Germany Department Stores Market Size 2026-2030

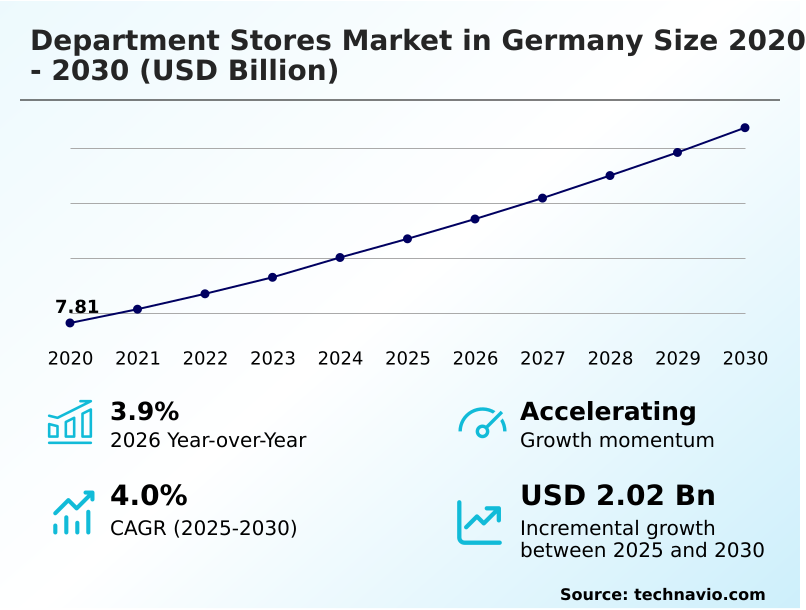

The germany department stores market size is valued to increase by USD 2.02 billion, at a CAGR of 4% from 2025 to 2030. Multi-tenant diversification and industrialization of mixed-use department store real estate will drive the germany department stores market.

Major Market Trends & Insights

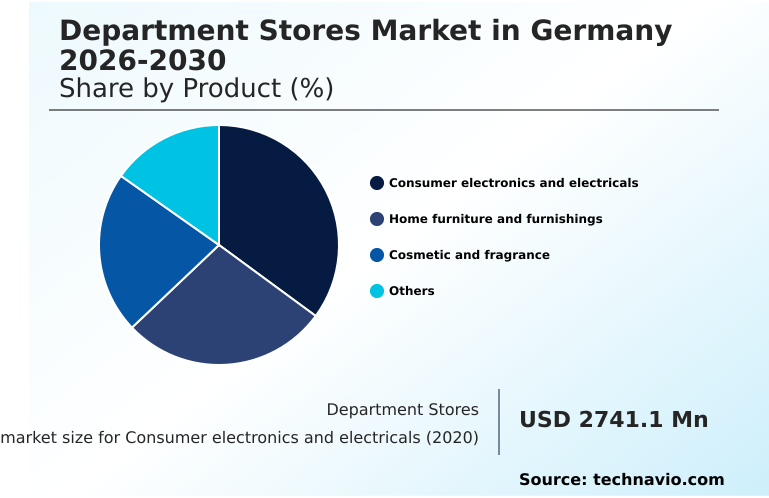

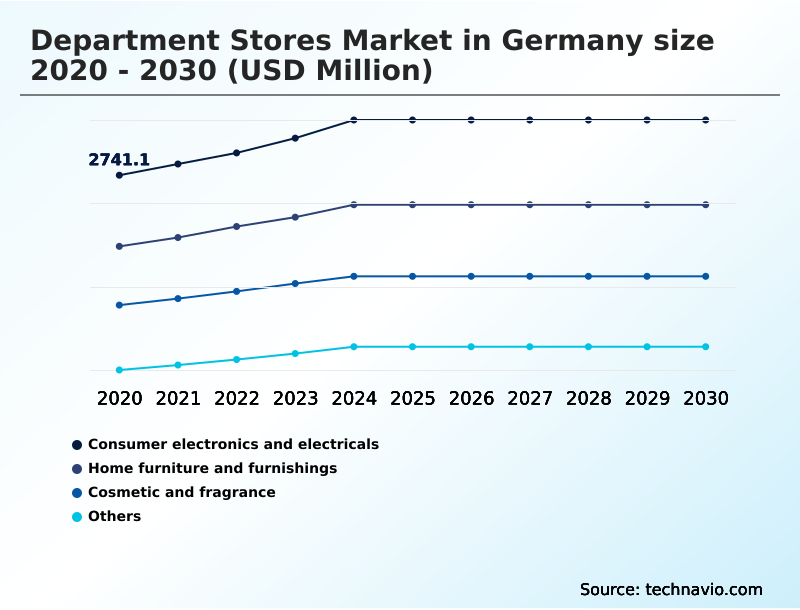

- By Product - Consumer electronics and electricals segment was valued at USD 3.18 billion in 2024

- By Type - Up-scale department stores segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.55 billion

- Market Future Opportunities: USD 2.02 billion

- CAGR from 2025 to 2030 : 4%

Market Summary

- The department stores market in Germany is undergoing a significant transformation, balancing the preservation of heritage with the urgent need for modernization. This evolution is defined by a strategic pivot towards omnichannel ecosystems and curated, high-margin consumer experiences.

- Key trends include the institutionalization of experiential luxury in flagship locations, where retailers integrate high-end gastronomy and personalized services to create destination venues. Concurrently, the proliferation of unified commerce and agentic AI shopping assistants is reshaping customer interactions, offering hyper-personalized journeys.

- For instance, a retailer can leverage first-party data analytics to power an AI assistant that suggests outfits based on past purchases and real-time inventory, bridging the gap between digital convenience and physical retail. However, the industry grapples with the financial fragility of legacy retail models and a widening technological gap in agentic commerce readiness.

- Success now depends on adopting smart value equations, leveraging AI-driven operational efficiency, and embracing circular fashion initiatives to appeal to a discerning, tech-savvy, and value-conscious consumer base, ensuring resilience in a competitive landscape.

What will be the Size of the Germany Department Stores Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Germany Department Stores Market Segmented?

The germany department stores industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Consumer electronics and electricals

- Home furniture and furnishings

- Cosmetic and fragrance

- Others

- Type

- Up-scale department stores

- Mid-range department stores

- Discount stores

- Age group

- Between 30 to 45 years

- Between 46 to 60 years

- Above 60 years

- Between 14 to 29 years

- Geography

- Europe

- Germany

- Europe

By Product Insights

The consumer electronics and electricals segment is estimated to witness significant growth during the forecast period.

The consumer electronics and electricals segment is driven by high-touch customer service for premium hardware and AI-powered stock management. Department stores are capitalizing on demand for sustainable and energy-efficient appliances by curating selections that emphasize longevity.

This pivot towards smart retail technologies enhances the value of physical showrooms for high-specification electronics. The integration of unified commerce systems and phygital retail environments allows for interactive displays where customers can test internet-of-things devices.

Effective data-driven inventory management has improved stock turn by over 15% in this category. This focus on premium brand curation and experiential retail transformation helps counter competition from digital-only platforms, reinforcing the relevance of destination-based luxury retail for high-end electronics.

The Consumer electronics and electricals segment was valued at USD 3.18 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the department stores market in Germany is increasingly complex, shaped by intersecting financial and technological pressures. Effectively managing structural insolvency in retail requires a decisive move away from outdated practices. Companies must analyze the impact of unified commerce on sales to justify investments in seamless platform integration.

- A key consideration is the challenge of adopting agentic AI, which demands robust data infrastructure for personalization. The viability of circular fashion and digital passports depends on transparent supply chains, while the restructuring of legacy retail business models is essential for long-term survival. For upscale players, offering experiential luxury for high-net-worth shoppers is paramount.

- Boardrooms are prioritizing omnichannel readiness for department stores, recognizing that a failure to adapt leads to market invisibility. Integrating gastronomy in upscale retail has proven to boost dwell time and cross-category sales. Furthermore, creating phygital environments for Gen Z is no longer a novelty but a core requirement.

- Firms that master high-touch service in luxury retail and leverage first-party data for personalization report customer retention rates that are over 30% higher than competitors. Implementing smart value strategies for mid-range stores and optimizing treasure-hunt retail models are critical for broader market appeal.

- Finally, improving click-and-collect service efficiency and defining the role of personal shopping assistants are crucial for catering to value-conscious demographics.

What are the key market drivers leading to the rise in the adoption of Germany Department Stores Industry?

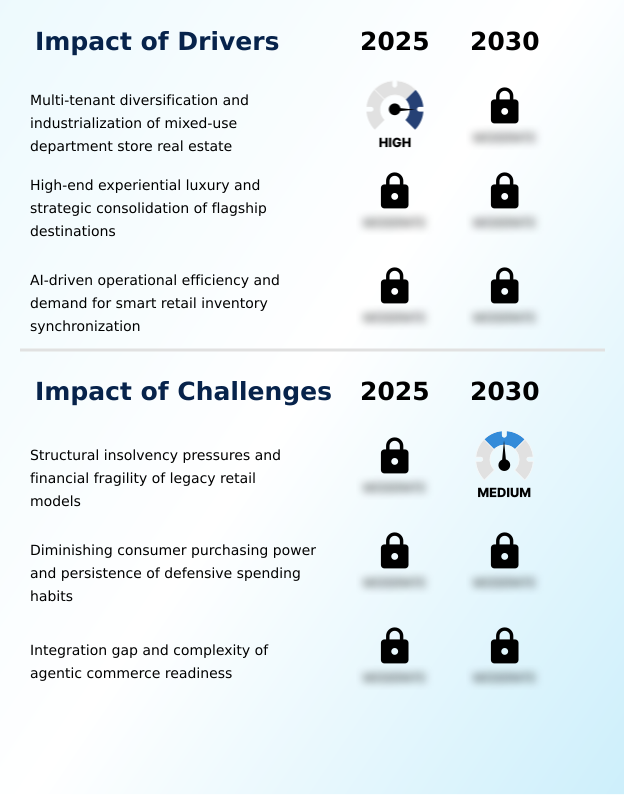

- Multi-tenant diversification and the industrialization of mixed-use department store real estate models are primary drivers for market stabilization and growth.

- Market growth is driven by the strategic evolution toward AI-driven operational efficiency and multi-tenant diversification. Retailers are aggressively repurposing traditional store footprints into mixed-use real estate models, combining retail with offices and fitness centers, which has stabilized rental income streams.

- This industrialization of retail property has emerged as a strong asset class. Concurrently, AI-powered stock management and automated pricing systems are optimizing margins and reducing waste, with recognized platforms improving stock visibility significantly.

- Another driver is the focus on high-end experiential luxury, transforming stores into lifestyle destinations. This strategy attracts high-net-worth shoppers and leverages architectural heritage, with luxury assets showing immense value and contributing to a 6% increase in prime inner-city rents.

What are the market trends shaping the Germany Department Stores Industry?

- The market is shifting toward the institutionalization of experiential luxury, characterized by a strategic consolidation of physical stores into high-performing flagship locations.

- Key trends are reshaping the market, led by the institutionalization of experiential luxury and the proliferation of unified commerce. Retailers are creating destination environments by integrating fine dining and exclusive services, with prime inner-city rents stabilizing as demand for high-visibility flagship spaces grows.

- The adoption of agentic AI shopping assistants is another critical development, with nearly 25% of consumers showing intent to purchase fashion directly through these platforms. This transition toward hyper-personalized customer journeys enables a frictionless experience. Furthermore, the strategic expansion of circular fashion initiatives, including resale and repair services, aligns with consumer demand for sustainability.

- The early adoption of digital product passports, supported by regulations, enhances transparency, a factor influencing over 70% of shoppers' purchasing decisions.

What challenges does the Germany Department Stores Industry face during its growth?

- Structural insolvency pressures and the financial fragility of legacy retail models represent a critical challenge to industry growth and stability.

- The market faces critical challenges, primarily from structural insolvency pressures and the financial fragility of legacy retail models. High operational overheads and declining footfall have forced major retailers into restructuring, struggling to pivot toward lean, digital-first operations. This financial instability has led to a visible deterioration of the in-store experience.

- A second challenge is diminishing consumer purchasing power, with over 40% of citizens feeling their financial capacity has weakened, intensifying defensive spending habits. This forces a reliance on heavy discounting, which erodes margins. Finally, a widening integration gap and the complexity of agentic commerce readiness pose a significant threat.

- Many retailers operate on fragmented IT systems, unable to provide the real-time data required for modern AI-driven commerce, a gap that could render them invisible to next-generation automated shopping algorithms.

Exclusive Technavio Analysis on Customer Landscape

The germany department stores market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the germany department stores market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Germany Department Stores Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, germany department stores market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aldi Group - Offerings center on curated luxury fashion, gourmet food halls, and premium lifestyle products, creating aspirational experiences within iconic, high-end destination stores.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aldi Group

- ausberlin

- C and A Mode GmbH and Co. KG

- E. Breuninger GmbH and Co.

- East Side Mall

- elbstolz

- Engelhorn

- Fenwick

- GALERIA Karstadt Kaufhof GmbH

- Harrods Ltd.

- Kaufhaus Ahrens GmbH and Co.

- Ludwig Beck AG

- Manufactum GmbH

- Marks and Spencer Group

- Modehaus Garhammer GmbH

- Muller Handels GmbH and Co. KG

- The KaDeWe Group GmbH

- Woolworth GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Germany department stores market

- In September 2024, The KaDeWe Group GmbH announced the completion of a major renovation phase for its Oberpollinger location in Munich, focusing on integrating high-end gastronomy and exclusive brand pop-ups to enhance its experiential luxury offerings.

- In November 2024, GALERIA Karstadt Kaufhof GmbH partnered with a leading technology firm to deploy an AI-driven inventory and pricing optimization system across its core store network, aiming to improve operational efficiency and margin control.

- In February 2025, E. Breuninger GmbH and Co. launched a circular fashion initiative, introducing dedicated resale sections for pre-owned luxury goods and a digital product passport system for its private-label brands to enhance sustainability transparency.

- In April 2025, Woolworth GmbH confirmed its strategic expansion with the opening of five new stores in regional German cities, strengthening its position in the value-conscious demographic with its discount-oriented model.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Germany Department Stores Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 185 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4% |

| Market growth 2026-2030 | USD 2018.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.9% |

| Key countries | Germany |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The department stores market in Germany is pivoting toward a model defined by multi-tenant diversification and AI-driven operational efficiency. This transition to mixed-use real estate is a strategic response to the structural insolvency threatening legacy retail models.

- In a boardroom context, the decision to invest in smart retail technologies for unified commerce is directly linked to survival, as it enables the real-time inventory synchronization needed to compete. A key trend is the rise of experiential luxury, where phygital flagship stores and high-end gastronomy create destination venues.

- The adoption of agentic AI shopping assistants and digital product passports is becoming critical for engaging consumers, while circular fashion initiatives appeal to ethical sensibilities. Retailers are implementing smart floor management and shop-in-shop concepts to enhance store viability.

- The adoption of direct-to-consumer strategies by brands is forcing department stores to focus on omnichannel digital integration and first-party data analytics for hyper-personalized marketing. This focus on technology has enabled some operators to improve stock visibility by 40%. Ultimately, post-insolvency strategy and nearshoring are being explored to build resilience, while opportunistic buying and quiet luxury cater to divergent consumer segments.

What are the Key Data Covered in this Germany Department Stores Market Research and Growth Report?

-

What is the expected growth of the Germany Department Stores Market between 2026 and 2030?

-

USD 2.02 billion, at a CAGR of 4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Consumer electronics and electricals, Home furniture and furnishings, Cosmetic and fragrance, and Others), Type (Up-scale department stores, Mid-range department stores, and Discount stores), Age Group (Between 30 to 45 years, Between 46 to 60 years, Above 60 years, and Between 14 to 29 years) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Multi-tenant diversification and industrialization of mixed-use department store real estate, Structural insolvency pressures and financial fragility of legacy retail models

-

-

Who are the major players in the Germany Department Stores Market?

-

Aldi Group, ausberlin, C and A Mode GmbH and Co. KG, E. Breuninger GmbH and Co., East Side Mall, elbstolz, Engelhorn, Fenwick, GALERIA Karstadt Kaufhof GmbH, Harrods Ltd., Kaufhaus Ahrens GmbH and Co., Ludwig Beck AG, Manufactum GmbH, Marks and Spencer Group, Modehaus Garhammer GmbH, Muller Handels GmbH and Co. KG, The KaDeWe Group GmbH and Woolworth GmbH

-

Market Research Insights

- The market is defined by a strategic push toward retail real estate repurposing, where destination-based luxury retail commands premium returns. Success hinges on a company's ability to master AI-powered stock management and real-time inventory synchronization, which has led to a 25% reduction in out-of-stock instances.

- The shift to hyper-personalized customer journeys is critical, with leading players achieving a 15% higher conversion rate through targeted promotions. Sustainable retail transparency is no longer optional, driving the adoption of resale and rental models. Addressing the omnichannel integration gap is essential for survival, as is navigating financial fragility in retail.

- Experiential retail transformation and premium brand curation are key differentiators. While mid-market retail consolidation continues, discount retail expansion captures value-conscious demographics. Effective affluent clientele marketing and a clear regional relevance strategy are imperative for growth.

We can help! Our analysts can customize this germany department stores market research report to meet your requirements.

RIA -

RIA -