Clinical Workflow Solution Market Size 2024-2028

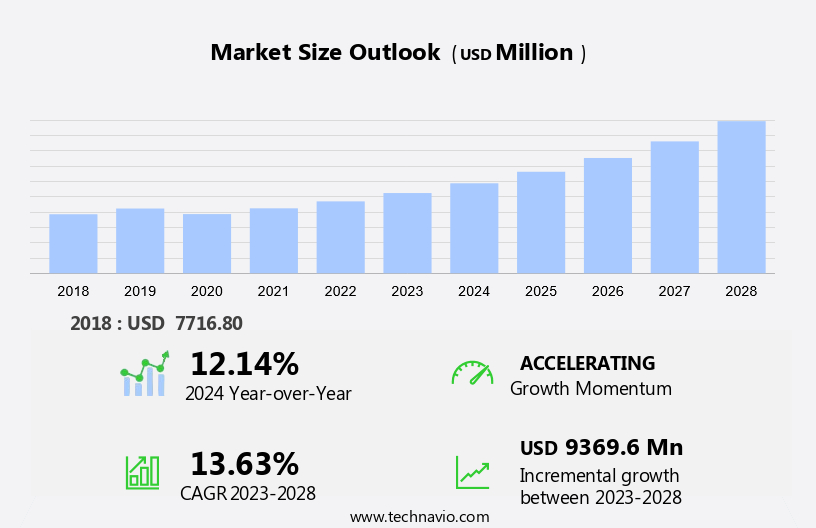

The clinical workflow solution market size is forecast to increase by USD 9.37 billion, at a CAGR of 13.63% between 2023 and 2028. Clinical workflow solutions are increasingly being adopted by healthcare providers in the US to streamline care delivery, improve patient outcomes, and enhance safety. These solutions offer numerous advantages, including the ability to close care gaps, facilitate visit planning and call scheduling, and support economic integration. The market is driven by the growing demand for cutting-edge clinical research and advanced care management solutions to remote patient monitoring that enable effective collaboration among nursing staff, doctors, pharmacists, and residents' relatives.

Furthermore, the trend towards connected hospitals and clinical communications is fueling the adoption of clinical workflow solutions, which enable real-time information exchange and help prevent medical errors. However, challenges such as interoperability and security issues must be addressed to ensure the successful implementation of these solutions. Overall, clinical workflow solutions are essential for effective care management and delivery in today's complex healthcare environment.

Clinical workflow solutions are essential tools for hospitals and clinics to manage patient volume efficiently and effectively. These solutions help streamline clinical care communications, optimize patient flow metrics, and enhance safety and care delivery. Electronic Health Records (EHRs) form the backbone of clinical workflow solutions, enabling IT professionals and nurses to access patient data in real-time. However, interoperability issues between different systems and health information exchanges remain a significant challenge. Telehealth and remote patient monitoring have become crucial components of clinical workflow solutions, allowing healthcare providers to deliver care beyond traditional clinic settings. Clinical workflow solutions offer flexibility, enabling healthcare organizations to adapt to changing patient needs and healthcare spending.

Interoperability solutions address the challenge of seamless data exchange between different systems, ensuring accurate and timely patient data insights. Predictive analytics and clinical pathways are essential features of advanced clinical workflow solutions, providing healthcare teams with valuable patient data insights to improve care quality and patient journey. Surveillance units in hospitals can benefit from clinical workflow solutions to monitor patient safety and care effectively. Overall, clinical workflow solutions are vital for healthcare organizations to deliver efficient, cost-effective, and high-quality care.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hospitals

- Long-term care facilities

- Ambulatory care centers

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- Asia

- China

- Rest of World (ROW)

- North America

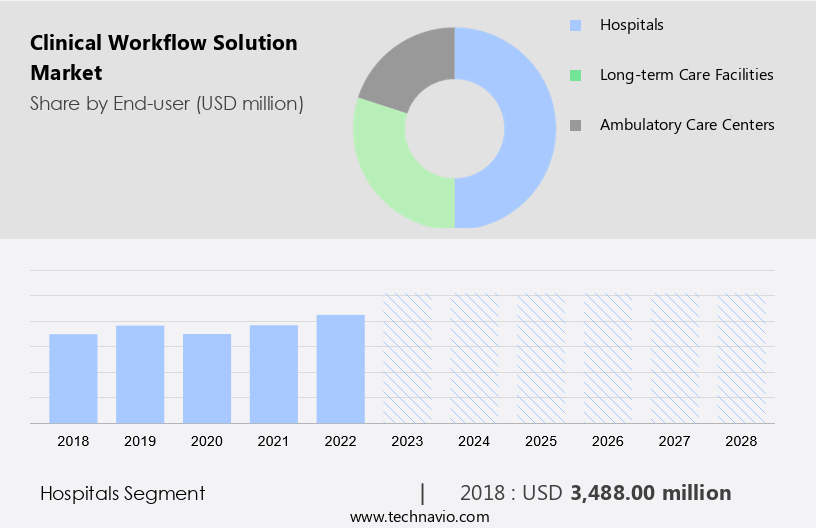

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period. Clinical workflow solutions play a vital role in various healthcare departments, including radiology, laboratory, and pharmacy, by standardizing procedures, minimizing human errors, and improving interdepartmental communication. In 2023, the hospitals sector held a significant market share in The market due to the increasing number of hospitals and the need to manage the accompanying data efficiently. Furthermore, government initiatives aiming to advance the medical industry and simplify the handling of vast hospital data are expected to fuel market growth. Additionally, the expanding demand for workflow optimization and the ongoing trend toward connected hospitals are projected to boost the market throughout the forecast period. Long-term care facilities, eHealth, medical tourism, and clinics also benefit from these solutions by ensuring quality healthcare, surveillance, safety, and flexibility for physicians, surgeons, nurses, patients, and units. Reimbursement levels continue to be a crucial factor driving the adoption of clinical workflow solutions in the healthcare sector.

Get a glance at the market share of various segments Request Free Sample

The hospitals segment accounted for USD 3.49 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

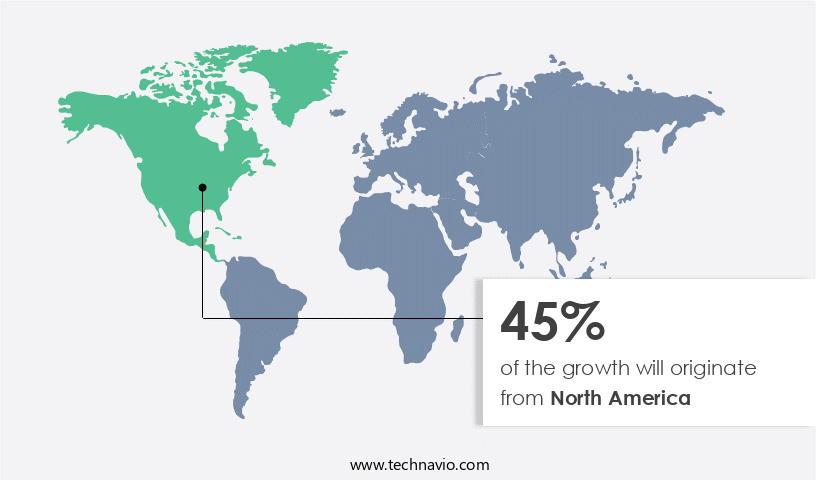

North America is estimated to contribute 45% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In the market, North America held a significant market share in 2023. This growth can be attributed to increased government initiatives promoting the efficient use of interoperability and electronic health records (EHRs), as well as the increasing number of hospital admissions and resulting data generation. Furthermore, the emphasis on quality healthcare and patient safety, coupled with rising healthcare spending on digitalization for secure data transfer between organizations, is driving the expansion of the market in the region. The escalating cost of managing chronic illnesses such as diabetes, cancer, and heart disease in the US necessitates the implementation of advanced clinical workflow solutions.

These solutions enable long-term care facilities, clinics, and medical tourism centers to optimize their operations, ensuring flexibility, safety, and improved reimbursement levels for physicians, surgeons, nurses, and patients alike. The IT infrastructure required to support these solutions is becoming increasingly essential for delivering effective and efficient healthcare services.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The advantages of clinical workflow solutions in enhancing patient care and safety is the key driver of the market. Clinical workflow solutions play a pivotal role in streamlining healthcare processes, improving patient experiences, and enhancing safety in hospitals and ambulatory care centers. With the increasing patient volume and complexity of Electronic Health Records (EHRs), clinical workflow solutions have gained significant importance. These solutions facilitate real-time data exchange, enabling healthcare providers to make informed decisions, coordinate care, and ensure seamless communication. Interoperability issues, such as data silos and interface challenges, are addressed through clinical workflow solutions, allowing for the integration of health information exchanges, telehealth, remote patient monitoring, and EMR systems. IT professionals rely on data integration and workflow automation solutions to optimize clinical processes, reduce healthcare costs, and promote care collaboration.

Further, real-time communication solutions enhance care coordination and ensure efficient patient care. Overall, clinical workflow solutions contribute to improved patient outcomes, increased safety, and better care coordination. Their adoption is expected to increase during the forecast period, as healthcare organizations continue to seek innovative ways to enhance care quality and patient satisfaction.

Market Trends

Growing telehealth and remote patient monitoring (RPM) is the upcoming trend in the market. Clinical workflow solutions have gained significant traction in the healthcare industry due to the increasing patient volume and the need to optimize healthcare costs. IT advancements have led to the availability of various tools such as EHRs, high-speed internet networks, mobile devices, and telehealth technologies. These innovations have enabled remote patient monitoring (RPM) and telehealth services, allowing patients to monitor their vital signs at home and transmit the data to healthcare providers in real-time.

Moreover, this trend has created a demand for clinical workflow solutions that offer data integration, workflow automation, care collaboration, and real-time communication capabilities. Hospitals and ambulatory care centers are increasingly adopting interfaces, health information exchanges, and EMR integration solutions to streamline their clinical workflows and improve patient care. The integration of these technologies has led to more efficient and cost-effective healthcare delivery, addressing interoperability issues and enhancing overall patient outcomes.

Market Challenge

Interoperability and security issues related to clinical workflow solutions is a key challenges affecting the market growth. Clinical workflow solutions play a crucial role in managing patient data and streamlining processes in healthcare facilities. Hospitals utilize these solutions to import and export data from various internal and external sources, such as Electronic Health Records (EHRs), laboratories, admit/discharge/transfer, medical devices, and outside laboratories. While a single hospital may require a few dozen interfaces, large health systems with multiple sites may need to manage hundreds or even thousands of interfaces. Health information exchanges, implemented to address interoperability issues, pose challenges for hospitals. Financial burdens and technological complexities in designing and operating these exchanges can hinder the expansion of the market.

Additionally, telehealth, remote patient monitoring, and care collaboration are driving the demand for advanced workflow automation, data integration, and real-time communication solutions. IT professionals are essential in implementing these systems, ensuring EMR integration, and addressing the intricacies of interfaces and health information exchanges.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Athenahealth Inc. - The company offers clinical workflow solutions such as electronic health records, patient management, population health, telehealth, platform services, market place program and advisoy services.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ascom Holding AG

- Baxter International Inc.

- Change Healthcare Inc.

- Cisco Systems Inc.

- Constellation Software Inc.

- Cybage Software Pvt. Ltd.

- Epic Systems Corp.

- General Electric Co.

- Getinge AB

- Koch Industries Inc.

- Koninklijke Philips N.V.

- McKesson Corp.

- NextGen Healthcare Inc.

- Oracle Corp.

- Spok Holdings Inc.

- Stanley Black and Decker Inc.

- Stryker Corp.

- TeleGroup

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Clinical workflow solutions are IT infrastructure offerings designed to optimize patient care and improve operational efficiency in healthcare facilities. These solutions address the challenges of managing increasing patient volume, interoperability issues, and healthcare costs in hospitals, ambulatory care centers, long-term care facilities, and other healthcare institutions. They integrate with Electronic Health Records (EHRs) and Health Information Exchanges (HIEs) to facilitate data exchange and care collaboration. Telehealth, remote patient monitoring, and real-time communication solutions enable flexible care delivery, especially for chronic disease management and geriatric populations. IT professionals employ data integration and workflow automation solutions to streamline processes, ensuring quality healthcare for patients with conditions like cancer, diabetes, end-stage renal disease, and other illnesses and infections.

In addition, these solutions cater to various healthcare providers, including physicians, surgeons, nurses, and residents' relatives. They offer enterprise reporting, analytics, and unified communications solutions to help manage and analyze medical data, enabling value-based services and economic integration. Care management and delivery solutions, such as rounding solutions, specimen collection solutions, and medication administration solutions, contribute to safety, care, and reimbursement levels. Clinical workflow solutions facilitate care collaboration and communication between healthcare providers, ensuring care gap closure and effective visit planning, call scheduling, and patient admissions. Predictive analytics and cutting-edge clinical research further enhance patient care, enabling personalized treatment plans and improving patient journey insights.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

146 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 13.63% |

|

Market Growth 2024-2028 |

USD 9.37 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

12.14 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 45% |

|

Key countries |

US, Germany, UK, Canada, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Ascom Holding AG, athenahealth Inc., Baxter International Inc., Change Healthcare Inc., Cisco Systems Inc., Constellation Software Inc., Cybage Software Pvt. Ltd., Epic Systems Corp., General Electric Co., Getinge AB, Koch Industries Inc., Koninklijke Philips N.V., McKesson Corp., NextGen Healthcare Inc., Oracle Corp., Spok Holdings Inc., Stanley Black and Decker Inc., Stryker Corp., and TeleGroup |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -