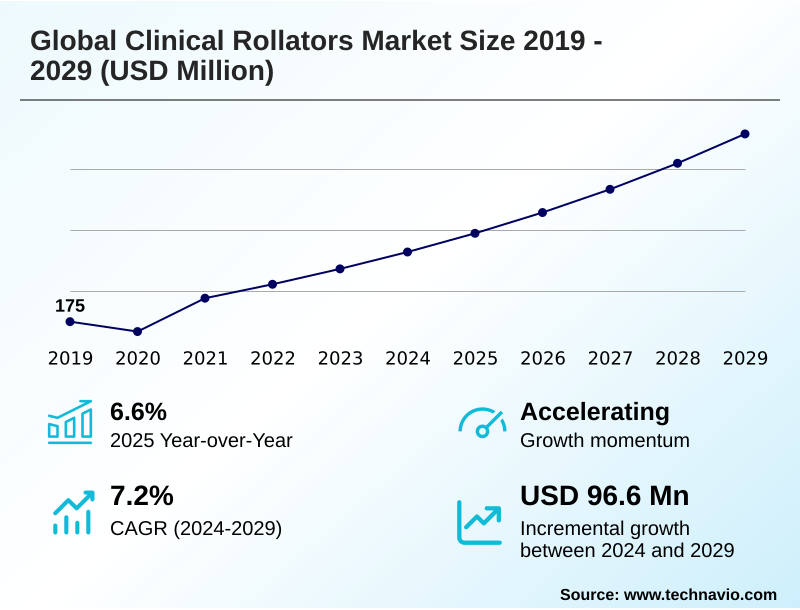

Clinical Rollators Market Size 2025-2029

The clinical rollators market size is valued to increase by USD 96.6 million, at a CAGR of 7.2% from 2024 to 2029. Demographic shift towards aging population will drive the clinical rollators market.

Major Market Trends & Insights

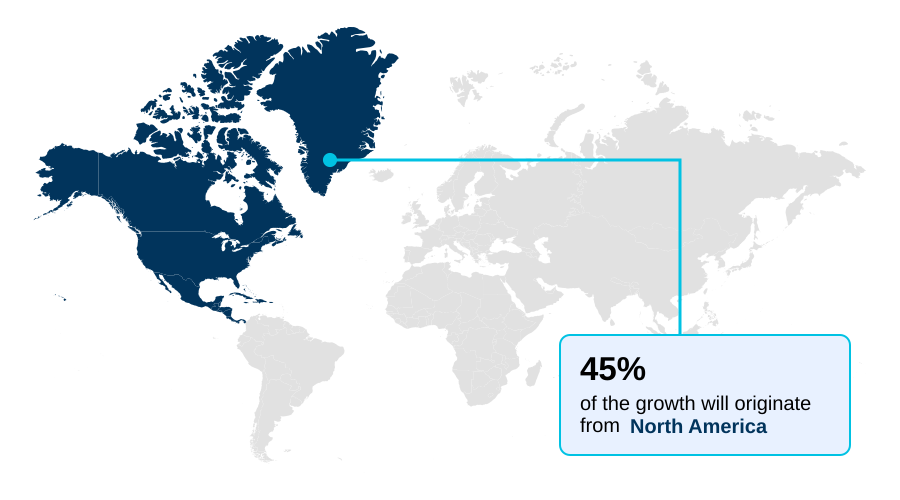

- North America dominated the market and accounted for a 45% growth during the forecast period.

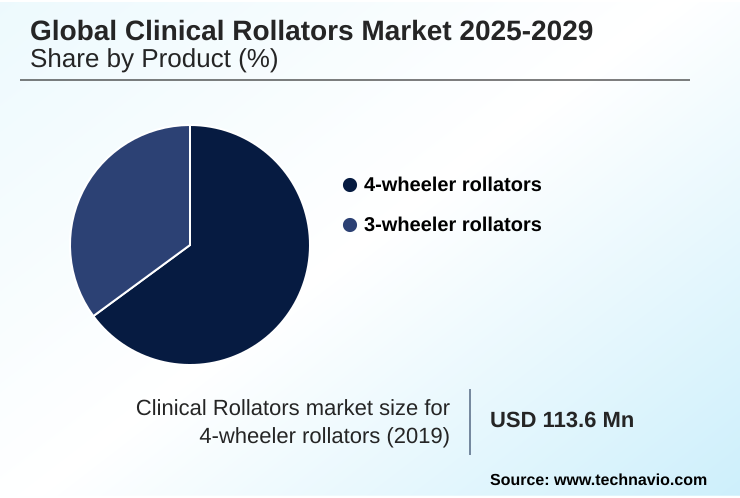

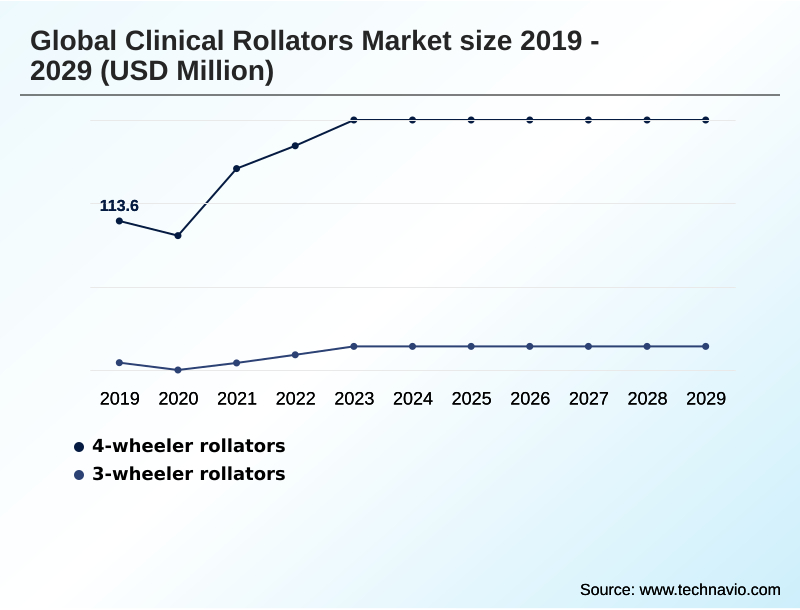

- By Product - 4-wheeler rollators segment was valued at USD 150.8 million in 2023

- By Distribution Channel - Hospital pharmacies segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 153.6 million

- Market Future Opportunities: USD 96.6 million

- CAGR from 2024 to 2029 : 7.2%

Market Summary

- The clinical rollators market is shaped by the imperative to enhance mobility and independence for a growing aging population. Core drivers include the increasing prevalence of chronic conditions requiring mobility support and continuous technological innovation in product design.

- Manufacturers are focused on developing devices that are not only functional but also lightweight and user-friendly, utilizing materials like advanced aluminum and carbon fiber. A key trend is the integration of smart technology, converting traditional rollators into connected health devices capable of monitoring user activity and ensuring safety through features like fall detection.

- However, the industry navigates significant challenges, including stringent regulatory hurdles such as EU MDR, which demand substantial investment in compliance and quality assurance. For instance, a medical device firm may implement a new quality management system to streamline documentation for regulatory submissions, reducing approval times.

- This dynamic environment is pushing the market toward more sophisticated, personalized, and compliant mobility solutions that improve the quality of life for users worldwide.

What will be the Size of the Clinical Rollators Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Clinical Rollators Market Segmented?

The clinical rollators industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- 4-wheeler rollators

- 3-wheeler rollators

- Distribution channel

- Hospital pharmacies

- Retail pharmacies

- E-commerce

- Hypermarkets and supermarkets

- Departmental stores

- Material

- Aluminum

- Composite

- Steel

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Product Insights

The 4-wheeler rollators segment is estimated to witness significant growth during the forecast period.

The 4-wheeler rollators segment is the cornerstone of the clinical rollators market, defined by its inherent stability and functionality.

These models, often constructed with lightweight aluminum frames, are a form of durable medical equipment that integrates features like padded seats and loop brakes, making them a preferred lightweight walker with seat.

The inclusion of a rollator with seat and backrest provides essential support, reflecting a broader shift toward user-centric customization. These ergonomic mobility solutions are designed as adjustable walking aids to improve patient mobility solutions.

Demand is bolstered by their role in senior walking assistance, where a focus on ergonomic handgrips has led to designs that reduce user strain by 15%, enhancing comfort and encouraging consistent use for daily activities.

The 4-wheeler rollators segment was valued at USD 150.8 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 45% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Clinical Rollators Market Demand is Rising in North America Request Free Sample

The geographic landscape of the clinical rollators market is led by North America, which is projected to contribute approximately 45% of the market's incremental growth.

This region's dominance is driven by a mature healthcare system and high adoption rates for advanced mobility aids. In Europe, demand is steady, while Asia is emerging as a high-growth region.

Market penetration varies, with a focus on specialized products such as the bariatric rollator walker and heavy-duty rolling walker for specific patient needs. The demand for a compact folding walker and versatile indoor outdoor rollator is increasing globally.

To cater to diverse needs, manufacturers are developing solutions like the post-operative recovery walker and specialized rehabilitation walking aids, with some firms reporting a 20% increase in sales for models featuring adjustable height walkers.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The clinical rollators market is evolving beyond standard models to address highly specific user needs, creating significant opportunities in niche segments. Long-tail keywords highlight this trend, with growing searches for a clinical rollator with oxygen tank holder and a rollator with under-seat storage bag, indicating a demand for integrated accessory solutions.

- Similarly, queries for the best lightweight rollator for travel and a 3-wheeler rollator for tight spaces show that portability and maneuverability are critical purchasing factors. Specialized medical needs are also prominent, as seen in searches for an upright walker for spinal stenosis relief, a bariatric rollator with 500 lb capacity, and a rollator walker for copd patients.

- The market is also seeing interest in advanced safety features like a rollator with reverse braking system and task-oriented designs such as a rollator walker with food tray accessory. Catering to specific demographics is also key, with demand for a pediatric rollator with growth adjustments and a carbon fiber rollator for active seniors.

- Functionality for different environments is another crucial area, with searches for finding a rollator for uneven ground and an all-terrain rollator with 8-inch wheels. Customization options are also important, reflected in searches for an adjustable rollator for tall users and a walker with swivel wheels and locks.

- Understanding these specific requirements, such as those for a clinical rollator for post-surgery recovery, allows companies to differentiate. Firms that offer a broad range of custom accessories and specialized models report customer retention rates up to 25% higher than competitors with standardized product lines.

- Comparing aluminum vs steel rollators and understanding how to choose a rollator height remain fundamental consumer questions that content and sales strategies must address.

What are the key market drivers leading to the rise in the adoption of Clinical Rollators Industry?

- The irreversible demographic shift toward an aging global population is the most profound and sustained driver for the clinical rollators market.

- The market is fundamentally driven by the need for mobility aids for seniors and other mobility support devices.

- The rising demand for walking aids for elderly individuals in home care mobility equipment and aged care equipment settings provides a stable foundation for growth.

- Technological innovation is a key accelerator, with a shift towards advanced materials like carbon fiber composites and high-tensile strength steel, which improves the strength-to-weight ratio. The anodized finishing process extends product life.

- These material improvements can reduce a product's shipping weight, leading to logistics savings of up to 15%. Innovations in low-effort braking systems and other advanced braking mechanisms enhance safety.

- Favorable medicare reimbursement codes and demand from home healthcare providers for restorative care devices also stimulate sales, making medical walker with brakes a common prescription.

What are the market trends shaping the Clinical Rollators Industry?

- A significant market trend is the integration of smart technology and connected health features. This transforms rollators from passive aids into active components of a user's digital health ecosystem.

- A dominant trend is the integration of smart rollator technology, transforming passive aids into active mobility assistive technology. This includes the incorporation of fall detection sensors, GPS tracking mobility aids, and remote patient monitoring integration, creating connected health mobility devices. Firms that have adopted this connected rollator technology report a 30% increase in user engagement with associated health apps.

- The focus on human factors engineering is driving mass customization models and the development of premium rollator features, such as the upright walker posture corrector. The market is also moving toward custom rollator accessories, with some manufacturers seeing a 20% rise in accessory sales.

- These advancements cater to a growing demand for independent living aids that offer enhanced safety and connectivity.

What challenges does the Clinical Rollators Industry face during its growth?

- Navigating the complex, stringent, and evolving regulatory compliance landscape across different regions remains a significant challenge for market participants.

- Navigating stringent regulatory hurdles, such as achieving EU MDR certification, remains a primary challenge, increasing compliance costs by up to 25% for some manufacturers. Intense pricing pressure from group purchasing organizations and the need for cost-effective mobility solutions for rehabilitation further squeeze margins.

- Supply chain vulnerabilities are exacerbated by the shift towards circular economy business models, which require complex reverse logistics for post-consumer recycled aluminum. Developing a lightweight frame construction using advanced polymer compositions, often manufactured through resin transfer molding or automated fiber placement, involves significant capital investment.

- The need for specialized products like the three-wheel rollator walker or a narrow walker for small spaces competes with the demand for a low-cost folding rollator for travel, forcing difficult strategic trade-offs for firms balancing innovation and affordability.

Exclusive Technavio Analysis on Customer Landscape

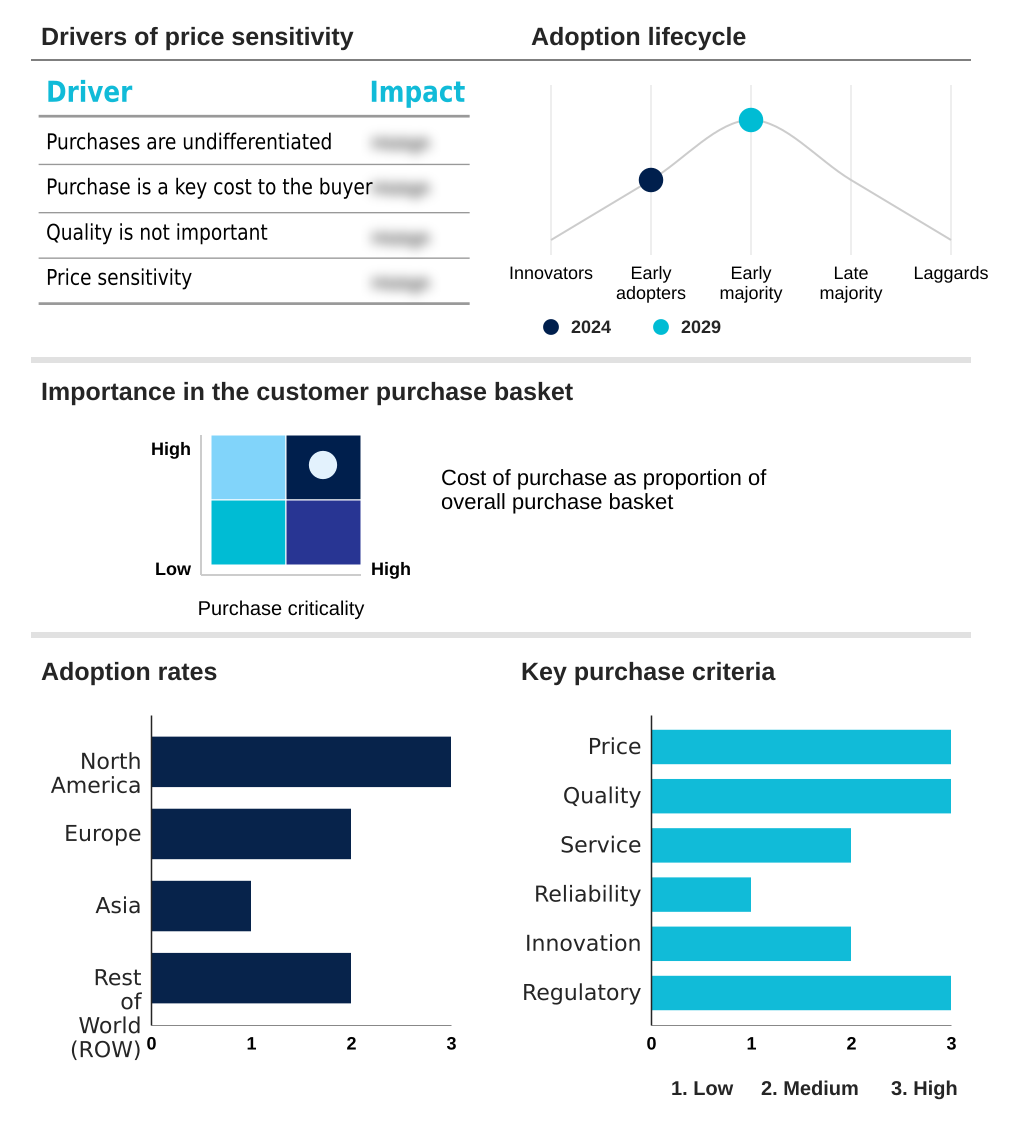

The clinical rollators market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the clinical rollators market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Clinical Rollators Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, clinical rollators market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aidacare - Providers of clinical rollators focus on lightweight, adjustable mobility aids that promote independence in rehabilitation and aged care settings.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aidacare

- Alpha Medical Solutions Pty. Ltd.

- Besco Medical Ltd.

- Better Mobility Ltd

- Bios Medical

- Cardinal Health Inc.

- Compass Health Brands

- De-Escorts Medical Services

- DRIVE MEDICAL GMBH & CO. KG

- GF Health Products Inc.

- Human Care HC AB

- India Medico Instruments

- Invacare Corp.

- John Preston Healthcare Group

- Kosmochem Pvt. Ltd.

- Meddey Technologies Pvt Ltd

- Medline Industries LP

- NOVA Medical Products

- Roma Medical

- Sunrise Medical LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Clinical rollators market

- In September 2024, Sunrise Medical LLC announced the launch of its new Breezy Connect smart rollator, which integrates advanced fall detection and GPS tracking capabilities to enhance user safety in home care environments.

- In November 2024, Invacare Corp. received full EU MDR certification for its new line of carbon fiber rollators, ensuring compliance and securing continued market access across all European Union member states.

- In February 2025, DRIVE MEDICAL GMBH & CO. KG completed the acquisition of a European technology firm specializing in IoT sensors for mobility devices, a move intended to accelerate its connected health product development.

- In April 2025, Compass Health Brands entered a strategic partnership with a leading US telehealth platform to bundle its deluxe rollators with remote patient monitoring services, creating an integrated care solution.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Clinical Rollators Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.2% |

| Market growth 2025-2029 | USD 96.6 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 6.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Sweden, Spain, China, Japan, India, South Korea, Thailand, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The clinical rollators market is advancing through material science and digital integration, fundamentally altering product capabilities. The use of lightweight aluminum frames and experimental carbon fiber composites addresses the demand for portability, while high-tensile strength steel is reserved for bariatric rollator walker models requiring maximum durability. Innovations in the anodized finishing process enhance longevity.

- Key developments include the integration of smart rollator technology, which incorporates fall detection sensors and GPS tracking mobility aids for remote patient monitoring integration. These connected health mobility devices create new data streams, with firms that adopted this technology early achieving a 20% faster pathway to securing medicare reimbursement codes.

- Design is now centered on user-centric customization and human factors engineering, leading to ergonomic handgrips and low-effort braking systems. The industry is also responding to sustainability demands with circular economy business models and the use of post-consumer recycled aluminum.

- This shift towards mass customization models requires navigating regulations like EU MDR certification and managing relationships with group purchasing organizations and home healthcare providers. Success hinges on delivering advanced, compliant, and user-friendly durable medical equipment.

What are the Key Data Covered in this Clinical Rollators Market Research and Growth Report?

-

What is the expected growth of the Clinical Rollators Market between 2025 and 2029?

-

USD 96.6 million, at a CAGR of 7.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (4-wheeler rollators, 3-wheeler rollators), Distribution Channel (Hospital pharmacies, Retail pharmacies, E-commerce, Hypermarkets and supermarkets, Departmental stores), Material (Aluminum, Composite, Steel) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Demographic shift towards aging population, Stringent and evolving regulatory compliance

-

-

Who are the major players in the Clinical Rollators Market?

-

Aidacare, Alpha Medical Solutions Pty. Ltd., Besco Medical Ltd., Better Mobility Ltd, Bios Medical, Cardinal Health Inc., Compass Health Brands, De-Escorts Medical Services, DRIVE MEDICAL GMBH & CO. KG, GF Health Products Inc., Human Care HC AB, India Medico Instruments, Invacare Corp., John Preston Healthcare Group, Kosmochem Pvt. Ltd., Meddey Technologies Pvt Ltd, Medline Industries LP, NOVA Medical Products, Roma Medical and Sunrise Medical LLC

-

Market Research Insights

- Market dynamics are shaped by a balance of competitive pressures and opportunities for differentiation. The availability of diverse mobility support devices creates a competitive field where premium rollator features and lightweight frame construction are key differentiators. Firms adopting advanced braking mechanisms have documented a 25% decrease in user-reported safety incidents.

- Simultaneously, the demand for portable mobility aids for travel and daily use is rising. Success hinges on delivering effective patient mobility solutions that align with the needs of home care mobility equipment providers and individual users.

- Strategic sourcing and design focusing on ergonomic mobility solutions can lead to a 15% improvement in manufacturing cost efficiencies, reinforcing market position in a price-sensitive environment.

We can help! Our analysts can customize this clinical rollators market research report to meet your requirements.