trains and telematics in Mining Trucks. Rigid Dump Trucks, Articulated Dump Trucks, Underground Mining Vehicles, and various types of Dump Trucks, including Rear Dump Trucks, Side Dump Trucks, and Roll-off Dump Trucks, are being upgraded to meet carbon impact reduction targets.

Mining and transportation infrastructure developments necessitate the use of energy-efficient vehicles and automation. Engine capacity and digitalization of vehicles are essential considerations for Mining Trucks. Phillips & Temro Industries and other leading manufacturers cater to this growing demand, offering a range of Internal Combustion and Electric Mining Trucks. Regulations governing mining and transportation industries continue to evolve, with a focus on reducing sulfur emissions and improving safety. The market for Mining Trucks is expected to grow significantly, driven by the need for efficient and sustainable transportation solutions.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The growing adoption of autonomous and semi-autonomous technologies in dump trucks and mining trucks is the key driver of the market. In the global mining industry, Mining Trucks play a pivotal role in transporting minerals and ores from mining sites to processing facilities. Dump trucks, specifically, are essential for hauling gravel, iron ore, sand, and other materials. Mining companies are increasingly investing in advanced technologies to enhance the performance and efficiency of their dump trucks and mining trucks. Autonomous and semi-autonomous technologies are being integrated into these vehicles to improve safety and productivity. These technologies enable trucks to operate with minimal human intervention, reducing the risk of accidents and injuries caused by human error. They also allow for continuous operation without the need for driver breaks, increasing operational efficiency.

Moreover, these technologies optimize routes, speeds, and payloads, maximizing efficiency and throughput in mining and construction operations. Real-time monitoring, tracking, and management of dump truck and mining truck fleets are also made possible through these advanced technologies. Fleet managers can remotely monitor vehicle performance, location, fuel consumption, and maintenance needs, enabling proactive decision-making and optimization of fleet operations. Emission regulations are driving the adoption of energy-efficient vehicles, such as those with electric power trains, in the mining industry. Telematics and digitalization of vehicles are also becoming increasingly important for optimizing fleet operations and reducing carbon impact. Rigid Dump Trucks, Articulated Dump Trucks, Underground Mining Vehicles, and various types of Dump Trucks, including Rear Dump Trucks, Side Dump Trucks, and Roll-off Dump Trucks, are all being upgraded with these advanced technologies.

Infrastructural developments and maintenance regulations are also influencing the mining truck market. Phillips & Temro Industries and other leading mining equipment manufacturers are investing in research and development to produce more efficient, productive, and environmentally friendly mining trucks. The future of the mining truck market lies in automation, energy-efficient vehicles, and the integration of robotic technology.

Market Trends

Integration of advanced safety features in dump trucks and mining trucks is the upcoming trend in the market. The global mining industry relies heavily on Mining Trucks for the transportation of minerals and ores from mining sites to processing facilities. Mining companies integrate various types of Mining Trucks, including Rigid Dump Trucks, Articulated Dump Trucks, Underground Mining Vehicles, and Off-road and On-road dump trucks, into their operations. With increasing emission regulations, there is a growing trend towards the adoption of Electric power trains and energy-efficient vehicles in the mining sector. Advancements in technology have led to the integration of Telematics, collision avoidance systems, and blind spot detection systems in Mining Trucks. These systems utilize sensors, cameras, and radar technology to enhance safety and productivity.

For instance, collision avoidance systems detect obstacles, vehicles, and pedestrians in the path of the truck, providing warnings and automatic braking or trajectory adjustments to prevent accidents. Blind spot detection systems monitor blind spots around the truck and alert operators to potential hazards, increasing awareness and reducing the risk of collisions. In addition, the mining industry is witnessing infrastructural developments, with a focus on automation and digitalization of vehicles. These advancements include the integration of robotic technology and engine capacity enhancements. Regulations governing carbon impact and sulfur emissions continue to evolve, further driving the need for energy-efficient and eco-friendly Mining Trucks.

Phillips & Temro Industries and other leading manufacturers are responding to these trends by introducing innovative solutions, such as Electric Mining Trucks and advanced engine technologies, to meet the evolving needs of the mining industry.

Market Challenge

Concerns associated with powertrain optimization in dump trucks and mining trucks is a key challenge affecting the market growth. In the global mining industry, mining trucks play a crucial role in transporting minerals and ores from extraction sites to processing facilities. Mining companies rely on various types of mining trucks, including rigid dump trucks, articulated dump trucks, and underground mining vehicles, to efficiently move large volumes of gravel, iron ore, sand, and other materials. However, with increasing focus on emission regulations, there is a growing demand for energy-efficient vehicles, such as electric mining trucks, to reduce carbon impact. Powertrain optimization in mining trucks and dump trucks is essential to hit a balance between performance and fuel efficiency. This involves enhancing the engine, transmission, and drivetrain systems to improve vehicle performance while minimizing fuel consumption.

However, increasing engine power and torque to meet performance requirements can result in higher fuel consumption and increased wear and tear on powertrain components. Telematics and automation technologies, such as the digitalization of vehicles and robotic technology, are being integrated into mining trucks to optimize performance and reduce maintenance costs. Rear dump trucks, side dump trucks, and roll-off dump trucks are also used for the transportation of various materials in construction sites and demolition wastage. Phillips & Temro Industries and other leading mining equipment manufacturers are focusing on developing energy-efficient powertrains and optimizing engine capacity to meet the demands of the mining industry while complying with emission regulations. Infrastructural developments and maintenance regulations also play a significant role in the market growth of mining trucks and dump trucks.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

BELAZ HOLDING - The company offers dump truck and mining truck such as Belaz mining dump trucks with hydromechanical transmission named Belaz 7540A series, dumpers series 7547, dump truck series 7544.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aramine

- Ashok Leyland Ltd.

- Atlas Copco AB

- Bell Equipment Ltd.

- Caterpillar Inc.

- China FAW Group Co. Ltd.

- Deere and Co.

- DUX Machinery Corp.

- Hitachi Ltd.

- Iveco Group NV

- J C Bamford Excavators Ltd.

- Komatsu Ltd.

- Liebherr International Deutschland GmbH

- SANY Group

- Scania AB

- Volvo Car Corp.

- Xuzhou Construction Machinery Group Co. Ltd.

- Zoomlion Heavy Industry Science and Technology Co. Ltd.

- Mercedes Benz Group AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The mining industry relies heavily on Dump Trucks and Mining Trucks for the transportation of minerals and ores from mines to construction sites or processing facilities. These vehicles play a crucial role in the mining value chain, enabling the efficient extraction and transportation of resources such as gravel, sand, iron ore, and other materials. Mining companies invest in various types of Dump Trucks, including Rigid Dump Trucks, Articulated Dump Trucks, Underground Mining Vehicles, and different types like Rear Dump Trucks, Side Dump Trucks, and Roll-off Dump Trucks.

Further, the choice of vehicle depends on factors such as terrain, payload capacity, and the specific requirements of the mining operation. Emission regulations are driving the adoption of energy-efficient vehicles and alternative powertrains, such as Electric and Internal Combustion engines, in the mining industry. Telematics and automation technologies are also increasingly being integrated into Dump Trucks and Mining Trucks to improve productivity, maintenance, and safety. Phillips & Temro Industries and other leading manufacturers are focusing on developing energy-efficient, automated, and digitally advanced vehicles to cater to the evolving needs of the mining industry. Infrastructural developments and regulations continue to shape the market for Dump Trucks and Mining Trucks, with a focus on reducing carbon impact and improving safety and efficiency.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

156 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.87% |

|

Market growth 2024-2028 |

USD 21.04 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.89 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 33% |

|

Key countries |

US, China, Australia, India, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Aramine, Ashok Leyland Ltd., Atlas Copco AB, BELAZ HOLDING, Bell Equipment Ltd., Caterpillar Inc., China FAW Group Co. Ltd., Deere and Co., DUX Machinery Corp., Hitachi Ltd., Iveco Group NV, J C Bamford Excavators Ltd., Komatsu Ltd., Liebherr International Deutschland GmbH, SANY Group, Scania AB, Volvo Car Corp., Xuzhou Construction Machinery Group Co. Ltd., Zoomlion Heavy Industry Science and Technology Co. Ltd., and Mercedes Benz Group AG |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -