Cytology Market Size 2026-2030

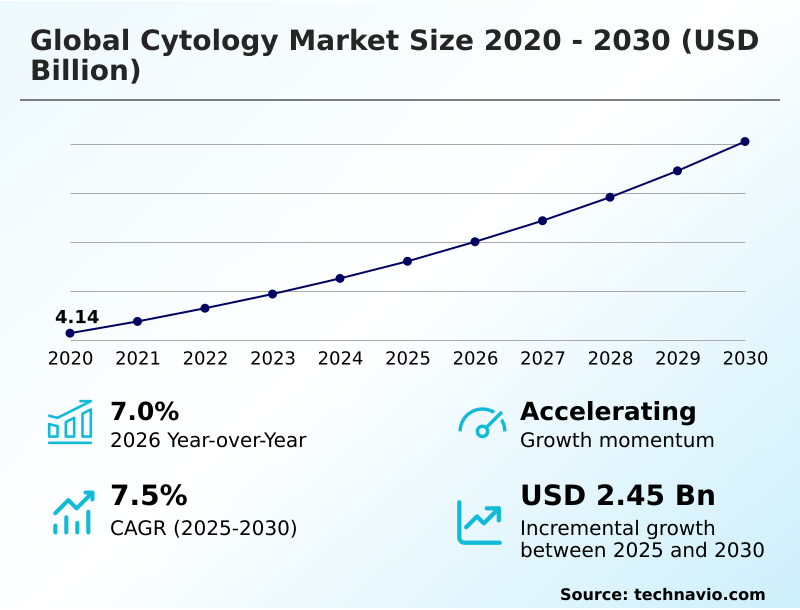

The cytology market size is valued to increase by USD 2.45 billion, at a CAGR of 7.5% from 2025 to 2030. Increasing prevalence of cancer and infectious diseases will drive the cytology market.

Major Market Trends & Insights

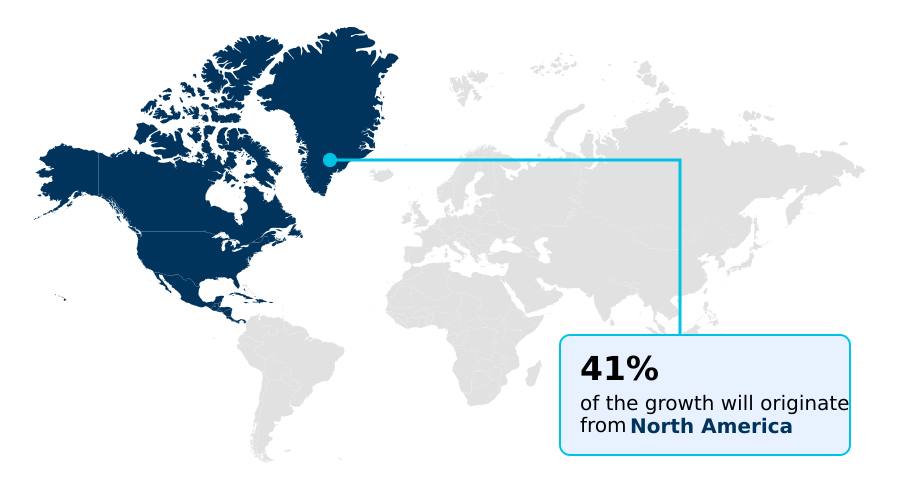

- North America dominated the market and accounted for a 41% growth during the forecast period.

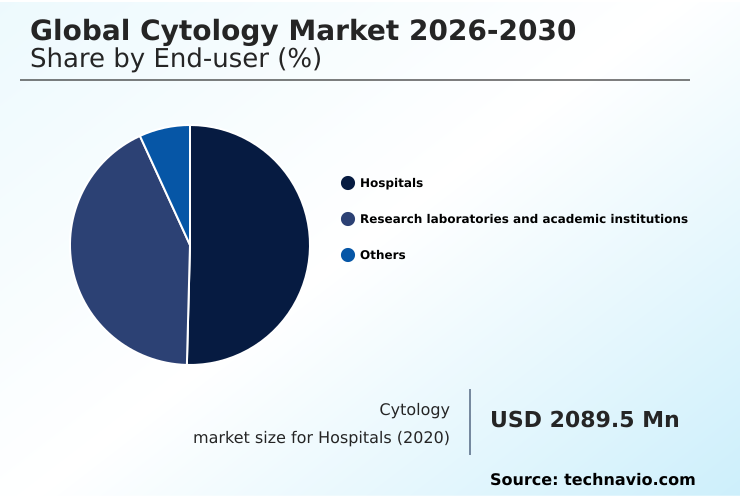

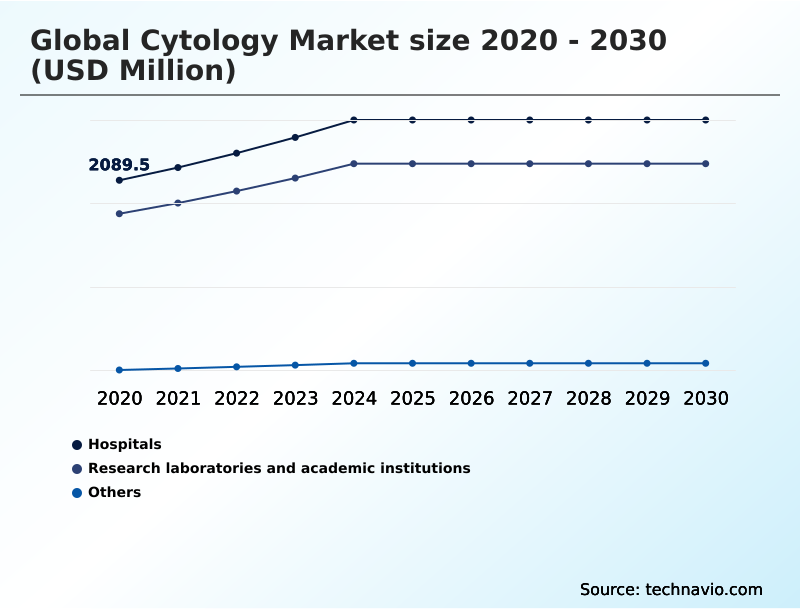

- By End-user - Hospitals segment was valued at USD 2.66 billion in 2024

- By Technique - Liquid-based cytology segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.92 billion

- Market Future Opportunities: USD 2.45 billion

- CAGR from 2025 to 2030 : 7.5%

Market Summary

- The cytology market is defined by a continuous drive for greater diagnostic precision and efficiency. At its core, the market serves the critical need for early disease detection, primarily for neoplastic conditions, through the microscopic analysis of cellular morphology.

- This is achieved via techniques like conventional cytology and the more advanced liquid-based cytology, which has improved sample quality and enabled the molecular diagnostics convergence. A key business scenario involves a high-volume diagnostic laboratory implementing an automated sample processing workflow.

- By leveraging pre-analytical automation and automated staining systems, the lab can standardize cell monolayer preparation, significantly reducing unsatisfactory specimen rates and freeing skilled cytotechnologists to focus on complex cases. This not only enhances diagnostic accuracy improvement but also optimizes test volume management, directly addressing the pathologist workforce deficit without compromising quality assurance protocols.

- The field faces challenges from alternative diagnostic technologies, but its value is reinforced by its integration into a broader precision medicine workflow. The integration with laboratory information systems ensures seamless patient record management, while digital pathology integration allows for remote diagnosis telecytology, overcoming geographical barriers to subspecialty expertise access.

- This evolution showcases a market adapting to demands for faster, more reliable, and integrated diagnostic solutions.

What will be the Size of the Cytology Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Cytology Market Segmented?

The cytology industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospitals

- Research laboratories and academic institutions

- Others

- Technique

- Liquid-based cytology

- Conventional cytology

- Application

- Cervical cancer screening

- Non-cervical cancer screening

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

Hospitals represent the most significant end-user segment, driven by high inpatient and outpatient volumes across specialties like oncology and gynecology.

These institutions are primary purchasers of the full spectrum of cytology products, from specimen collection vials to advanced digital imaging systems.

Procurement decisions are increasingly complex, balancing total cost of ownership with the adoption of technologies like liquid-based cytology and automated slide preparation. A key objective is workflow automation to improve laboratory efficiency and address workforce challenges.

Integrating these platforms with existing laboratory information systems is critical for seamless data management, which can reduce turnaround times for critical results by over 25%, ensuring a stable, foundational demand.

The Hospitals segment was valued at USD 2.66 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cytology Market Demand is Rising in North America Request Free Sample

The geographic landscape is marked by varying technology adoption, with North America and Europe leading in advanced diagnostics. The use of fine-needle aspiration for non-gynecological cytology is growing globally, driving demand for specimen collection vials and diagnostic slide scanners.

In developed regions, the implementation of sophisticated image management software and laboratory information systems is standard, improving patient record management and creating a lean laboratory environment.

This digital infrastructure enables remote diagnosis telecytology, which connects rural clinics with urban specialists and reduces diagnostic turnaround times by over 30%.

This access to subspecialty expertise helps mitigate issues like high unsatisfactory specimen rates and ensures a consistent total cost of ownership by optimizing resource use across networks.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- An in-depth analysis of the global cytology market 2026-2030 reveals complex dynamics. A key debate is the global cytology market 2026-2030 liquid-based versus conventional techniques, with adoption varying by region. The global cytology market 2026-2030 AI integration impact is transformative, closely tied to global cytology market 2026-2030 digital pathology adoption rates.

- The technology's foundational global cytology market 2026-2030 role in cervical screening is evolving, while the global cytology market 2026-2030 non-gynecological application growth is accelerating, particularly for global cytology market 2026-2030 FNA biopsy diagnostic utility. Firms are leveraging global cytology market 2026-2030 automation for lab efficiency, driven by global cytology market 2026-2030 molecular testing integration trends.

- However, the market faces global cytology market 2026-2030 challenges from liquid biopsy and is constrained by the global cytology market 2026-2030 skilled workforce shortage impact, alongside global cytology market 2026-2030 reimbursement hurdles for new tech.

- The core global cytology market 2026-2030 drivers of market expansion remain strong, influenced by global cytology market 2026-2030 end-user segment dynamics and significant global cytology market 2026-2030 regional technology adoption differences. The success of global cytology market 2026-2030 impact of population screening programs is a major factor, while compliance with global cytology market 2026-2030 in vitro diagnostic regulation is non-negotiable.

- Finally, solutions like global cytology market 2026-2030 telecytology for remote diagnostics are key to global cytology market 2026-2030 improving diagnostic turnaround times, and the use of global cytology market 2026-2030 immunocytochemistry in cancer diagnosis continues to expand.

- For instance, labs adopting automation report efficiency gains in sample processing that are at least 40% greater than those using manual methods, directly impacting operational planning.

What are the key market drivers leading to the rise in the adoption of Cytology Industry?

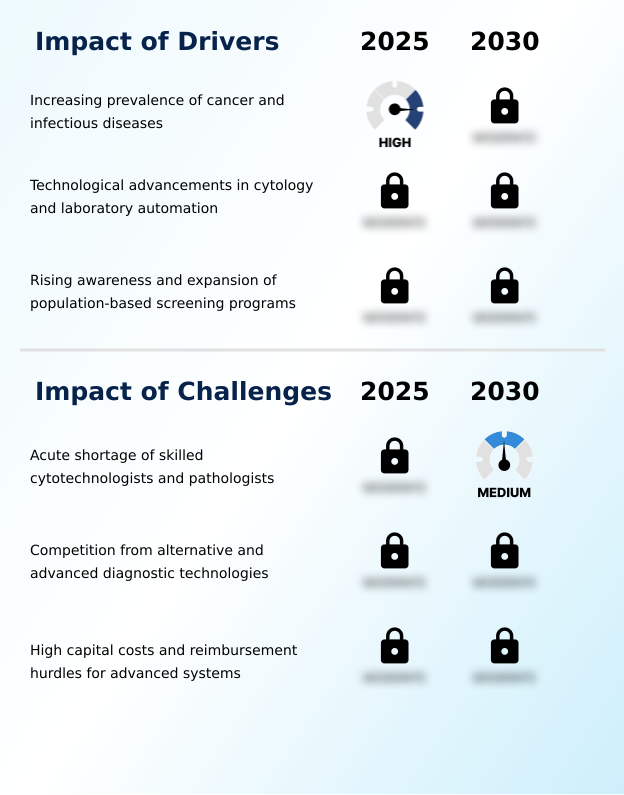

- The increasing global prevalence of cancer and infectious diseases serves as a primary driver for market growth.

- Key market drivers include large-scale population-based screening programs and a focus on early disease detection. Organized programs for cervical cancer screening, which rely on the long-established papanicolaou test methodology, drive significant test volume management and demand for exfoliative cell analysis.

- While conventional cytology is still used in some regions, its higher false negative result rate is a concern. Effective screening for neoplastic conditions and pathogen identification requires adherence to strict quality assurance protocols and clinical validation data.

- These initiatives improve public health outcomes, as organized screening can increase participation by 40% compared to opportunistic testing. Implementing clear standard operating procedures is crucial for the success of any diagnostic algorithm integration, ensuring consistent and reliable results.

What are the market trends shaping the Cytology Industry?

- The progressive integration of digital pathology and artificial intelligence represents a transformative trend. This evolution is reshaping diagnostics toward a more dynamic and data-driven model.

- Key trends are centered on digital pathology integration and the molecular diagnostics convergence. The shift from traditional methods to liquid-based cytology has enabled more effective ancillary molecular testing for precise biomarker status detection. This data-driven diagnostic model leverages whole-slide imaging and artificial intelligence screening to achieve significant diagnostic accuracy improvement, with some platforms reducing inter-observer variability by up to 15%.

- These workflow optimization solutions are central to the modern precision medicine workflow, creating an integrated diagnostic approach. This evolution allows for greater access to subspecialty expertise regardless of location, as AI-powered analysis has demonstrated an 18% improvement in detecting abnormalities in complex cases.

What challenges does the Cytology Industry face during its growth?

- An acute shortage of skilled cytotechnologists and pathologists presents a fundamental challenge, constraining market capacity and growth.

- Significant challenges arise from competition and regulation. The rise of liquid biopsy technologies, analyzing circulating tumor dna, presents a long-term alternative, while primary screening for high-risk human papillomavirus is already shifting cytology to a diagnostic triage role. Gaining market access is complicated by the rigorous in vitro diagnostic regulation and clinical laboratory improvement amendments.

- This regulatory approval process can delay market entry by up to 24 months for novel systems like automated staining systems. Furthermore, high capital equipment investment costs, which can be three times higher for automated platforms, combined with hurdles in reimbursement code establishment, create substantial financial barriers for laboratories, impacting the adoption of high-throughput screening technologies.

Exclusive Technavio Analysis on Customer Landscape

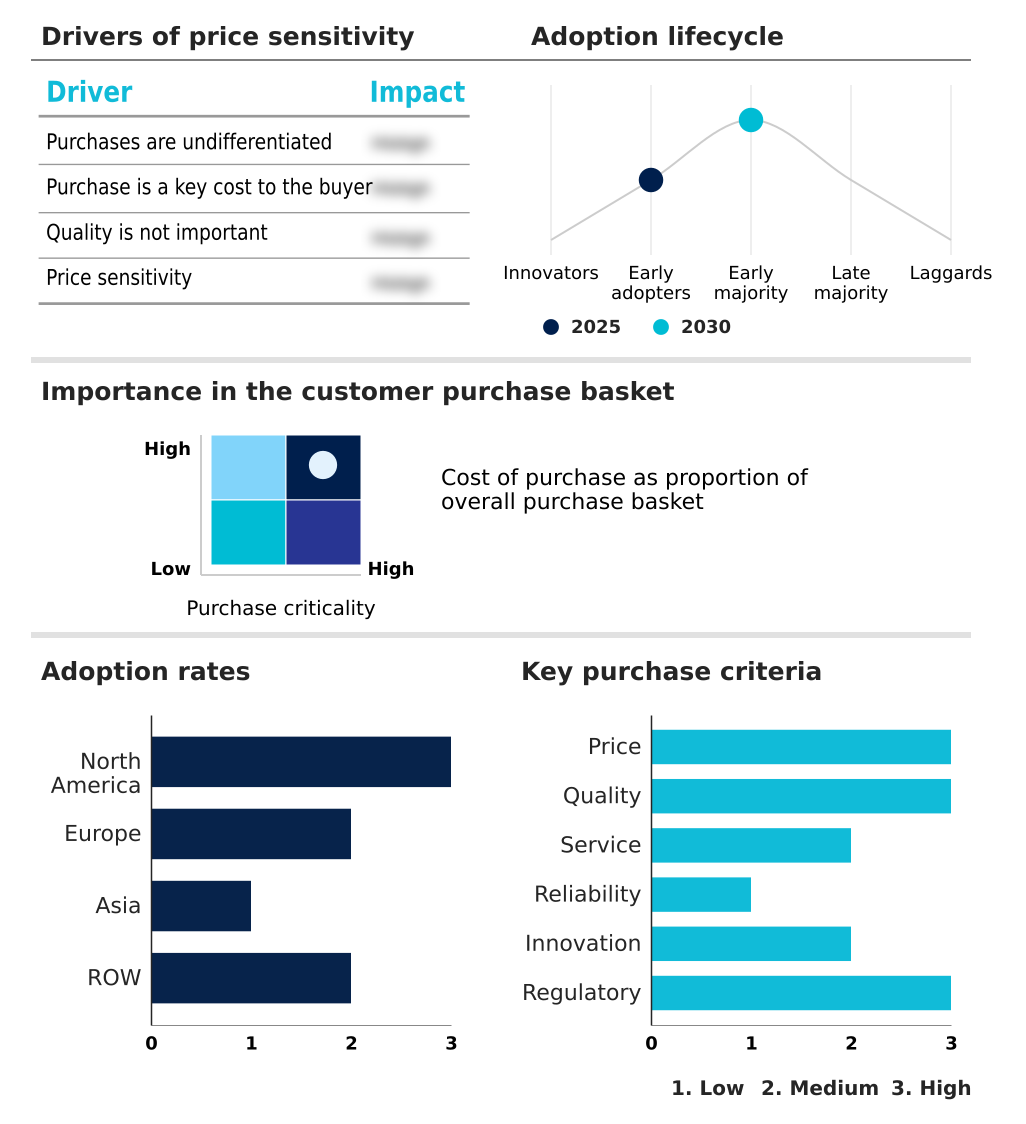

The cytology market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cytology market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cytology Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cytology market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Key offerings include instruments and consumables designed to enhance diagnostic precision and laboratory efficiency, catering to advanced histology and cytology applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Agilent Technologies Inc.

- Becton Dickinson and Co.

- Biocare Medical LLC

- CellaVision

- COPAN Diagnostics Inc.

- Danaher Corp.

- F. Hoffmann La Roche Ltd.

- Hologic Inc.

- IDEXX Laboratories Inc.

- Inpeco SA

- Koninklijke Philips NV

- QIAGEN N.V.

- Sakura Finetek

- Sysmex Corporation

- Thermo Fisher Scientific Inc.

- Trivitron Healthcare

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cytology market

- In January 2025, Roche received U.S. Food and Drug Administration clearance for its VENTANA Kappa and Lambda Dual ISH mRNA Probe Cocktail, enhancing diagnostic precision for B-cell lymphoma subtypes.

- In February 2025, Thermo Fisher Scientific announced a definitive agreement to acquire the Purification and Filtration business from Solventum, strengthening its Life Sciences Solutions segment and capabilities.

- In February 2025, Hologic Inc. announced the full commercial launch of its Genius Digital Diagnostics System, an AI-powered platform for Pap test analysis, in key European markets to improve workflow efficiency.

- In January 2025, Deciphex, a developer of AI-enabled pathology platforms, secured $31 million in a Series C funding round to expand its diagnostic services and address the global pathologist shortage.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cytology Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 291 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.5% |

| Market growth 2026-2030 | USD 2450.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Thailand, Brazil, South Africa, UAE, Turkey, Saudi Arabia, Argentina, Colombia and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cytology market is undergoing a significant transformation, driven by digital pathology integration and the convergence with molecular diagnostics. The shift from conventional cytology to liquid-based cytology is nearly complete in developed markets, facilitating ancillary molecular testing and the analysis of biomarker status. For non-gynecological cytology, fine-needle aspiration remains a cornerstone, with its diagnostic utility enhanced by immunocytochemistry applications.

- A major focus is on automation, including automated slide preparation and artificial intelligence screening, to manage high test volumes. The use of whole-slide imaging and diagnostic slide scanners is fundamental to this shift, enabling remote diagnosis telecytology.

- This technological evolution, governed by standards like the clinical laboratory improvement amendments, is creating systems where pre-analytical automation can reduce sample processing workflow time by up to 30%, directly impacting lab efficiency and patient care pathways.

What are the Key Data Covered in this Cytology Market Research and Growth Report?

-

What is the expected growth of the Cytology Market between 2026 and 2030?

-

USD 2.45 billion, at a CAGR of 7.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals, Research laboratories and academic institutions, and Others), Technique (Liquid-based cytology, and Conventional cytology), Application (Cervical cancer screening, and Non-cervical cancer screening) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of cancer and infectious diseases, Acute shortage of skilled cytotechnologists and pathologists

-

-

Who are the major players in the Cytology Market?

-

Abbott Laboratories, Agilent Technologies Inc., Becton Dickinson and Co., Biocare Medical LLC, CellaVision, COPAN Diagnostics Inc., Danaher Corp., F. Hoffmann La Roche Ltd., Hologic Inc., IDEXX Laboratories Inc., Inpeco SA, Koninklijke Philips NV, QIAGEN N.V., Sakura Finetek, Sysmex Corporation, Thermo Fisher Scientific Inc. and Trivitron Healthcare

-

Market Research Insights

- Market dynamics are shaped by a push for greater efficiency and accuracy. The adoption of a data-driven diagnostic model improves diagnostic accuracy improvement, with some systems reducing errors by over 15%. This integrated diagnostic approach, central to the precision medicine workflow, is enabling workflow optimization solutions that increase laboratory output by 20%.

- While initial capital equipment investment is a factor, the focus remains on enhancing diagnostic consistency and reducing the inter-observer variability that can impact outcomes, creating a lean laboratory environment focused on value.

We can help! Our analysts can customize this cytology market research report to meet your requirements.

RIA -

RIA -