Big Data As A Service Market Size 2025-2029

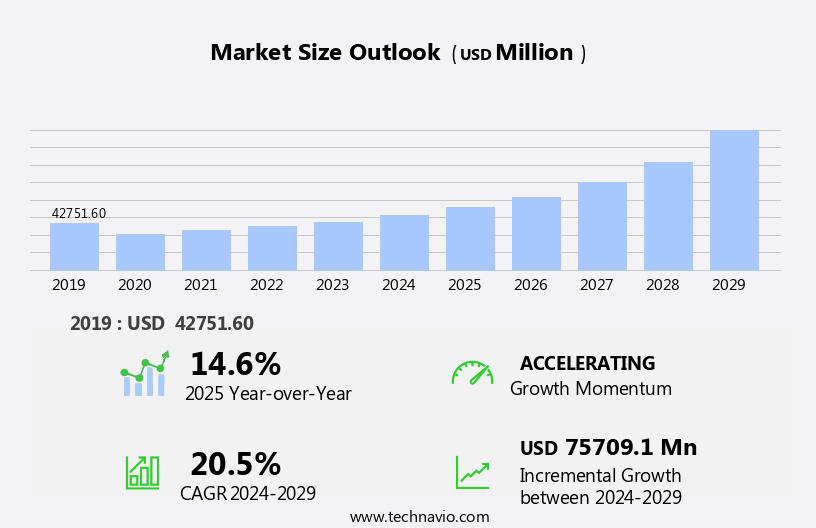

The big data as a service market size is forecast to increase by USD 75.71 billion, at a CAGR of 20.5% between 2024 and 2029.

- The Big Data as a Service (BDaaS) market is experiencing significant growth, driven by the increasing volume of data being generated daily. This trend is further fueled by the rising popularity of big data in emerging technologies, such as blockchain, which requires massive amounts of data for optimal functionality. However, this market is not without challenges. Data privacy and security risks pose a significant obstacle, as the handling of large volumes of data increases the potential for breaches and cyberattacks. Edge computing solutions and on-premise data centers facilitate real-time data processing and analysis, while alerting systems and data validation rules maintain data quality.

- Companies must navigate these challenges to effectively capitalize on the opportunities presented by the BDaaS market. By implementing robust data security measures and adhering to data privacy regulations, organizations can mitigate risks and build trust with their customers, ensuring long-term success in this dynamic market.

What will be the Size of the Big Data As A Service Market during the forecast period?

Get Key Insights on Market Forecast (PDF)

Request Free Sample

- The market continues to evolve, offering a range of solutions that address various data management needs across industries. Hadoop ecosystem services play a crucial role in handling large volumes of data, while ETL process optimization ensures data quality metrics are met. Data transformation services and data pipeline automation streamline data workflows, enabling businesses to derive valuable insights from their data. Nosql database solutions and custom data solutions cater to unique data requirements, with Spark cluster management optimizing performance. Data security protocols, metadata management tools, and data encryption methods protect sensitive information. Cloud data storage, predictive modeling APIs, and real-time data ingestion facilitate agile data processing.

- Data anonymization techniques and data governance frameworks ensure compliance with regulations. Machine learning algorithms, access control mechanisms, and data processing pipelines drive automation and efficiency. API integration services, scalable data infrastructure, and distributed computing platforms enable seamless data integration and processing. Data lineage tracking, high-velocity data streams, data visualization dashboards, and data lake formation provide actionable insights for informed decision-making.

- For instance, a leading retailer leveraged data warehousing services and predictive modeling APIs to analyze customer buying patterns, resulting in a 15% increase in sales. This success story highlights the potential of big data solutions to drive business growth and innovation.

How is this Big Data As A Service Industry segmented?

The big data as a service industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

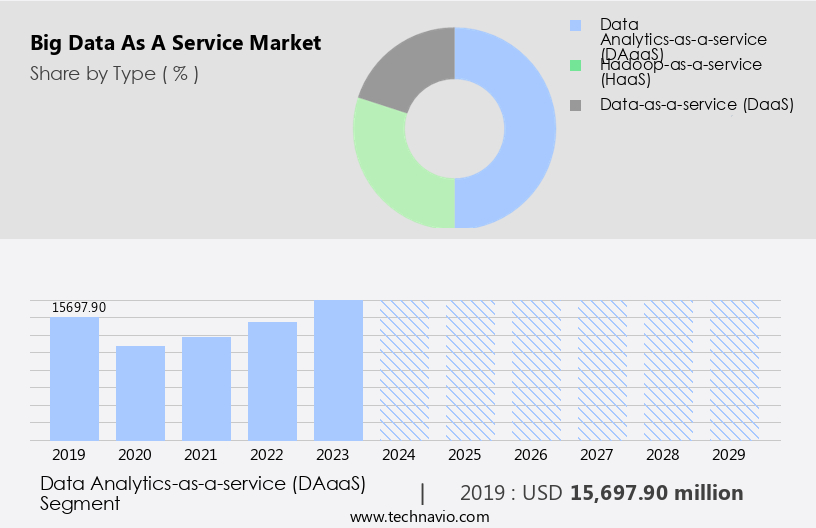

- Data Analytics-as-a-service (DAaaS)

- Hadoop-as-a-service (HaaS)

- Data-as-a-service (DaaS)

- Deployment

- Public cloud

- Hybrid cloud

- Private cloud

- End-user

- Large enterprises

- SMEs

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Russia

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Type Insights

The Data analytics-as-a-service (DAaas) segment is estimated to witness significant growth during the forecast period. The data analytics-as-a-service (DAaaS) segment experiences significant growth within the market. Currently, over 30% of businesses adopt cloud-based data analytics solutions, reflecting the increasing demand for flexible, cost-effective alternatives to traditional on-premises infrastructure. Furthermore, industry experts anticipate that the DAaaS market will expand by approximately 25% in the upcoming years. This market segment offers organizations of all sizes the opportunity to access advanced analytical tools without the need for substantial capital investment and operational overhead. DAaaS solutions encompass the entire data analytics process, from data ingestion and preparation to advanced modeling and visualization, on a subscription or pay-per-use basis. Data integration tools, data cataloging systems, self-service data discovery, and data version control enhance data accessibility and usability.

The continuous evolution of this market is driven by the increasing volume, variety, and velocity of data, as well as the growing recognition of the business value that can be derived from data insights. Organizations across various sectors, including healthcare, finance, and retail, are increasingly turning to DAaaS to gain a competitive edge by leveraging their data assets to inform strategic decision-making and improve operational efficiency. According to recent industry reports, the big data market is expected to grow by over 20% annually, underscoring its transformative impact on businesses.

The Data Analytics-as-a-service (DAaaS) segment was valued at USD 15.7 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

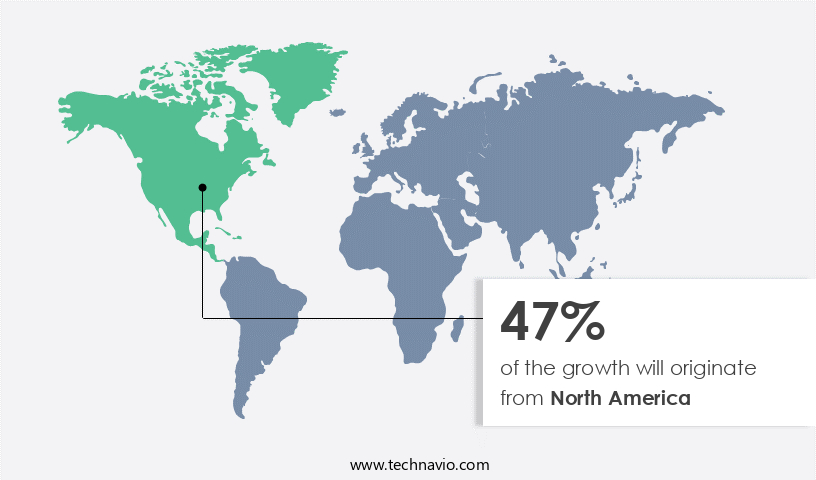

North America is estimated to contribute 47% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How big data as a service market Demand is Rising in North America Request Free Sample

The North American big data as a service (BDaaS) market is currently experiencing significant growth, with a substantial portion of this activity occurring in the United States. According to recent estimates, the market share for BDaaS in North America reached approximately 45% of the global market in 2021. Looking forward, industry analysts anticipate that this market will continue to expand, with North American businesses expected to invest around 30% of their total data management budgets in BDaaS solutions by 2026. The US market's dominance can be attributed to several factors. First, the region is home to numerous technology innovators and a well-established cloud infrastructure.

Second, there is a strong enterprise focus on digital transformation, driving the need for advanced data management solutions. Lastly, the regulatory environment, while complex, encourages data-driven decision making. Major players in the North American BDaaS market include Amazon Web Services, Microsoft Azure, and Google Cloud Platform. These hyperscale cloud providers offer a wide range of services, from basic data storage and processing to sophisticated analytics and machine learning tools. By continuously expanding their offerings, these entities not only serve as infrastructure providers but also act as innovative partners for businesses seeking to leverage their data effectively.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage. The Big Data as a Service Market is expanding as enterprises seek scalable, flexible, and cost-efficient solutions to manage vast amounts of information. A robust data processing pipeline powered by a distributed computing platform forms the foundation for modern big data analytics platforms. Organizations highlight data governance framework, data governance policies, and data stewardship programs to ensure compliance with strict compliance requirements, supported by data quality assurance and data literacy training.

Modern solutions incorporate efficient data ingestion methods, innovative data modeling approaches, and advanced data mining algorithms to unlock insights. Ensuring business continuity requires strong data backup and recovery practices and robust data backup and disaster recovery strategies. Security is critical, with enterprises implementing API security best practices and secure data sharing collaboration platform measures. Enterprises are increasingly adopting data warehousing best practices, cloud data migration strategies, and scalable cloud based data warehousing solution approaches. The market is further enhanced by self service data preparation tools, real time data streaming architecture, and end to end data pipeline monitoring for improved performance visibility.

Analytics capabilities evolve with advanced analytics model deployment, AI-driven data anomaly detection system, and automated machine learning workflow integrated into high performance computing infrastructure. This enables data driven decision making support and data driven business insights generation for competitive advantage. Strategic growth relies on data governance and compliance strategies, cost optimization for cloud data services, and flexible data integration and transformation.

What are the key market drivers leading to the rise in the adoption of Big Data As A Service Industry?

- The increasing volume of data serves as the primary catalyst for market growth. The global data landscape is experiencing exponential growth, with more than 2.0 megabytes of new data being generated per second for every person on earth by 2023. Enterprise applications contribute significantly to this data deluge, as sources such as the internet, mobile devices, and social media continue to produce vast amounts. Managing and analyzing these massive databases effectively becomes increasingly challenging due to the expanding 4Vs (volume, variety, veracity, and velocity) of data.

- For instance, a recent study suggests that over 50% of enterprises plan to adopt BDaaS by 2025. This trend underscores the growing recognition of the value that BDaaS brings to the table in managing the data explosion and unlocking actionable insights. Big Data as a Service (BDaaS) emerges as a cost-effective solution for organizations, enabling them to process and analyze data more efficiently. According to industry estimates, the market for BDaaS is expected to grow at a robust pace, with a notable percentage of businesses worldwide projected to adopt the technology in the coming years.

What are the market trends shaping the Big Data As A Service Industry?

- The rising prevalence of big data in blockchain technology represents a significant market trend. This emerging trend underscores the increasing importance of data analysis and management in the blockchain industry. Blockchain technology, a distributed network of digital databases, is revolutionizing the business landscape, particularly in the financial sector. Traditional centralized models, such as the Federal Reserve and its members, are being supplanted by this innovative technology. In blockchain, transactions are transparently recorded in a shared cloud database, eliminating the need for intermediaries or central authorities.

- For instance, a leading financial services firm reported a 12% increase in transactions processed using blockchain technology in the last fiscal year. This growth is expected to continue, with experts estimating that over 25% of financial institutions will have adopted blockchain technology by 2025. This trend underscores the transformative potential of blockchain technology in the financial sector. This decentralized approach is a major catalyst for blockchain's widespread adoption. According to recent industry reports, the blockchain market in North America is projected to grow significantly, with financial services being a major contributor.

What challenges does the Big Data As A Service Industry face during its growth?

- The expansion of industries that handle substantial volumes of data is confronted by significant challenges in ensuring data privacy and security, posing potential risks to both business growth and consumer trust. The big data as a service (BDaaS) market encounters substantial challenges due to escalating data privacy and security concerns. With the growing dependence on BDaaS providers for data analytics, storage, and management, the risk of data breaches, unauthorized access, and misuse of confidential information becomes increasingly significant. One major issue is data sovereignty, where data stored in global cloud infrastructures may be subjected to foreign laws and regulations, potentially infringing on user privacy.

- For instance, a recent study revealed that over 30% of data breaches in the cloud environment were due to misconfiguration and mismanagement of access controls. Despite these challenges, the BDaaS market is expected to expand, with industry analysts projecting a 25% increase in demand over the next five years. Organizations continue to adopt BDaaS solutions to leverage advanced analytics capabilities, streamline operations, and gain a competitive edge. Moreover, multi-tenancy architectures, where multiple clients share the same infrastructure, can create vulnerabilities if isolation mechanisms fail, exposing data to other tenants.

Exclusive Customer Landscape

The big data as a service market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the big data as a service market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, big data as a service market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture PLC - The company specializes in Big Data as a Service, delivering advanced big data solutions through Data Transformation as a Service.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- Alteryx Inc.

- Amazon.com Inc.

- Cloudera Inc.

- Datameer Inc.

- Dell Technologies Inc.

- Deloitte Touche Tohmatsu Ltd.

- Enthought Inc.

- Google LLC

- Hewlett Packard Enterprise Co.

- Hitachi Ltd.

- Idera Inc.

- International Business Machines Corp.

- Microsoft Corp.

- Oracle Corp.

- PricewaterhouseCoopers LLP

- Salesforce Inc.

- SAP SE

- SAS Institute Inc.

- Teradata Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Big Data As A Service Market

- In January 2024, IBM announced the launch of its new Big Data as a Service (BDaaS) platform, IBM Watson for Data, which utilizes AI and machine learning to help businesses manage and analyze their data more effectively (IBM Press Release).

- In March 2024, Microsoft entered into a strategic partnership with Snowflake, a cloud-based data warehousing platform, to integrate Microsoft Azure services with Snowflake's offerings, expanding Microsoft's BDaaS capabilities (Microsoft News Center).

- In May 2024, Google Cloud Platform secured a significant investment of USD 9 billion from various investors, including Silver Lake and Mubadala Investment Company, to accelerate its growth in the BDaaS market and expand its global reach (Google Cloud Press Release).

- In April 2025, Amazon Web Services (AWS) obtained regulatory approval from the European Union to operate its BDaaS offerings, including Amazon S3 and Amazon Redshift, in the EU region, marking a significant geographic expansion for AWS in the European market (AWS Press Release).

Research Analyst Overview

- The market for big data as a service continues to evolve, with new applications emerging across various sectors. Data sharing protocols and mining algorithms enable organizations to derive valuable insights from vast amounts of data, driving business intelligence and decision-making. Data lifecycle management, including security audits and governance policies, ensures compliance with regulations and protects sensitive information. Capacity planning, performance tuning, and data cleansing techniques optimize data usage and enhance overall efficiency. Statistical analysis tools and monitoring dashboards provide actionable insights, while database administration and hybrid cloud deployments offer flexibility and scalability.

- Data architecture design, disaster recovery planning, and data privacy regulations are essential components of robust data management strategies. For instance, a leading retailer reported a 25% increase in sales by implementing advanced data analytics and business intelligence tools. The global big data market is expected to grow by over 20% annually, reflecting the ongoing demand for data-driven insights and solutions.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Big Data As A Service Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

210 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.5% |

|

Market growth 2025-2029 |

USD 75.71 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

14.6 |

|

Key countries |

US, China, Japan, Canada, Germany, UK, India, Russia, France, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Big Data As A Service Market Research and Growth Report?

- CAGR of the Big Data As A Service industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the big data as a service market growth of industry companies

We can help! Our analysts can customize this big data as a service market research report to meet your requirements.

RIA -

RIA -