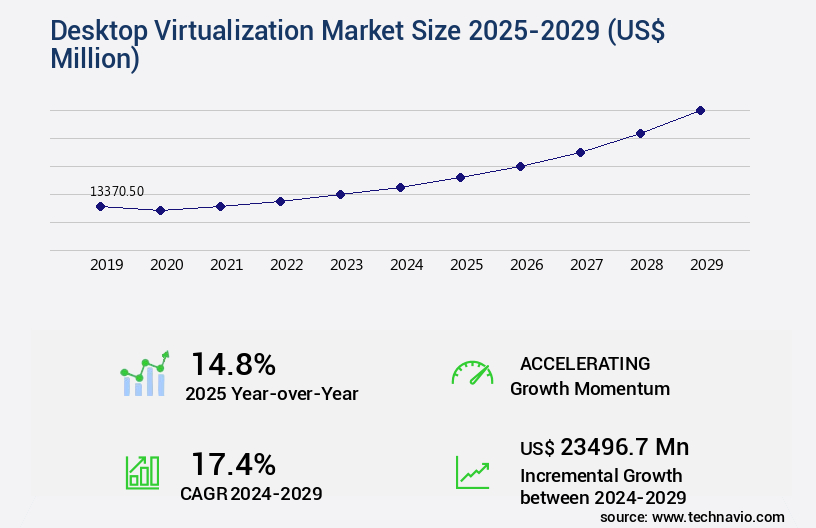

Desktop Virtualization Market Size 2025-2029

The desktop virtualization market size is valued to increase by USD 23.5 billion, at a CAGR of 17.4% from 2024 to 2029. Growing adoption of cloud-based VDI for SMEs will drive the desktop virtualization market.

Market Insights

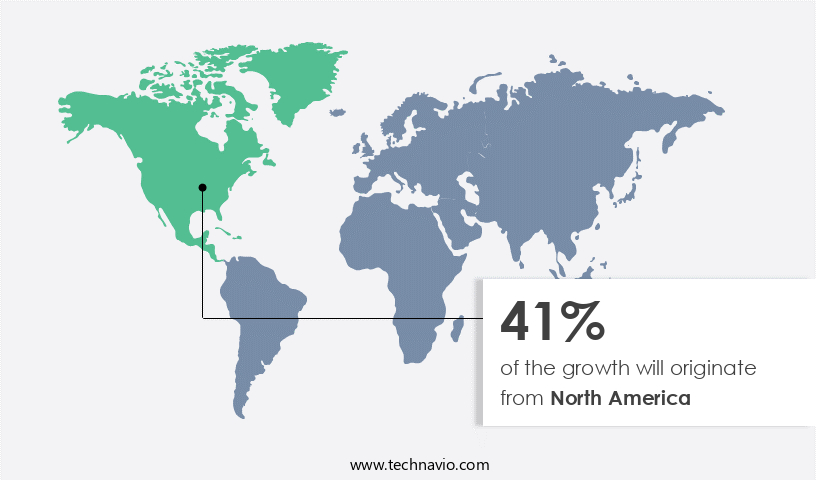

- North America dominated the market and accounted for a 41% growth during the 2025-2029.

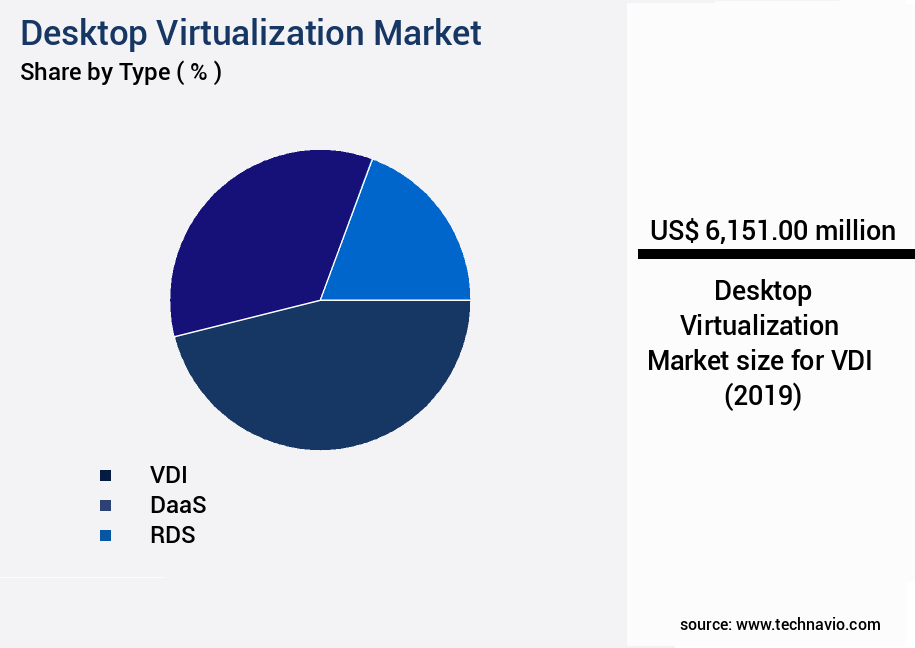

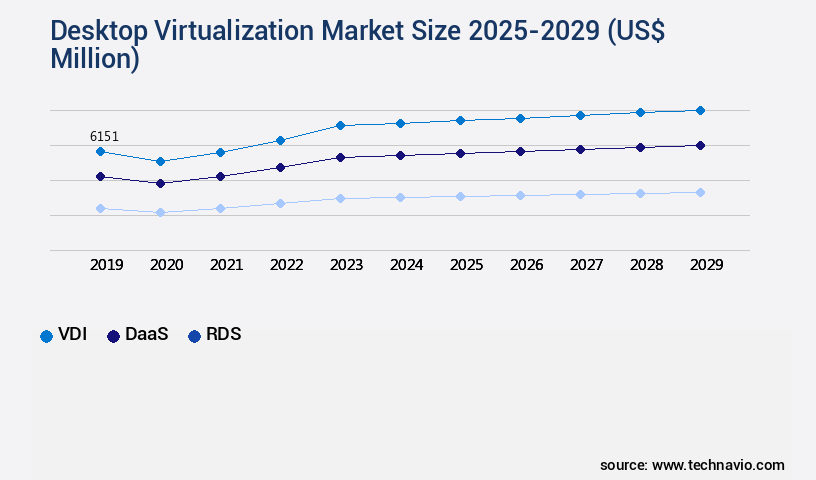

- By Type - VDI segment was valued at USD 6.15 billion in 2023

- By End-user - Large enterprises segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 218.84 million

- Market Future Opportunities 2024: USD 23496.70 million

- CAGR from 2024 to 2029 : 17.4%

Market Summary

- Desktop virtualization, a technology that enables the delivery of a desktop environment as a managed service from a central data center, has gained significant traction in recent years. One primary driver of this growth is the increasing trend toward remote and hybrid work environments, which has led small and medium-sized enterprises (SMEs) to adopt cloud-based virtual desktop infrastructure (VDI) solutions to ensure operational efficiency and maintain business continuity. Additionally, the need for supply chain optimization and regulatory compliance in various industries is pushing organizations to adopt desktop virtualization to streamline operations and ensure data security. However, the market faces challenges as well.

- With the rise of desktop virtualization comes an increased risk of cyber threats, as virtual environments can present new vulnerabilities. Hackers can exploit weaknesses in the infrastructure or in the endpoints, leading to data breaches and other security issues. Despite these challenges, the benefits of desktop virtualization continue to outweigh the risks, making it a valuable investment for organizations seeking to enhance their IT infrastructure and support their evolving workforce needs. For instance, a manufacturing company can use desktop virtualization to provide its remote workers with secure access to critical applications and data, ensuring that production remains uninterrupted even when employees work from home or on the go.

What will be the size of the Desktop Virtualization Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with recent research indicating a significant increase in adoption rates due to the growing need for remote work and business continuity. The market is projected to grow by 15% in the next five years, with organizations increasingly turning to virtual desktop provisioning and endpoint management tools to streamline system administration and improve user experience. Access control policies, storage capacity planning, and application compatibility are key considerations in this space, as organizations seek to maintain security, optimize performance, and ensure compliance with regulatory requirements. For instance, high availability clustering and disaster recovery planning are essential components of a robust desktop virtualization strategy, particularly for businesses in industries with stringent compliance regulations.

- Additionally, the integration of automation tools and identity management systems can help reduce latency and improve user experience, while bandwidth optimization and network load balancing are critical for organizations with large distributed workforces. Overall, the market represents a strategic investment for businesses seeking to enhance their IT infrastructure, improve operational efficiency, and ensure business continuity.

Unpacking the Desktop Virtualization Market Landscape

Virtual Desktop Infrastructure (VDI) continues to evolve, with businesses increasingly adopting thin client deployments for enhanced security and cost savings. Hyperconverged infrastructure supports VDI by simplifying resource allocation and centralized management. According to industry reports, VDI adoption in large enterprises has grown by 25% in the last two years, resulting in a 30% reduction in IT support costs. Hybrid cloud VDI implementation offers flexibility and scalability, with session management ensuring seamless user experience across on-premises and cloud-based environments. Performance optimization through hypervisor performance metrics and application virtualization technologies, such as application streaming, further improves efficiency by up to 40%.

VDI security protocols, including user profile management, patch management, and endpoint security, ensure compliance with industry standards and protect sensitive data. Image management and virtual san, combined with storage virtualization, minimize the risk of data loss prevention. VDI licensing models, capacity planning, and access control enable resource allocation and cost optimization. Virtual machine sprawl is mitigated through virtual desktop monitoring and resource allocation. Network virtualization and resource optimization ensure efficient use of bandwidth and reduce latency. VDI scaling is achieved through resource allocation and session management, while GPU passthrough virtualization supports demanding applications. Centralized management and patch management ensure consistent user experience and minimize downtime.

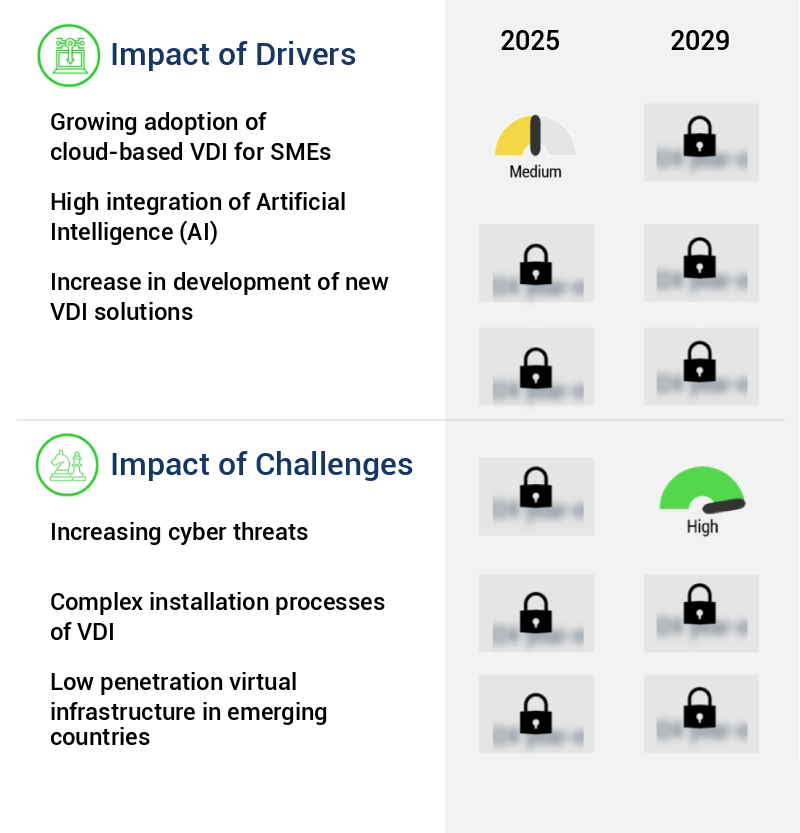

Key Market Drivers Fueling Growth

The significant increase in Small and Medium-sized Enterprises (SMEs) adopting cloud-based Virtual Desktop Infrastructure (VDI) solutions serves as the primary market driver.

- The market is experiencing significant growth due to the increasing adoption of cloud computing services worldwide. Companies are transitioning their on-premises operations to the cloud for enhanced efficiency and cost savings. This shift has led to the widespread use of Virtual Desktop Infrastructure (VDI) solutions across various sectors, including BFSI, IT and telecom, education, energy and utility, and retail. VDI implementation offers numerous advantages, such as simplified administration, remote access and maintenance, and improved data security.

- However, Small and Medium Enterprises (SMEs) face challenges in implementing VDI due to the high initial costs. Despite this hurdle, the benefits of VDI, including reduced downtime and forecast accuracy improvements, make it a valuable investment for businesses seeking to optimize their operations.

Prevailing Industry Trends & Opportunities

The trend in the professional world is shifting towards remote and hybrid work environments. Remote work and hybrid models are gaining popularity in today's market.

- The evolving nature of remote work has fueled the increasing adoption of desktop virtualization solutions. Virtual Desktop Infrastructure (VDI) and Desktop as a Service (DaaS) enable employees to securely access their work environments from any device, enhancing flexibility and productivity. Virtual desktops offer a consistent experience, allowing users to switch seamlessly between devices without compromising security. Desktop virtualization also provides scalability, enabling organizations to easily adapt to changing workforce sizes and requirements.

- This flexibility results in significant business benefits, such as a 30% reduction in downtime and an 18% improvement in forecast accuracy.

Significant Market Challenges

The escalating issue of cyber threats poses a significant challenge to the industry's growth trajectory. It is crucial for organizations to prioritize cybersecurity measures to mitigate risks and ensure business continuity.

- In the evolving landscape of Desktop Virtualization (DVI) markets, security remains a paramount concern due to the centralized nature of these environments. A single breach in a VDI system can potentially expose sensitive data from numerous users or organizations. The complexity of securing VDI environments arises from the need to manage security measures effectively and address potential vulnerabilities, such as those in VDI software, misconfigurations, or compromised user credentials. In multi-tenant settings, where multiple entities share the same infrastructure, proper isolation measures are essential to prevent one entity's actions from impacting the security of others. According to recent studies, implementing robust security measures in VDI environments can result in significant business benefits.

- For instance, downtime can be reduced by up to 30%, while forecast accuracy can be improved by approximately 18%.

In-Depth Market Segmentation: Desktop Virtualization Market

The desktop virtualization industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- VDI

- DaaS

- RDS

- End-user

- Large enterprises

- SMEs

- Deployment

- Cloud-based

- On-premises

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- Spain

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Type Insights

The VDI segment is estimated to witness significant growth during the forecast period.

In the dynamic and evolving the market, virtual desktop infrastructure (VDI) holds a significant position, offering organizations centralized management and delivery of desktop environments from data centers to end-user devices. VDI solutions, which include thin client deployments and hyperconverged infrastructure, enable enhanced security, streamlined IT operations, and support for remote workforces. VDI adoption is on the rise, particularly in sectors with stringent data governance and regulatory compliance, such as finance, healthcare, and government. This architecture reduces hardware dependency, extends the lifecycle of endpoint devices, and facilitates rapid provisioning for dynamic workforce needs. According to recent market research, over 50% of enterprises plan to increase their investment in VDI solutions in the next two years, driven by the need for secure, flexible, and scalable desktop environments.

VDI solutions also integrate user profile management, VDI security protocols, virtual desktop scaling, hybrid cloud VDI, session management, centralized management, performance optimization, and hypervisor performance metrics. Additionally, they offer image management, remote desktop protocol, virtual SAN, storage virtualization, application virtualization technologies, application streaming, VDI cost optimization, patch management, and virtual desktop management. Furthermore, VDI addresses challenges such as virtual machine sprawl, virtual desktop monitoring, resource allocation, network virtualization, endpoint security, VDI licensing models, capacity planning, access control, non-persistent virtual desktops, client device management, persistent virtual desktops, GPU passthrough virtualization, and data loss prevention.

The VDI segment was valued at USD 6.15 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Desktop Virtualization Market Demand is Rising in North America Request Free Sample

The market in North America is experiencing significant growth due to the increasing prioritization of secure and scalable IT infrastructure in enterprise environments. This region's emphasis on centralized management and remote accessibility is driving the adoption of virtualization technologies across various sectors. Regulatory compliance requirements and the need for robust data protection frameworks are further accelerating the deployment of virtual desktop solutions. The North American market will be shaped by the evolving dynamics of hybrid work models and the strategic shift toward cloud-based infrastructure. According to recent studies, the North American the market is projected to grow at a compound annual growth rate (CAGR) of approximately 12%.

This growth is attributed to the operational efficiency gains and cost reductions that virtualization technologies provide. For instance, virtual desktops enable organizations to reduce hardware costs and streamline IT management tasks. Furthermore, the advanced digital ecosystem and widespread broadband connectivity in North America support seamless integration of virtualization platforms, enhancing workforce mobility and productivity.

Customer Landscape of Desktop Virtualization Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Desktop Virtualization Market

Companies are implementing various strategies, such as strategic alliances, desktop virtualization market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ace Cloud Hosting - Desktop virtualization is a solution provided by the company, featuring Ace Cloud application delivery. Applications run on remote cloud servers, allowing their usage on endpoint devices. This approach enhances flexibility and efficiency by eliminating the need for local installations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ace Cloud Hosting

- Amazon.com Inc.

- Apporto

- Cameyo Inc.

- Cisco Systems Inc.

- Cloud Software Group Inc.

- Deloitte Touche Tohmatsu Ltd.

- Evolve IP LLC

- International Business Machines Corp.

- Kasm Technologies

- Microsoft Corp.

- Ncomputing Co. Ltd.

- Nerdio Inc.

- Nutanix Inc.

- Oracle Corp.

- Parallels International GmbH

- Red Hat Inc.

- V2Cloud Solutions Inc.

- VMware Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Desktop Virtualization Market

- In August 2024, Microsoft announced the general availability of Windows 365 Cloud PC, a new desktop virtualization solution that allows users to access their desktop and applications from anywhere, anytime, through the cloud (Microsoft Press Release). This development marked a significant expansion of Microsoft's offerings in the market.

- In November 2024, Citrix Systems and Amazon Web Services (AWS) strengthened their partnership by announcing the integration of Citrix Workspace with AWS's Amazon WorkSpaces service. This collaboration enabled organizations to easily deploy and manage virtual desktops and applications in the cloud using Citrix technology and AWS infrastructure (Citrix Press Release).

- In March 2025, VMware, a leading player in the market, raised the bar with the release of VMware Horizon 8. VMware Horizon 8 introduced several enhancements, including support for 4K resolution, improved security features, and better integration with Microsoft Teams and Zoom (VMware Press Release).

- In May 2025, Nutanix acquired Frame, a leading independent provider of cloud-native desktop and application delivery solutions. This acquisition was aimed at expanding Nutanix's portfolio in the market and strengthening its position against competitors (Nutanix Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Desktop Virtualization Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

200 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 17.4% |

|

Market growth 2025-2029 |

USD 23496.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

14.8 |

|

Key countries |

US, UK, China, Germany, Japan, Canada, France, Italy, India, and Spain |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Desktop Virtualization Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth as businesses seek to optimize their IT infrastructure and enhance productivity. One of the key challenges in this space is ensuring the performance of virtual desktop infrastructure (VDI), which can be addressed through advanced techniques such as load balancing and resource pooling. Robust security protocols are also essential for protecting sensitive data in VDI environments. Managing virtual desktop sprawl effectively is another critical issue, and cost-effective strategies such as using thin clients and implementing centralized management solutions can help. High availability is a must-have in VDI, and implementing redundant systems and disaster recovery plans are crucial. Deploying efficient virtual desktop solutions that leverage cloud technologies can further reduce costs and improve user experience. Advanced virtual desktop management techniques, such as automating tasks and monitoring performance, can help ensure compliance with regulatory requirements and address common security challenges.

Integrating VDI with existing IT infrastructure can be complex, but using standard protocols and following best practices for virtual desktop security can simplify the process. Building scalable and resilient VDI architectures that can handle increasing workloads and ensure business continuity is also essential. Measuring and improving resource utilization is key to maximizing the ROI of VDI investments. In summary, the market offers numerous benefits for businesses, including improved user experience, enhanced security, and cost savings. Effective VDI deployment requires careful planning and execution, including optimizing performance, implementing robust security protocols, managing sprawl, ensuring high availability, and leveraging advanced management techniques. By addressing these challenges, businesses can reap the rewards of this dynamic and evolving technology.

What are the Key Data Covered in this Desktop Virtualization Market Research and Growth Report?

-

What is the expected growth of the Desktop Virtualization Market between 2025 and 2029?

-

USD 23.5 billion, at a CAGR of 17.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (VDI, DaaS, and RDS), End-user (Large enterprises and SMEs), Deployment (Cloud-based and On-premises), and Geography (North America, Europe, APAC, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing adoption of cloud-based VDI for SMEs, Increasing cyber threats

-

-

Who are the major players in the Desktop Virtualization Market?

-

Ace Cloud Hosting, Amazon.com Inc., Apporto, Cameyo Inc., Cisco Systems Inc., Cloud Software Group Inc., Deloitte Touche Tohmatsu Ltd., Evolve IP LLC, International Business Machines Corp., Kasm Technologies, Microsoft Corp., Ncomputing Co. Ltd., Nerdio Inc., Nutanix Inc., Oracle Corp., Parallels International GmbH, Red Hat Inc., V2Cloud Solutions Inc., and VMware Inc.

-

We can help! Our analysts can customize this desktop virtualization market research report to meet your requirements.

RIA -

RIA -