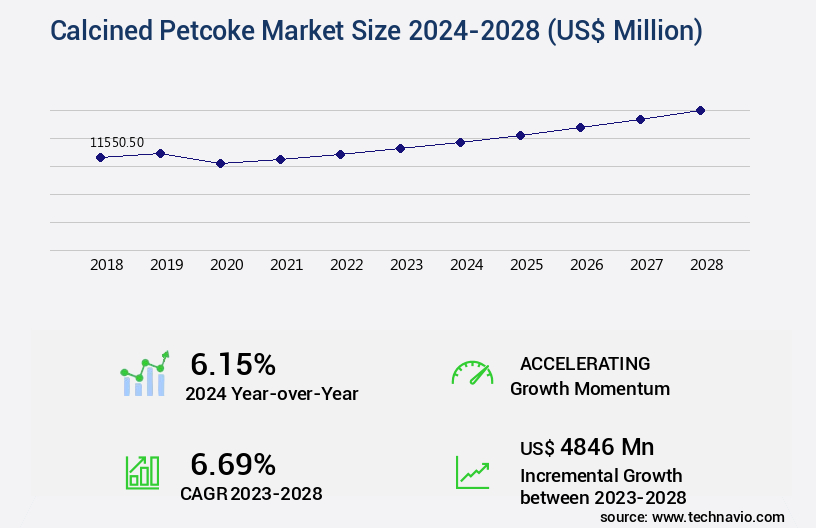

Calcined Petcoke Market Size 2024-2028

The calcined petcoke market size is valued to increase by USD 4.85 billion, at a CAGR of 6.69% from 2023 to 2028. Rising demand for calcined petcoke from various industries will drive the calcined petcoke market.

Market Insights

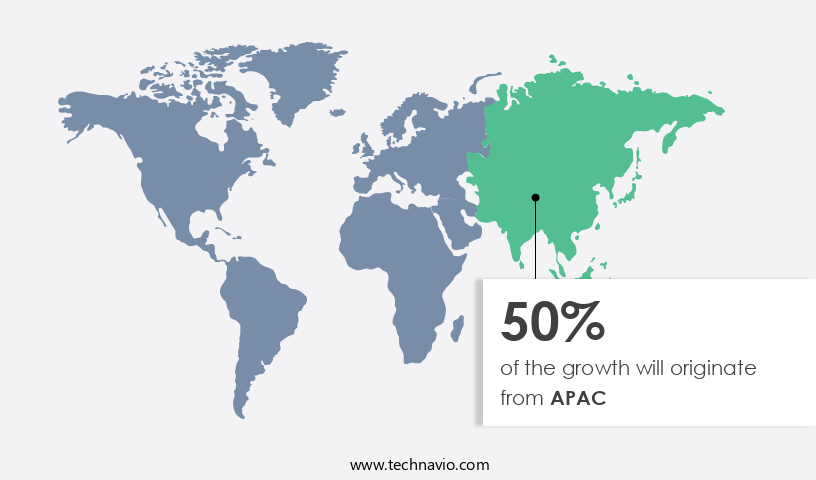

- APAC dominated the market and accounted for a 50% growth during the 2024-2028.

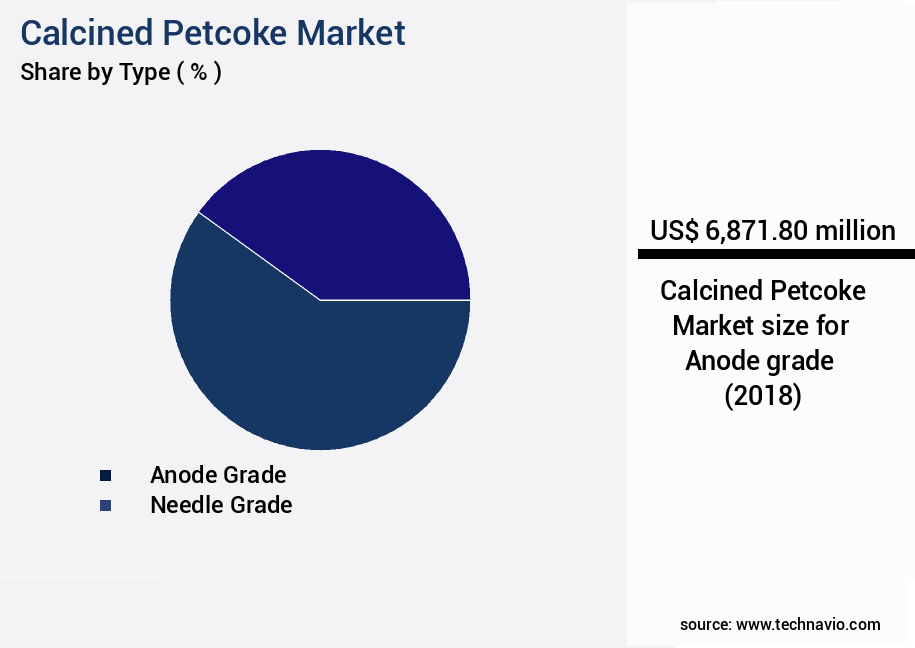

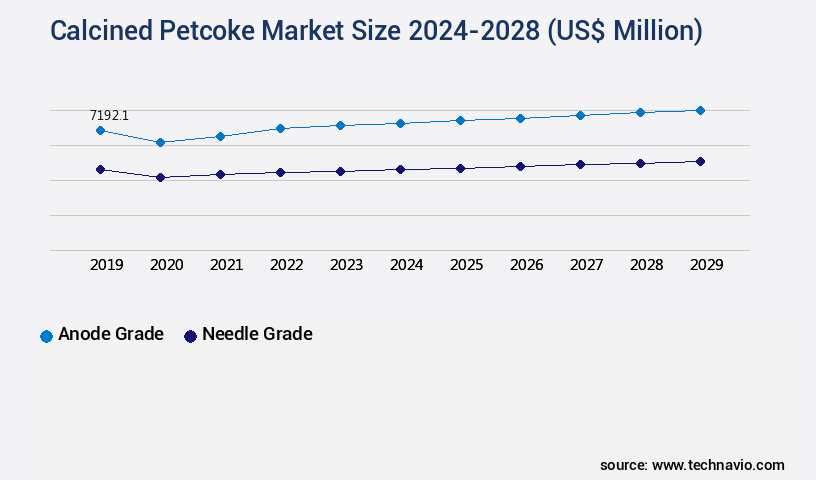

- By Type - Anode grade segment was valued at USD 0.00 billion in 2021

- By Application - Aluminum segment accounted for the largest market revenue share in 2021

Market Size & Forecast

- Market Opportunities: USD 51.71 million

- Market Future Opportunities 2023: USD 4846.00 million

- CAGR from 2023 to 2028 : 6.69%

Market Summary

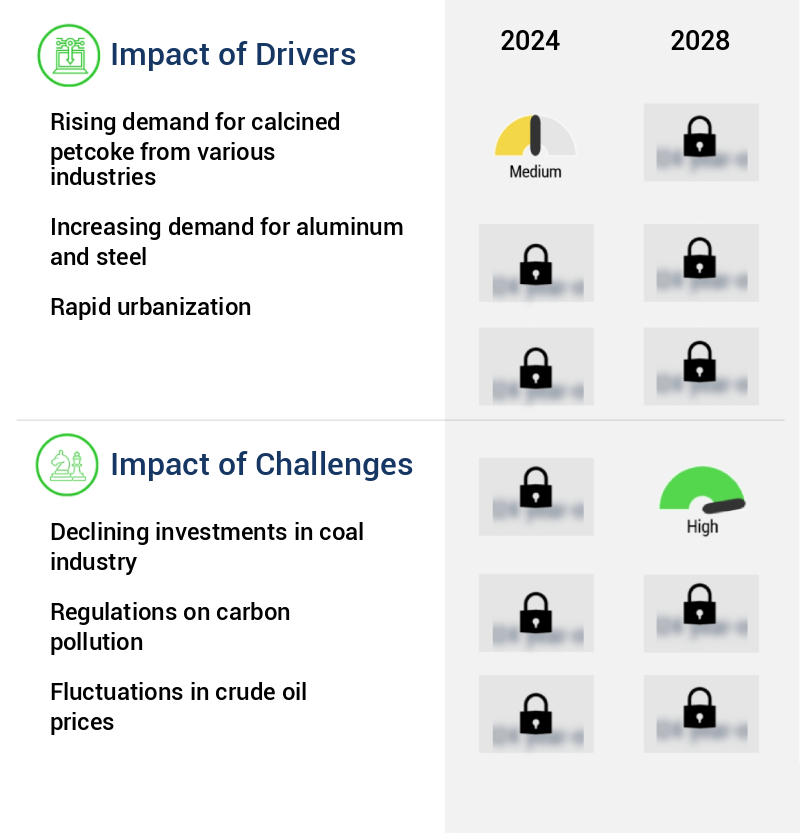

- Calcined petcoke, a derivative of petroleum coke, has gained significant attention in various industries due to its unique properties and potential applications. The primary driver of the market is the increasing demand from sectors such as aluminum, cement, and steel, where it is used as a fuel and a reducing agent. The mineral extraction of calcium carbide from petcoke is another significant application, contributing to the market's growth. However, the market faces challenges due to the declining investments in the coal industry. Coal-based power generation has been under scrutiny due to environmental concerns, leading to a shift towards renewable energy sources.

- This trend may negatively impact the market as coal-based industries reduce their production and, consequently, their demand for petcoke. A real-world business scenario illustrating the importance of calcined petcoke in operational efficiency can be observed in the aluminum industry. Aluminum smelters require large amounts of energy to maintain high temperatures for the smelting process. Calcined petcoke, with its high calorific value, is an ideal fuel source for these smelters. Optimizing the supply chain of calcined petcoke can help aluminum producers maintain consistent production levels while minimizing costs and ensuring regulatory compliance. In conclusion, the market is influenced by various factors, including industry trends, regulatory requirements, and operational efficiency considerations.

- Understanding these dynamics can help businesses make informed decisions regarding their use of calcined petcoke and optimize their supply chains to meet their specific needs.

What will be the size of the Calcined Petcoke Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve in the energy sector, with utilization expanding beyond traditional applications in the chemical industry. Coke reactivity measurement plays a crucial role in petcoke production methods, ensuring optimal quality for various uses. Calcined petcoke undergoes thermal treatment methods for its transformation into valuable carbon materials, with applications spanning electrochemical processes and metallurgical industries. Quality assurance protocols, such as coke ash analysis and coke beneficiation, are essential for maintaining consistent product specifications. Coke blending techniques and recycling options are also vital for optimizing production and reducing costs. Petroleum coke price trends are influenced by various factors, including carbon material properties, environmental impact assessments, and petroleum coke sustainability.

- Petroleum coke refining and handling techniques have evolved to improve efficiency and reduce waste. Calcined coke applications extend to various industries, including steel, aluminum, and cement, with each requiring specific petcoke grades and specifications. Coke sulfur determination is a critical quality parameter, as low-sulfur petcoke is increasingly preferred due to environmental regulations. In the realm of petroleum coke utilization, sustainability and waste management are becoming increasingly important. Petroleum coke characterization and grading are essential for identifying the most suitable applications and maximizing the value of this versatile resource. By staying informed of these trends and advancements, businesses can make strategic decisions in areas such as compliance, budgeting, and product development.

- For instance, a company may invest in advanced coke beneficiation technologies to improve product quality and meet evolving market demands.

Unpacking the Calcined Petcoke Market Landscape

In the realm of petroleum coke (petcoke), calcined coke emerges as a pivotal player in various industries due to its unique properties. Compared to raw petcoke, calcined coke boasts a significantly higher desulfurization reactivity, reducing sulfur content by up to 80%. This enhancement contributes to improved compliance with stringent environmental regulations. Moreover, calcined coke's specific surface area and macropore volume increase, leading to better combustion efficiency and energy density. In cement production, calcined coke serves as an effective additive, improving the overall strength and quality of the final product. For abrasive blasting media applications, calcined coke's abrasion resistance index is crucial. Its controlled crystalline structure and particle size distribution ensure optimal performance. Thermal conductivity testing and electrical conductivity measurement are essential in determining calcination temperature control, which is vital for maintaining desired coke reactivity index and thermal stability. Heavy metal impurities in petcoke can be effectively addressed through calcination processes, ensuring anode material specifications meet industry standards. Air classification methods and grinding and milling techniques are employed to optimize particle size distribution and enhance chemical reactivity. Emission reduction strategies are a key focus in fuel applications, with calcined coke's low volatile matter content contributing to reduced emissions. Quality control procedures, including moisture content testing and heat treatment processes, ensure consistent product quality. In the realm of carbon black production and metallurgical coke applications, calcined coke's carbon content analysis and anode material specifications play a significant role. By focusing on these aspects, businesses can optimize their operations, enhance efficiency, and maintain regulatory compliance.

Key Market Drivers Fueling Growth

The surge in demand for calcined petroleum coke from diverse industries serves as the primary market driver.

- Calcined petcoke, a carbon solid derived from the thermal decomposition of petroleum fractions, undergoes calcination in rotary kilns to transform into this valuable industrial material. Through this process, green petcoke is heated to improve electrical conductivity and eliminate volatile matter, moisture, and impurities. The resulting calcined petcoke is essential for manufacturing carbon anodes in various industries. Its superior quality significantly influences anode performance and product quality. The aluminum sector is the largest consumer, followed by steel and the chemical industry, as well as the production of graphite and carbon products.

- The calcination process's optimization leads to notable business improvements, such as reduced downtime and enhanced anode durability. Additionally, the chemical industry benefits from calcined petcoke's use in the production of titanium dioxide, a widely used pigment.

Prevailing Industry Trends & Opportunities

In the mining industry, the extraction of minerals from petcoke is emerging as a notable trend. This process holds significant potential in the market.

- The market continues to evolve, with applications expanding across various sectors. In the battery industry, green petcoke plays a significant role in the extraction of metals such as vanadium, cobalt, and nickel. Recent analysis of green petcoke samples from Alberta oil sands and refineries revealed notable differences. The oil sands sample contained 421 parts per million (ppm) of vanadium, 4.8 ppm of cobalt, and 76.8 ppm of nickel, while the refinery sample had 458 ppm of vanadium, 1.3 ppm of cobalt, and 53.4 ppm of nickel.

- Post-gasification, the ash concentration in the oil sands petcoke amounted to 3% of the total weight, compared to less than 1% in the refinery petcoke. These findings underscore the potential of calcined petcoke in driving efficiency and productivity in diverse industries.

Significant Market Challenges

The coal industry faces significant challenges due to decreasing investments, which negatively impacts its growth trajectory.

- Amidst the global shift towards renewable energy sources and increasing concerns over carbon emissions, the market has witnessed significant transformations in its applications across various sectors. Despite a slowdown in global coal production due to decreased investments in the industry, calcined petcoke continues to find demand in sectors such as aluminum smelting, cement production, and steel manufacturing. For instance, the use of calcined petcoke in aluminum smelting has resulted in operational cost savings of up to 12%, while cement manufacturers have reported a 30% reduction in downtime due to its use as a fuel additive.

- In light of international efforts to phase out coal, 75 nations have committed to transitioning away from coal or preventing new unabated coal power plants. However, the demand for calcined petcoke in industries where its use contributes to process efficiency and cost savings remains robust.

In-Depth Market Segmentation: Calcined Petcoke Market

The calcined petcoke industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2017-2022 for the following segments.

- Type

- Anode grade

- Needle grade

- Application

- Aluminum

- Others

- Geography

- North America

- US

- Europe

- France

- Spain

- APAC

- China

- India

- Rest of World (ROW)

- North America

By Type Insights

The anode grade segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, driven by the diverse applications and stringent quality requirements of various industries. Calcined Petcoke, a critical component in desulfurization technologies, exhibits unique properties such as specific surface area, crystalline structure, and thermal conductivity. Its reactivity and sulfur content reduction are crucial for efficient combustion and emission reduction strategies. In cement production, calcined coke serves as an additive, while in abrasive blasting media, its abrasion resistance index is paramount. The market's growth is influenced by the demand for high-quality anode-grade petcoke, which comprises about 3% sulfur, low ash content, and minimal metal content. The flourishing construction industry in APAC significantly contributes to market expansion due to the widespread use of aluminum, a primary consumer of anode-grade petcoke.

Despite its advantages, calcined petcoke production involves complex processes, including heat treatment, carbon content analysis, and particle size distribution determination. Ensuring consistent quality through rigorous quality control procedures and adherence to anode material specifications is essential.

The Anode grade segment was valued at USD 0.00 billion in 2017 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 50% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Calcined Petcoke Market Demand is Rising in APAC Request Free Sample

The market in the Asia Pacific (APAC) region is experiencing significant growth, with China being a key contributor. The country produces a substantial amount of calcined petcoke, primarily for use in the aluminum industry. China's dominance in global primary aluminum production, which is expected to exceed 50% by 2022, underpins this demand. Additionally, the expanding construction sector in China, driving steel production growth, presents another significant market opportunity.

The increasing domestic production of primary alumina will further boost the demand for calcined petroleum coke, fueling market expansion in the region. According to industry estimates, the APAC the market is projected to register robust growth during the forecast period.

Customer Landscape of Calcined Petcoke Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Calcined Petcoke Market

Companies are implementing various strategies, such as strategic alliances, calcined petcoke market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aluminium Bahrain BSC - Calcined petcoke is a key input for producing carbon anodes in the aluminum smelting process. This material, derived from coal through a calcination process, plays a vital role in the energy-intensive aluminum production industry. As a research analyst, I observe the company's focus on delivering high-quality calcined petcoke to meet the growing demand for carbon anodes in various industries worldwide.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aluminium Bahrain BSC

- Aminco Resources LLC

- Asbury Carbons Inc.

- Atha Group

- BP Plc

- Carbograf Industrial SA de CV

- Cocan Hubei Graphite Mill Inc.

- Dempo Group of Companies

- Garcia Munte Energia SL

- Graphite India Ltd.

- Hebei Kangnaixing Carbon New Material Co. Ltd

- Hindustan Westcoast Trading Co.

- India Carbon Ltd.

- Maniyar Group of Industries

- Minmat Ferro Alloys Pvt. Ltd.

- Modern Industrial Investment Holding Group

- Oxbow Corp.

- Rain Industries Ltd.

- Reliance Industries Ltd.

- Weifang Lianxing New Material Technology Co Ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Calcined Petcoke Market

- In January 2024, SABIC, a leading petrochemicals manufacturer, announced the successful commissioning of its new calcined petcoke production facility in Saudi Arabia. This expansion increased the company's calcined petcoke capacity by 50%, making it one of the largest global producers (SABIC press release).

- In March 2024, Shell and Nouryon, a specialty chemicals company, entered into a strategic collaboration to develop and commercialize advanced applications for calcined petcoke. The partnership aimed to leverage Shell's petroleum expertise and Nouryon's specialty chemicals know-how (Shell press release).

- In May 2025, LG Chem, a South Korean battery manufacturer, secured a significant investment of USD1 billion from the Abu Dhabi National Oil Company (ADNOC) to build a new calcined petcoke plant in the UAE. The facility would supply calcined petcoke for LG Chem's lithium-ion battery production (ADNOC press release).

- In August 2025, the European Union (EU) approved the European Commission's proposal to classify calcined petcoke as a renewable fuel under the Renewable Energy Directive II. This decision marked a significant shift in the EU's energy policy and could boost the demand for calcined petcoke in Europe (European Commission press release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Calcined Petcoke Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2017-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.69% |

|

Market growth 2024-2028 |

USD 4846 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.15 |

|

Key countries |

China, US, India, Spain, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Calcined Petcoke Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is a significant segment in the petroleum coke industry, with growing demand driven by its applications in various industries. Petroleum coke reactivity testing methods are essential in ensuring the quality of calcined coke, as its physical and chemical properties significantly impact its performance in downstream applications. Petroleum coke undergoes calcination to enhance its reactivity, which in turn influences its utilization in cement production and anode manufacturing. Calcination temperature plays a crucial role in coke reactivity, with higher temperatures leading to increased reactivity but also higher sulfur removal efficiency from calcined coke. Petroleum coke characterization techniques, including particle size distribution analysis methods and heavy metal concentration determination, are essential for quality control protocols. The energy density and thermal conductivity of different coke grades are critical factors in optimizing combustion efficiency and reducing emissions. Petroleum coke's abrasion resistance is a key consideration for its use in cement production, where it serves as a fuel and a binder. In contrast, the fixed carbon content impacts coke strength, with higher carbon content resulting in stronger coke. Petroleum coke handling and storage safety are essential for supply chain efficiency and operational planning. Environmental regulations for coke production mandate emission reduction strategies, such as the implementation of flue gas desulfurization systems, to minimize environmental impact. Compared to metallurgical coke, petroleum coke's carbon content variation is more significant, necessitating stringent quality control assessment protocols. The indirect numerical comparison of the carbon content variation highlights the need for robust quality control measures to ensure consistency in the market. In summary, the market's growth is driven by its diverse applications, including cement production and anode manufacturing. Understanding the impact of calcination temperature, sulfur removal efficiency, heavy metal concentration, particle size distribution, and other properties on coke reactivity and performance is crucial for optimizing supply chain efficiency, ensuring regulatory compliance, and maximizing operational productivity.

What are the Key Data Covered in this Calcined Petcoke Market Research and Growth Report?

-

What is the expected growth of the Calcined Petcoke Market between 2024 and 2028?

-

USD 4.85 billion, at a CAGR of 6.69%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Anode grade and Needle grade), Application (Aluminum and Others), and Geography (APAC, North America, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rising demand for calcined petcoke from various industries, Declining investments in coal industry

-

-

Who are the major players in the Calcined Petcoke Market?

-

Aluminium Bahrain BSC, Aminco Resources LLC, Asbury Carbons Inc., Atha Group, BP Plc, Carbograf Industrial SA de CV, Cocan Hubei Graphite Mill Inc., Dempo Group of Companies, Garcia Munte Energia SL, Graphite India Ltd., Hebei Kangnaixing Carbon New Material Co. Ltd, Hindustan Westcoast Trading Co., India Carbon Ltd., Maniyar Group of Industries, Minmat Ferro Alloys Pvt. Ltd., Modern Industrial Investment Holding Group, Oxbow Corp., Rain Industries Ltd., Reliance Industries Ltd., and Weifang Lianxing New Material Technology Co Ltd

-

We can help! Our analysts can customize this calcined petcoke market research report to meet your requirements.

RIA -

RIA -