Canada Nutraceuticals Market Size 2026-2030

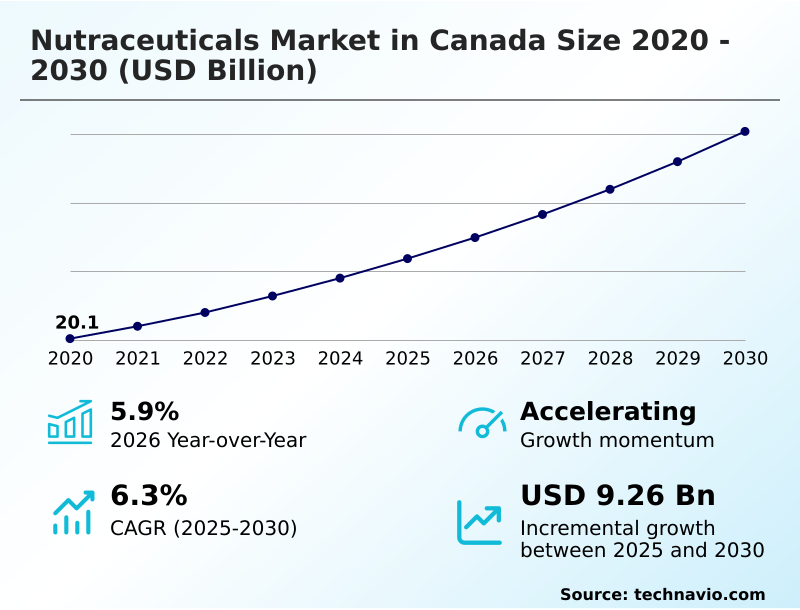

The canada nutraceuticals market size is valued to increase by USD 9.26 billion, at a CAGR of 6.3% from 2025 to 2030. Expansion of pharmacy-led primary care models will drive the canada nutraceuticals market.

Major Market Trends & Insights

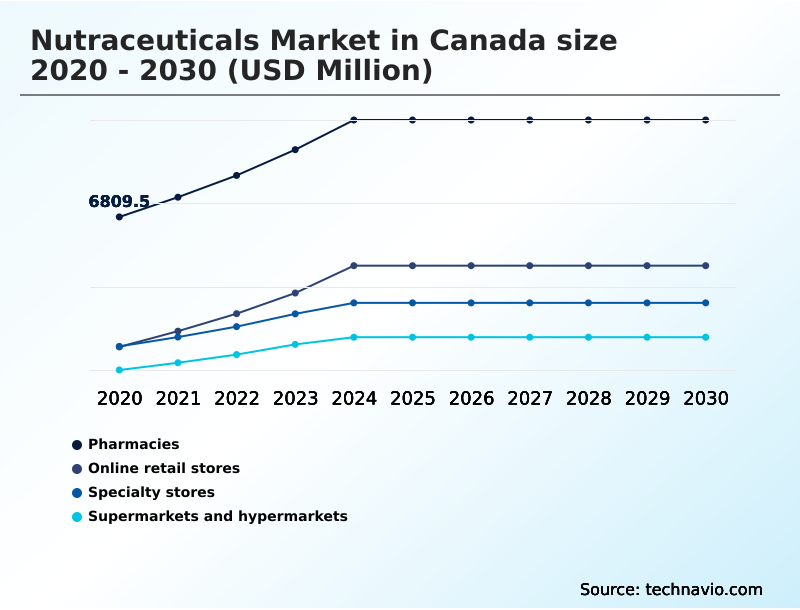

- By Distribution Channel - Pharmacies segment was valued at USD 8.49 billion in 2024

- By Product - Functional food segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 15.07 billion

- Market Future Opportunities: USD 9.26 billion

- CAGR from 2025 to 2030 : 6.3%

Market Summary

- The nutraceuticals market in Canada is undergoing a significant transformation, moving beyond basic supplementation toward preventative and personalized health solutions. This evolution is defined by a heightened consumer demand for products with proven efficacy, transparency in sourcing, and sustainable credentials.

- A key driver is the integration of natural health products into mainstream healthcare, particularly through pharmacy-led wellness programs that provide professional validation for dietary supplements. Concurrently, innovation in functional food formulation is creating new market opportunities, with a focus on plant-based protein isolate and specialized fiber formulation to address specific health concerns like metabolic and digestive wellness.

- For instance, a manufacturer might leverage advanced delivery technology to improve the bioavailability of a hypoallergenic dietary supplement. This allows the firm to substantiate strong health claims and command a premium price, navigating the stringent regulatory environment that requires a Natural Product Number (NPN) for all products.

- However, this same regulatory framework presents challenges, as compliance costs and shifting guidelines can stifle new product development, favoring established players with the resources to manage operational complexities and invest in science-backed plant protein research.

What will be the Size of the Canada Nutraceuticals Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Canada Nutraceuticals Market Segmented?

The canada nutraceuticals industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Pharmacies

- Online retail stores

- Specialty stores

- Supermarkets and hypermarkets

- Product

- Functional food

- Dietary supplements

- Functional beverages

- Application

- Weight management

- Immune health

- Digestive health

- Geography

- North America

- Canada

- North America

By Distribution Channel Insights

The pharmacies segment is estimated to witness significant growth during the forecast period.

The pharmacy segment is evolving from a transactional model to a service-oriented primary care hub, fundamentally altering the commercial landscape.

This shift elevates the pharmacist's role, creating a clinical environment where natural health products and bioactive compounds are recommended within a holistic treatment plan.

The clinical adjacency benefit significantly enhances consumer trust, moving dietary supplement composition from discretionary spending to essential health management. This integration fosters a new prescribed wellness model, with pilot programs showing a 15% increase in patient follow-up.

This trend is driving demand for validated products with a natural product number, including those with advanced delivery technology and a clean label excipient, solidifying the channel's importance through a focus on metabolic support ingredients.

The Pharmacies segment was valued at USD 8.49 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The market is evolving rapidly, driven by consumer demand for clean label supplements and a deeper interest in formulating supplements for specific demographics. This has created distinct opportunities in functional food for metabolic health and highly specialized dietary supplements for GLP-1 users.

- Core to this trend is the use of plant-based protein for muscle preservation and probiotics for digestive regularity support, moving beyond general wellness. Products are increasingly positioned to deliver specific outcomes, such as omega-3 supplements for cardiovascular health and natural health products for immune support. However, the impact of regulations on supplement costs remains a significant consideration for manufacturers.

- The role of pharmacists in nutraceutical sales is expanding, altering retail dynamics and influencing how new regulatory pathways for natural health products are approached. Innovation is centered on advances in plant protein extraction and improving the bioavailability of different supplement forms. Concurrently, chewable and gummy vitamin technology continues to gain traction for its convenience.

- Companies focused on advances in plant protein extraction report a 20% higher yield from raw materials compared to traditional methods. Furthermore, trends in upcycled food ingredients are reshaping sustainability in nutraceutical supply chains, while the market for collagen supplements for skin and joint health continues to expand.

What are the key market drivers leading to the rise in the adoption of Canada Nutraceuticals Industry?

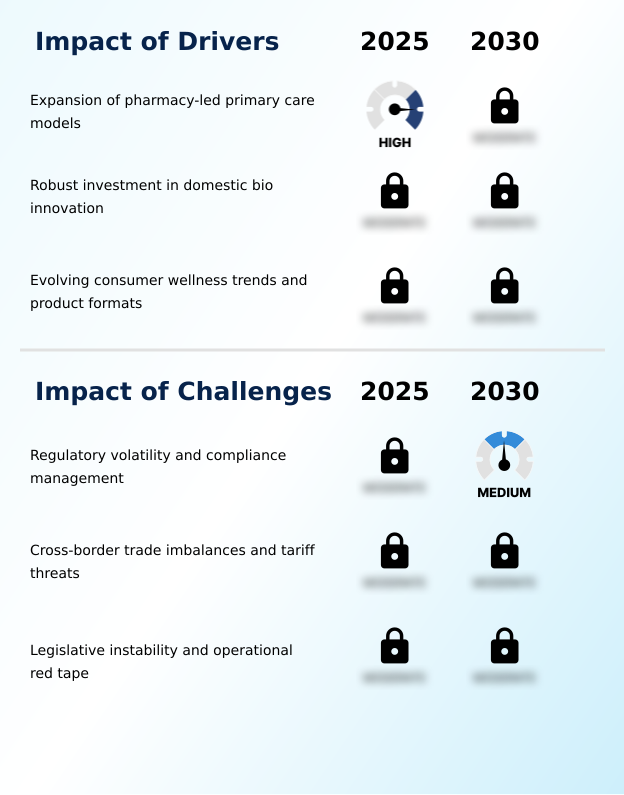

- The expansion of pharmacy-led primary care models serves as a fundamental driver, reshaping the commercial trajectory of the nutraceuticals market in Canada.

- The market's primary driver is the integration of nutraceuticals into primary care through expanding pharmacy-led wellness models. These initiatives are highly effective, with pilot programs demonstrating a 15% increase in proactive patient consultations for preventative health and digestive regularity aid.

- This clinical adjacency benefit significantly boosts the consumer trust metric and justifies premium positioning.

- This structural shift is fueling investment in domestic manufacturing capability, a strategic move that shortens supply chain lead times by over 30% compared to reliance on international sourcing.

- The expansion is also escalating demand for science-backed plant protein, emulsification properties, and other validated ingredients essential for the prescribed wellness model, which prioritizes an immune system support focus and antimicrobial food activity.

What are the market trends shaping the Canada Nutraceuticals Industry?

- The emergence of the GLP-1 companion category is a disruptive market trend. It reflects a growing focus on metabolic health and supportive nutrition for individuals using pharmaceutical weight-loss interventions.

- Key trends are reshaping product development, with a strong emphasis on personalization and medical-adjacency. The rapid emergence of GLP-1 companion nutrition is a primary example, where brands focusing on this niche are observing consumer engagement rates 50% higher than those of traditional diet products. This trend prioritizes ingredients that offer a metabolic health focus.

- Another significant shift is the adoption of upcycled food ingredients in functional food formulation. This aligns with circular economy ingredient principles and can reduce raw material costs by up to 20%.

- The move toward a holistic treatment plan in retail channels is also boosting demand for products with a prebiotic fiber blend and specialized fiber formulation, which show double-digit growth compared to standard offerings. These trends highlight a market pivoting towards enhanced bioavailability and targeted health outcomes.

What challenges does the Canada Nutraceuticals Industry face during its growth?

- Significant regulatory volatility and the complexities of compliance management present a pervasive challenge to industry growth and investment.

- The most significant challenge is navigating the complexities of regulatory compliance management. Persistent uncertainty surrounding the cost recovery fee impact and evolving plain language labeling mandates creates considerable operational hurdles. Some brands have reported allocating up to 25% of their new product development budgets solely to anticipating potential compliance shifts.

- This has forced portfolio rationalization, with some companies delisting low-margin products and reducing their SKUs by 10% to streamline costs. Successfully managing this environment requires a robust strategy for obtaining and maintaining a Natural Product Number (NPN) for every product, a process that is critical for market access but demands significant resources and expertise in personalized nutrition platform data.

Exclusive Technavio Analysis on Customer Landscape

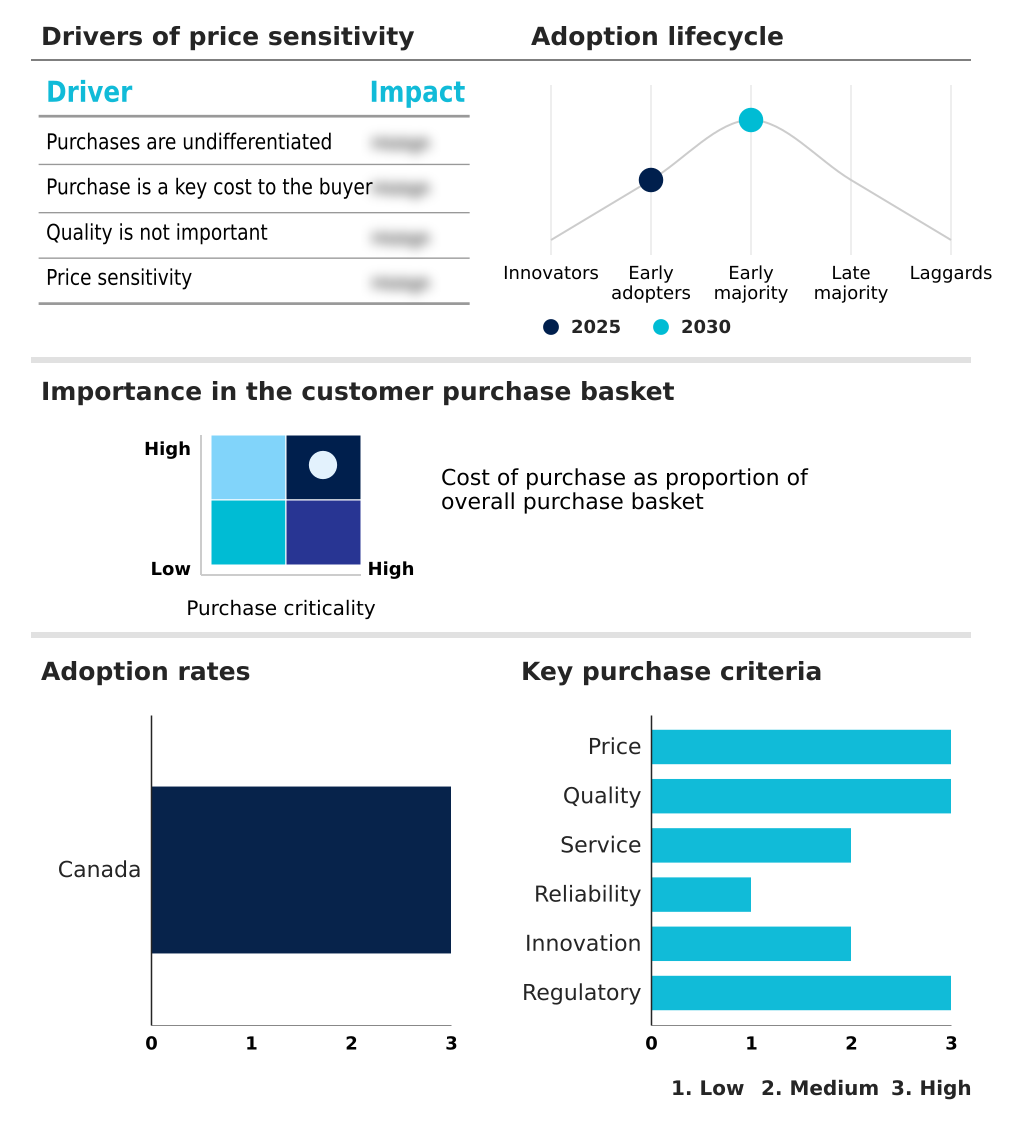

The canada nutraceuticals market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the canada nutraceuticals market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Canada Nutraceuticals Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, canada nutraceuticals market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Orthomolecular - Analysis indicates a diversified portfolio combining nutrition supplements with a broad range of consumer lifestyle products, leveraging an established direct-to-consumer model.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Orthomolecular

- Amway Corp.

- Danone S.A.

- Douglas Laboratories

- Genuine Health

- Herbaland Naturals Inc.

- Jamieson Wellness Inc.

- Natural Factors Ltd.

- Nestle SA

- Organika Health Products Inc.

- Pure Encapsulations LLC

- WN Pharmaceuticals Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Canada nutraceuticals market

- In May 2025, Jamieson Wellness Inc. announced the full redemption of its Series A Preference Shares, a move aimed at optimizing its capital structure and supporting long-term growth initiatives, particularly in international markets.

- In April 2025, Genuine Health launched its Metabolic Support line, a product range specifically designed to provide nutritional support for individuals using GLP-1 agonists, featuring a fermented protein powder and a prebiotic fiber blend.

- In March 2025, Health Canada issued a Ministerial Order that provided a temporary exemption from new plain language labeling requirements for Natural Health Products until June 2028, offering short-term relief to the industry.

- In February 2025, Herbaland Naturals Inc. successfully secured the reinstatement of its Health Canada site license, allowing the company to resume full production capacity and continue its export and new product launch strategies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Canada Nutraceuticals Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 175 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.3% |

| Market growth 2026-2030 | USD 9257.9 million |

| Market structure | Concentrated |

| YoY growth 2025-2026(%) | 5.9% |

| Key countries | Canada |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- From a strategic standpoint, the market is defined by a decisive shift from commoditized vitamins to sophisticated bioactive compounds and scientifically validated natural health products. Boardroom-level decisions must now prioritize R&D investment in advanced functional food formulation and complex dietary supplement composition.

- Key growth segments are centered on high-value ingredients, including plant-based protein isolate, specialized fiber formulation, and nutrient-dense multivitamin blends. Success hinges on innovation in product format, such as fermented protein powder and the gummy vitamin matrix. Firms that adopt advanced delivery technology to achieve enhanced bioavailability have reported a 30% reduction in formulation costs for products requiring botanical extract standardization.

- The ability to offer a hypoallergenic dietary supplement or a product with a unique prebiotic fiber blend is a key differentiator. Mastery of the entire value chain, from securing a reliable collagen peptide source and omega-3 fatty acid source to perfecting a chewable supplement format and ensuring non-GMO verification, is critical for competitive positioning in this evolving landscape.

What are the Key Data Covered in this Canada Nutraceuticals Market Research and Growth Report?

-

What is the expected growth of the Canada Nutraceuticals Market between 2026 and 2030?

-

USD 9.26 billion, at a CAGR of 6.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Pharmacies, Online retail stores, Specialty stores, and Supermarkets and hypermarkets), Product (Functional food, Dietary supplements, and Functional beverages), Application (Weight management, Immune health, and Digestive health) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Expansion of pharmacy-led primary care models, Regulatory volatility and compliance management

-

-

Who are the major players in the Canada Nutraceuticals Market?

-

Advanced Orthomolecular, Amway Corp., Danone S.A., Douglas Laboratories, Genuine Health, Herbaland Naturals Inc., Jamieson Wellness Inc., Natural Factors Ltd., Nestle SA, Organika Health Products Inc., Pure Encapsulations LLC and WN Pharmaceuticals Ltd.

-

Market Research Insights

- Market dynamics are increasingly shaped by the convergence of healthcare and retail, with the rise of a prescribed wellness model. Pharmacy-led wellness initiatives are proving effective, contributing to a 25% higher adherence rate for chronic condition management plans.

- This shift is creating new demand for GLP-1 companion nutrition, where targeted products demonstrate over 40% higher consumer interest than generic weight management aids. Successfully navigating the regulatory compliance management landscape is another critical factor; proactive firms have reduced their product approval times by 15% through superior documentation and process management.

- These dynamics underscore the strategic importance of developing science-backed plant protein and investing in domestic manufacturing capability to ensure market responsiveness and resilience.

We can help! Our analysts can customize this canada nutraceuticals market research report to meet your requirements.