Carrier Screening Market Size 2025-2029

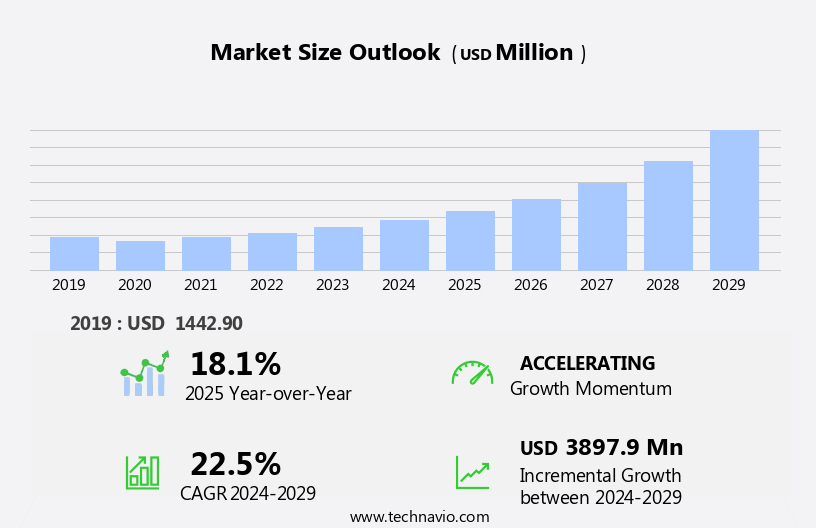

The carrier screening market size is forecast to increase by USD 3.9 billion at a CAGR of 22.5% between 2024 and 2029.

- The market is witnessing significant growth, driven by the increasing prevalence of genetic diseases and disorders. This trend is further fueled by the rising adoption of next-generation sequencing (NGS) technology in carrier screening. NGS technology enables the simultaneous analysis of multiple genes, increasing the efficiency and accuracy of carrier screening. Dominant and recessive genes, biochemical markers, and chromosomal microarray analysis are integral to diagnostic testing. However, the market's dynamics are influenced by varying regulations on carrier screening and research globally. These regulatory differences create challenges for market players, requiring them to navigate complex legal frameworks and adapt to diverse regulatory requirements.

- Additionally, investing in research and development to improve the accuracy and affordability of carrier screening solutions could provide a competitive edge. Data security is a significant concern, with strict protocols in place to protect patient information. Overall, the market presents significant growth potential, with the integration of advanced technologies and a growing focus on early disease detection offering new opportunities for innovation. Companies seeking to capitalize on market opportunities must stay informed of these regulatory developments and develop strategies to address the associated complexities.

What will be the Size of the Carrier Screening Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

Genetic disease prevention through carrier screening is gaining momentum, fueled by the adoption of next-generation sequencing (NGS) and targeted sequencing. Variant interpretation and risk modeling are essential components of this process, which are increasingly relying on artificial intelligence (AI) and machine learning (ML) to improve accuracy and efficiency. Access to care and preconception counseling are key challenges in the market. Healthcare IT and mHealth are addressing these issues by streamlining data management and improving access to clinical decision support.

Quality control and quality assurance are paramount in this context, ensuring the reliability of test results and maintaining public health standards. Clinical trials and professional development are crucial for advancing the field of carrier screening. Reimbursement policies and healthcare equity are also significant factors influencing market trends. Predictive analytics and precision medicine are transforming the landscape by enabling personalized approaches to care, while public health initiatives aim to ensure equal access to these services. In summary, the market is undergoing rapid transformation, driven by advances in technology, a growing focus on personalized medicine, and efforts to improve access to care. These trends are shaping the future of reproductive health and genetic disease prevention.

How is this Carrier Screening Industry segmented?

The carrier screening industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Expanded

- Targeted disease

- Technology

- DNA sequencing

- Polymerase chain reaction (PCR)

- Microarrays

- Others

- Test

- Molecular screening tests

- Biochemical screening tests

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- Spain

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

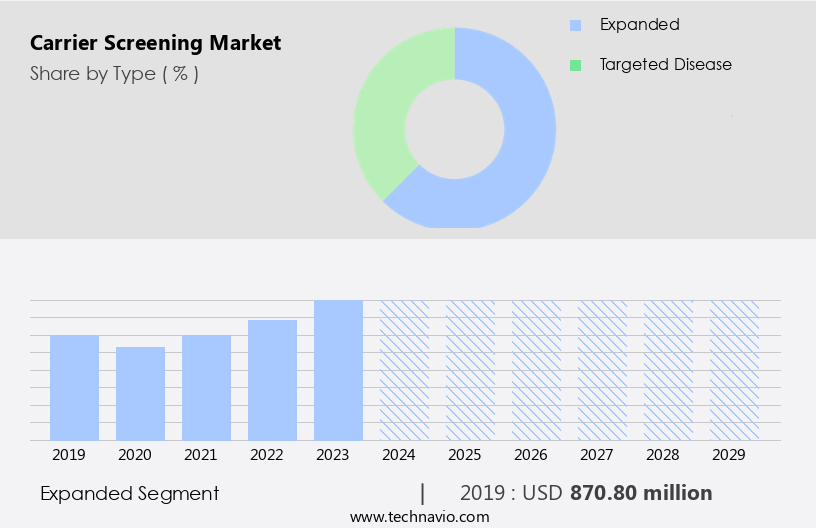

By Type Insights

The expanded segment is estimated to witness significant growth during the forecast period. Prenatal carrier screening has evolved to encompass a comprehensive array of tests for single-gene disorders, extending beyond traditional guidelines. This expansion enables simultaneous screening for multiple genetic conditions. The American College of Obstetricians and Gynecologists (ACOG) advises practitioners to include disorders that affect at least 1 in 100 people, significantly impact quality of life, impair cognitive or physical abilities, necessitate surgical or medical intervention during childhood, and have early onset. Carrier screening tests, including second-trimester and confirmatory testing, employ risk stratification and data analysis to identify carriers. Fetal anomaly screening, fetal growth restriction, and neural tube defects are also crucial components of prenatal screening.

Genetic counselors play a vital role in patient education, informed consent, and clinical interpretation. Conditions such as klinefelter syndrome, chromosomal abnormalities, Tay-Sachs disease, Down syndrome, and cystic fibrosis are among those screened for. Integrated screening, which combines maternal serum screening and ultrasound, is increasingly popular. First-trimester screening for Down syndrome, neural tube defects, and gestational diabetes is also available. Ethical considerations, including informed consent and genetic counseling, are paramount. The market, a critical segment of reproductive health, is experiencing significant advancements driven by the integration of reproductive technologies and precision medicine.

Conditions like Turner syndrome, sickle cell anemia, phenylketonuria (PKU), and Fragile X syndrome are also screened for. False positive and false negative rates are essential considerations in carrier screening. Healthcare providers play a crucial role in implementing these tests and providing appropriate follow-up care.

The Expanded segment was valued at USD 870.80 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

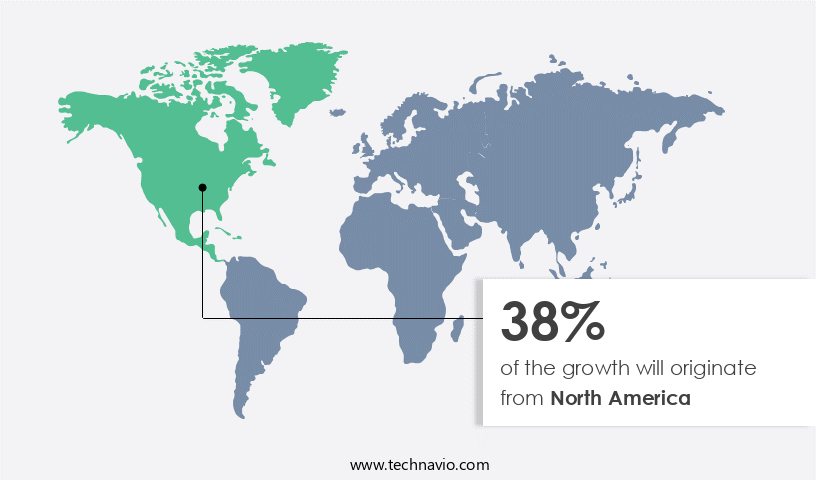

North America is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing significant growth, with the US leading the region due to increasing concerns for early disease diagnosis and a rise in commercial approvals for advanced carrier screening. The use of pharmacogenomic testing is also contributing to market expansion. Rising cases of birth defects, such as fetal growth restriction, neural tube defects, and congenital heart defects, have fueled the demand for prenatal testing and newborn screening. In this context, the Centers for Disease Control and Prevention (CDC) reports that approximately 5% of births in the US are affected by birth defects, and 3% of infants are born with genetic disorders.

Carrier screening tests, including those for chromosomal abnormalities like Klinefelter syndrome and Turner syndrome, single gene disorders like cystic fibrosis and sickle cell anemia, and recessive genes like Tay-Sachs disease and Fragile X syndrome, are essential in identifying potential risks and enabling early interventions. Patient education and informed consent are crucial components of the screening process, with genetic counselors playing a vital role in explaining test results and providing guidance. Data security and data analysis are also essential considerations in the market, as sensitive patient information must be protected. Integrated screening, which combines first-trimester and second-trimester screening, as well as sequential screening, fetal anomaly screening, and diagnostic testing, offers improved accuracy and reduces false positives and false negatives.

Ethical considerations are an ongoing concern in the market, with healthcare providers emphasizing the importance of clinical interpretation, positive and negative predictive values, and the implications of testing for families and future generations.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Carrier Screening market drivers leading to the rise in the adoption of Industry?

- The escalating incidence of genetic diseases and disorders serves as the primary catalyst for market growth. Carrier screening is experiencing growing demand in laboratories and hospitals due to the rising incidence of genetic disorders such as cystic fibrosis, Tay-Sachs disease, and sickle cell anemia. Prenatal carrier screening procedures are a significant contributor to this trend, as they enable early detection and treatment of manageable genetic conditions. According to the Centers for Disease Control and Prevention (CDC), approximately 1 in every 33 babies born in the US has a birth defect. The World Health Organization (WHO) estimates that around 8 million babies are born with a birth defect globally each year. Data analysis plays a crucial role in carrier screening, ensuring accurate results and reducing false positives and false negatives.

- Negative predictive value and false positive rate are essential metrics for diagnostic testing. Patient education is another essential aspect, as healthcare providers must communicate the benefits and limitations of carrier screening effectively. Data security is a critical concern in carrier screening, as sensitive patient information must be protected. Turner syndrome and Down syndrome are common genetic disorders that can be detected through carrier screening. Ensuring data security through robust cybersecurity measures and compliance with regulations such as HIPAA is essential. The increasing prevalence of genetic disorders, the benefits of prenatal testing, and the importance of data analysis, patient education, and data security are driving the demand for carrier screening in the healthcare industry.

What are the Carrier Screening market trends shaping the Industry?

- Next-generation sequencing (NGS) technology is experiencing a significant rise in carrier screening applications, marking a notable trend in the industry. This innovative approach to genetic testing is gaining increasing attention and adoption due to its improved accuracy and efficiency compared to traditional methods. The Human Genome Project and the emergence of next-generation sequencing (NGS) technologies have significantly advanced carrier screening in the medical field. NGS allows for large-scale sequencing of the human genome to identify mutations and gene variants linked to various diseases and disorders. This technological advancement has led to a reduction in the cost of sequencing and genomic analysis, making carrier screening more accessible. Fetal anomaly screening, including the detection of recessive genes associated with conditions such as cystic fibrosis and fragile X syndrome, is a primary application of carrier screening. First-trimester screening and chromosomal microarray analysis are other essential techniques used to identify potential genetic risks.

- Informed consent and genetic counselors play a crucial role in the carrier screening process, ensuring individuals fully understand the implications of the test results. NGS has transformed the market by providing a comprehensive understanding of genetic functionalities and structures. It enables the detection of intermediate to large-sized mutations and gene variants, contributing to the early identification and prevention of genetic disorders. With the emphasis on personalized medicine and the growing awareness of genetic conditions, the demand for carrier screening is expected to continue growing. Positive predictive value, a critical metric in carrier screening, is significantly influenced by the accuracy and comprehensiveness of the testing methods.

How does Carrier Screening market face challenges during its growth?

- The varying regulations on carrier screening and research, which are subject to significant global differences, pose a significant challenge to the industry's growth trajectory. The market is subject to varying regulatory standards and compliances worldwide, posing significant challenges for market participants. Carrier screening results significantly influence the diagnostic process for critical health conditions, making accuracy, safety, and reliability essential. Consequently, stringent and complex regulations have been imposed by regulatory authorities such as the US Food and Drug Administration (FDA), European Medicines Agency (EMA), European Agency for the Evaluation of Medicinal Products (EAEMP), Australia Therapeutic Goods Administration (ATGA), World Health Organization (WHO), International Organization for Standardization (ISO), and China Food and Drug Administration (CFDA).

- These regulations cover aspects like genetic testing, clinical interpretation, and genetic counseling for conditions like phenylketonuria (PKU) and sickle cell anemia. Biochemical markers play a crucial role in carrier screening, and their interpretation necessitates expertise to ensure correct diagnosis. Ethical considerations are also essential, as carrier screening can reveal information about dominant genes and potential health risks for future generations. DNA sequencing, a crucial component of NGS, plays a vital role in improving the positive predictive value by providing a more precise analysis of the genetic material. The integration of these advanced technologies in carrier screening is expected to lead to more accurate diagnoses and better health outcomes.

Exclusive Customer Landscape

The carrier screening market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the carrier screening market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, carrier screening market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The company specializes in advanced genetic testing, specifically carrier screening for aneuploidies in amniotic fluid samples.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Agilent Technologies Inc.

- CENTOGENE NV

- Danaher Corp.

- DiaSorin SpA

- Eurofins Scientific SE

- F. Hoffmann La Roche Ltd.

- Fulgent Genetics Inc.

- Gene By Gene Ltd

- Illumina Inc.

- Invitae Corp.

- Laboratory Corp. of America Holdings

- MedGenome Labs Ltd.

- Myriad Genetics Inc.

- Natera Inc.

- OPKO Health Inc.

- Otogenetics Corporation

- Quest Diagnostics Inc.

- Sema4 OpCo Inc.

- Thermo Fisher Scientific Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Carrier Screening Market

- In January 2024, Illumina, a leading genetics technology company, announced the launch of its new carrier screening solution, "Grail CarrierScreen NGS," which uses next-generation sequencing technology to detect genetic conditions with higher accuracy and efficiency (Illumina Press Release).

- In March 2024, Thermo Fisher Scientific and Invitrogen, two prominent players in the market, entered into a strategic partnership to integrate Invitrogen's carrier screening panels with Thermo Fisher's Ion Torrent Genomic Solutions. This collaboration aimed to enhance the efficiency and accessibility of carrier screening services (Thermo Fisher Scientific Press Release).

- In May 2025, Myriad Genetics, a major player in genetic testing, completed the acquisition of Counsyl, a leading carrier screening company, for approximately USD800 million. This acquisition expanded Myriad's carrier screening offerings and strengthened its position in the market (Myriad Genetics Press Release).

- In May 2025, the European Union's In Vitro Diagnostic Medical Devices Regulation (IVDR) came into effect, mandating stricter regulations for carrier screening tests. This regulatory change is expected to increase the demand for high-quality, reliable carrier screening solutions from approved manufacturers (European Commission Press Release).

Research Analyst Overview

Carrier screening tests, a subset of laboratory testing, continue to evolve in response to advancements in genetics and healthcare. These tests identify individuals who carry genes associated with various genetic disorders, including fetal anomalies, chromosomal abnormalities, and single gene disorders. Fetal anomaly screening, often performed during the second trimester, aims to detect structural defects, while recessive genes, such as cystic fibrosis and fragile X syndrome, require sequential screening. Risk stratification plays a crucial role in carrier screening, guiding healthcare providers in offering testing based on an individual's ethnicity and family history. Conditions like Klinefelter syndrome and Turner syndrome are among the chromosomal abnormalities screened for.

Informed consent and genetic counselors are integral components of the screening process, ensuring patients receive accurate information and support. First-trimester screening offers early detection for certain conditions, such as neural tube defects and gestational diabetes. Diagnostic testing, including chromosomal microarray analysis and DNA sequencing, provides confirmatory results when initial screening indicates a potential issue. False positive and false negative rates are essential considerations in the context of data analysis and clinical interpretation. Healthcare providers employ integrated screening strategies, combining biochemical markers and genetic testing, to enhance the accuracy and efficiency of carrier screening. Ethical considerations, including data security, are essential as the volume of genetic data grows.

Dominant genes, like sickle cell anemia and phenylketonuria (PKU), are also screened for, emphasizing the continuous dynamism of this evolving market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Carrier Screening Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

208 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 22.5% |

|

Market growth 2025-2029 |

USD 3.9 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

18.1 |

|

Key countries |

US, Germany, UK, Canada, Japan, France, China, Italy, Spain, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Carrier Screening Market Research and Growth Report?

- CAGR of the Carrier Screening industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the carrier screening market growth of industry companies

We can help! Our analysts can customize this carrier screening market research report to meet your requirements.

RIA -

RIA -