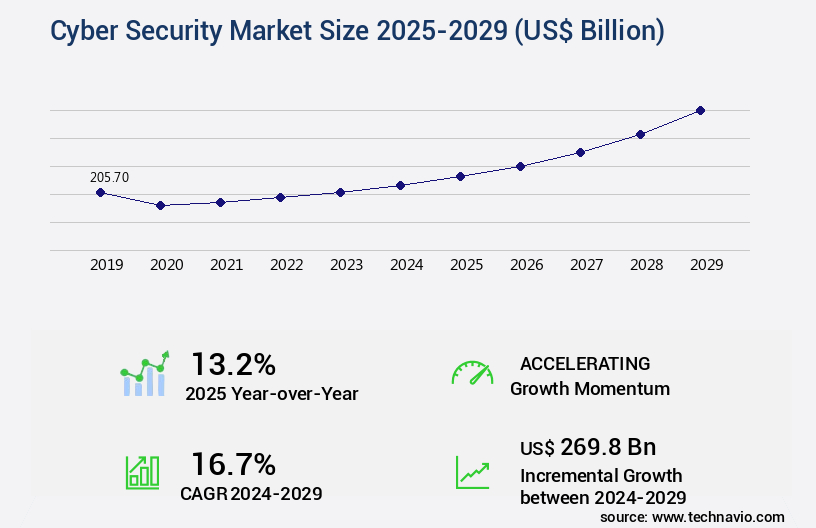

Cyber Security Market Size 2025-2029

The cyber security market size is valued to increase USD 269.8 billion, at a CAGR of 16.7% from 2024 to 2029. Increase in use of mobile devices will drive the cyber security market.

Major Market Trends & Insights

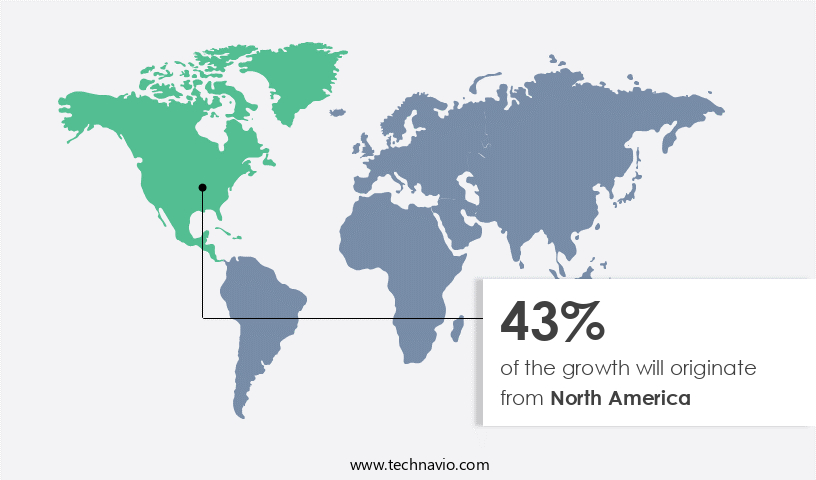

- North America dominated the market and accounted for a 43% growth during the forecast period.

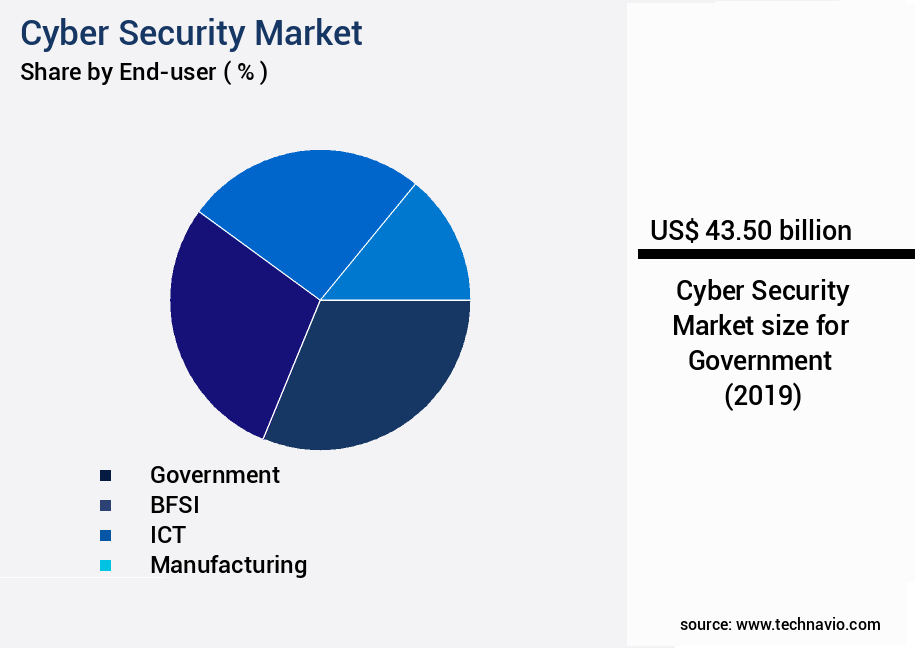

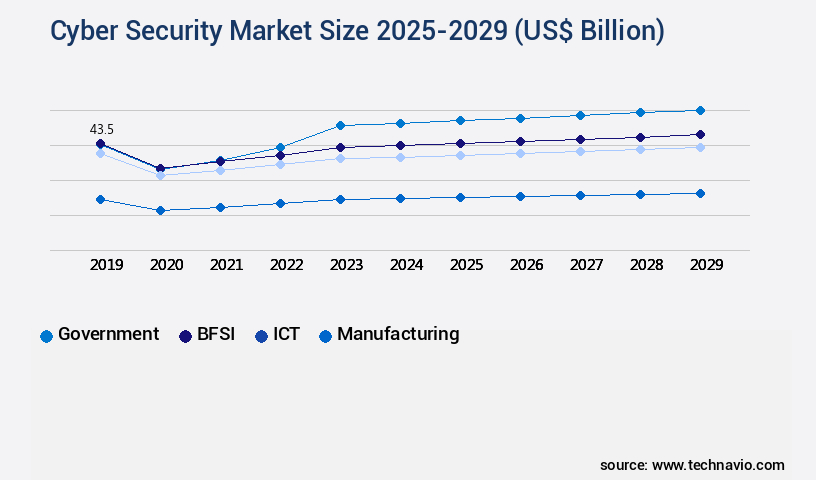

- By End-user - Government segment was valued at USD 43.50 billion in 2023

- By Deployment - On-premises segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 143.61 billion

- Market Future Opportunities: USD 269.80 billion

- CAGR from 2024 to 2029 : 16.7%

Market Summary

- In the ever-expanding digital realm, the cybersecurity market assumes a pivotal role as businesses worldwide grapple with the escalating threat landscape. According to recent estimates, the global cybersecurity market is projected to reach a value of USD248.26 billion by 2023, underscoring its significant growth trajectory. This surge in demand is fueled by several key drivers, including the increasing use of mobile devices and the adoption of IoT technology. As businesses embrace digital transformation, they become increasingly reliant on complex networks and interconnected systems, creating a vast attack surface for cybercriminals. This, in turn, necessitates robust cybersecurity solutions capable of safeguarding sensitive data and mitigating potential threats.

- However, the high cost of deployment remains a significant challenge, necessitating a balance between security and cost-effectiveness. Moreover, the cybersecurity landscape is characterized by rapid evolution, with emerging threats and technologies requiring continuous adaptation and innovation. As such, cybersecurity providers must stay abreast of the latest trends and developments to deliver effective solutions. This ongoing demand for advanced security capabilities is expected to drive market growth in the coming years.

What will be the Size of the Cyber Security Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Cyber Security Market Segmented ?

The cyber security industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Government

- BFSI

- ICT

- Manufacturing

- Others

- Deployment

- On-premises

- Cloud-based

- Product

- Solution

- Services

- Sector

- Large enterprises

- SMEs

- Type

- Cloud

- End-point and IoT

- Network

- Application

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Russia

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

The government segment is estimated to witness significant growth during the forecast period.

Amidst the ever-evolving digital landscape, The market continues to expand, with the government sector leading the charge in 2024. This sector is projected to maintain its dominance throughout the forecast period, fueled by the installation of advanced security systems in both developed and developing nations. Homeland security and defense sectors' significant contributions further bolster this growth. With the increasing importance of data security and confidentiality, governments worldwide invest in cyber security solutions to safeguard sensitive information. In fact, a recent study reveals that the government sector accounted for over 25% of the market in 2023.

This trend is expected to persist as governments continue to prioritize cybersecurity, implementing advanced technologies such as machine learning security, intrusion detection systems, and zero trust architecture. Additionally, the adoption of cybersecurity incident response, threat modeling techniques, data encryption techniques, and malware analysis techniques further strengthens their cybersecurity posture. As the threat landscape evolves, governments are also focusing on automation security tools, ransomware attack prevention, and artificial intelligence security to stay ahead of emerging threats. Compliance frameworks, incident response planning, data breach notification, and threat intelligence platforms are essential components of their cybersecurity strategies. Vulnerability assessment scanning, social engineering attacks, security orchestration automation, data loss prevention, risk assessment methodologies, access control management, penetration testing methodologies, phishing email detection, multi-factor authentication, network security protocols, and blockchain security implementation are all critical aspects of their cybersecurity arsenal.

The Government segment was valued at USD 43.50 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cyber Security Market Demand is Rising in North America Request Free Sample

The North American region dominates The market, accounting for the largest market share. This trend is anticipated to persist throughout the forecast period. The US, in particular, is a significant contributor to the market's growth in North America. Several factors fuel this expansion. These include the increasing adoption of cyber security solutions by various industries, the transition of traditional IT services to cloud-based IT systems, the expansion of end-user industries, escalating government initiatives to implement cyber security measures, and the proliferation of IT companies and startups in the region.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing robust growth as businesses worldwide prioritize securing their digital assets against an ever-evolving threat landscape. Implementing a zero trust security framework is becoming a best practice, ensuring that access to sensitive data is granted based on verified identity and location. Advanced persistent threat detection solutions help organizations identify and respond to stealthy attacks that can evade traditional security measures. Managing security information events effectively is crucial for swift incident response. Developing an effective incident response plan is essential, as is detecting and responding to phishing attacks in real-time. Data loss prevention techniques are vital for safeguarding sensitive information, both at rest and in transit. Best practices for secure software development, such as automating vulnerability management and leveraging threat intelligence platforms, are essential for proactively addressing potential weaknesses. Securing cloud infrastructure environments and performing regular security audits are also essential to mitigate risks associated with cyberattacks. Configuring robust access control systems, deploying multi-factor authentication, applying effective data encryption methods, and using machine learning for threat detection are all critical components of a comprehensive cybersecurity strategy. Enhancing security awareness among employees and ensuring compliance with regulatory standards are also essential for maintaining a strong security posture. Building resilience against ransomware attacks and strengthening network security protocols are ongoing efforts that require continuous attention and investment. By prioritizing these initiatives, businesses can effectively navigate the complexities of the market and protect their most valuable assets.

What are the key market drivers leading to the rise in the adoption of Cyber Security Industry?

- The prevalent trend of heightened mobile device utilization serves as the primary catalyst for market growth.

- In the contemporary business landscape, the escalating utilization of mobile devices for personal and professional purposes has significantly amplified the necessity for robust cyber security solutions. This trend is driven by the increasing Internet accessibility via mobile phones, laptops, and tablets, which expands the potential for cyber threats. Moreover, the growing acceptance of mobile devices for m-commerce, bill payments, and GPS usage heightens the significance of securing the confidential data accessed through these devices.

- The proliferation of mobile technology in various sectors underlines the continuous evolution of this market, necessitating advanced cyber security measures.

What are the market trends shaping the Cyber Security Industry?

- The adoption of Internet of Things (IoT) is an emerging market trend. IoT technology is increasingly being implemented in various industries.

- IoT, or the Internet of Things, represents the interconnected network of devices exchanging data in the cloud. The significance of this technology lies in its ability to manage and simplify the analysis and presentation of vast data sets. IoT's potential is vast, extending beyond home automation to various sectors, including healthcare, transportation, and manufacturing. Advancements in IoT are continuous, with devices becoming more integrated and sophisticated. For example, smart homes enable users to control appliances using mobile applications, such as thermostats for power and temperature regulation. In healthcare, IoT-enabled wearable devices monitor vital signs, count calories burned, and track distance traveled.

- IoT's impact on communication between systems, devices, and services is substantial. It allows for real-time data processing and response, ensuring optimal performance and resolution of critical situations. As a professional, it's essential to recognize IoT's potential and adapt to its evolving capabilities. The technology's future integrations with advanced features promise to enhance its functionality, making it an indispensable tool for businesses and individuals alike.

What challenges does the Cyber Security Industry face during its growth?

- The high cost of deployment is a significant challenge that can hinder industry growth. This issue, which is mandatory for businesses to address, can limit expansion and profitability in the sector.

- The escalating costs of implementing and maintaining cyber security solutions pose a significant challenge for The market. With cyber threats becoming increasingly intricate and frequent, organizations are under immense pressure to safeguard their valuable data and systems. However, the financial burden of acquiring advanced hardware and software, hiring skilled cyber security personnel, and conducting regular assessments can be substantial, particularly for small and medium-sized enterprises. The expenses extend beyond initial investment, as ongoing training and compliance with industry regulations also add to the overall cost. Despite these challenges, the importance of robust cyber security strategies cannot be overstated, as data breaches can result in irreparable damage to an organization's reputation and bottom line.

- The continuous evolution of cyber threats necessitates a dynamic approach to cyber security, with organizations requiring agile solutions that can adapt to emerging risks. This dynamic landscape underscores the importance of ongoing investment in cyber security, even as costs remain a significant concern.

Exclusive Technavio Analysis on Customer Landscape

The cyber security market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cyber security market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cyber Security Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cyber security market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AO Kaspersky Lab - This company specializes in providing comprehensive cybersecurity solutions, including Kaspersky Total Security. Their offerings ensure robust protection against digital threats, safeguarding users' data and privacy. By implementing advanced technologies and continuous research, they remain at the forefront of cybersecurity innovation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AO Kaspersky Lab

- Booz Allen Hamilton Holding Corp.

- Broadcom Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems Inc.

- Dell Technologies Inc.

- Fortinet Inc.

- F Secure Corp.

- General Dynamics Corp.

- Hewlett Packard Enterprise Co.

- International Business Machines Corp.

- Juniper Networks Inc.

- Lockheed Martin Corp.

- McAfee LLC

- Microsoft Corp.

- Northrop Grumman Corp.

- RTX Corp.

- Sophos Ltd.

- The Boeing Co.

- Trend Micro Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cyber Security Market

- In January 2024, IBM Security announced the acquisition of Reason Software, a leading AI-powered threat detection and response company, to enhance its X-Force Threat Intelligence platform. This strategic move aimed to bolster IBM's threat detection capabilities and better protect clients from advanced cyber threats (IBM Press Release, 2024).

- In March 2024, Microsoft and Google formed a partnership to collaborate on zero-trust security solutions. This alliance aimed to integrate Microsoft Azure and Google Cloud security services, providing customers with a more comprehensive and seamless security experience (Microsoft Blog, 2024).

- In April 2025, CrowdStrike, a leading cybersecurity company, raised USD1.1 billion in a Series F funding round. This significant investment will support the company's continued growth and innovation in cloud-native endpoint protection and threat intelligence (CrowdStrike Press Release, 2025).

- In May 2025, the European Union's General Data Protection Regulation (GDPR) was expanded to include mandatory breach reporting for all organizations processing personal data, regardless of their size or location. This policy change aims to strengthen data protection and enhance transparency for EU citizens (European Commission Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cyber Security Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

261 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.7% |

|

Market growth 2025-2029 |

USD 269.8 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

13.2 |

|

Key countries |

US, China, Japan, Germany, Canada, France, India, Russia, UK, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cybersecurity market continues to evolve, with new threats and technologies shaping its dynamic landscape. Machine learning security solutions are increasingly being integrated into vulnerability management programs to enhance intrusion detection capabilities. Zero trust architecture is gaining traction as organizations adopt a more proactive approach to security. Intrusion detection systems employing artificial intelligence and threat modeling techniques are becoming essential components of robust cybersecurity incident response strategies. Data encryption techniques and malware analysis tools are integral parts of a comprehensive security strategy, with automation security tools streamlining processes and improving efficiency. Ransomware attack prevention and cryptography algorithms are crucial elements in securing digital assets.

- Endpoint detection response and security awareness training are vital components of a holistic approach to cybersecurity. Network security protocols, threat intelligence platforms, and vulnerability assessment scanning are essential for maintaining a strong defense against social engineering attacks and security orchestration automation. Data loss prevention and risk assessment methodologies help minimize potential damage from breaches. Access control management and penetration testing methodologies ensure that vulnerabilities are identified and addressed before they can be exploited. According to recent market research, the cybersecurity industry is expected to grow by over 12% annually, underscoring the increasing importance of robust security measures in today's digital world.

- For instance, a leading financial institution reported a 30% reduction in security incidents after implementing a multi-factor authentication system and a response platform for cybersecurity threats.

What are the Key Data Covered in this Cyber Security Market Research and Growth Report?

-

What is the expected growth of the Cyber Security Market between 2025 and 2029?

-

USD 269.8 billion, at a CAGR of 16.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Government, BFSI, ICT, Manufacturing, and Others), Deployment (On-premises and Cloud-based), Product (Solution and Services), Sector (Large enterprises and SMEs), Type (Cloud, End-point and IoT, Network, and Application), and Geography (North America, Europe, APAC, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Increase in use of mobile devices, High cost of deployment

-

-

Who are the major players in the Cyber Security Market?

-

AO Kaspersky Lab, Booz Allen Hamilton Holding Corp., Broadcom Inc., Check Point Software Technologies Ltd., Cisco Systems Inc., Dell Technologies Inc., Fortinet Inc., F Secure Corp., General Dynamics Corp., Hewlett Packard Enterprise Co., International Business Machines Corp., Juniper Networks Inc., Lockheed Martin Corp., McAfee LLC, Microsoft Corp., Northrop Grumman Corp., RTX Corp., Sophos Ltd., The Boeing Co., and Trend Micro Inc.

-

Market Research Insights

- The market is a dynamic and ever-evolving landscape, requiring constant attention and adaptation to address emerging threats. According to recent industry reports, the number of recorded cyber attacks increased by 32% last year, underscoring the urgent need for robust security measures. Furthermore, market projections indicate a growth rate of approximately 12% annually over the next five years, as businesses continue to invest in advanced security solutions. Endpoint security solutions, for instance, have seen significant adoption due to the rise in remote work and the associated risks.

- In one instance, a company implementing a new endpoint security solution experienced a 45% reduction in security incidents. These trends underscore the importance of staying informed and proactive in the face of evolving cyber threats.

We can help! Our analysts can customize this cyber security market research report to meet your requirements.

RIA -

RIA -