Cloud Machine Learning Market Size 2025-2029

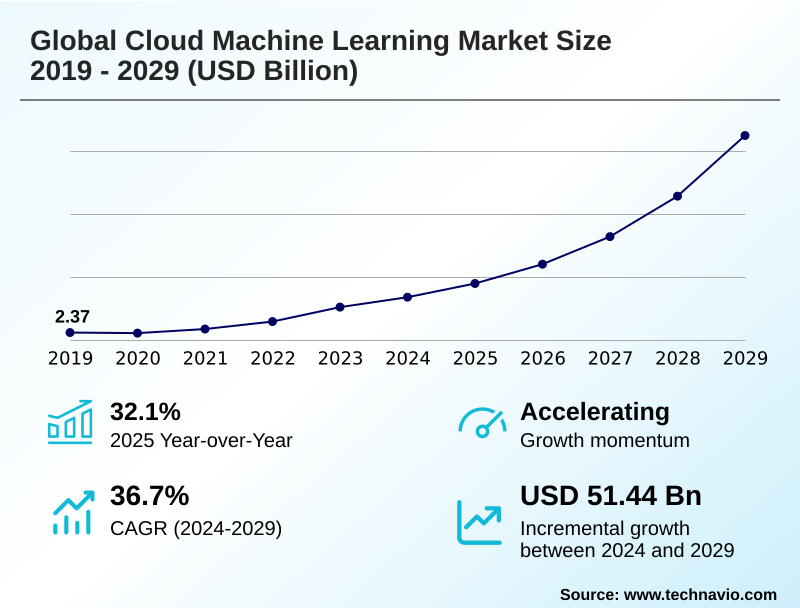

The cloud machine learning market size is valued to increase by USD 51.44 billion, at a CAGR of 36.7% from 2024 to 2029. Escalating volume and complexity of data will drive the cloud machine learning market.

Major Market Trends & Insights

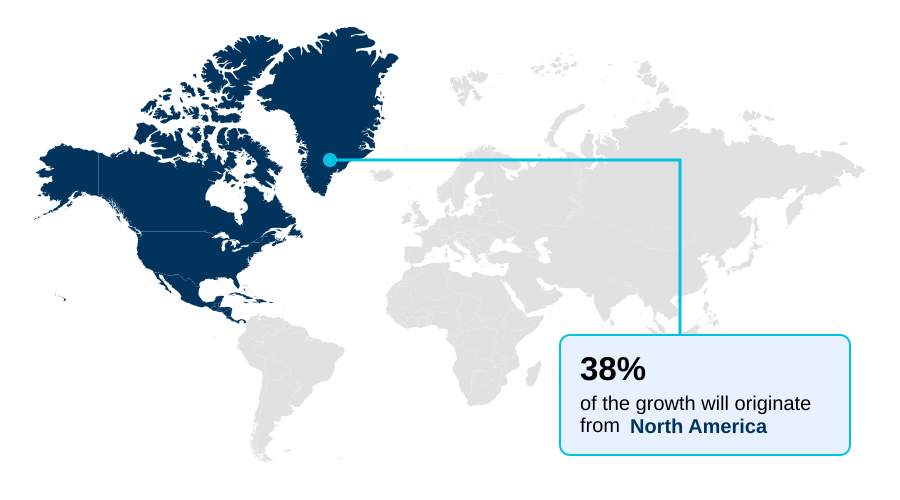

- North America dominated the market and accounted for a 37.7% growth during the forecast period.

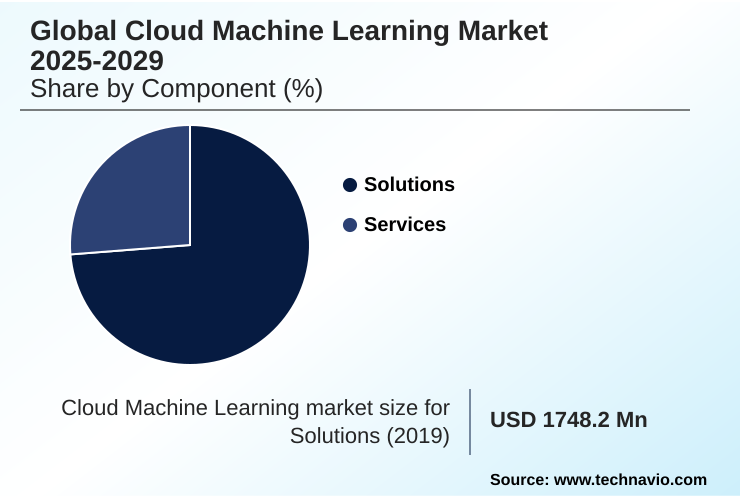

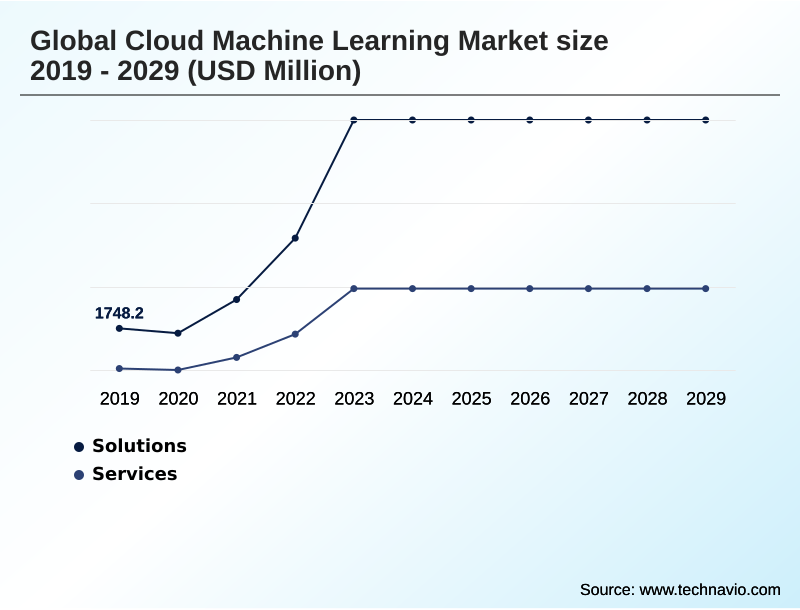

- By Component - Solutions segment was valued at USD 7.59 billion in 2023

- By Deployment - Public cloud segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 62.69 billion

- Market Future Opportunities: USD 51.44 billion

- CAGR from 2024 to 2029 : 36.7%

Market Summary

- The cloud machine learning market is undergoing a significant transformation, driven by the democratization of advanced AI capabilities. Organizations are increasingly shifting from capital-intensive on-premises infrastructures to scalable, flexible cloud environments to harness the power of big data technologies. This transition is fueled by the escalating demand for data-driven decisions across all sectors.

- Key trends shaping the landscape include the pervasive integration of generative artificial intelligence, the operational discipline of machine learning operations (MLOps), and the convergence of cloud with edge computing for low-latency applications. For example, in the manufacturing sector, businesses utilize cloud platforms to analyze real-time sensor data for predictive maintenance, forecasting equipment failures to minimize downtime and optimize operational efficiency.

- However, realizing the full potential of these technologies is contingent on navigating challenges such as a persistent digital skills gap, the complexities of data governance, and the need to demonstrate a clear return on investment from escalating cloud infrastructure expenses.

- The market's trajectory points toward more accessible, automated, and integrated AI solutions that are embedded into core business processes, enabling a new wave of innovation and competitive advantage.

What will be the Size of the Cloud Machine Learning Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Cloud Machine Learning Market Segmented?

The cloud machine learning industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Solutions

- Services

- Deployment

- Public cloud

- Hybrid cloud

- Private cloud

- Application

- Marketing and advertising analytics

- Fraud detection and risk management

- Predictive maintenance and demand forecasting

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The solutions segment is defined by software platforms and tools providing the foundational infrastructure for developing and managing machine learning models.

A key component involves Machine Learning as a Service (MLaaS) offerings, which feature tools for data preprocessing and model deployment, making advanced AI-powered applications accessible through a pay-as-you-go model.

Specialized platforms for machine learning operations (MLOps) are also critical, focusing on model management and the entire lifecycle to ensure scalability and governance.

The rise of automated machine learning, or AutoML, which can accelerate development cycles by up to 30%, further democratizes access.

These solutions increasingly incorporate generative artificial intelligence, edge computing, and capabilities for natural language processing and computer vision, enabling more sophisticated and intelligent applications.

The Solutions segment was valued at USD 7.59 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cloud Machine Learning Market Demand is Rising in North America Request Free Sample

North America leads the global cloud machine learning market, commanding over 32% of the market share, driven by high adoption rates and the presence of major technology providers.

The region's focus on AI-first strategies and high-performance computing fosters innovation across finance, healthcare, and retail. Meanwhile, APAC is the fastest-growing region, fueled by digital transformation and government initiatives.

The expansion of cloud infrastructure is critical, with investments aimed at reducing latency and complying with data sovereignty laws.

The convergence with edge computing is creating new opportunities, with thick edge locations enabling real-time processing that can improve equipment runtime by 10%.

Across regions, the push for AI-driven automation is balanced by the need for secure and sovereign cloud solutions to manage sensitive data and navigate complex regulatory environments.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The enterprise adoption of cloud machine learning is accelerating, driven by the clear advantages of integrating AI into core business operations. A primary application is cloud machine learning for fraud detection, where financial institutions leverage scalable platforms to analyze transaction patterns in real time.

- Similarly, the industrial sector benefits from cloud machine learning for predictive maintenance, using sensor data to prevent costly equipment failures. The technology is rapidly advancing, with generative AI in cloud service offerings becoming a standard feature, enabling businesses to innovate with new content and services.

- To manage this complexity, organizations are adopting MLOps for scalable model deployment, which can more than double the speed of model updates compared to manual methods. This operational discipline is crucial for deploying large-scale inference models on cloud architectures efficiently. Architectural choices are also evolving, with hybrid cloud for sensitive data workloads providing a balance of security and flexibility.

- For applications requiring instant response, edge AI for low-latency applications is becoming essential. However, challenges remain, including managing costs of generative AI training and the impact of skills gap on AI adoption. Demonstrating ROI for AI cloud projects is a key executive focus, requiring robust strategies for effective cloud cost optimization.

- Furthermore, navigating data privacy in cloud machine learning and the challenges in cross-border data transfers for AI are critical for global operations. Building AI-ready data architecture on cloud and understanding the role of GPUs in cloud machine learning are foundational steps for any organization embarking on this transformative journey, particularly in sectors like cloud machine learning in financial services.

What are the key market drivers leading to the rise in the adoption of Cloud Machine Learning Industry?

- The escalating volume and complexity of data serve as a key driver for the market, necessitating powerful cloud-based solutions for analysis and insight extraction.

- Market growth is propelled by a confluence of powerful drivers. The exponential increase in data volume and complexity necessitates the scalable computational resources offered by cloud platforms.

- Organizations are leveraging foundation models and multimodal generative models to transform vast data lakes and data warehousing assets into actionable insights. This is fueling a surge in demand for AI-powered applications, with 78% of businesses now reporting AI use.

- The economic advantages are also a significant factor, as the cloud's pay-as-you-go model and the availability of containerized AI software lower the barrier to entry.

- This shift is reflected in the over 20% increase in public cloud spending, as companies prioritize digital skills gap closure and a clear return on investment over traditional IT budget allocation.

What are the market trends shaping the Cloud Machine Learning Industry?

- The pervasive integration of generative artificial intelligence is emerging as a significant market trend. This technology is becoming a fundamental component of cloud service offerings, driving innovation and growth.

- The market is being reshaped by three pivotal trends. First, the widespread integration of generative artificial intelligence is transforming service offerings, with deep learning models capable of creating novel content. Second, the rise of machine learning operations (MLOps) is industrializing AI deployment.

- North America's MLOps market dominance, with over 41% share, highlights the strategic move toward scalable and governed model management. This disciplined approach ensures the reliability of predictive analytics. Third, the convergence of cloud with edge computing enables real-time data processing and low latency applications, which can reduce processing delays by over 50%.

- This synergy, powered by GPU orchestration and accessible through MLOps platforms, allows for sophisticated local data processing while leveraging the cloud for computationally intensive tasks like continuous training.

What challenges does the Cloud Machine Learning Industry face during its growth?

- Complexities surrounding data privacy, security, and governance present a key challenge affecting the growth of the industry.

- Navigating the complexities of cost, skills, and governance remains a primary challenge. While cloud platforms offer scalability, 67% of businesses anticipate rising cloud costs, which directly impacts the financial viability of large-scale AI projects. Compounding this is the difficulty in quantifying success, as a staggering 82% of organizations lack a formal strategy for tracking AI return on investment.

- A persistent digital skills gap in data science and data engineering further hampers the ability to leverage big data technologies effectively and make data-driven decisions. This creates a reliance on specialized platforms like Amazon SageMaker or watsonx.ai.

- Moreover, ensuring data privacy and security within hybrid cloud environments and private cloud AI deployments presents ongoing hurdles, requiring robust frameworks for governance and compliance.

Exclusive Technavio Analysis on Customer Landscape

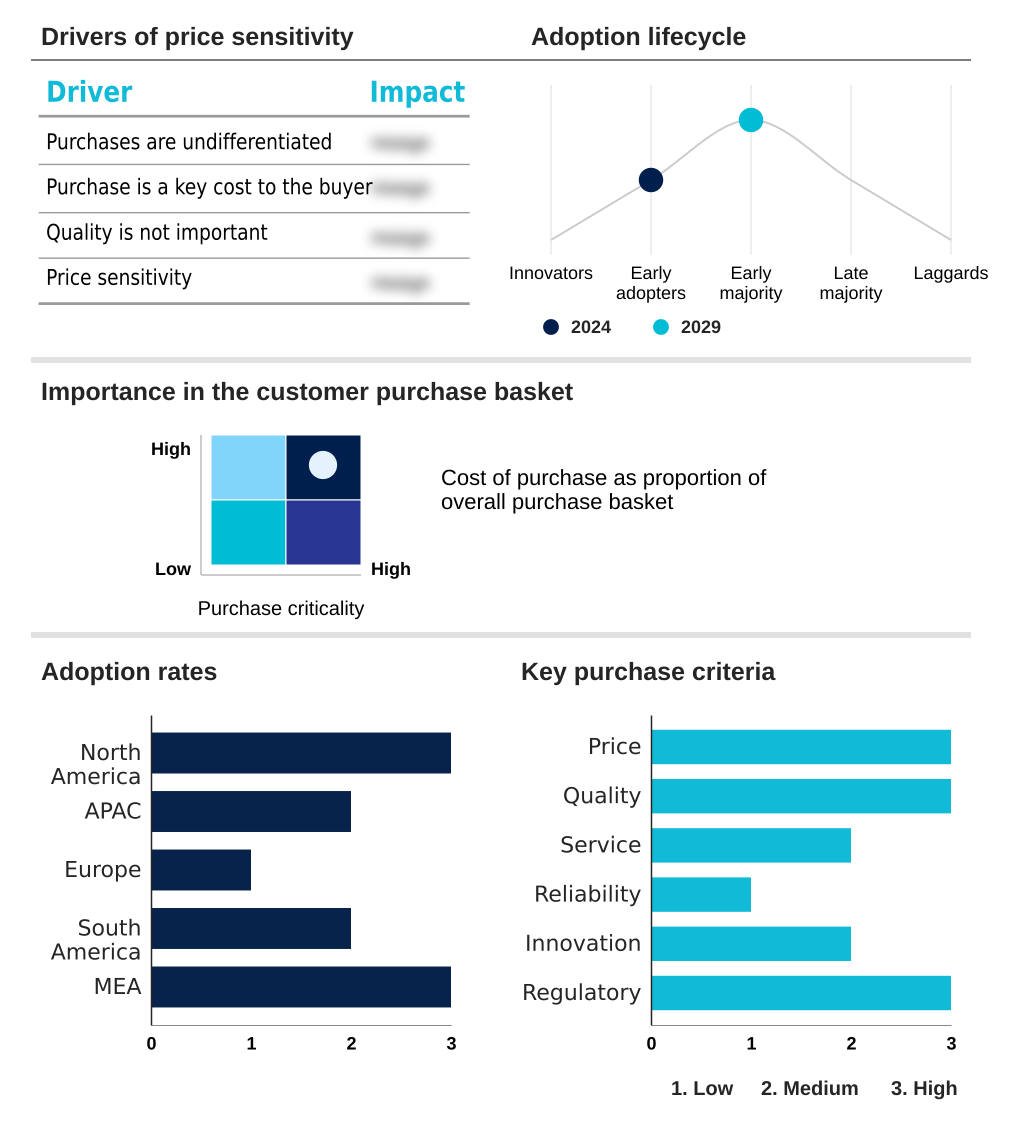

The cloud machine learning market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cloud machine learning market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cloud Machine Learning Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cloud machine learning market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alibaba Group Holding Ltd. - The offering includes a comprehensive AI platform supporting the entire model lifecycle, from development and training to deployment, utilizing AutoML, visual workflows, and scalable GPU clusters.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Group Holding Ltd.

- Amazon Web Services Inc.

- Anaconda Inc.

- Baidu Inc.

- Cisco Systems Inc.

- Cloudera Inc.

- DataRobot Inc.

- Dell Technologies Inc.

- Google LLC

- Hewlett Packard

- IBM Corp.

- Microsoft Corp.

- NVIDIA Corp.

- Open Text Corp.

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- Snowflake Inc.

- Tencent Holdings Ltd.

- Teradata Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cloud machine learning market

- In February, 2025, Alibaba Cloud announced the launch of its first cloud region in Mexico, a move designed to provide scalable and secure cloud services and strengthen the AI ecosystem in Latin America.

- In October, 2024, Infineon launched its DEEPCRAFT Edge AI development suite, aimed at simplifying the deployment of artificial intelligence models on its microcontroller platforms for edge computing applications.

- In September, 2024, Alibaba Cloud introduced over 100 new open-source AI models and released its Qwen 2 large language model series, underscoring its commitment to advancing AI innovation.

- In August, 2024, Broadcom and Hitachi Vantara launched a new private and hybrid cloud solution designed to help organizations manage data proliferation and the increasing demands of AI workloads.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cloud Machine Learning Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 36.7% |

| Market growth 2025-2029 | USD 51444.6 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 32.1% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, UAE, Saudi Arabia, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is defined by a strategic shift from experimental AI projects to the industrialization of machine learning, embedded within core business processes. This evolution is driven by the accessibility of high-performance computing, enabling the use of sophisticated deep learning models and foundation models for a wide range of applications, including predictive analytics and real-time fraud detection.

- A key boardroom consideration is the adoption of machine learning operations (MLOps), which necessitates budgeting for specialized platforms and data science proficiency to ensure governance and a quantifiable return on investment. Effective cloud cost optimization is paramount, as organizations have demonstrated the ability to reduce infrastructure waste by 20 to 30% through disciplined management.

- The landscape is advancing with technologies like multimodal generative models and agentic workflows, powered by GPU orchestration and containerized AI software. Success hinges on mastering data engineering to build AI-ready intelligence from data lakes and data warehousing, while navigating challenges like data sovereignty laws, insecure APIs, and the demand for predictive maintenance and demand forecasting.

What are the Key Data Covered in this Cloud Machine Learning Market Research and Growth Report?

-

What is the expected growth of the Cloud Machine Learning Market between 2025 and 2029?

-

USD 51.44 billion, at a CAGR of 36.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions, and Services), Deployment (Public cloud, Hybrid cloud, and Private cloud), Application (Marketing and advertising analytics, Fraud detection and risk management, Predictive maintenance and demand forecasting, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating volume and complexity of data, Data privacy, security, and governance complexities

-

-

Who are the major players in the Cloud Machine Learning Market?

-

Alibaba Group Holding Ltd., Amazon Web Services Inc., Anaconda Inc., Baidu Inc., Cisco Systems Inc., Cloudera Inc., DataRobot Inc., Dell Technologies Inc., Google LLC, Hewlett Packard, IBM Corp., Microsoft Corp., NVIDIA Corp., Open Text Corp., Oracle Corp., Salesforce Inc., SAP SE, Snowflake Inc., Tencent Holdings Ltd. and Teradata Corp.

-

Market Research Insights

- The market's momentum is shaped by the compelling economics of the pay-as-you-go model, which lowers entry barriers for AI adoption. With 78% of organizations reporting AI use, the demand for accessible and scalable intelligent applications is surging.

- This is driving a shift toward AI-first strategies, where businesses leverage platforms like Vertex AI platform and Azure Machine Learning to modernize data architectures. The focus on return on investment is critical, as effective cloud cost optimization strategies can reduce infrastructure waste by 20% to 30%.

- This dynamic interplay between cost-efficiency, widespread AI adoption, and the strategic need for a clear ROI is accelerating the integration of cloud machine learning into core business operations, fostering innovation while demanding rigorous financial governance and IT budget allocation.

We can help! Our analysts can customize this cloud machine learning market research report to meet your requirements.