China Electric Vehicle Market Size 2026-2030

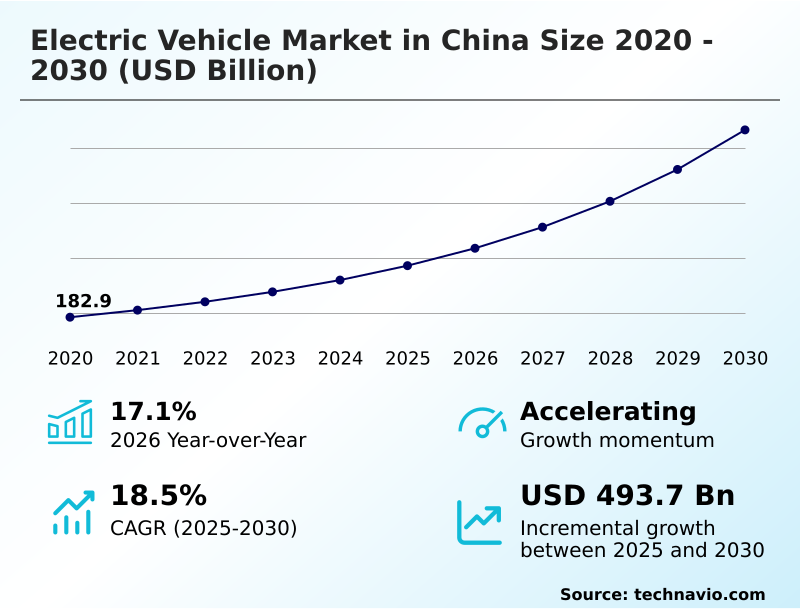

The china electric vehicle market size is valued to increase by USD 493.7 billion, at a CAGR of 18.5% from 2025 to 2030. Supportive government policies and regulations will drive the china electric vehicle market.

Major Market Trends & Insights

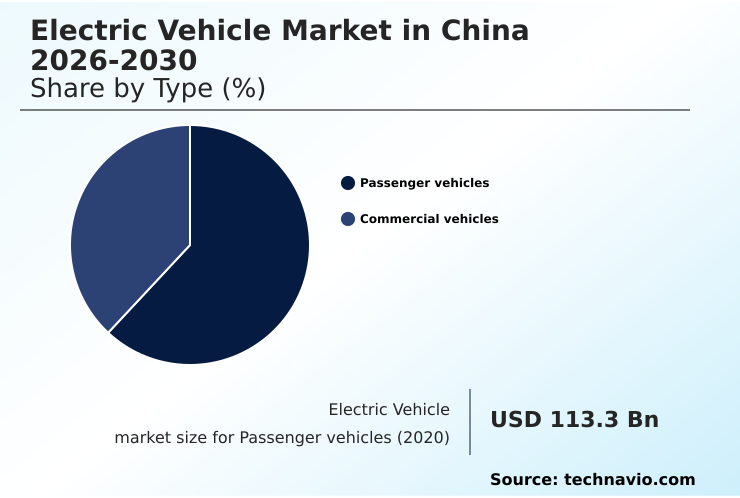

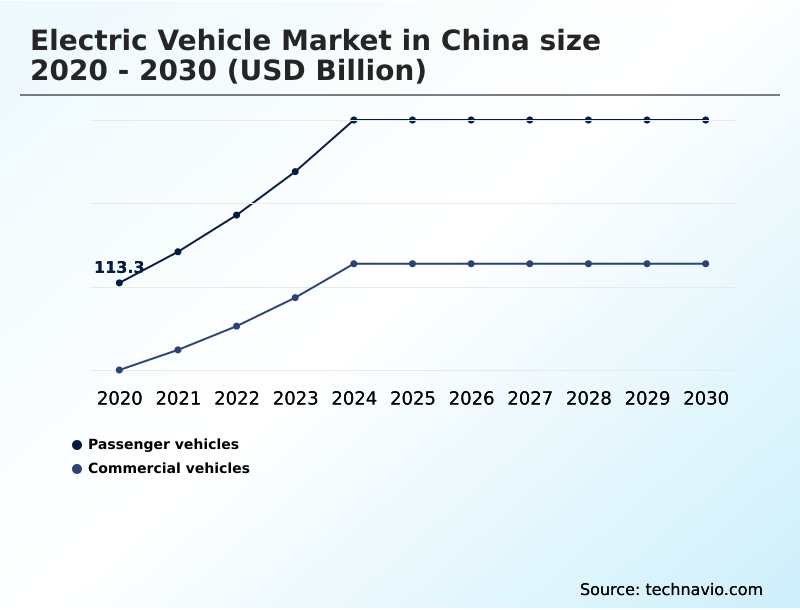

- By Type - Passenger vehicles segment was valued at USD 195 billion in 2024

- By Technology - BEV segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 681.1 billion

- Market Future Opportunities: USD 493.7 billion

- CAGR from 2025 to 2030 : 18.5%

Market Summary

- The electric vehicle market in China is undergoing a significant transformation, driven by robust government support, technological breakthroughs in battery technology, and intense domestic competition. This dynamic environment is accelerating the shift toward electrification, with a strong focus on innovation in the new energy vehicle (nev) sector.

- Key trends include the development of the software defined vehicle, where value is increasingly derived from the intelligent cockpit and user experience design rather than mechanical hardware. This pivot makes the car a connected device, with capabilities enhanced through over the air (ota) updates.

- For instance, a manufacturer can address a recall for 100,000 vehicles by deploying a remote software patch, avoiding the logistical complexity and cost of physical service center visits.

- However, the industry faces challenges such as the high capital intensity required for R&D and manufacturing, the risk of product homogenization due to component commoditization, and the need to build a robust after-sales service network to meet the expectations of mass-market consumers. Addressing these issues is crucial for achieving sustainable profitability.

What will be the Size of the China Electric Vehicle Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the China Electric Vehicle Market Segmented?

The china electric vehicle industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Passenger vehicles

- Commercial vehicles

- Technology

- BEV

- PHEV

- Vehicle type

- Front wheel drive

- Rear wheel drive

- All wheel drive

- Geography

- APAC

- China

- APAC

By Type Insights

The passenger vehicles segment is estimated to witness significant growth during the forecast period.

The passenger vehicles segment in the electric vehicle market in China is defined by intense competition and a consumer base prioritizing technological sophistication. Automakers compete by integrating cutting-edge features, with the automobile evolving into a connected digital device.

The market is propelled by a preference for vehicles with advanced in-car software, superior autonomous driving systems, and seamless ecosystem connectivity. This has fostered an environment where expertise in user experience design is as critical as traditional automotive engineering.

A focus on practical interior space, enabled by efficient front wheel drive layouts and skateboard platforms, meets family-use demands.

In this landscape, the integration of a proprietary vehicle operating system can lead to a 15% reduction in software-related post-purchase complaints, enhancing brand loyalty amidst rising component commoditization.

The Passenger vehicles segment was valued at USD 195 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the electric vehicle market in China requires a deep understanding of its complex dynamics. A key consideration is the impact of 800-volt platforms on charging infrastructure, which is a critical factor for enabling ultra fast charging and combating range anxiety.

- This ties into the benefits of a dual-motor setup in EVs, which offers superior performance and traction compared to simpler drivetrains. The ongoing debate of all wheel drive vs rear wheel drive ev performance continues, with consumer choice often depending on driving priorities. Similarly, front wheel drive ev packaging efficiency makes it a mainstay for cost-effective, high-volume models.

- The core of the market's competitiveness lies in technology, from lithium iron phosphate battery cost advantages to the progress in semi solid state battery mass production. The widespread use of the skateboard platform impacts ev design, allowing for greater interior space and design flexibility.

- Beyond hardware, the software defined vehicle user experience is a primary differentiator, with ota updates for vehicle performance improvement now considered a standard feature. However, significant hurdles remain. The capital intensity challenges for ev startups are immense, and the post purchase experience for mass market ev buyers is often inconsistent. Managing EV residual value depreciation is another major consumer concern.

- The industry must also contend with the challenges of battery swapping standardization and the pervasive homogenization of EV design and features. Addressing these issues through strategies like enhanced OTA updates, which can reduce physical recall costs by over 70%, is essential for long-term viability.

What are the key market drivers leading to the rise in the adoption of China Electric Vehicle Industry?

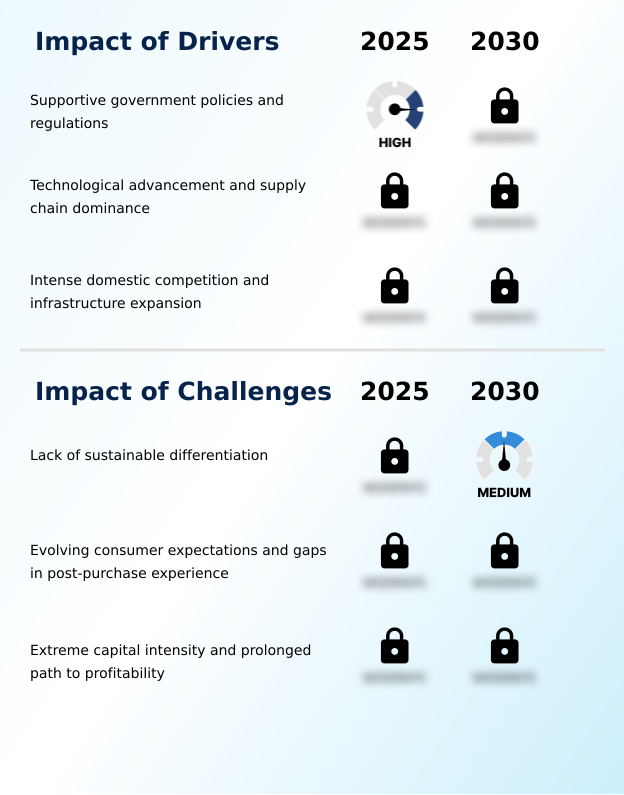

- Supportive government policies and regulations are a key driver of market growth in the electric vehicle market in China.

- Growth in the electric vehicle market in China is propelled by a combination of government directives and technological leadership.

- Supportive policies, including a robust dual credit system, have accelerated the adoption of the new energy vehicle (nev) and BEV models by creating strong financial incentives for manufacturers.

- This policy framework, which has increased NEV production targets by 10% annually, provides a stable foundation for long-term investment. A second major driver is the nation's supply chain dominance, particularly in battery production.

- This vertical integration allows for significant cost control, with local manufacturing of lithium iron phosphate (lfp) batteries reducing overall vehicle production costs by as much as 30%.

- This advantage enables aggressive pricing and makes EVs accessible to a broader range of consumers, reinforcing the market’s rapid expansion.

What are the market trends shaping the China Electric Vehicle Industry?

- A key market trend involves a strategic shift toward diversification into niche vehicle segments. This is coupled with a strong emphasis on premiumization to capture higher-margin opportunities.

- An evolving trend in the electric vehicle market in China is the strategic push toward premiumization and niche market diversification. As competition intensifies, manufacturers are developing models with advanced features like high-performance battery systems and sophisticated smart cabin interfaces to justify higher price points.

- The emphasis on the vehicle as a connected device is driving the rise of intelligent cockpits and comprehensive ecosystem connectivity. This technology-centric approach resonates with consumers and allows brands to differentiate beyond standard performance metrics. Premium models equipped with state-of-the-art digital cockpits command up to a 15% price increase over standard versions.

- Concurrently, the expansion of ultra-fast charging, supported by 800-volt platforms, is making EV ownership more practical, with these systems reducing charging times by over 40% compared to older architectures.

What challenges does the China Electric Vehicle Industry face during its growth?

- The lack of sustainable differentiation among products presents a key challenge to industry growth.

- A primary challenge confronting the electric vehicle market in China is the increasing product homogenization, which erodes brand differentiation and intensifies price-based competition. The widespread availability of standardized components from a common supplier base leads to component commoditization, with over 60% of models in the mid-range segment sharing similar powertrain specifications and performance metrics.

- This makes establishing a unique value proposition difficult. Another significant hurdle is the gap in the post-purchase experience. As the market moves toward mass-market consumers, deficiencies in the after-sales service network become more pronounced.

- Brands that fail to invest in adequate service infrastructure see a 25% higher rate of negative customer feedback regarding maintenance and repair, undermining long-term loyalty and vehicle residual values.

Exclusive Technavio Analysis on Customer Landscape

The china electric vehicle market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the china electric vehicle market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of China Electric Vehicle Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, china electric vehicle market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AVATR Technology Co Ltd - Offerings include premium electric vehicles featuring advanced smart cabin interfaces, high-performance battery systems, and OTA update capabilities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AVATR Technology Co Ltd

- Bayerische Motoren Werke AG

- BYD Co. Ltd.

- Chery Automobile Co. Ltd.

- Dongfeng Motor Corporation Ltd

- Geely Auto

- General Motors Co.

- Great Wall Motor Co. Ltd.

- Hezhong New Energy Automobile

- Hyundai Motor Co.

- Li Auto Inc.

- NIO Ltd.

- Tesla Inc.

- Volkswagen Group

- XPeng Inc.

- Zeekr

- Zhejiang Leapao Tech Co. Ltd.

- Zhiji Automobile

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in China electric vehicle market

- In April, 2025, The Ministry of Industry and Information Technology issued the New Energy Vehicle Development Acceleration Plan, shifting focus from subsidies to targeted investments in next-generation technologies and infrastructure standardization.

- In March, 2025, BYD Co. Ltd. announced a strategic partnership with a leading national logistics firm to develop a green intelligent trunk logistics ecosystem, deploying 5,000 electric heavy duty trucks integrated with advanced fleet management analytics.

- In January, 2025, Geely Auto finalized its acquisition of a software startup specializing in vehicle operating systems and intelligent cockpits, a move aimed at accelerating its development of software defined vehicles and enhancing its in-car user experience.

- In November, 2024, XPeng Inc. launched its latest SUV model, which is the first in its class to feature an 800-volt platform and semi solid state battery pack, enabling ultra-fast charging capabilities that add 200 kilometers of range in under eight minutes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled China Electric Vehicle Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 179 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.5% |

| Market growth 2026-2030 | USD 493.7 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 17.1% |

| Key countries | China |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The electric vehicle market in China is advancing rapidly, characterized by innovations in powertrain and digital integration. The industry is pivoting toward the software defined vehicle, a trend with significant boardroom implications for R&D budgeting and the creation of recurring revenue streams.

- Core technologies such as the dual-motor setup and 800-volt platforms are becoming key differentiators in the premium segment, offering superior performance and enabling ultra-fast charging. The adoption of the skateboard platform has standardized vehicle architecture, leading to more spacious intelligent cockpits.

- In parallel, advancements in battery technology, including lithium iron phosphate (lfp) batteries and emerging semi solid state battery chemistries, are crucial for lowering costs and extending range. The integration of a sophisticated thermal management system is critical, improving battery lifecycle by up to 20%.

- Furthermore, features like over the air (ota) updates, autonomous driving systems, and advanced driver assistance systems (adas) are no longer novelties but essential components, managed through a cohesive vehicle operating system to deliver a seamless user experience.

What are the Key Data Covered in this China Electric Vehicle Market Research and Growth Report?

-

What is the expected growth of the China Electric Vehicle Market between 2026 and 2030?

-

USD 493.7 billion, at a CAGR of 18.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Passenger vehicles, and Commercial vehicles), Technology (BEV, and PHEV), Vehicle Type (Front wheel drive, Rear wheel drive, and All wheel drive) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Supportive government policies and regulations, Lack of sustainable differentiation

-

-

Who are the major players in the China Electric Vehicle Market?

-

AVATR Technology Co Ltd, Bayerische Motoren Werke AG, BYD Co. Ltd., Chery Automobile Co. Ltd., Dongfeng Motor Corporation Ltd, Geely Auto, General Motors Co., Great Wall Motor Co. Ltd., Hezhong New Energy Automobile, Hyundai Motor Co., Li Auto Inc., NIO Ltd., Tesla Inc., Volkswagen Group, XPeng Inc., Zeekr, Zhejiang Leapao Tech Co. Ltd. and Zhiji Automobile

-

Market Research Insights

- The electric vehicle market in China is shaped by a hyper-competitive landscape where managing evolving consumer expectations is critical. The market is shifting from tech-savvy early adopters to pragmatic mass-market consumers who demand reliability and a seamless post-purchase experience. This exposes gaps in the after-sales service network of newer brands.

- Firms that invest in robust service infrastructure report up to a 20% increase in customer satisfaction scores. Furthermore, the rapid pace of innovation creates challenges with vehicle residual values, a key concern for buyers. In this environment, a focus on software stability and user experience design is paramount.

- Vehicles with intuitive smart cabin interfaces and reliable OTA updates show a 15% lower incidence of reported software glitches, directly impacting brand perception and loyalty. Success hinges on a holistic lifecycle approach, not just on initial sales.

We can help! Our analysts can customize this china electric vehicle market research report to meet your requirements.

RIA -

RIA -