Europe Craft Beer Market Size 2026-2030

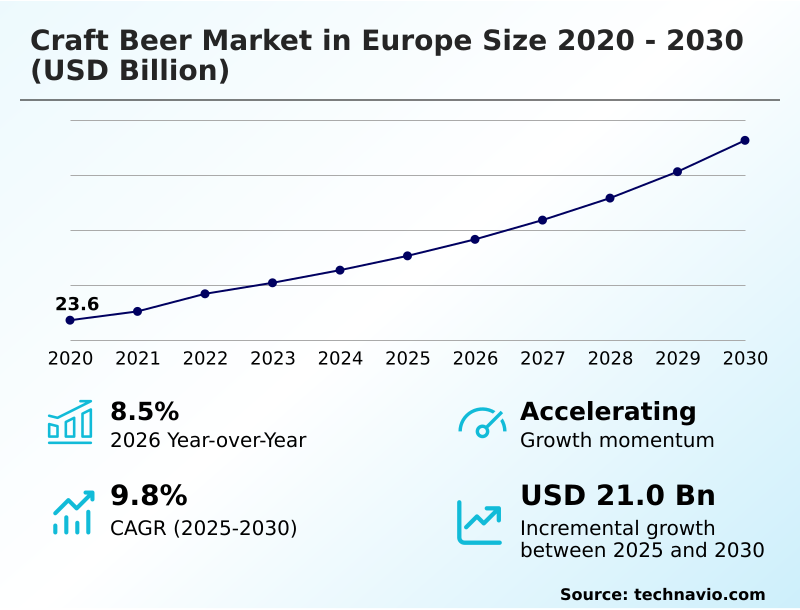

The europe craft beer market size is valued to increase by USD 21 billion, at a CAGR of 9.8% from 2025 to 2030. Increasing demand for premium beverages will drive the europe craft beer market.

Major Market Trends & Insights

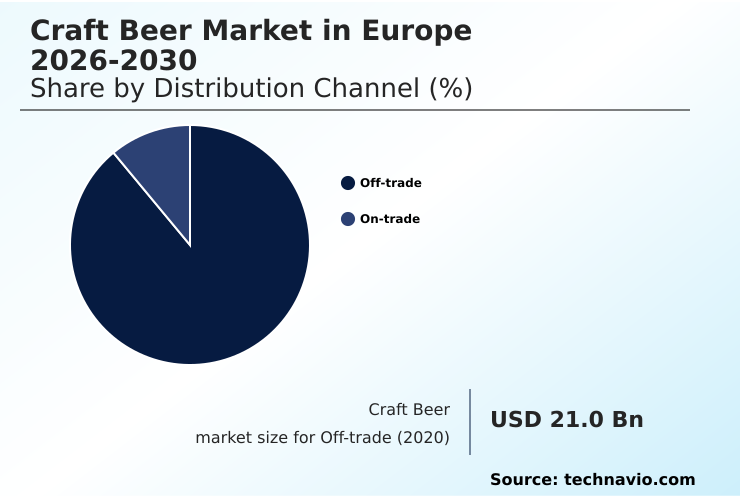

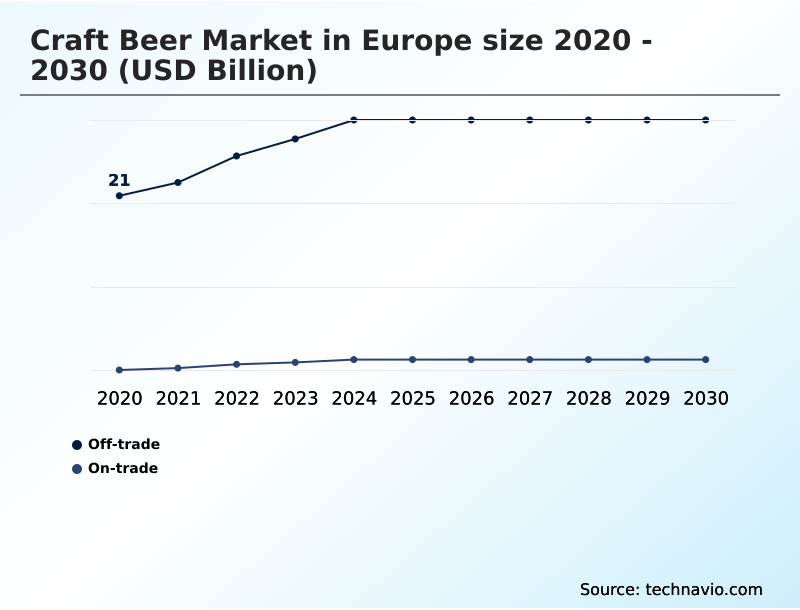

- By Distribution Channel - Off-trade segment was valued at USD 29 billion in 2024

- By Product - IPA-based craft beer segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 32.7 billion

- Market Future Opportunities: USD 21 billion

- CAGR from 2025 to 2030 : 9.8%

Market Summary

- The craft beer market in Europe is undergoing a significant transformation, driven by consumer demand for authenticity, quality, and innovation. This evolution is characterized by a shift away from mass-produced beverages toward artisanal products that feature complex flavor profiles and unique ingredients.

- Key market dynamics include the rise of direct-to-consumer sales channels, the growing popularity of non-alcoholic and low-alcohol craft options, and a strong focus on sustainable and localized production. For example, a mid-sized brewery can optimize its supply chain by partnering with local farms for heritage hop varieties, reducing transportation costs and enhancing its brand story around sustainability and regional identity.

- This strategy not only caters to eco-conscious consumers but also provides a unique selling proposition in a crowded marketplace. However, the industry grapples with challenges such as volatile raw material prices and complex, fragmented regulatory landscapes across different nations.

- Success in this environment requires a balance of creative brewing, strategic sourcing, and adept navigation of both market trends and operational hurdles, utilizing tools like advanced yeast management and efficient packaging lines.

What will be the Size of the Europe Craft Beer Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Europe Craft Beer Market Segmented?

The europe craft beer industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Off-trade

- On-trade

- Product

- IPA-based craft beer

- Seasonal-based craft beer

- Pale ale-based craft beer

- Amber ale-based craft beer

- Others

- Packaging

- Cans

- Bottles

- Kegs

- Geography

- Europe

- UK

- Germany

- Europe

By Distribution Channel Insights

The off-trade segment is estimated to witness significant growth during the forecast period.

The off-trade segment has become the primary volume driver as consumers seek artisanal products for home consumption.

Growth is supported by expanding shelf space in retail chains and the rise of e-commerce platforms offering direct-to-doorstep delivery, which in turn builds brand loyalty.

This channel allows for a diverse beverage portfolio, from traditional cask ale to modern sour beers, with some producers even offering options for private label clients.

Advanced automated packaging lines ensure product integrity, while innovations in dealcoholization processes are expanding offerings.

Effective yeast management tools are critical for consistency, with some breweries reporting a 15% improvement in batch uniformity, ensuring that everything from a grodziskie to a classic cask conditioned ale meets quality standards.

The Off-trade segment was valued at USD 29 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

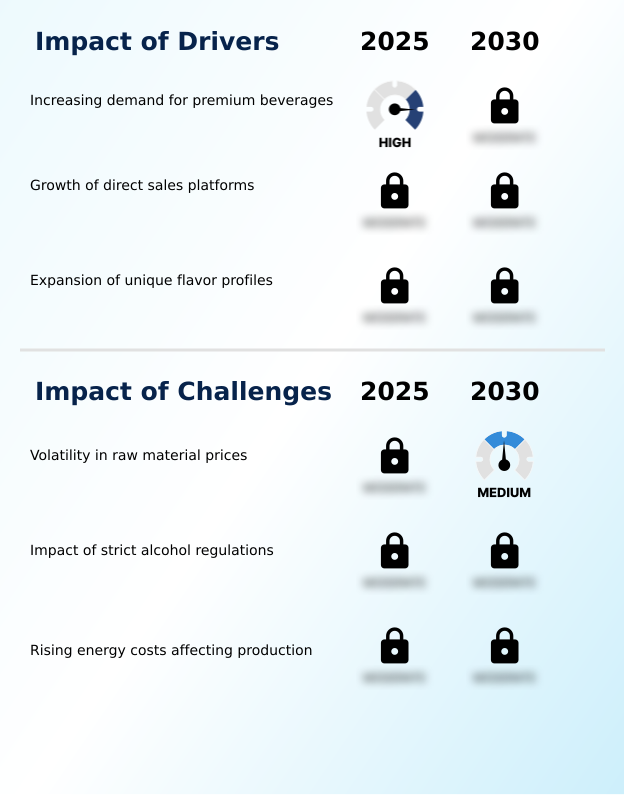

- Navigating the craft beer market in Europe requires a multifaceted strategy. A key concern is the impact of raw material price volatility on breweries, which necessitates robust sourcing strategies and efficient production. Utilizing technology for brewing process consistency is therefore paramount.

- Simultaneously, companies are navigating complex European alcohol advertising regulations by shifting focus to utilizing social media for craft beer marketing and promotion. The growth of direct to consumer beer sales channels is a major opportunity, as the role of taprooms in building community and brand loyalty cannot be overstated.

- This direct model aids in expanding craft beer appeal to new consumer demographics. Operationally, managing cold chain logistics for unpasteurized craft beer is a critical challenge, directly linked to quality perception. Successful premiumization strategies for independent European breweries often involve advanced barrel aging techniques for high-end specialty beers and sourcing local and heritage hop varieties for differentiation.

- This helps in meeting demand for experimental and sour beer styles while balancing flavor innovation with traditional beer styles. The debate over craft beer packaging trends focusing on cans versus bottles continues, with cans showing an adoption rate 20% higher for new product launches due to logistical benefits.

- Finally, market entry strategies for new craft beer brewers must account for these dynamics, alongside the impact of consumer health and wellness trends on brewing and overcoming challenges in craft beer distribution networks. Implementing sustainable brewery waste management solutions is also becoming a standard expectation.

What are the key market drivers leading to the rise in the adoption of Europe Craft Beer Industry?

- The increasing demand for premium beverages, characterized by artisanal quality and unique flavor profiles, is a key driver for market growth.

- The market is propelled by the premiumization trend and the expansion of direct to consumer sales through e commerce websites and subscription models.

- The taproom model fosters experiential consumption, allowing brewers to showcase products with unique fermentation profiles and adjunct ingredients. Innovation is constant, with brewers utilizing new aroma hop varieties and advanced dry hopping techniques.

- This focus on unique flavors has led to a 40% rise in experimental batches.

- Barrel aging program initiatives and the use of wild yeast strains and specialized malts create high-value products that command premium pricing, appealing to consumers seeking distinct and complex artisanal beverages.

What are the market trends shaping the Europe Craft Beer Industry?

- The growing adoption of non-alcoholic options represents a key market trend. Consumers are increasingly seeking sophisticated craft beverages that deliver complex flavors without the alcohol.

- A major trend is the adoption of sustainable brewing practices aligned with circular economy principles, where breweries are implementing heat recovery systems that recapture up to 20% of thermal energy. The focus on regional sourcing is promoting heritage hop varieties and terroir beers. This reduces the carbon footprint and supports local agriculture.

- The sober curious movement has driven demand for high-quality non alcoholic alternatives, leading to investment in vacuum distillation units and reverse osmosis systems to preserve flavor. Some innovative facilities are also exploring carbon capture technology to reclaim CO2.

- The use of hyper-local ingredients, including wet hops and revived landrace hop variety, further enhances product uniqueness, with a 30% increase in breweries launching region-specific series.

What challenges does the Europe Craft Beer Industry face during its growth?

- Volatility in the prices of essential raw materials, such as hops and barley, presents a significant challenge to the industry's growth and profitability.

- Breweries face significant operational challenges, including rising raw material costs that impact the production of everything from sessionable beers to high gravity beers. The need for reliable cold chain services is critical for distributing unpasteurized craft products, adding logistical complexity and cost. To mitigate this, some firms have improved logistics to reduce spoilage by 15%.

- Instability requires adept craft maltings relationships and supply chain transparency. Firms that leverage digital marketing and establish their taprooms as community hubs build resilience. Models like gypsy brewing and contract brewing offer asset-light alternatives. However, maintaining quality with strains like Brettanomyces and Lactobacillus requires strict controls, as failure can affect brand perception significantly.

Exclusive Technavio Analysis on Customer Landscape

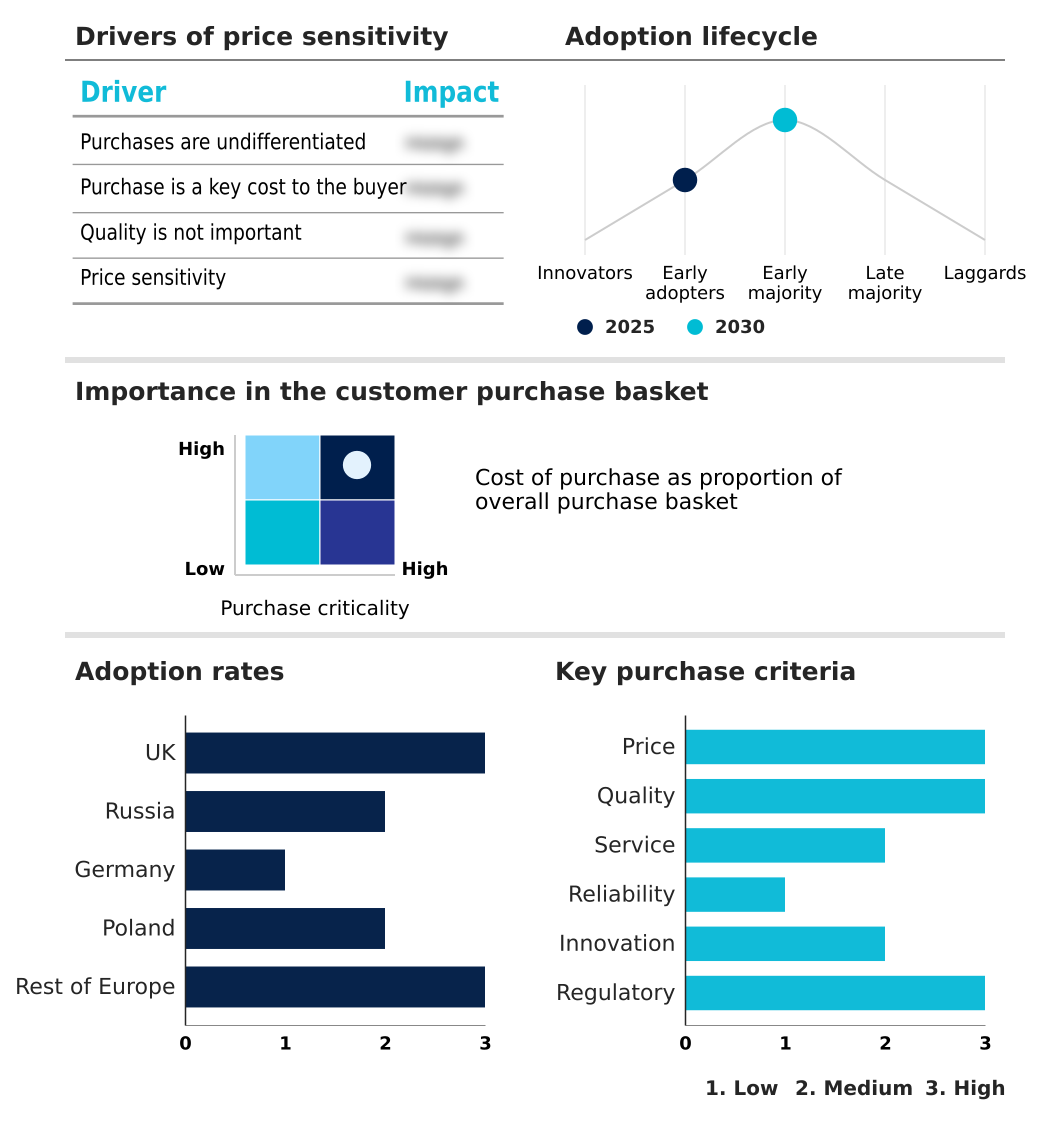

The europe craft beer market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe craft beer market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Craft Beer Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe craft beer market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Anheuser Busch InBev SA NV - Core offerings include a diverse portfolio of craft beer styles, ranging from traditional ales to innovative IPAs, targeting various consumer preferences and market segments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anheuser Busch InBev SA NV

- Asahi Group Holdings Ltd.

- Boston Brewery

- Brasserie De La Senne

- BrewDog Plc

- Buxton Brewery Co. Ltd.

- Carlsberg Breweries AS

- Cloudwater Brew Co.

- Duvel Moortgat NV

- German Kraft Brewery Ltd.

- Lagunitas Brewing Co.

- Lervig Aktiebryggeri AS

- Magic Rock Brewing Co. Ltd.

- Mikkeller ApS

- Royal Swinkels

- Stone Brewing Co. LLC

- Thornbridge Brewery

- Van Pur SA

- Wild Beer Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Europe craft beer market

- In January, 2025, Cloudwater Brew Co. expanded its premium barrel aging program, releasing a limited series of blended ales that demonstrated the market capacity for high-end offerings.

- In February, 2025, Magic Rock Brewing Co. Ltd. launched a new integrated digital platform that connects its taproom inventory with its online store, allowing for real-time stock updates and local delivery.

- In February, 2025, Stone Brewing Co. LLC introduced a new range of non-alcoholic west coast style pale ales across its European distribution hubs to meet rising consumer appetite for hop-forward beverages that lack alcohol.

- In January, 2025, Thornbridge Brewery implemented a new solar-powered refrigeration system at its primary production site to reduce its reliance on the traditional power grid and lower its carbon footprint.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Craft Beer Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 211 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.8% |

| Market growth 2026-2030 | USD 21.0 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.5% |

| Key countries | UK, Russia, Germany, Poland and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The European craft beer sector is defined by intense innovation in production and ingredients. The use of aroma hop varieties and specialized malts is fundamental, with brewers employing sophisticated dry hopping techniques and managing unique fermentation profiles to create differentiation. This extends to high gravity beers, sour beers, and traditional cask conditioned ales and real ale.

- The application of wild yeast strains like Brettanomyces and Lactobacillus is increasingly common for achieving terroir driven flavors in styles like gose and other experimental brews. On the operational side, boardroom decisions are increasingly focused on capital investment in dealcoholization processes using vacuum distillation units or reverse osmosis systems, driven by consumer health trends.

- Breweries are also adopting carbon capture technology and heat recovery systems to improve sustainability. Investment in these technologies has enabled some facilities to reduce energy consumption by over 15%, directly impacting profitability. Success hinges on mastering everything from a barrel aging program to ensuring the quality of unpasteurized craft products via superior cold chain services.

What are the Key Data Covered in this Europe Craft Beer Market Research and Growth Report?

-

What is the expected growth of the Europe Craft Beer Market between 2026 and 2030?

-

USD 21 billion, at a CAGR of 9.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Off-trade, and On-trade), Product (IPA-based craft beer, Seasonal-based craft beer, Pale ale-based craft beer, Amber ale-based craft beer, and Others), Packaging (Cans, Bottles, and Kegs) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for premium beverages, Volatility in raw material prices

-

-

Who are the major players in the Europe Craft Beer Market?

-

Anheuser Busch InBev SA NV, Asahi Group Holdings Ltd., Boston Brewery, Brasserie De La Senne, BrewDog Plc, Buxton Brewery Co. Ltd., Carlsberg Breweries AS, Cloudwater Brew Co., Duvel Moortgat NV, German Kraft Brewery Ltd., Lagunitas Brewing Co., Lervig Aktiebryggeri AS, Magic Rock Brewing Co. Ltd., Mikkeller ApS, Royal Swinkels, Stone Brewing Co. LLC, Thornbridge Brewery, Van Pur SA and Wild Beer Co.

-

Market Research Insights

- Market dynamics are shaped by a pronounced consumer shift toward premium and authentic experiences. The expansion of the taproom model and direct to consumer sales via e commerce websites has been pivotal, enabling breweries to improve margins by up to 40% and foster brand loyalty. This is complemented by the premiumization trend, with consumers embracing experiential consumption.

- The growth in non alcoholic alternatives, driven by the sober curious movement, has led to a 25% increase in product launches in this category. Sustainable brewing practices are no longer optional, with environmental stewardship becoming a core brand pillar.

- Breweries are leveraging digital marketing to connect with consumers, using food pairing suggestions and storytelling to differentiate their beverage portfolio and solidify their market position.

We can help! Our analysts can customize this europe craft beer market research report to meet your requirements.

RIA -

RIA -