Deep Sea Robot Market Size 2024-2028

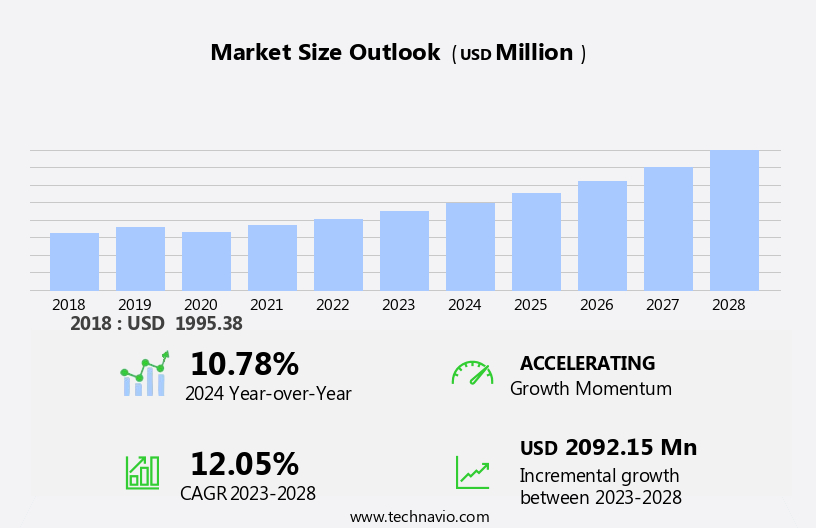

The deep sea robot market size is forecast to increase by USD 2.09 billion, at a CAGR of 12.05% between 2023 and 2028.

- The market is witnessing significant growth due to the increasing demand for underwater exploration and maritime security. The market is driven by the growing trend of using Unmanned Underwater Vehicles (UUVs) for various applications such as oceanography research, leak detection in pipelines, and submarine inspections. The high cost of developing deep sea robots, primarily due to the use of expensive materials like titanium, nickel, cobalt, and copper, acts as a challenge for market growth. However, advancements in battery technology, such as the use of zinc-air batteries, and the integration of advanced sensors and software for improved functionality, act as catalysts for market expansion. Furthermore, the use of deep sea robots in construction projects and maritime security, including torpedo detection and drone applications, is also contributing to market growth.

What will be the Size of the Deep Sea Robot Market During the Forecast Period?

- The market encompasses the design, production, and application of underwater exploration robots, including submersibles, submarines, underwater surveillance vehicles, and torpedoes. Driven by the demand for advanced ocean exploration and underwater surveillance, this market continues to expand, particularly in sectors such as oil and gas, oceanography, and anti-submarine warfare. These robots often feature cube-like structures, propellers for maneuverability, and cameras and manipulator arms for data collection.

- They can navigate ocean depths, employing sonar pulses, electromagnetic waves, and free-space optical (FSO) technology to map the seafloor and detect objects. Utilized for tasks ranging from underwater inspections of shipwrecks to the monitoring of marine life, deep sea robots are increasingly integral to our understanding of the ocean's mysteries and resources.

How is this Deep Sea Robot Industry segmented and which is the largest segment?

The deep sea robot industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- ROV

- AUV

- Submersible vehicles

- Application

- Commercial exploration

- Defense and security

- Scientific research

- Geography

- North America

- Canada

- US

- Europe

- Germany

- Norway

- APAC

- China

- Middle East and Africa

- South America

- North America

By Type Insights

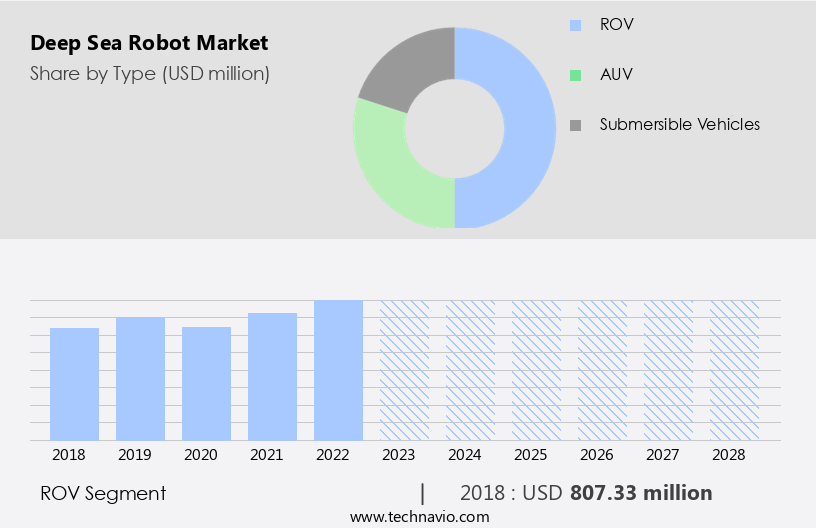

- The ROV segment is estimated to witness significant growth during the forecast period.

Deep-sea robots, specifically Remotely Operated Vehicles (ROVs,) have gained significant importance in various industries, including oil and gas, marine biology, and oceanography. Equipped with cameras, sensors, and manipulator arms, ROVs can navigate and execute tasks In the deep ocean. In the oil and gas sector, ROVs are instrumental for underwater exploration, pipeline maintenance, and repair. They enable precise and accurate inspections of underwater structures, while also featuring oil leak detection systems to minimize environmental damage. In marine biology, ROVs facilitate research and exploration of the underwater world, contributing to the discovery of new marine species and the study of existing ones.

Advanced ROVs incorporate AI software, autonomous navigation, and environmental perception, enhancing their functionality. The commercial exploration segment and defense & security sectors also utilize ROVs for tasks such as shipwreck exploration, sonar technology, and anti-submarine warfare. Companies are at the forefront of ROV development. ROVs are essential tools for underwater surveillance and exploration, providing valuable insights and data in a safe and efficient manner.

Get a glance at the market report of share of various segments Request Free Sample

The ROV segment was valued at USD 807.33 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

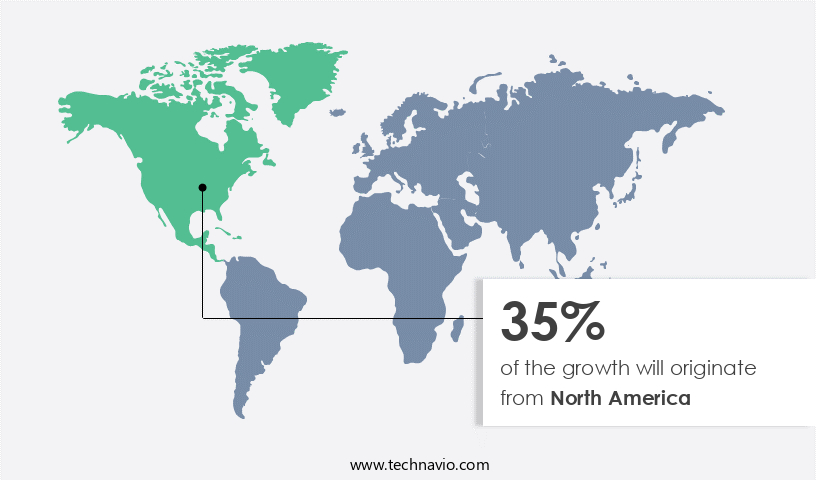

- North America is estimated to contribute 35% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

Deep sea robots have gained significant traction in various industries, including oil and gas, defense, and underwater exploration. The North American market for deep sea robots is experiencing substantial growth due to the presence of key players and favorable government initiatives. A primary driver of this growth is the increasing demand for deep sea robots In the oil and gas sector. Major oil and gas companies in North America have invested heavily In the development of these robots for exploration and production activities. Deep sea robots are employed for underwater surveillance, self-maintenance, and autonomous navigation.

They feature advanced technologies such as AI software, cameras, manipulator arms, sonar technology, and propellers. Applications include underwater exploration, shipwreck detection, and commercial exploration. Additionally, deep sea robots are utilized in anti-submarine warfare and defense and security sectors. The ROVs and commercial exploration segments are expected to dominate the market. Deep sea robots offer numerous benefits, including reduced crew requirements, increased efficiency, and enhanced safety.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Deep Sea Robot Industry?

Growing demand for oceanography research is the key driver of the market.

- The market is experiencing significant growth due to the increasing demand for underwater surveillance and exploration. This includes the oil & gas sector's reliance on submersibles for underwater inspections and maintenance, as well as commercial exploration and defence & security applications. Self-maintenance, environmental perception, autonomous navigation, and AI software are key features driving the development of advanced deep-sea robots. Deep-sea robots are used for various purposes, such as underwater exploration, oceanography, anti-submarine warfare, and commercial exploration. These robots come in various forms, including cube-like structures with propellers, cameras, manipulator arms, and sonar technology. Some are modeled after submarines or torpedoes, while others resemble eels or have unique designs.

- Deep-sea robots are essential for exploring the ocean depths, where human presence is limited or impossible. They can withstand extreme pressure and temperature conditions, as well as navigate through challenging environments. These robots can also collect valuable data on shipwrecks, seafloor geology, and marine life, which is crucial for scientific research and resource management. Sonar technology, including sonar pulses and electromagnetic waves, is a critical component of deep-sea robots. They can also use free-space optical (FSO) and sound waves to communicate with surface vessels or other underwater robots. Seawater and surface ambient noise can affect the performance of deep-sea robots, making it essential to design them with advanced technologies to mitigate these challenges.

What are the market trends shaping the Deep Sea Robot Industry?

Increasing deployment of UUVs is the upcoming market trend.

- Underwater drones, also known as Unmanned Underwater Vehicles (UUVs), are gaining significant attention due to the increasing demand for underwater surveillance in various sectors. UUVs are utilized for diverse applications, including naval mine detection, seabed mapping, seabed mining, underwater mine searches, and recovery missions. Equipped with sonar systems and oceanographic sensors, these drones enable effective monitoring of underwater environments. The need for underwater surveillance is escalating due to security concerns, particularly in relation to naval bases, offshore oil-and-gas production and transport facilities, and nuclear power plants. Furthermore, environmental concerns are driving the demand for monitoring water quality and detecting pollutants in sensitive areas and larger basins.

- UUVs are instrumental in underwater exploration, with companies such as Nauticus Robotics, Vaarst, Equinor, Open Ocean Robotics, and Schilling Robotics leading the way in this field. These drones employ AI software, autonomous navigation, and environmental perception to navigate the ocean depths. They come in various forms, including cube-like structures with propellers and cameras, as well as manipulator arms. UUVs are also used in commercial exploration, such as oil and gas industries, and in defense and security applications, including anti-submarine warfare. Sonar technology, which is a critical component of UUVs, emits sonar pulses and detects electromagnetic waves or sound waves In the seawater.

- However, surface ambient noise can interfere with sonar detection, necessitating advanced technologies like Free-space optical (FSO) for clearer communication between UUVs and their operators. UUVs have replaced crewed submarines and torpedoes in several applications, providing a safer and more cost-effective solution. Aquanauts, human divers, are increasingly being replaced by UUVs due to their ability to operate in harsh conditions and for extended periods without the need for crew members. Unmanned drone systems, such as UUVs, are revolutionizing underwater exploration and surveillance, offering significant benefits to various industries and governments.

What challenges does the Deep Sea Robot Industry face during its growth?

The high cost of development of deep sea robots is a key challenge affecting the industry growth.

- Deep sea robots, also known as underwater exploration robots, are essential tools for underwater surveillance and commercial exploration in various industries, including oil & gas and defence & security. The demand for these robots is driven by the need to explore the vast ocean depths, where human presence is limited due to extreme conditions. These robots come in various forms, such as submersibles, self-maintenance vehicles, and autonomous underwater vehicles (AUVs). They are equipped with AI software, cameras, manipulator arms, sonar technology, and other advanced features for environmental perception, autonomous navigation, and commercial exploration. The development of deep sea robots is a complex and costly process due to the requirement for specialized materials and components.

- These robots must be constructed from materials that can withstand extreme pressures, temperatures, and corrosive seawater. For instance, ROVs (Remotely Operated Vehicles) used in oceanography and anti-submarine warfare are often made of titanium and other strong metals. Companies like Nauticus Robotics, Vaarst, Equinor, Open Ocean Robotics, and Schilling Robotics are leading the way in this field, using the latest technologies to create advanced deep sea robots. The ROVs segment and commercial exploration segment are expected to dominate the market due to their wide applications and increasing demand. Deep sea robots are used for various purposes, including underwater surveillance, exploration of shipwrecks, and even the inspection of submarines and torpedoes.

Exclusive Customer Landscape

The deep sea robot market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the deep sea robot market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, deep sea robot market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BAE Systems Plc

- Blue Robotics Inc.

- CRRC Corp. Ltd.

- Deep Ocean Engineering Inc.

- DOER Marine

- Exail Technologies

- Forum Energy Technologies Inc.

- Halma Plc

- International Submarine Engineering Ltd.

- Kongsberg Gruppen ASA

- L3Harris Technologies Inc.

- Lockheed Martin Corp.

- Mariscope

- Nauticus Robotics Inc.

- Oceaneering International Inc.

- ROVOP Ltd.

- Saab AB

- Shark Marine Technologies Inc.

- TechnipFMC plc

- VideoRay LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is experiencing significant growth due to the increasing demand for underwater surveillance and exploration. Robots designed for underwater applications are becoming increasingly important in various sectors, including oceanography, oil and gas, commercial exploration, and defense and security. Underwater exploration robots, also known as underwater robots or autonomous underwater vehicles (AUVs), are gaining popularity due to their ability to operate in extreme ocean depths and collect valuable data. These robots are typically designed with advanced features such as self-maintenance, environmental perception, and autonomous navigation. Self-maintenance is a crucial aspect of deep-sea robots, as the harsh underwater environment can cause significant wear and tear on the machinery.

Further, robots equipped with self-maintenance capabilities can extend their operational lifespan and reduce the need for costly and time-consuming maintenance and repair. Environmental perception is another essential feature of deep-sea robots, as they must be able to navigate and interact with their environment effectively. Advanced sensors and AI software enable robots to perceive their surroundings and make informed decisions based on the data they collect. Autonomous navigation is a critical component of deep-sea robots, as it allows them to operate independently and cover large areas of the ocean floor. This capability is particularly important in commercial exploration, where robots are used to search for resources such as minerals and oil and gas deposits.

In addition, deep-sea robots are also being used in defense and security applications, including anti-submarine warfare and underwater surveillance. These robots are equipped with advanced sonar technology, which allows them to detect and track underwater objects, including submarines and torpedoes. The oil and gas sector is another significant market for deep-sea robots, particularly In the ROVs (remotely operated vehicles) segment. These robots are used for underwater inspections, maintenance, and repair of offshore installations and pipelines. The commercial exploration segment is also experiencing significant growth, with deep-sea robots being used to explore the ocean floor for resources and to study marine life.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 12.05% |

|

Market Growth 2024-2028 |

USD 2.09 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

10.78 |

|

Key countries |

US, Canada, China, Germany, and Norway |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Deep Sea Robot Market Research and Growth Report?

- CAGR of the Deep Sea Robot industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the deep sea robot market growth of industry companies

We can help! Our analysts can customize this deep sea robot market research report to meet your requirements.

RIA -

RIA -